Paint And Coating Owner Income: $150M Before Fixed Costs

A paint and coating business owner’s income can’t be read from revenue alone In the first-year researched assumptions, 33,000 units produce $1695M in revenue and about $1502M after COGS, sales commissions, and shipping That is not guaranteed owner pay because facility costs, payroll, compliance, debt service, taxes, inventory, receivables, and reinvestment still come next Here’s the quick math: $1695M revenue minus $914k COGS minus $1017k variable selling and shipping costs leaves about $1502M before fixed costs

Owner incomeNot determinableNet margin94.6%Revenue for target pay$1.70MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the full model view for Paint and Coating?

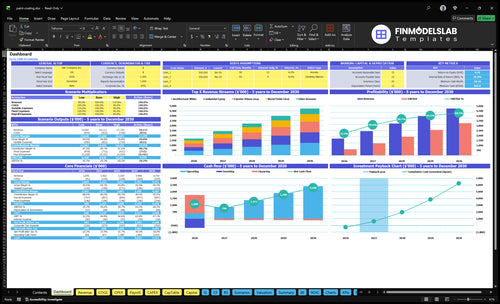

The screenshot shows the Paint and Coating Financial Model Template with dashboard, revenue by product, COGS, expenses, cash flow, scenarios, and owner income. It ties 33,000 first-year units to $1.695M revenue, $914k COGS, $1.017M sales and shipping, and $1.502M contribution before fixed overhead. Open the model.

Owner-income model highlights

33,000 units planned

$1.695M revenue shown

Scenarios drive owner take-home

Can a paint and coating business owner pay themselves a salary?

Yes, a Paint and Coating business owner can pay themselves a salary, but only after gross margin, fixed overhead, staff payroll, debt service, taxes, and reserves are covered; see What Is The Most Critical Metric To Measure The Success Of Paint And Coating Business? for the metric discipline behind that call. The data shows $1.502M in first-year contribution before fixed costs, but owner salary is still unknown because facility cost, compliance, financing, payroll, and taxes are not supplied. If fixed overhead rises by $100k, cash available before owner pay falls by $100k.

Pay salary after

Cover gross margin first

Pay staff payroll first

Fund debt service first

Keep cash reserves first

Salary vs draw

Salary is planned payroll

Distributions come from profit

Overhead cuts owner cash

$100k overhead cuts $100k pay room

What paint and coating gross margin most affects owner take-home?

For Paint and Coating, gross margin is the main early lever for owner take-home because it pays overhead before any owner draw. With first-year gross profit of $1.604M on $1.695M revenue, margin is about 94.6%, and each 1-point change moves pre-overhead profit by about $17k; for launch-cost context, see What Is The Estimated Cost To Open And Launch Your Paint And Coating Business?

Margin is the pay lever

94.6% gross margin funds overhead first

$1.604M gross profit supports owner pay

One point adds about $16,950

Price and material mix matter most

What the data hides

Raw materials are combined per-unit costs

No split for resin, pigments, additives, solvents

Input-level cost control is harder to isolate

Watch gross margin before fixed overhead

How much revenue does a paint business need to pay the owner?

For Paint and Coating, you can’t size owner pay from revenue alone; you need fixed costs and a cash reserve. With a first-year 88.6% contribution margin, $1,695M of revenue supports about $1,502M of contribution before fixed overhead. The clean formula is (owner pay + overhead + reserves) / 0.886, so every $1 of fixed cost needs about $1.13 of revenue.

Revenue math

88.6% contribution margin

$1,695M revenue

$1,502M contribution

Divide fixed needs by 0.886

What moves the target

Price lifts revenue fast

Units drive total sales

Margin sets the gap

Cash cycle affects payout timing

Paint and Coating Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Sales & Price

33K / $51.36

Year 1 plans 33,000 units at a $51.36 blended price, or about $1.695M in revenue and $1.502M after variable costs, so demand and pricing move owner cash fast.

2

Gross Margin

94.6%

After unit COGS, the model keeps about 94.6% of sales, so scrap, waste, and rework cut straight into profit.

3

Product Mix

$25-$120

The price spread from $25 to $120 means mix shifts between Surface Prep Cleaner and Industrial Epoxy can lift revenue without the same unit growth.

4

Fulfillment

6.0%

Sales commissions and shipping take 6.0% of revenue in Year 1, so channel terms and delivery control decide how much cash stays with the owner.

5

Operating Costs

$66.8K/mo

Fixed overhead plus wages run about $66.8K a month, so rent, staff count, and lab spend set the floor for take-home.

6

Cash Discipline

$968K

Cash bottoms at $968K in Month 7, so collection speed and inventory timing matter if you want to avoid extra funding and protect equity.

Paint and Coating Core Six Income Drivers

Sales Volume And Pricing

Sales Volume and Pricing

Here’s the quick math: 33,000 × $5,136 = $169.5M in year 1, then 83,000 × $5,723 = $475.0M by year 5. More units help only when price holds enough contribution to cover fixed costs and still leave owner pay. If discounting weakens margin, the extra volume can add work without adding cash.

The key inputs are units sold, blended average price, and returns. A lower selling price only works if it creates enough extra volume to offset the lost margin. If not, gross profit per unit falls faster than revenue rises, and the owner’s draw gets squeezed.

Protect Margin on Volume

Track net price per unit, discount rate, and return rate by product and channel. Then compare each deal to the base price range of $5,136 to $5,723. If a promotion cuts price but does not add profitable units, it hurts cash and pay instead of helping growth.

Set a floor before approving price cuts. Watch inventory and receivables too, because more units sold on loose terms can delay cash even when revenue looks strong. The clean rule is simple: if the deal lowers margin, raises returns, or slows collection, it is not helping the owner.

1

Gross Margin And Raw Material Cost

Gross Margin and Raw Material Cost

Gross margin is the money left after raw materials and manufacturing costs, and it pays every fixed bill before the owner sees profit. With $1.695M first-year revenue and $914k COGS, the quick math is about $781k gross profit, or roughly 46% gross margin. If source cost shifts from $0.70 on Surface Prep Cleaner to $3.50 on Industrial Epoxy, owner pay moves with the mix.

What this estimate hides is batch loss, packaging, supplier price increases, and freight-in. Those costs sit inside source COGS, so a clean selling price does not guarantee cash left for rent, payroll, or the owner draw. If raw cost runs up faster than price, gross profit shrinks first, and net profit usually follows.

Track Raw Cost by SKU

Measure margin by product line, not just in total. Track unit source cost, packaging, batch loss, and supplier terms for each SKU, then compare that to selling price and order volume. Here’s the quick test: if a higher-cost item sells well but weakens gross margin, it can still cut take-home income by squeezing the cash that funds fixed costs.

Raise prices or change the mix first on the items with the widest cost swings, especially the $0.70 to $3.50 source-cost range. That keeps gross profit aligned with cash needs and makes it easier to pay the owner after overhead. A small cost increase matters more than a small volume gain when margin is the main gate to profit.

2

Product And Sales Channel Mix

Product Mix

Product mix is not just a sales chart; it decides both revenue and workload. In year 1, the line mix totals $1.695M: $450k Architectural White, $360k Industrial Epoxy, $300k Wood Finish Clear, $200k Surface Prep Cleaner, and $385k Exterior Primer Gray. Architectural White is about 26.5% of sales, so a shift in one SKU can move owner pay fast.

Channel mix changes cash and profit, not just top line. Compare retail, wholesale, contractor, industrial, private-label, and specialty sales on net margin after credit terms, service time, and volume. A lower headline margin can still win if it ships in larger lots and needs less support. The wrong mix can trap cash in receivables and shrink the owner’s draw.

Track Net Contribution

Track units by SKU, channel mix, and net price after discounts. Then add credit days, returns, freight, and service labor. If a product sells well but needs more tinting, tech help, or custom packaging, its real contribution falls, and owner pay drops even when revenue holds.

Test mix shifts in small steps. Push more volume toward the SKUs and channels with the best cash contribution per order, not just the best posted margin. That keeps gross profit dollars high and working capital lighter, so the owner can pay themselves sooner.

3

Production Or Fulfillment Efficiency

Production Efficiency

Efficiency is what protects gross margin before owner pay. In a coatings business, COGS includes direct labor, packaging, freight inbound, labeling, manufacturing overhead, quality control, utilities, depreciation allocation, and indirect labor. On $1.695M of first-year revenue, just 1% of waste or rework is about $16,950 lost from contribution.

Track batch size, plant utilization, waste, tinting time, QC rework, and labor productivity. Here’s the quick math: lower scrap and faster changeovers cut unit cost, lift gross profit, and leave more cash for fixed overhead and owner draw. If rework rises, profit falls even when sales do not.

Measure the Cost Leak

Start with one weekly dashboard. Tie each batch to output, scrap, labor hours, and rework so you can see which product or shift is hurting margin. For stores or resellers, add warehouse picking, tinting labor, delivery cost, and stockouts so fulfillment cost does not hide inside COGS.

Track yield by batch.

Measure rework hours daily.

Compare labor hours per unit.

Watch stockouts and rush freight.

Set cost targets by product line and price from the real process, not a wish. If tinting, picking, or delivery drifts up, raise the price, fix the process, or both. The goal is simple: keep contribution before fixed overhead high enough that owner pay is not squeezed out later.

4

Operating Costs And Compliance

Overhead and Compliance Cost Control

Overhead is the gap between contribution and owner income. In this model, first-year contribution before fixed overhead is $1502M after COGS, 40% sales commissions, and 20% shipping, so every extra dollar of rent, utilities, insurance, permits, testing, safety, sales staff, delivery, or marketing cuts owner pay dollar for dollar.

That makes fixed cost control a hard gate on distributions. Here’s the quick math: owner income = contribution - fixed overhead. If compliance spend climbs, or headcount comes in early, cash flow tightens fast even when sales look strong. One clean rule: keep recurring overhead tied to booked volume, not hope.

Track Overhead by Month

Measure fixed overhead separately from variable cost of goods sold. Track rent, utilities, insurance, permits, testing, safety, sales staff, delivery, and marketing each month, then compare them to contribution from sales, commissions, and shipping.

Watch the burn rate if sales slow or mix shifts toward lower-margin jobs. A simple control is to set a cap on fixed overhead as a share of contribution and review it before adding staff or compliance spend. If the gap widens, owner pay gets squeezed before revenue drops.

Separate fixed and variable costs.

Review compliance spend monthly.

Test overhead before hiring.

Protect contribution for owner pay.

5

Working Capital And Cash Reserves

Working Capital And Cash Reserves

Cash profit is not the same as cash you can take home. In a paint and coating business, cash gets tied up in raw materials, packaging, finished goods, and customer credit terms before it ever reaches the owner. If sales grow but inventory and receivables grow faster, owner pay has to wait.

Reserve need cannot be calculated from the source data because there are no inventory days or receivable terms. So the right rule is simple: do not draw profits until inventory, packaging, and receivables are fully funded. One missed credit cycle can wipe out a month of distributions.

Protect Cash Before Owner Pay

Track inventory value, accounts receivable, and cash on hand every month. Also watch seasonality, because coating demand can spike before weather changes or project starts, and that can force extra cash into finished goods. The owner should only pay themselves after the business can cover production buys and customer lag.

Use a simple gate: if inventory or receivables are rising, hold distributions. Here’s the quick check: cash available = cash after raw materials, packaging, freight, and receivables funding. That keeps the business liquid and protects owner income from a strong sales month that has not turned into collected cash yet.

6

Paint and Coating Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-pay capacity

Owner income scenarios

Owner income moves with volume, pricing, and how well fixed plant costs get spread. Year 1 is the tightest case; Year 5 shows the strongest scale effect.

Low, base, and high cases show how output and overhead change owner income.

Scenario

Low CaseLower case

Base CaseModeled case

High CaseStrong upside

Launch model

This is the lower earnings path, tied to the first-year ramp.

This is the modeled middle path, tied to the Year 3 operating case.

This is the stronger earnings path, tied to the Year 5 scale case.

Typical setup

The plant is still absorbing fixed wages and overhead, with 33,000 units and about $1.695M of revenue.

The business has more volume spread across the plant, with 59,000 units and about $3.220M of revenue.

The plant is running at fuller scale, with 83,000 units and about $4.750M of revenue.

Cost drivers

fixed wages

plant utilization

sales commissions

shipping and handling

startup absorption

higher volume

fixed cost spread

lower commission rate

shipping efficiency

steadier pricing

fuller utilization

better price mix

lower commission rate

stronger overhead absorption

stable freight

Owner income rangeBefore owner reserves

$599kYear 1 income

$1.89MYear 3 income

$3.25MYear 5 income

Best fit

Use it to stress-test the early ramp and cash pressure.

Use it for the core plan and budget.

Use it to test upside if volume and price hold.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The source data supports contribution before fixed costs, not final owner take-home In the first year, revenue is $1695M from 33,000 units, gross profit is about $1604M, and contribution after commissions and shipping is about $1502M Owner pay comes after facility costs, payroll, debt, taxes, reserves, and reinvestment

Steady pay depends on overhead, collections, and repeat demand, not just sales growth The model grows from 33,000 units in the first year to 83,000 units by Year 5 Revenue rises from $1695M to $4750M, but cash can still tighten if inventory builds or customers pay slowly

Not always Manufacturing can improve control over product margin, but it also brings batch quality, labor, facility, compliance, and inventory risk Resale or distribution may carry lower production risk but can depend more on channel margin and supplier terms The right model depends on cash cycle, customer type, and owner role

Inventory and receivables often decide what the owner can actually take out Even with a 946% first-year gross margin in the source model, cash may be tied up in raw materials, packaging, finished goods, or customer credit Profit on paper does not fund payroll or owner distributions until cash is collected

Reinvest when growth needs stock, capacity, quality control, or sales coverage more than the owner needs distributions In the model, revenue grows from $1695M to $3220M by Year 3 and $4750M by Year 5 That growth may require more inventory, staff, delivery support, and reserves before higher owner pay is safe

About the author

Edward Fisher

Practical Business Analyst

Edward Fisher is a practical business analyst at Financial Models Lab, focused on small business budgeting and estimating what service businesses can realistically earn. He writes break-even explanations and other planning content for founders who want optimistic growth ideas grounded in realistic assumptions and cost-aware decision-making.

Choosing a selection results in a full page refresh.