How Much Does a Pizza Shop Owner Make? $112K Year 1 EBITDA

Pizza Shop Bundle

You’re trying to see whether a pizza shop can pay you, not just post big sales This model estimates $112K of Year 1 EBITDA, rising to $807K by Year 5, based on covers, average tickets, food cost, labor, fixed overhead, startup cash, and payback It excludes personal taxes, legal advice, valuation, and any guaranteed owner salary

Owner income$112K-$807KNet margin15%-46%Revenue for target pay$762KBusiness difficultyHard

Want to test your own pizza shop pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Can you check owner income in the Pizza Shop model?

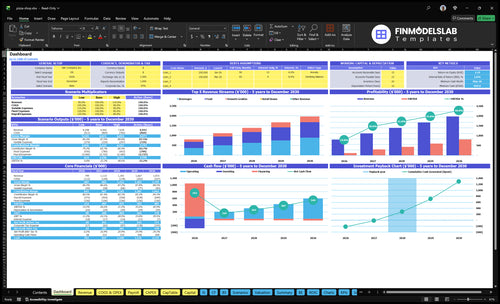

See Pizza Shop Financial Model Template for revenue, EBITDA, cash need, payback, and break-even. Assumptions tabs cover covers, ticket, mix, ingredients, payroll, fixed costs, capex, and reserves.

Owner-income model highlights

Year 1-5: $9.139M to $210M

EBITDA: $112K to $807K

Rent and labor scale

Gross margin stays visible

Owner income is clear

What costs affect pizza shop profit the most?

If you’re sizing up How Much Does It Cost To Open A Pizza Shop?, the biggest profit hits are ingredients, labor, rent, processing, and marketing. In this case, raw ingredients run at 120% of Year 1 sales, packaging is 20%, card processing is 25%, and marketing is 30%. Payroll starts at $325K in Year 1 and rises to $538K by Year 5, while fixed overhead is $130K/month, led by $95K rent.

Main profit drains

Ingredients hit margin first.

Labor scales fast with sales.

Rent is the biggest fixed cost.

Processing cuts every card sale.

Small changes that matter

Cheese and toppings move food cost.

Waste and overtime hit cash fast.

Delivery mix changes fee load.

Marketing at 30% needs control.

Does a pizza shop owner make more if they work in the business?

If Pizza Shop owner works the floor, cash flow can look stronger, but that is labor value, not pure owner profit. The model already includes $60,000 for a store manager and $55,000 for a kitchen lead, so cutting those costs can lift EBITDA (earnings before interest, taxes, depreciation, and amortization) but also raise burnout, service gaps, and training risk. A manager-run shop gives the owner more time for systems and a second location, but only if sales volume and margin can cover those wages.

Owner-operator tradeoff

$60,000 manager cost can be reduced

$55,000 kitchen lead cost can be reduced

Owner labor helps protect cash flow

It does not equal higher true profit

Manager-run shop tradeoff

Owner gets time for systems

Owner gets time for a second location

Needs enough volume to fund wages

Weak staffing can hurt training and service

How much revenue does a pizza shop need to make money?

A Pizza Shop needs about $913.9K in Year 1 revenue in this case to start making money, with break-even reached in Month 4; use What Strategies Are You Using To Grow The Customer Base For Pizza Shop? to pressure-test the demand side. Revenue alone isn’t profit, because owner pay starts after payroll, rent, food, packaging, card fees, marketing, debt service, reserves, and reinvestment.

Break-Even Math

Target $913.9K Year 1 revenue

Reach break-even by Month 4

Serve 1,120 weekly covers

Track midweek $12.50 AOV

Profit Watchouts

Protect weekend $18.00 AOV

Budget payroll at $325K

Plan fixed costs near $130K

Pay owners after operating needs

Pizza Shop Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main pizza shop income drivers?

1

Weekly Covers

1,120/wk

More covers spread rent and payroll across more orders, so take-home rises fastest when traffic is steady.

2

Menu Price

$12.5-$18

Higher midweek and weekend ticket sizes lift revenue per order without adding many extra labor hours.

3

Gross Margin

86%

With ingredients and packaging at about 14% of sales, each point of margin change flows straight to EBITDA.

4

Payroll Load

$325K

Year 1 payroll is about $325K, so staffing discipline decides how much sales turns into owner cash.

5

Fixed Overhead

$13K/mo

About $13K a month in fixed costs sets the break-even floor and makes occupancy control critical.

6

Channel Mix

TBD

Set dine-in, pickup, and delivery mix before modeling fees, because channel mix changes delivery profit and cash take-home.

Pizza Shop Core Six Income Drivers

Order volume

Order volume

Order volume is the cash engine that pays payroll, rent, and owner take-home. In the source case, weekly covers rise from 1,120 in Year 1 to 2,170 in Year 5, or about 94% growth. Weekend traffic matters most: Saturdays move from 250 to 450 covers, and Sundays from 220 to 420.

More covers help only if the kitchen, staffing, and neighborhood demand can handle rush periods. The key inputs are covers by daypart, repeat orders, and marketing spend; if volume rises without flow control, overtime, slower service, and waste can eat the added profit fast.

Track covers by daypart

Build a weekly forecast for breakfast, brunch, dinner, and weekends, then compare it with labor hours and prep capacity. Watch covers per labor hour, repeat visits, and promo response. If Saturday or Sunday demand outruns staffing, extra sales can raise owner income less than expected.

Track covers by daypart.

Monitor repeat-order rate.

Match staff to rush peaks.

Test marketing by neighborhood.

1

Average ticket and menu pricing

Average Ticket and Menu Pricing

Average ticket, or average order value (AOV), is the dollars collected per order. In the source case, midweek AOV is $1,250 in Year 1 and $1,450 by Year 5, while weekend AOV rises from $1,800 to $2,200. That's up 16% midweek and 22% on weekends. Higher ticket lifts revenue without adding customers, so it can raise owner pay if food, labor, and discount costs stay in line.

The catch is mix and margin. A shop with strong topping, drink, dessert, and bundle sales can push ticket up, but discounts can raise order count while shrinking gross profit. The real test is profit per order, not menu price alone, because a higher ticket that needs heavy promos may still leave less cash for rent, payroll, and owner draw.

Track Profit per Order

Start with the simple math: orders × average ticket = revenue. Then track add-on rate for toppings, specialty pizzas, sides, drinks, desserts, and bundles, plus the discount rate. You need weekday and weekend mix, because a higher weekend ticket only helps if that traffic holds. If the menu change lifts ticket but cuts margin, owner income can fall.

Watch net profit per order after food, labor, and promos. If a bundle increases tickets but drives deeper discounts, test it against full-price add-ons. Keep pricing tied to local demand, and recheck it each period against actual ticket, not just top-line sales.

2

Food, packaging, and waste control

Food and packaging cost

Food and boxes set gross profit before labor and overhead. In the source case, raw ingredients are 120% of Year 1 sales and packaging is 20%, improving to 100% and 15% by Year 5. If those are sales-based costs, Year 1 gross profit is negative before payroll and rent, so waste control is not a side task.

This driver includes cheese, dough, sauce, toppings, and packaging. The inputs are sales, order count, recipe yields, spoilage, and unit buy costs. One extra ounce per pie or one bad box per order cuts cash flow right away, because food waste and packaging waste hit owner take-home directly.

Tighten waste fast

Track cost per pizza, box cost per order, and spoilage by item. Use prep sheets, weigh portions, and lock recipes so staff do not overtop pies or overmake dough. Here’s the quick math: owner take-home = sales - ingredients - packaging - waste. If that number does not improve, pay stays thin.

Set a weekly par for dough, sauce, cheese, and toppings, then buy to plan. Compare actual use to theoretical use each week, and flag variance over 5%. Watch spoilage, remake rate, and end-of-day leftovers; those are the leak points that turn sales into cash the owner can pay themselves with.

3

Labor scheduling and productivity

Labor Scheduling and Productivity

Labor is the biggest swing cost after food. In this pizza shop, the source case lists payroll at $325K in Year 1, $4555K in Year 3, and $538K in Year 5, so every idle hour cuts EBITDA and owner draw. The job is to staff for breakfast, brunch, dinner, and delivery peaks without paying for slow hours.

This driver includes cooks, servers, managers, prep, dish, and delivery labor. Use daily covers, average ticket, wage rates, overtime, and manager coverage to estimate it. If staff are too light, service slips and hiring gets harder; if hours run hot, profit falls before the owner can pay themselves.

Track labor by daypart

Measure labor against orders and covers by daypart. Here’s the quick math: paid hours should move with rush demand, not with a padded schedule. Track overtime, tickets per labor hour, kitchen throughput, and delivery labor so you can see which shift is burning cash and which one is paying for itself.

Use owner shift coverage only where it replaces paid hours, but don’t let that turn into burnout. If the owner or manager works too many shifts, service quality and retention can slip. Tight cross-training, shorter prep blocks, and staggered starts help keep labor lean without choking peak-period sales.

Orders per labor hour

Overtime by shift

Manager coverage hours

Delivery labor per order

4

Rent and fixed overhead

Rent and Fixed Overhead

Fixed overhead is the monthly cost base that gets paid before owner income appears. Here, it is $130K per month, led by $95K rent, plus utilities, cleaning, property taxes, accounting/legal, insurance, POS, and music licensing. These costs stay due even when sales slow, so they set the break-even bar for profit and owner draw.

Here’s the quick math: the model needs $694K minimum cash by Month 5. So a bad sales stretch does not just trim profit; it can drain cash and block owner pay. If overhead is not covered by steady gross profit, the business can look busy and still fail to pay the owner.

Protect the Cash Floor

Track fixed overhead as a monthly run rate and compare it to sales and gross margin. Break it into the real inputs: rent, utilities, cleaning, property taxes, accounting/legal, insurance, POS, and music licensing. If that base climbs, owner pay should wait until cash still clears the next few months.

Use the $694K Month 5 cash need as the reserve test. Update it after any rent hike or utility spike. If cash is short, the fix is faster sales, lower space cost, or delayed owner draws. Fixed costs do not flex down, so the buffer has to do the work.

5

Delivery and channel mix

Delivery and channel mix

This driver is the split between carryout, dine-in, in-house delivery, and third-party delivery. It changes owner income because the same sales dollar can carry very different labor, packaging, and fee loads, so revenue alone does not show true profit.

The model should require delivery mix and platform fees before it estimates delivery profit. Compare net margin per order after labor, packaging, card costs, and promotions; otherwise, a higher order count can still leave less cash for owner pay.

Measure margin by channel

Track each channel separately: order count, average ticket, labor minutes, packaging, card fees, promo spend, and delivery fees. That gives you a real margin view by channel, instead of mixing carryout and delivery into one number. One clean rule: if you can’t price the order after fees, you can’t forecast the profit.

Use the mix to protect cash. Carryout often needs less labor, while delivery can add drivers, packaging, and fees, so a shift toward delivery can cut owner income fast if the margin slips. Test channel changes weekly and only scale the orders that raise take-home profit, not just sales.

6

Pizza Shop Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Low, base, and high pizza shop income scenario objective

Owner income scenarios

Owner income shifts with traffic, menu mix, and payroll. Early ramp is tight, but higher weekend volume and better AOV widen take-home after debt service, reserves, and owner pay.

Compare early ramp, base volume, and mature-year income before financing and owner draws.

Scenario

Low CaseEarly ramp

Base CaseScaled ops

High CaseMature volume

Launch model

The low case uses Year 1 ramp, with 1,120 weekly covers and $112k EBITDA before debt service, reserves, and owner pay.

The base case uses Year 3, with 1,640 weekly covers and $431k EBITDA before debt service, reserves, and owner pay.

The high case uses Year 5, with 2,160 weekly covers and $807k EBITDA before debt service, reserves, and owner pay.

Typical setup

Year 1 uses $913.9k revenue, 1,120 weekly covers, $12.50 midweek AOV, $18.00 weekend AOV, and about $325k payroll on $13k monthly fixed costs.

Year 3 supports about $1.466M revenue, 1,640 weekly covers, $13.50 midweek AOV, $20.00 weekend AOV, and a larger staffing base with the assistant manager at 1.0 FTE.

Year 5 supports about $2.101M revenue, 2,160 weekly covers, $14.50 midweek AOV, $22.00 weekend AOV, and the heaviest staffing load in the model.

Cost drivers

weekday volume

weekend AOV

payroll load

rent and utilities

ingredients and packaging

higher weekend mix

more retail beans

assistant manager

payroll growth

promo spend decline

peak weekend traffic

higher AOV

more retail beans

added staffing

lower ingredient rate

Owner income rangeBefore owner reserves

About $112kTake-home tight

About $431kCore model

About $807kUpside case

Best fit

Use this if you want a cautious opening-year case that stress-tests cash and early owner draw.

Use this as the stabilized operating case once traffic, staffing, and menu mix settle.

Use this to test what mature demand can support when volume stays strong and costs keep easing.

!

Planning note: Ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In this researched case, the shop generates $112K of Year 1 EBITDA and $807K by Year 5 That is cash-flow potential before personal taxes, debt service, reserves, and final distributions Revenue is much higher, from about $9139K in Year 1 to $210M in Year 5, but sales are not owner pay

The modeled payback period is 27 months, with break-even reached in Month 4 That depends on the $286K startup capex and the $694K minimum cash need shown in the model If build-out runs over budget or early sales lag, the owner may need more cash before taking distributions

Not always, but the model already carries paid labor, including $325K of Year 1 payroll and a $60K store manager role If the owner works shifts, cash flow can improve, but that is compensation for labor, not pure profit If the owner stays absentee, manager quality and scheduling discipline matter more

Labor, rent, ingredients, packaging, and order volume drive most of the result In Year 1, payroll is $325K, fixed overhead is $13K per month, raw ingredients are 120% of sales, and packaging is 20% Small waste, overtime, and pricing changes can move EBITDA quickly

Plan owner pay after break-even, reserves, and startup cash needs This model shows Month 4 break-even, $112K Year 1 EBITDA, and a $694K minimum cash requirement by Month 5 A safe plan separates working-owner wages, debt payments, reinvestment, and distributions before assuming take-home cash

About the author

Marcus Cole

Business Operations Writer

Marcus Cole is a business operations writer for Financial Models Lab who researches how small businesses launch, operate, and earn money. He focuses on first-year business costs and simple business projections, helping local business owners move from a side project to a real business. His work guides readers from an idea to a basic business plan.

Choosing a selection results in a full page refresh.