How Much Does an Outdoor Gear Store Owner Make? $27k-$322k

An outdoor gear store owner can make little or nothing in the first year if inventory, payroll, and rent absorb cash In the provided planning case, first-year revenue is about $2875k, with about $273k in operating profit before owner pay, personal taxes, debt service, and inventory reserves By the second year, revenue reaches about $7318k and operating profit before owner pay reaches about $3223k under the same source assumptions Treat these as researched planning assumptions, not a guaranteed salary or distribution

Owner income-$186k to $702kNet margin-6.5%Revenue for target pay$7.3MBusiness difficultyHard

Want to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Outdoor Gear Store model?

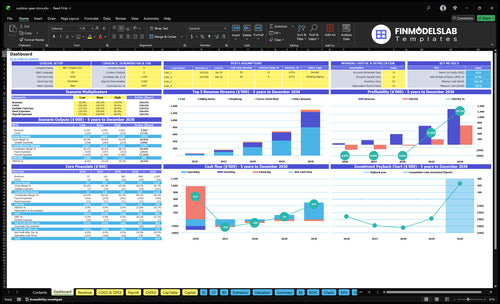

This dashboard in the Outdoor Gear Store Financial Model Template shows revenue, margin, payroll, fixed costs, operating profit, and owner take-home; it also compares $2.875M first-year revenue and $7.318M second-year revenue, so open the model.

Owner-income model highlights

Owner pay before distributions

Revenue and margin view

Scenario and assumption tabs

What profit margin does an outdoor gear store need?

An Outdoor Gear Store needs a gross margin high enough to cover product cost, markdowns, shrinkage, payroll, rent, and restocking cash, so a 50% first-year COGS line that only includes payment processing and packaging does not confirm the true margin. Product mix drives the answer: tents are 300% of the first-year mix at $450, boots are 400% at $180, headlamps are 200% at $45, and meals are 100% at $12. See How Much Does It Cost To Open And Launch Your Outdoor Gear Store? for the startup-cost side. Markdowns hurt twice: they cut margin and trap cash in stock.

What margin must cover

Product cost comes first

Markdowns reduce cash twice

Shrinkage hits store profit

Payroll and rent still matter

Why mix changes margin

Tents: $450, 300% mix

Boots: $180, 400% mix

Headlamps: $45, 200% mix

Meals: $12, 100% mix

Can you make a living owning an outdoor gear store?

Yes, you can make a living owning an Outdoor Gear Store, but only after cash flow covers payroll, rent, inventory needs, and reserves; the first-year model shows $2.875M revenue and $273K operating profit before owner pay, which is tight. The second-year case improves to $7.318M revenue and $3.223M before owner pay, but What Is The Current Growth Trend For Outdoor Gear Store? matters because the model excludes wholesale inventory cost, so safe owner pay may be much lower.

Cash Reality

Year 1 revenue: $2.875M

Year 1 profit: $273K pre-owner pay

Implied margin: 9.5%

Owner pay: not yet protected

Main Caveat

Year 2 revenue: $7.318M

Year 2 profit: $3.223M pre-owner pay

Implied margin: 44.0%

Missing cost: wholesale inventory

Does an owner-operated outdoor gear store make more money?

Yes, often in the first years, because the owner can cover sales, buying, merchandising, and local events instead of paying a $65k store manager. With 1.5 sales associate FTEs at $35k and 0.5 gear specialist FTE at $45k, first-year payroll is about $140k; removing that manager role can improve cash flow fast. But it also shifts work to the owner, and an absentee Outdoor Gear Store usually needs manager pay, tighter controls, and more cash reserve.

Owner-led upside

Save the $65k manager salary

Keep payroll near $140k in year one

Use owner time for sales and buying

Delay extra headcount and protect cash

Watch the tradeoff

Owner workload rises fast

Absentee operation needs manager pay

Tighter controls become necessary

Keep a larger cash reserve

Outdoor Gear Store Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers behind owner income?

1

Foot Traffic

27,040

Year 1 traffic is about 27,040 visits, so small gains in conversion turn into more orders and more owner cash fast.

2

Product Mix

$261 AOV

More tents and boots lift average order value, but the missing wholesale inventory cost still hides true gross margin.

3

Stock Turns

Markdowns

Slow movers tie up cash and force markdowns, so tighter buying protects take-home even when sales look fine.

4

Rent Load

$4K/mo

With $4,000 rent each month, the store needs enough traffic per square foot before profit starts to show up.

5

Labor Load

$140K

Year 1 payroll is about $140,000, so owner involvement and staff output directly shape the cash left for pay.

6

Cash Buffer

$337K

Cash bottoms at about $337,000 in month 37, so seasonal dips need reserves well before breakeven arrives.

Outdoor Gear Store Core Six Income Drivers

Sales Volume And Foot Traffic

Foot Traffic to Gross Profit

Owner income only rises when visits turn into enough gross profit. With 520 visits per week, that is 27,040 visits a year; at 30% conversion, the model says about 811 new buyers before repeat orders. If average order value is about $26064, each lost sale cuts cash fast because rent, payroll, and inventory costs still stay in place.

The point is simple: slow weekdays do not make fixed costs shrink. The store still carries $5,950 in monthly fixed overhead, so weak conversion lowers revenue density and can block owner pay even when traffic looks decent on paper.

Track Conversion by Day

Measure visits, conversion rate, and average order value together. Here’s the quick math: more traffic helps only when enough buyers create gross profit after product cost and discounts. A busy Saturday can still miss the mark if weekday traffic is low and close rates stay soft.

Track by day, by event, and by staff shift. If workshops or demos raise ticket close rates, keep them; if they bring browsers but not buyers, cut them. Use a simple weekly sheet for traffic source, ticket size, and gross profit per sale so owner pay is based on cash, not footfall.

Count visits by day

Track conversion every week

Record gross profit per ticket

Compare weekday and weekend close rates

1

Product Mix And Gross Margin

Product Mix Drives Ticket and Margin

With a first-year mix of 300% tents at $450, 400% hiking boots at $180, 200% headlamps at $45, and 100% meals at $12, the weighted unit price is $217.20. That mix lifts ticket size, but it does not tell you gross margin yet, because wholesale cost is missing. One line matters most: revenue is not profit.

Owner pay should be based on post-markdown and post-replenishment cash, not sticker sales. If tents or boots sit too long, markdowns can erase margin fast, and seasonal stock ties up cash before it hits the bank. Without product cost, you can track sales mix, but you cannot safely forecast draw or distributable profit.

Track Mix, Cost, and Markdown Loss

Track units by category, selling price, wholesale cost, and markdowns on every reorder. Then watch cash margin by SKU, not just total sales. If a $450 tent needs a 20% discount to move, the cash return drops fast, so the mix can look strong while owner income falls. That’s the real risk.

Use a simple margin check before paying yourself: sales minus product cost minus markdowns minus replenishment cash. If boots and tents carry the profit, protect their price first and clear slow items early. One clean rule helps: don’t take owner draw from gross sales; take it from cash left after inventory is replaced.

Track category mix weekly.

Measure markdowns by SKU.

Model margin after replenishment.

Base draws on free cash only.

2

Inventory Turnover And Markdowns

Inventory Turnover and Markdowns

This driver is about how fast tents, boots, sizes, and seasonal goods turn into cash, not just sales. If 12 units per order in year 1 sit too long, markdowns cut gross margin and shrink the cash you can safely withdraw. In a mature year, 16 units per order ties up even more money, so owner pay should wait until stock clears.

Track units on hand, sell-through, and markdown dollars by style and size. Here’s the quick math: every discount lowers gross margin first, then reduces the cash left for distributions. Slow movers can look busy on the shelf and still trap profit in inventory.

Protect Cash Before Owner Draws

Start with weekly sell-through and weeks on hand for each core item. Build buys from order size, seasonality, and expected markdown risk, then compare actual cash recovered after discounts to planned gross margin. If stock turns slow, cut reorders fast and clear weak sizes before peak season ends.

Track units sold by SKU

Watch weeks on hand

Log markdown dollars weekly

Hold cash for replenishment

Keep a reserve for markdowns and replenishment before owner draws. That reserve matters most on seasonal goods, where unsold stock can force price cuts and reduce take-home income even when top-line sales look fine.

3

Rent And Location Economics

Rent and Location Economics

$4,000 a month in rent is $48,000 a year, and it makes up about 67% of the store’s $5,950 monthly fixed overhead. That means location can lift traffic, but the store still has to produce enough buyer volume to cover $71,400 in yearly fixed costs before owner pay starts.

A trail town, tourist corridor, college market, or urban outdoor area can work only if visits turn into sales. High visibility is not useful if conversion stays low. One clean rule: more foot traffic helps only when each visit adds enough gross profit to cover rent and payroll.

Track Buyer Volume Before You Sign

Measure weekly visits, conversion rate, average order value, and gross profit per buyer. Those four inputs show whether the location can pay its fixed cost before owner draws. If traffic is strong but conversion is weak, rent just pushes break-even higher and squeezes cash.

Track visits by week

Track conversion by store

Test sales per square foot

Compare rent to gross profit

Delay owner pay until overhead clears

Before renewing or signing, ask if the store can cover $5,950 in monthly fixed overhead from actual buyer volume, not just traffic counts. If the answer is no, the site may look busy and still drain cash.

4

Staffing And Owner Involvement

Payroll and Owner Pay

Payroll is the biggest fixed cost here: $140k in year 1, or about $11.7k per month, then $221k in year 2, or about $18.4k per month. If sales do not rise with the extra manager, sales associate, gear specialist, and later marketing coordinator, owner income gets squeezed fast because wages are paid before profit.

If the owner works the floor, that labor still has value. Treat owner time as a real expense, then pay yourself only from leftover profit after payroll, rent, and inventory buys. One clean rule: unpaid owner work can hide a loss.

Track Labor Before Taking Draws

Measure payroll as a share of gross profit and sales per labor dollar. Add staff only when the extra hours lift conversion, ticket size, or repeat buys enough to cover the added wage. Year 2 payroll is 58% higher than year 1, so the store needs a real sales bump, not just busier shifts.

Before owner draws, forecast cash for payroll plus slow weeks. Track each role by hours, sales helped, and margin brought in. If the owner is doing manager work, include a fair owner salary in the model so distributable profit is not overstated.

Track payroll by role.

Track sales per labor hour.

Price owner time at market rate.

5

Seasonality And Cash Reserves

Seasonal Cash Reserves

Outdoor retail cash is uneven. Camping, hiking, weather, holidays, and preseason buying push demand up and down, so profitable months must fund slow months. With a 6-month repeat-customer life and about 3 monthly orders per repeat customer, owner pay depends on cash left after rent, payroll, replenishment, and markdown reserves.

Here’s the quick math: sales can look fine in peak season, but that does not mean cash is free. If inventory has to be restocked and slow goods get marked down, paper margin can disappear fast. The owner should not draw cash until the store has covered rent, payroll, replenishment, and markdown reserves.

Build the reserve before paying yourself

Track weekly sales by season, repeat orders, and cash on hand. Also track how much gross profit is already committed to rent, payroll, replenishment, and markdowns. That tells you if the store can keep paying bills when traffic drops.

Weekly sales by month

Repeat orders per customer

Inventory sell-through rate

Markdown dollars reserved

If the slow months cannot cover fixed costs and restocking from reserve cash, cut owner draws and reduce seasonal buying. That protects take-home income when demand softens and keeps the business from funding growth with debt or unpaid bills.

6

Outdoor Gear Store Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high outdoor gear store owner income scenarios

Owner income scenarios

Owner income shifts mostly with traffic, conversion, basket size, and payroll. The model also leaves out wholesale inventory cost, reserves, debt service, and personal taxes, so these are planning cases, not take-home pay.

Low, base, and high owner income cases for planning.

Scenario

Low CaseDownside case

Base CaseCore case

High CaseUpside case

Launch model

Lower earnings path if first-year traffic and conversion stay soft.

Modeled middle case with steadier traffic and second-year assumptions.

Stronger earnings path if traffic, conversion, and basket size all run hot.

Typical setup

Year 1 model: $2.875M revenue, 83.0% contribution, $2.114M fixed payroll and overhead, and $273k operating profit before owner pay.

Year 2 model: $7.318M revenue, 84.0% contribution, $2.924M fixed payroll and overhead, and $3.223M operating profit before owner pay.

Year 3 model: $17M revenue and $115M operating profit before owner pay, with scale from higher traffic and a better product mix.

Cost drivers

3.0% conversion

slower weekday traffic

20.0% repeat share

8.0% marketing

lean staffing

4.0% conversion

stronger weekend traffic

25.0% repeat share

7.5% marketing

added coordinator

5.0% conversion

higher traffic

larger basket

30.0% repeat share

fuller staffing

Owner income rangeBefore owner reserves

$273k pre-owner payLow income

$3.223M pre-owner payBase income

$115M pre-owner payHigh income

Best fit

Use this to stress-test a slow start and tighter labor control.

Use this as the normal ramp case for planning staffing and cash needs.

Use this to test an upside run with fast growth and higher store density.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; the model excludes wholesale inventory cost, reserves, debt service, and personal taxes.

A small store can show modest owner cash early and stronger cash only after traffic scales In this model, first-year revenue is about $2875k, with $273k operating profit before owner pay Second-year revenue reaches about $7318k, with $3223k before owner pay, but inventory cost is not fully modeled

Owner pay usually starts after the store covers rent, payroll, inventory replenishment, and cash reserves Here, first-year fixed overhead is $714k and payroll is $140k, so the owner has little cushion at $2875k revenue If inventory buying is heavy, distributions may wait beyond the first year

E-commerce can help, but only if it adds profitable orders rather than just more marketing and fulfillment cost The model already includes website maintenance at $150 per month, packaging at 30% of revenue in the first year, and marketing at 80% Track contribution per order before expanding online

Traffic, conversion, payroll, rent, and inventory discipline drive cash flow First-year assumptions include 27,040 annual visits, 30% visitor-to-buyer conversion, $4,000 monthly rent, and $140k payroll Even profitable sales can leave little owner cash if too much money sits in slow tents, boot sizes, or seasonal stock

Raise take-home by improving conversion, increasing repeat orders, and controlling payroll before adding new fixed costs Moving conversion from 30% in the first year to 40% in the second year helps revenue rise from about $2875k to $7318k Still, true owner pay depends on wholesale inventory cost and reserves

About the author

Nicholas Webb

Founder-Focused Content Writer

Nicholas Webb is a founder-focused content writer for Financial Models Lab who helps online business beginners make sense of business expense analysis and what it really costs to operate. He writes practical founder checklists and planning guides that support decisions before money is invested. With a calm, structured approach, he explains business costs clearly and without unnecessary jargon.

Choosing a selection results in a full page refresh.