How Much Can an Opera Vocal Training Studio Owner Make? $85k to $133M

An opera vocal training studio owner’s income depends on whether the owner takes only the modeled $85,000 Director and Lead Vocal Coach role or also draws profit after reserves These first-year estimates use $1874M revenue, $1248M EBITDA, 45% occupancy, and $6,200 monthly fixed overhead They are planning assumptions, not tax advice, guaranteed earnings, or automatic distributions

Owner income$71kNet margin66.6%–83.2%Revenue for target pay$85kBusiness difficultyMedium

Want to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Can you test the full studio forecast?

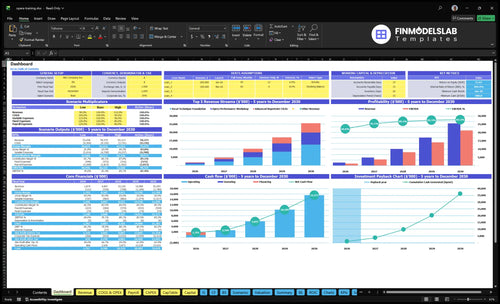

Open the Opera Vocal Training Studio Financial Model Template to check the dashboard, assumptions, income statement, staffing, cash flow, and scenario tabs. It shows revenue, EBITDA, owner pay, payback, and cash need, plus pricing, student volume, instructor use, rent, reserves, and owner pay targets from 45% to 90% occupancy.

Owner-income model highlights

Owner pay capacity

Revenue and EBITDA

Occupancy scenario ranges

Solo opera vocal coach vs studio owner income: which earns more?

For Opera Vocal Training Studio, the solo coach usually earns more per lesson because gross margin stays high when the owner teaches everything. Hiring one associate instructor in Year 1 and 3 by the mature year can raise revenue, but only if occupancy, package renewals, and unpaid admin time stay under control.

Solo coach model

Keeps gross margin higher

Caps paid teaching hours

Leaves less payroll risk

Works best with strong occupancy

Studio with instructors

Adds 1 associate in Year 1

Grows to 3 instructors later

Adds payroll and management load

Needs renewals to lift take-home

Can an opera vocal training studio replace my salary?

Yes, How Do I Launch Opera Vocal Training Studio? can replace your salary in the model, but only after paid demand covers the $85k owner role, payroll, and overhead. At 45% occupancy, first-year revenue is $1.874M against $193.5k payroll and $74.4k fixed overhead, so the salary works only if onboarding, cancellations, and retention stay on plan.

Salary test

Cover $85k owner pay first

Fund $193.5k payroll next

Protect $74.4k fixed overhead

Watch 45% occupancy closely

Cash rule

Delay raises if onboarding slips

Track cancellations every week

Hold pay near salary line

Build reserves before distributions

What opera vocal training studio operating costs reduce owner income most?

For an Opera Vocal Training Studio, payroll is the biggest cost that cuts owner income, with costs rising from $1935k to $388k as instructor and accompanist hours grow. Fixed overhead is also heavy at $62k a month, led by a $45k studio lease, so if you’re still mapping the plan, see How To Write A Business Plan For Opera Vocal Training Studio?. Variable costs take 175% of revenue in Year 1 and 145% later, so every added accompanist, recital, or marketing dollar has to earn back through paid sessions.

Biggest income drag

Payroll grows fastest.

Instructors and accompanists drive it.

$45k lease anchors overhead.

$62k monthly fixed cost is heavy.

Cost pressure to watch

175% of revenue in Year 1.

145% of revenue later.

Each recital must fill paid seats.

Each marketing dollar needs tuition back.

Opera Vocal Training Studio Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the six income drivers?

1

Seat Fill

45%-90%

More filled lesson slots raise revenue fast, and empty time is lost income.

2

Package Price

$300-$630

Higher class prices lift revenue without much extra cost, so margin improves if demand holds.

3

Instructor Mix

1.0-3.0 FTE

Using more hired instructors can scale capacity, but the mix decides how much profit stays with the studio.

4

Performance Prep

$550-$630

Advanced repertoire work sells at the top end of the price band, so each student adds more revenue.

5

Coaching Upsells

$2.5K-$8K

Private coaching adds extra income on top of core classes, and it tends to carry better take-home margin.

6

Fixed Overhead

$74K

Rent, software, and studio ops sit in a fixed cost layer, so tight overhead control protects cash.

Opera Vocal Training Studio Core Six Income Drivers

Lesson and Package Pricing

Package Pricing

$300-$340 for foundation, $450-$510 for performance workshop, and $550-$630 for advanced repertoire creates the revenue ladder. Moving one student from foundation to advanced adds about $250-$330 a month, before any private coaching add-ons. That only works if students can see better credentials, audition prep, repertoire coaching, and results.

Price resistance shows up fast when progress stalls or retention drops. Here’s the quick math: higher tuition lifts revenue per student, but if upgrades slow or refunds rise, the extra cash never reaches owner pay. What this estimate hides is extra prep time, because premium packages can raise teaching labor and feedback costs.

Track Package Value

Measure mix, upgrade rate, and retention. Watch how many students sit in each tier, how many move up after each term, and whether attendance and audition outcomes justify the price. If students stay in the lowest tier too long, the pricing ladder is weak and monthly revenue per student stays capped.

Track tier-by-tier enrollment.

Test price against outcomes.

Document audition and repertoire wins.

Review churn after each term.

Use package names that match the work: foundation, performance workshop, advanced repertoire. Tie each step to a clear deliverable, like diction work, audition prep, or recital readiness. If a price increase does not come with visible progress, cash flow weakens and owner draw gets squeezed.

1

Paid Student Volume

Paid Student Volume

Paid student volume is the chain from inquiries to enrolled students to paid completed sessions. With 22 billable days a month, revenue depends on filled seats and paid attendance, not raw traffic. In the model, monthly revenue rises from $1,874 to $25,555 as capacity and occupancy improve, so owner income only grows after the calendar turns into collected tuition.

Referrals, audition seasons, and steady follow-up usually matter more than website leads. If students inquire but do not enroll, or enroll but miss paid sessions, cash slows and the owner still carries studio time and fixed costs. The risk is simple: weak conversion looks like demand, but it does not pay the owner.

Fill Seats, Then Sessions

Track three ratios: inquiry-to-enrollment, enrollment-to-paid-session, and seat occupancy across the 22-day month. Here’s the quick math: more paid seats per day spreads fixed studio time over more tuition, which lifts owner draw. If conversion drops during audition season, the owner should tighten follow-up and watch the fill rate weekly.

Measure each conversion step.

Track paid sessions by class.

Review fill rate every week.

Use referrals and audition-prep messaging to keep demand warm when interest spikes. Open seats hurt twice: you lose tuition now and you weaken next month’s cash base. What this estimate hides is attendance friction, so the owner needs paid completions, not just a full inquiry list.

2

Utilization and Retention

Utilization and Retention

Utilization is the share of teaching capacity that turns into paid lessons. Here, the model moves from 45% to 90% occupancy, which is about 2.0x more collected revenue if tuition and seat count stay the same. Owner pay rises only when filled seats stay filled, so empty capacity is pure lost income.

Cancellations, seasonal breaks, and uneven practice can break the link between a full calendar and real cash. The key inputs are filled seats, attendance rate, monthly tuition, make-up usage, and renewals. A schedule can look busy and still under-collect if students miss often or drop out after one cycle.

Track attendance, not just bookings

Use recurring schedules and clear make-up rules so cash is predictable. Packages help because they lock in monthly revenue better than one-off lessons. Here’s the quick math: if occupancy stays near 90%, the same room and teacher hours generate far more take-home than at 45%.

Track booked seats versus attended seats

Measure renewal by cohort

Cap make-up lesson leakage

Watch seasonal drop-offs early

3

Owner-Taught Versus Hired-Instructor Mix

Owner vs. Instructor Mix

Owner-taught lessons usually keep more margin because less payroll leaves the business, but they also consume the owner’s calendar. Hired instructors add capacity, yet their margin only works when paid hours stay filled and the payroll rate stays below lesson revenue. The key inputs are booked hours, hourly pay, cancellations, and the owner’s own coaching time.

As staffing moves from 10 FTE to 30 FTE, the business can grow faster, but quality control gets harder. If the owner teaches everything, cash margin may look better, but growth stalls. If the mix shifts too far to associates, empty hours become a payroll drag and reduce take-home pay. One empty teaching hour still costs money.

Track Fill Rate Before You Add Staff

Track filled hours by teacher, not just total inquiries. Compare lesson revenue per hour to instructor pay per hour, then test whether the owner’s time is better spent teaching or supervising. If hired hours are not consistently full, keep the owner in the high-value lessons and limit associate growth until demand is stable.

Use a simple staffing rule: add instructors only when recurring demand can cover their payroll, not just peak weeks. Watch cancellations, student-to-teacher fit, and the owner’s coaching load. If the owner is pulled out of sales, curriculum, or performance prep, income can fall even when the studio looks busier.

Measure revenue per teaching hour.

Watch payroll per filled hour.

Track owner hours spent coaching.

Limit associates when fill drops.

4

Fixed Overhead Control

Fixed Overhead Control

$6,200/month of fixed overhead sets the break-even floor before owner pay: $4,500 lease, $650 utilities and internet, $200 piano tuning, $300 insurance, $150 student software, and $400 cleaning. Every month starts at that cost base, so the studio needs enough paid lessons just to stay even.

The key input is paid utilization on top of that fixed base. A larger room only helps if it brings enough paying students or billable hours to cover the higher rent and support costs. If overhead rises faster than paid seats, owner take-home falls even when the calendar looks busy.

Reduce the fixed base

Track each fixed line monthly and flag any move over 5%. Here’s the quick math: if rent or utilities go up, the owner must sell more lesson time just to protect the same draw. Keep space decisions tied to paid seats, not room size alone.

Review lease, utilities, and cleaning monthly

Separate fixed from variable costs

Test room size against paid seats

Renew software only if used

5

Premium Performance Preparation Revenue

Premium Prep Packages

When a student buys opera audition coaching or performance prep, the studio raises annual revenue per student without adding a full new seat. These packages can add $2,500 to $8,000 a year, or about $208 to $667 a month, if they include repertoire coaching, diction support, masterclasses, intensives, and recital prep. The spread only helps if the price covers extra teaching time and the student stays enrolled.

Price the Add-On to Clear Labor

Estimate this driver from package price, student count, and attach rate for private coaching. Track how many current students buy the prep package, how often they renew, and whether the added revenue stays ahead of the extra lesson hours. One clean rule: keep the offer tied to classical and opera goals, not general voice-school extras.

Repertoire coaching

Diction support

Masterclasses

Intensives

Recital preparation

6

Opera Vocal Training Studio Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-pay scenarios

Owner income scenarios

Owner income rises as occupancy, package mix, and payroll scale improve. Year 1 is a tight launch case; Year 3 is the working plan; Year 5 shows the mature upside.

A quick view of owner take-home across low, base, and high operating levels.

Scenario

Low CaseLow case

Base CaseBase case

High CaseHigh case

Launch model

This is the lower earnings path built on first-year traction and lighter fill.

This is the modeled earnings path at a normal Year 3 operating pace.

This is the stronger earnings path built on mature-year fill and fuller scheduling.

Typical setup

Year 1 runs at 45% occupancy with $300, $450, and $550 packages, $1.874M revenue, $1.248M EBITDA, and the owner still drawing the $85k lead-coach role.

Year 3 reaches 75% occupancy with $320, $480, and $590 packages, $10.12M revenue, $8.107M EBITDA, and $302k payroll.

Year 5 reaches 90% occupancy with $340, $510, and $630 packages, $25.555M revenue, $21.271M EBITDA, and $388k payroll.

Cost drivers

45% occupancy

$300/$450/$550 pricing

$1.874M revenue

$1.248M EBITDA

$85k owner role

75% occupancy

$320/$480/$590 pricing

$10.12M revenue

$8.107M EBITDA

$302k payroll

90% occupancy

$340/$510/$630 pricing

$25.555M revenue

$21.271M EBITDA

$388k payroll

Owner income rangeBefore owner reserves

$1.25MLow income

$8.11MCore income

$21.27MHigh income

Best fit

Use this to stress test early demand, slower enrollment, and thin launch-month cash.

Use this as the main planning case for staffing, owner pay, and reinvestment pacing.

Use this to test upside if demand stays strong and the studio keeps rooms full.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The modeled first-year owner role is $85,000, and EBITDA is $1248M on $1874M revenue If profit is distributed, owner take-home capacity can be much higher, but that is before personal taxes, debt service, reserves, and reinvestment The safer planning view separates salary, profit, and cash kept in the business

The model shows breakeven in Month 1 and payback in one month, driven by high starting revenue and 45% occupancy That is an aggressive planning output, not a normal guarantee Stress test slower enrollment, delayed collections, cancellations, and the $887k minimum cash need before treating early profit as spendable

Not always, but this model assumes a dedicated studio lease at $4,500 per month Total fixed overhead is $6,200 per month after utilities, piano maintenance, insurance, software, and cleaning A lower-cost space can reduce break-even pressure, but opera training still needs sound quality, scheduling control, and reliable accompanist access

Occupancy, pricing, payroll, and overhead drive owner take-home most The model moves from 45% to 90% occupancy, with package prices rising from $300 to $630 depending on program and year Payroll grows from $1935k to $388k, so instructor hiring must be matched by paid lesson volume

Fill paid recurring packages before adding more fixed cost Start with utilization, retention, and pricing discipline, then add instructors only when demand is steady The model’s margins improve as marketing falls from 8% to 5% of revenue and occupancy rises, but cancellations and weak renewals can erase that gain fast

About the author

Noah Quinn

Business Operations Writer

Noah Quinn is a business operations writer at Financial Models Lab who researches how small businesses launch, operate, and earn money. He focuses on first-year business costs and simple business projections for first-time entrepreneurs, helping them move from side project to real business. With a calm, structured approach, he turns broad business ideas into clear planning assumptions that make early decisions easier.

Choosing a selection results in a full page refresh.