How Much Does a Payment Gateway Owner Make With $180K CEO Pay

You’re estimating owner income before the gateway has proved volume, so treat pay as a cash-flow decision, not a guaranteed salary This US-focused view uses the five-year model assumptions, including $180,000 CEO payroll, $14,300 monthly fixed overhead, and a 25% Year 1 variable commission It excludes tax-specific advice, legal compliance advice, debt terms, and guaranteed distributions

Owner income$180kNet margin-17%Revenue for target pay$1.03MBusiness difficultyHard

Want to test your payment gateway owner income

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Payment Gateway forecast model?

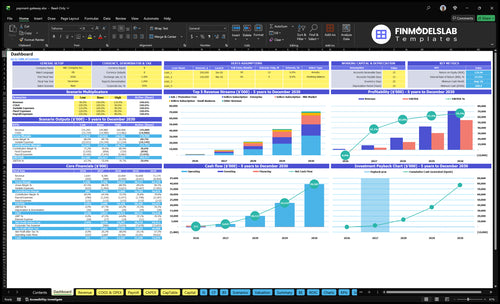

See the Payment Gateway Financial Model Template dashboard for revenue, TPV, orders, merchant count, costs, EBITDA before owner distributions, and cash reserves; open it to review assumptions.

Owner-income model highlights

Owner take-home after EBITDA

Revenue and margin drivers

Scenario tests and budgets

What is a realistic payment gateway profit margin

A realistic Payment Gateway margin is not fixed; it depends on pricing and risk, not the label. If you want the startup-cost side, see How Much Does It Cost To Open, Start, Launch Your Payment Gateway Business? Here’s the quick math: at a 25% take on order value plus $0.25 per order, Year 1 also carries modeled costs of 100% processing and bank fees, 25% cloud, 35% sales and marketing, and 15% support.

By Year 5, the model improves to 80%, 17%, 27%, and 11%, but chargebacks, fraud monitoring, PCI compliance, reserves, and high-risk merchants can still reduce distributable cash even when revenue grows.

Year 1 pressure

25% take on order value

$0.25 fee per order

100% processing and bank fees

35% sales and marketing cost

Year 5 still exposed

80% lower processing burden

17% cloud infrastructure cost

27% sales and marketing cost

11% variable support cost

How much transaction volume does a payment gateway need

Scaling a Payment Gateway starts with merchant volume and retention, not founder optimism. Here’s the quick math: sellers grow from 2,000 in Year 1 to 28,125 in Year 5, and buyers grow from 5,000 to about 41,667. Income only improves if the modeled take rate, costs, churn, and cash reserves all hold.

Grow volume first

Scale sellers from 2,000 to 28,125.

Grow buyers from 5,000 to 41,667.

Shift mix to 25% enterprise by Year 5.

Keep retention ahead of acquisition.

Run the company shift

Move from sales to risk work.

Own partnerships and hiring.

Track compliance every month.

Plan cash reserves before growth.

Payment Gateway Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the six main payment gateway income drivers

1

Processed Volume

$102M

More TPV means more fee revenue; Year 1 volume is $102M, so every extra dollar processed lifts take-home.

2

Take Rate

2.5%+$0.25

The variable fee starts at 2.5% and the fixed $0.25 per order stacks on top, so margin lifts with order value.

3

Seller Retention

2K-28K

Merchant count rises from 2,000 in Year 1 to 28,125 in Year 5, so retention protects recurring revenue.

4

Risk Reserves

High

Chargebacks and fraud reduce distributable cash, so tighter controls protect owner income.

5

Tech Costs

12.5%

Year 1 processing and cloud costs take 12.5% of revenue before overhead, so small cuts flow straight to EBITDA.

6

Acquisition Cost

$250-$160

Seller CAC drops from $250 to $160, so the same marketing budget buys more merchants and more volume.

Payment Gateway Core Six Income Drivers

Monthly Processed Volume

Monthly Processed Volume

Monthly processed volume is the total dollars that move through the gateway. It is the base for transaction revenue, but it is not owner income. In Year 1, modeled TPV is about $102M from 11,750 orders, or about $848k per month; by Year 5, it reaches about $1,607M from 143,751 orders.

Here’s the quick math: revenue comes from take rate × TPV + fixed fee × orders, plus subscriptions and promotion fees. So higher TPV only raises owner pay if the volume is retained and priced well. The risk is confusing payment flow with company money. Cash can move fast without becoming profit.

Track the fee base, not just the flow

Measure monthly TPV by merchant, order count, average order value, take rate, and fixed fee per order. Those inputs show whether growth comes from more orders, bigger baskets, or better pricing. If TPV rises but fee yield falls, revenue quality slips and margin can thin fast.

Monthly TPV

Order count

Average order value

Take rate and fixed fee

Subscriptions and promotion fees

Protect owner income by keeping merchants active and pricing by segment. A small fee change moves profit fast, and the model expects higher revenue only when volume is retained and priced well. Watch churn, payment mix, and subscription attach rate, since they keep TPV steady and support more predictable distributions.

1

Net Take Rate

Net Take Rate

Net take rate is the share of TPV left after bank, network, acquirer, and cloud costs. It is calculated from TPV, order count, average order value, the commission %, the fixed per-order fee, and the processing and cloud costs that sit underneath it.

On $102M TPV, Year 1 pricing of 25% of order value plus $0.25 per order creates an effective gross transaction revenue rate of about 27.9%, but that is not profit. Owner income depends on the spread after costs, not the top-line fee.

The risk is simple: a small fee change can move profit fast. In Year 5, the variable commission falls to 21% while the $0.25 fixed fee stays flat, so the flat fee matters less as orders get larger. If processing and cloud costs stay high, the owner keeps less cash even when volume rises.

Track Gross Spread Per Order

Measure TPV, order count, average order value, commission %, fixed fee, and all payment-processing costs each month. Here’s the quick math: net spread = take rate minus bank, network, acquirer, and cloud costs. If the spread slips by even 1 point on $1,607M of Year 5 TPV, that is about $16.1M of revenue at risk before fixed fees.

Keep pricing reviews tied to cost data, not gut feel. When the variable commission drops from 25% to 21%, test whether volume growth and lower support or cloud cost can protect cash that funds owner pay.

2

Merchant Retention

Merchant Retention

If merchants leave fast, TPV resets and the owner has to keep buying growth. In this model, Year 1 adds 2,000 sellers at $250 CAC, and Year 5 reaches 28,125 sellers at $160 CAC, so retention matters because it spreads acquisition cost over more months of revenue.

Retained merchants also keep monthly subscription income alive, from $19 up to $600 by segment and year. Enterprise share rises from 5% to 25%, which can improve cash flow, but churn still weakens revenue durability and makes owner pay less predictable.

Track churn by merchant cohort

Measure monthly churn, renewal rate, TPV per merchant, and subscription tier by cohort. Here’s the quick math: better retention lowers effective CAC payback and protects gross margin because fewer merchants need replacing just to hold revenue flat.

Track start date and cancellation date.

Segment starter vs enterprise accounts.

Watch support tickets before churn.

Test renewal nudges after onboarding.

Flag failed payments and downgrades fast.

If onboarding drags or payment failures spike, churn risk rises and the model needs more selling spend just to stand still. That hits distributable cash first, then owner draw.

3

Risk Costs And Reserves

Risk Costs and Reserves

Risk costs cut owner cash fast because they come out before profit reaches the bank. In this model, chargebacks, disputes, fraud tools, monitoring, and reserve holds can reduce distributable cash even when TPV rises. The model already counts transaction processing and bank fees at 100% of revenue in Year 1 and 80% in Year 5, so fraud losses and reserves need their own inputs.

The key input set is TPV, order count, average order value, chargeback rate, reserve percentage, reserve timing, and high-risk merchant mix. One clean rule: cash available for owner pay is not the same as revenue booked. If reserves jump during volatile growth, profit can look fine while distributions stay thin.

Track Chargebacks and Reserve Holds

Measure chargebacks per 1,000 orders, reserve % of TPV, and days cash is held. Then separate fraud loss from normal processing cost so the forecast shows real owner cash. Here’s the quick math: TPV × reserve % tells you cash trapped, not income.

Set merchant rules by risk tier, and test stricter monitoring for high-risk accounts. If onboarding takes 14+ days or disputes rise after launch, build a larger reserve cushion before you promise owner draws. That protects payroll, support, and vendor payments when volume spikes.

4

Technology And Compliance Costs

Technology and compliance load

This driver covers gateway uptime, security, tokenization, audits, developer maintenance, and support tools. In the model, cloud infrastructure is 25% of revenue in Year 1 and 17% in Year 5. Add $3,000 monthly legal and compliance fees, $1,000 for security audits and certifications, and $1,500 for software licenses. These costs lower operating profit before owner pay.

Here’s the quick math: fixed tech and compliance spend is $5,500/month before cloud. If reliability slips, merchants churn and disputes rise, so fee income can fall while support costs rise. The owner feels that twice: less cash left after operating costs, and a weaker profit base for draws.

Protect uptime, control spend

Track uptime, failed payments, disputes, and support tickets together. If tokenization and security tools cut chargebacks, they help revenue quality even when they cost cash. The test is simple: does retained revenue cover the 25% to 17% cloud load plus the $5,500 monthly fixed tech and compliance bill?

Keep vendor count tight and review license use every month. As volume grows, fixed compliance costs spread over more TPV, so margin can improve and owner distributions can steady. If merchants see outages or weak support, churn risk rises fast and take-home income usually falls before revenue does.

5

Sales Partnerships And Integrations

Partnership-Driven Acquisition Efficiency

Sales partnerships and integrations lower how much it costs to win each seller and buyer, so more of each new account can turn into owner cash. In this model, seller marketing rises from $500k in Year 1 to $45M in Year 5, while seller CAC falls from $250 to $160. Buyer marketing rises from $50k to $250k, while buyer CAC falls from $10 to $6.

That only helps if the accounts stay long enough to earn back the spend. Bank, software, ecommerce, and agency partnerships can cut CAC and shorten payback, but integrations still need developer support and onboarding time. Simple rule: if payback trails churn and support cost, the owner’s take-home falls even when gross volume grows.

Track Payback by Channel

Measure each channel separately: seller CAC, buyer CAC, onboarding time, support tickets, and developer hours. The inputs that matter are new sellers, new buyers, conversion rate, retention, and the cost to keep each account live. A cheap partner lead is not cheap if it takes weeks to activate and needs heavy help.

Use a hard gate before scaling a partnership: the account must pay back faster than it churns. Here’s the quick test: if a channel lowers CAC from $250 to $160 for sellers or from $10 to $6 for buyers, keep it only if support load stays flat or drops. Otherwise, the extra revenue won’t reach owner income.

Track payback by partner.

Count onboarding days.

Log developer hours.

Watch churn by cohort.

Stop weak integrations fast.

6

Payment Gateway Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Payment gateway owner income scenario objective

Owner income scenarios

Owner income moves fast here because seller mix, buyer mix, TPV, and acquisition spend all change together. Early losses can turn into strong operating profit as enterprise share and repeat orders rise.

Low, base, and high cases show how payment volume and cost mix change owner take-home.

Scenario

Lean CaseLean case

Base CaseBase case

High-Scale CaseHigh scale

Launch model

This mirrors Year 1, where 2,000 sellers, 5,000 buyers, and about $102M TPV still leave operating profit under pressure.

This mirrors Year 3, where 12,500 sellers, 18,750 buyers, and about $535M TPV turn operating profit positive.

This mirrors Year 5, where about 28,125 sellers, 41,667 buyers, and roughly $1.607B TPV push operating profit much higher.

Typical setup

The book stays small-business heavy, with a 25% commission, a $0.25 fixed fee, a $550k combined acquisition budget, and about $143k in monthly fixed overhead.

The mix shifts toward mid-market, with a 23% commission, a $0.25 fixed fee, and about a $2.65M combined acquisition budget.

Enterprise share rises, the commission rate falls to 21%, and a $4.75M combined acquisition budget supports larger repeat-volume accounts.

Cost drivers

Small-business mix

25% commission

$0.25 fixed fee

$550k acquisition budget

$143k fixed overhead

Mid-market mix

23% commission

$0.25 fixed fee

$2.65M acquisition budget

lower CAC

Enterprise mix

21% commission

$4.75M acquisition budget

lower CAC

repeat orders

Owner income rangeBefore owner reserves

($145k)Lean case

$14.4MBase case

$54.5MHigh scale

Best fit

Use this to test launch risk, cash burn, and whether fixed staff costs are too heavy early on.

Use this as the main plan for a scaling platform that is past launch but not yet enterprise-led.

Use this to test upside if enterprise sales, repeat usage, and lower CAC all land together.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; actual owner take-home can be lower after reserves, taxes, and working-capital needs.

The model supports $180,000 in CEO payroll, with any extra take-home dependent on operating profit, reserves, and reinvestment In Year 1, the assumptions create about $102M in TPV and $284k in transaction commission revenue Owner distributions should not be treated as guaranteed income, especially before chargeback and compliance reserves are funded

It can pay the owner when recurring revenue and gross profit cover payroll, fixed costs, acquisition spend, and reserves This model includes $180,000 CEO pay from the start, but that requires enough cash support Year 1 also carries $550k in acquisition budgets, $350k in known CEO and CTO payroll, and $1716k in fixed overhead

You need legal review before operating, but this estimate does not give legal advice A gateway may face payment network rules, bank partner requirements, PCI compliance, data security duties, and state or federal obligations depending on its role The model includes $3,000 monthly legal and compliance fees plus $1,000 monthly security audits and certifications

TPV, take rate, merchant retention, risk costs, infrastructure, and acquisition cost drive profit most In Year 1, transaction pricing is 25% plus $025 per order, while processing and bank fees are 100% of revenue Seller CAC starts at $250 and falls to $160 by Year 5, which can improve payback if churn stays controlled

The strongest model usually blends transaction fees with recurring merchant revenue In this forecast, transaction commission is small in Year 1 at about $284k, while merchant subscriptions, promotion fees, and buyer subscriptions add larger recurring revenue pools That mix helps owner income because it reduces reliance on TPV alone, but only if merchants stay active

About the author

Stephen Knight

Business Idea Researcher

Stephen Knight is a business idea researcher at Financial Models Lab who focuses on revenue and profit basics for founders building a simple business plan. He breaks down business model overviews in plain English, helping non-finance readers understand what it really takes to open a physical location and turn an idea into a workable plan.

Choosing a selection results in a full page refresh.