How Much a Pepper's Ghost Installation Owner Can Make: $33M+

Key Takeaways

Larger contracts lift income faster than unit count.

More units spread fixed costs, but missed installs delay cash.

Labor and change orders can erase margin fast.

Year 1 overhead is $21k monthly, so reserves matter.

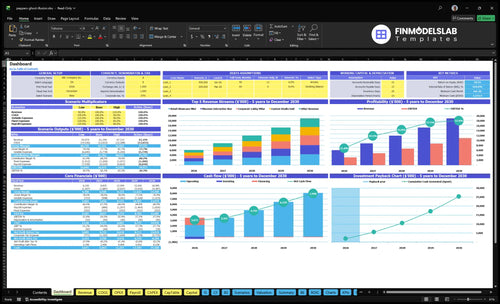

Owner income$3.2MNet margin51.8%Revenue for target pay$6.1MBusiness difficultyHard

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed and depends on revenue, margin, payroll, reserves, taxes, and distribution choices. Not tax advice or owner distribution advice.

Want the full owner income model for Pepper's Ghost Illusion Installation?

It shows revenue, margin, costs, reserves, and owner take-home; open the Pepper's Ghost Illusion Installation Financial Model Template. $6105M Year 1 revenue, 780% gross margin, $33M pre-tax owner capacity, and $190M Year 5 revenue are in the charts.

Model tabs that matter

Dashboard to owner pay

Revenue, COGS, margins

Payroll, reserves, scenarios

Can a Pepper's Ghost illusion installation business scale owner income?

Yes—Pepper's Ghost Illusion Installation can scale owner income if sales volume, production capacity, and quality control grow together. The model moves from 210 units and $6105M revenue in Year 1 to 705 units and $18985M revenue in Year 5. Payroll also rises from $480k to $115M for the listed roles, so an owner-led creative studio keeps quality tight but caps capacity, while a subcontractor-managed model scales faster but adds rework, travel, and client-approval risk.

Owner-led model

Keeps quality control tight

Works well for custom installs

Slows unit output growth

Limits owner scale speed

Subcontracted model

Raises production capacity faster

Needs stricter approval checks

Can increase rework risk

Can add travel costs

How much does a Pepper's Ghost illusion installation owner make per year?

A Pepper's Ghost Illusion Installation owner makes about $3.3M before tax in Year 1 under the researched assumptions; see What Five KPI Metrics Should Pepper's Ghost Illusion Installation Track? for the operating KPIs behind that result. That is based on 210 installs, $6.105M revenue, and about 78.0% gross margin, before separating owner pay from distributions, taxes, and reinvestment cash.

Year 1 math

$6.105M revenue from 210 installs

78.0% gross margin after COGS

$732.6k variable expenses

$252k fixed overhead plus $480k payroll

Owner reality

$3.3M before-tax Year 1 profit

$18.985M Year 5 revenue

$11.8M Year 5 before-tax profit

Profit isn’t the same as cash distributions

What affects profit margins in a Pepper's Ghost installation business?

If you’re pricing a Pepper’s Ghost Illusion Installation, margin gets squeezed by optics, projection gear, fabricated housings, rigging, labor, logistics, and subcontracted field work, so the first step is tight scope control; see How To Write Pepper's Ghost Illusion Installation Business Plan?. Source unit COGS ranges from $1,750 for a Retail Showcase Mini to $28,000 for a Custom Studio Unit. In Year 1, revenue-based COGS can add 40%, including a 10% warranty reserve, and variable expenses can add 120%, so profit depends on how well you manage change and travel.

Big cost drivers

Optics and projection gear set base cost.

Fabricated housings and rigging add labor.

Logistics and travel hit field jobs fast.

Subcontracted work can lift install cost.

Margin controls

Use scoped drawings before pricing.

Approve change orders before extra work.

Stage procurement to avoid rush buys.

Plan travel to cut field overruns.

Pepper's Ghost Illusion Installation Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the six income drivers?

1

Booked Volume

210/yr

More booked units spread setup and overhead, so the Year 1 plan has 210 installs to grow owner cash.

2

Avg Deal Size

$29K

A higher blended deal size lifts revenue even if unit count holds steady, and the mix of larger installs matters.

3

Gross Margin

78%

At 78% gross margin, small gains in fabrication yield, assembly labor, and field time flow straight to profit.

4

Fixed Overhead

$21K/mo

Fixed overhead of about $21K a month sets the floor, so lean rent, software, and admin keep more cash in the business.

5

Warranty Reserve

10%

The 10% warranty reserve can quietly eat take-home, so tight rework control protects cash.

6

Add-on Revenue

High

Add-on design, change orders, and maintenance raise profit without a full new build, so attach rate is pure upside.

Pepper's Ghost Illusion Installation Core Six Income Drivers

Average Contract Value

Average Contract Value

Average contract value is the average price per signed installation, not the number of units sold. In Year 1, project prices run from $12,500 for a Retail Showcase Mini to $150,000 for a Custom Studio Unit, so one large job can equal 12 mini contracts. That mix drives revenue faster than unit count alone, but higher-scope museum, lobby, stage, and studio work adds design hours, fabrication, optics, projectors, install time, and margin risk.

The owner’s take-home rises when bigger contracts keep gross margin intact and cash comes in on time. If change orders, procurement, and rework are not billed and controlled, a high contract value can still leave less profit than several smaller installs. One clean rule: price the scope, not the wish list.

Raise Contract Size Without Squeezing Margin

Track average booked value, change orders, install days, and gross margin by project type. Split estimates into design, fabrication, optics, projectors, and install labor so you can see where scope expands. That matters because a $150,000 job can pay well only if extra work is billed instead of absorbed.

Use tight scope documents, deposit milestones, and procurement approvals before build starts. If the client changes content, hardware, or site layout after sign-off, invoice it fast. Bigger contracts help owner income most when cash is collected early and the team is not stuck doing unpaid revisions or rush freight.

1

Annual Project Volume

Annual Project Volume

Project volume is the number of completed Pepper’s Ghost installations shipped, installed, and commissioned in a year. It drives owner income by spreading $21k per month of fixed overhead across more jobs. Volume moves from 210 units in Year 1 to 705 units in Year 5, so each extra completed install lowers overhead per unit and can lift profit if pricing, labor, and callbacks stay controlled.

Here’s the quick math: annual fixed overhead is $252k. At 210 units, that is about $1,200 per unit; at 705 units, it falls to about $358 per unit. The catch is timing. Sales cycle length, approvals, site readiness, crew availability, travel, and commissioning all decide when cash lands, so missed install windows can delay revenue and owner pay.

Track installs, not just bookings

Measure the full funnel: quoted jobs, signed jobs, ready sites, installed jobs, and commissioned jobs. The key inputs are completion rate and days from deposit to install. If a project slips, overhead keeps running while cash stays tied up in work in progress.

Track booked-to-installed conversion.

Track average approval days.

Track crew days lost to travel.

Track commissioning lag by site.

One clean rule: more completed installs beat more promises. If you lock site readiness earlier and standardize commissioning, you turn the same fixed cost base into more owner draw capacity without changing the overhead line.

2

Gross Margin

Unit Gross Margin

When you sell a Pepper's Ghost install, gross margin is the spread after unit COGS and revenue-based COGS. In Year 1, the model shows about 780%, with source unit costs from $1,750 for a mini to $28,000 for a custom build. That kind of spread can fund owner pay, but only after the rest of the cost stack is handled.

This margin excludes payroll, sales commissions, marketing, shipping, fixed overhead, taxes, and owner pay. So the real cash left for the owner can shrink fast if procurement runs hot or the project mix shifts toward higher-cost museum, stage, or custom jobs. A tighter bill of materials helps more than chasing volume alone.

Control Build Costs

Track gross margin by install type, not just total revenue. Use the actual bill of materials for projector specs, reflective glass or foil, frames, controllers, playback systems, and fabricated housings. Here’s the quick math: if source costs rise, owner take-home falls before overhead even hits the P&L.

Watch quoted cost versus actual cost on every job, and require sign-off on substitutions. The useful inputs are unit price, unit COGS, project mix, and change orders. If the team misses spec control, the model’s 780% spread gets eaten by rework, rush buys, and margin leakage.

Track cost by install type.

Approve substitutions before ordering.

Log change orders separately.

Compare quote to actual COGS.

3

Labor Costs

Labor Costs That Protect Margin

Labor costs decide whether each install keeps its margin or leaks it. Unit COGS already include assembly or engineering labor, from $250 on small units to $4,500 on custom studio units, so labor should not be counted twice. When crew time, founder time, and subcontractors run over plan, project profit drops and there’s less cash left for owner pay.

Here’s the quick math: labor rises with install hours, travel days, rigging, venue rules, union labor, and rework. Listed payroll adds $480k in Year 1 and $115M by Year 5, so every missed hour matters. Clear acceptance tests and schedule slack are what stop margin leakage before it hits gross profit.

Track Labor Per Install

Measure labor by job type, not just by payroll total. Track estimated crew hours, actual hours, subcontracted AV labor, travel time, and rework by project. If a custom studio unit keeps needing extra rigging or client sign-off, that cost should be visible in the job file so pricing and staffing can adjust fast.

Log hours by install phase.

Separate in-house and subcontract labor.

Charge for travel and standby days.

Use acceptance tests before demobilizing.

One clean rule: if labor is not measured per install, margin gets guessed away. The owner keeps more income when each quote includes real crew load, the schedule has slack for venue delays, and change work is billed before the team starts it.

4

Design Fees And Maintenance Revenue

Billable design and service add-ons

When previsualization, technical drawings, content integration, training, refresh work, change orders, and service visits are priced as paid work, they protect gross margin and speed cash collection. If proposal and revision time stays free, the owner is subsidizing engineering labor, and take-home income drops even when the core install sells well.

Do not count this as guaranteed recurring revenue. The key inputs are revision count, billable design hours, service-visit frequency, and the fee tied to each milestone. If a client changes content, optics, site layout, or playback requirements, the extra fee keeps the job from turning into margin leakage.

Turn revisions into billable milestones

Build the quote so scope changes trigger a new line item. Track how many hours are free versus billed, how often change orders are approved, and how many service calls are charged. One simple rule helps: if the work changes the install, it changes the invoice, so the owner gets paid for the extra labor instead of eating it.

Track unpaid revision hours.

Price every scope change.

Log service visits by job.

Bill training before launch.

Set fees for refresh work.

5

Overhead And Reserves

Overhead and reserves

Here’s the quick math: fixed overhead is $21k a month, or $252k a year, and listed payroll is $480k in Year 1. The warranty reserve, the cash set aside for callbacks and fixes, is 10% of revenue, about $61k in Year 1. Owner income is not what’s left after sales; it’s what remains after overhead, labor, and reserve funding.

Year 1 digital marketing, commissions, and shipping add 120% of revenue, so if revenue is about $610k, those costs run about $732k before fixed overhead and payroll. Profit must also fund demo assets, software, working capital, and equipment replacement, so owner pay comes last.

Control reserve cash early

Track each deal’s cash load: marketing, commission, shipping, warranty risk, and install support. Set aside the 10% reserve at booking, not after close. That keeps callbacks and rework from eating the owner draw.

Watch overhead per install.

Separate reserve cash from ops cash.

Delay owner pay until replacements are funded.

Use a weekly cash view that shows booked revenue, reserve balance, and nonrecurring spends like demo assets and software. If the reserve is underfunded, one callback can wipe out the month.

6

Pepper's Ghost Illusion Installation Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income shifts with unit mix, price, and install load. Higher-ticket custom work lifts profit, but sales, production, and field execution get tighter as volume rises.

Compare low, base, and high owner income paths.

Scenario

Low CaseSales pipeline: hard

Base CaseProduction load: heavy

High CaseField execution: intense

Launch model

Lower-case demand keeps the business close to Year 1 scale and a tighter sales funnel.

Modeled demand follows the core plan and keeps the shop moving at a steady, buildable pace.

Stronger demand pushes the business into higher volume and more complex field work.

Typical setup

Year 1 moves 210 units, does $6.105M revenue, and lands at $3.161M EBITDA after the model's overhead and warranty reserve.

Year 3 reaches 428 units, does $12.009M revenue, and lifts EBITDA to $6.712M as staffing and install work scale.

Year 5 reaches 705 units, does $18.985M revenue, and delivers $11.001M EBITDA with a larger sales and install team.

Cost drivers

Sales commissions

shipping and logistics

digital marketing

factory overhead

warranty reserve

Sales commissions

shipping and logistics

digital marketing

higher headcount

install labor

Sales commissions

shipping and logistics

digital marketing

field engineering

production load

Owner income rangeBefore owner reserves

$3.2MLow Case

$6.7MBase Case

$11.0MHigh Case

Best fit

Use this to test launch risk, slower closes, and lean owner pay.

Use this as the most likely operating plan and budget anchor.

Use this to test strong demand, heavier installs, and execution strain.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Revenue is not owner pay In Year 1, the model shows $6105M revenue, but about $134M goes to COGS, $7326k to variable expenses, $252k to fixed overhead, and $480k to listed payroll That leaves about $33M before tax, debt, benefits, and reinvestment

Longer sales cycles delay owner pay because these projects need proposals, approvals, fabrication, install scheduling, and final acceptance The model assumes 210 units in Year 1 and 705 by Year 5 If client approvals or site readiness slip, booked revenue may not turn into cash when payroll, rent, and vendor bills are due

The researched model includes a real team from the start: one technology lead, one optical engineer, two assembly techs, and one sales director, totaling $480k in Year 1 payroll A solo founder could lower payroll, but capacity, quality control, and sales follow-up would become the bottleneck quickly

Project mix, deposits, vendor timing, payroll, and warranty work affect cash most Year 1 includes $1097M of unit COGS, 40% revenue-based COGS, and 120% variable expenses Even with strong margins, cash can tighten if hardware is bought before client deposits clear

Protect owner income with clear scopes, staged payments, signed change orders, and a warranty reserve The model already includes a 10% warranty reserve and $21k monthly fixed overhead The goal is simple: bill design time, control install labor, and avoid using owner profit to fix preventable scope gaps

About the author

Oscar Bryant

Startup Planning Writer

Oscar Bryant is a startup planning writer at Financial Models Lab, where he helps early-stage founders make a business idea easier to evaluate through simple financial projections. He breaks down revenue, expenses, and profit in a clear, practical way, with a focus on cost and income assumptions that help readers understand the numbers behind everyday business ideas.

Choosing a selection results in a full page refresh.