Owner income$185k salary

Owner income$185k salaryHow Much Planogram Compliance Service Owners Make: $185k Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$185k salary  Net margin88% to 91%

Net margin88% to 91% Revenue for target pay$210k

Revenue for target pay$210k Business difficultyHard

Business difficultyHard

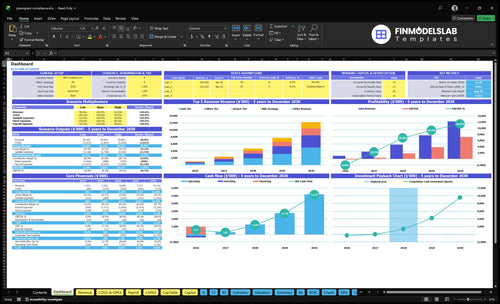

You’re sizing owner pay before the route network is proven, so separate salary from profit This five-year model uses $1051M Year 1 revenue, -$193k Year 1 EBITDA, Month 8 breakeven, and a $185k CEO salary as pre-tax owner-manager pay It excludes taxes, benefits, debt service, and guaranteed distributions

Owner income$185k salaryNet margin88% to 91%Revenue for target pay$210kBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay for a planogram compliance service.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed and this is not tax advice or owner distribution advice.

Want to see the Planogram Compliance Service model layout?

See revenue, margin, costs, reserves, and owner take-home assumptions—open the Planogram Compliance Service Financial Model Template.

Owner-income model highlights

- Owner take-home charts

- Revenue from $1,051M to $12,192M

- EBITDA from -$193k to $7,140M

- Month 8 breakeven, Month 27 payback

- $519k minimum cash

- Scenario assumptions visible

What affects planogram compliance service profit margins?

Planogram Compliance Service profit margins are driven mostly by field network cost, route density, reporting time, cloud processing, payroll, and rework, so the fastest gains come from tighter routing and less manual reporting. In Year 1, variable cost is 12% of revenue, split into 8% field network costs and 4% cloud/reporting fees, then it improves to 9% by Year 5. If you’re mapping the setup, How To Start Planogram Compliance Service Business? fits this cost structure, and EBITDA margin rises from -184% in Year 1 to 586% in Year 5.

Main margin drivers

- 8% field network cost in Year 1

- 4% cloud/reporting fees in Year 1

- Route density cuts travel waste

- Rework lifts direct variable cost

EBITDA margin path

- -184% in Year 1

- 185% in Year 2

- 387% in Year 3

- 586% in Year 5

How much should a planogram compliance service charge?

For a Planogram Compliance Service, don’t use a flat price; charge by scope. The researched monthly rates are $1,500 Bronze, $3,500 Silver, $7,500 Gold, and $5,000 blitz, which gives a $3,650 weighted monthly price on a 40%/30%/20%/10% mix. That mix drives $1.051M in Year 1 revenue, but EBITDA is still -$193k because payroll, marketing, overhead, field costs, and reporting costs absorb the margin.

Tier pricing

- $1,500 Bronze monthly

- $3,500 Silver monthly

- $7,500 Gold monthly

- $5,000 blitz price

Year 1 math

- 40% Bronze mix

- 30% Silver mix

- 20% Gold mix

- 10% blitz mix

Can a planogram compliance service replace my income?

A Planogram Compliance Service can support modeled owner-manager pay of $185k, but it’s not a guaranteed Year 1 salary; the model shows -$193k EBITDA, meaning profit before interest, taxes, depreciation, and amortization, with breakeven in Month 8. Before taking heavy draws, pressure-test payroll, routes, marketing, and What Are Operating Costs For Planogram Compliance Service? because fixed overhead is modeled at $148k per month.

Income Reality

- Supports modeled pay of $185k

- Not guaranteed in Year 1

- EBITDA starts at -$193k

- Breakeven lands in Month 8

What Must Work

- Win recurring monthly contracts

- Keep routes tight and dense

- Cut rework from bad audits

- Cover $148k monthly overhead first

Want to see the main income drivers?

1

$1.1M-$12.2MAudit Volume

More audits are the main top-line engine, and EBITDA moves from -$193K in Year 1 to $7.14M in Year 5.

2

$3.65KContract Price

The weighted monthly contract price sets cash per account, with pricing from $1.5K Bronze to $8.5K Gold by Year 5.

3

8%-6%Route Density

Packing more stores into each route cuts field-network cost from 8% to 6%, so more revenue turns into owner profit.

4

$710K-$2.4MLabor Efficiency

If each audit takes fewer hours, payroll can stay closer to the $710K Year 1 base instead of rising to $2.405M by Year 5.

5

$2.5K-$1.8KClient Retention

With marketing rising from $120K to $650K, keeping clients longer lowers CAC from $2,500 to $1,800 and protects the $519K cash floor.

6

4%-3%QA Load

Tighter reporting and QA can push cloud and processing fees from 4% to 3%, which matters more as volume grows.

Planogram Compliance Service Core Six Income Drivers

Store Audit Volume

Store Audit Volume

Store audit volume is the number of contracted stores you visit and report on each cycle. Revenue rises when active contracts × stores per contract × visit frequency go up, but only if staffing, routing, and reporting stay clean. More visits help take-home pay only when each extra stop is billed and completed without piling up overtime or rework.

The model shows $1,051M in Year 1 revenue and $12,192M in Year 5 revenue. Marketing divided by CAC implies 48 acquired customers in Year 1 and about 361 in Year 5, but that is acquisition volume, not store count. Here’s the quick math: if audit volume grows faster than labor and QA capacity, margin gets squeezed fast.

Track Volume by Contract, Not Headcount

Use active contracts, stores per contract, and visit cadence as forecast inputs. Then tie staffing to completed visits, not signed deals. If a client adds stores but report review slows, cash gets tied up in unpaid follow-up work, and owner pay drops even when top-line revenue looks better.

- Active contracts

- Stores per contract

- Visits per store

- Auditor hours per route

- Report turnaround time

Track whether each added store still covers field labor, QA, and admin. More volume only helps when the extra visit income beats the cost of travel, photo review, and customer fixes. If onboarding takes too long or routes spread out, gross profit per visit falls and the owner keeps less.

1

Price Per Audit Contract

Price Per Audit Contract

Price per contract sets take-home income because it has to cover audit depth, SKU count, photo proof, and report detail. Year 1 pricing runs from $1,500 to $7,500 a month across four tiers, with weighted monthly revenue per client at $3,650. If the scope is bigger than the fee, the extra review work turns into unpaid admin time.

Here’s the quick math: more detail should mean a higher fee, not just more work. By Year 5, pricing rises to $1,700, $4,000, $8,500, and $6,000. That only helps owner income if reporting standards stay tied to price. One-liner: scope creep kills margin.

Measure Scope, Then Price It

Track SKU count, photo volume, revision time, and report hours by tier. If a deeper audit takes longer, price it as a separate level or charge more per contract. The goal is simple: keep gross margin aligned with the work, so detailed reports stay profitable instead of becoming free labor.

- Match fee to audit depth.

- Count SKUs and photos.

- Measure report time weekly.

- Watch revision requests per client.

- Raise price when scope expands.

2

Route Density

Route Density

Route density is how many audits fit into a paid day without wasted drive time. The model does not give miles or store maps, so field network cost is the proxy. That cost falls from 8% of revenue in Year 1 to 6% in Year 5, which saves about $20,000 per $1,000,000 of revenue.

Same monthly price can still produce very different owner pay. Dense routes cut gaps, mileage, and repeat visits, so more of each contract turns into profit before overhead. If geography is spread out, the same service level can look fine on revenue but weak on cash. One clean route can beat two messy ones.

Cut Travel Waste

Track active stores, stops per route, drive minutes, revisit rate, and field network cost as a share of revenue. If a market pushes network cost above the Year 1 benchmark of 8%, the route is probably too thin. One extra stop on the same drive loop usually lifts margin faster than a price increase.

Before adding a new geography, test whether the contract still clears travel cost at the current fee. If the route needs longer gaps or more repeat visits, the owner is subsidizing field work. Tighten scheduling, cluster stores by area, and drop low-density accounts that pull take-home income down.

3

Field Labor Efficiency

Field Labor Efficiency

Owner income here is what’s left after auditor pay, travel, and completion time. If the owner performs audits, that time is real labor and should be priced in, not treated as free. If hired auditors do the work, the model’s core input is field network cost, which moves from 8% of revenue in Year 1 to 6% in Year 5.

Slower audits raise cost per completed visit. That means the same revenue can produce less take-home pay if routes are messy, reports take longer, or each store takes too many minutes to finish. One clean hour saved can matter more than a small price increase when labor is the main variable cost.

Cut Cost Per Completed Visit

Track minutes per visit, visits per day, travel time, and auditor pay. Here’s the quick math: more completion time means fewer completed visits, so labor cost per visit rises even if pay stays flat. If the owner audits, assign a wage to that time too, or margin will look too high.

- Minutes per store

- Drive time

- Pay per field hour

- Owner labor rate

4

Reporting And QA Workload

Reporting Load

Detailed photo reports can support higher fees, but they also add review time, software cost, revision loops, and customer success work. In this model, cloud and processing fees are 4% of revenue in Year 1 and 3% by Year 5, so the owner’s margin depends on keeping reporting work from growing faster than price.

The key inputs are customer count, audit volume, photo depth, revision count, software spend, and QA staffing. If report standards tighten faster than pricing, each audit takes longer, support load rises, and owner take-home falls even when revenue grows. One extra review step can quietly erase the benefit of a richer report.

Protect QA Margin

Set a cap on reporting cost as a share of revenue, then compare it with the 4% to 3% benchmark. If deeper photo proof or stricter QA rules raise labor, reprice the tier or narrow the report scope so the added work is paid for.

- Track hours per report.

- Count revisions per client.

- Price detailed reports higher.

- Staff QA before delays grow.

5

Recurring Client Retention

Recurring Client Retention

Recurring clients are the revenue seatbelt here. The model uses monthly tiers plus blitz work, so a sticky base of Bronze, Silver, and Gold accounts keeps cash coming in while cutting the need to constantly replace lost work.

The mix shifts from 40% Bronze, 30% Silver, 20% Gold, and 10% blitz in Year 1 to 20% Bronze and 35% Gold by Year 5. No renewal rate is given, so the real test is churn, seasonality, and client concentration; if retention slips, sales spend rises and owner pay gets less predictable.

Track renewal by tier

Measure retained clients by tier, monthly revenue kept, and blitz share. Here’s the quick math: stronger retention raises route density and lowers sales pressure, so the same team can spend more time auditing and less time replacing accounts.

- Track churn by Bronze, Silver, Gold.

- Watch top-client revenue concentration.

- Test seasonality by month and region.

- Separate blitz work from retainers.

If Bronze churns fastest, the mix can drift toward more sales work and less stable cash flow even if headline revenue stays flat. Sensitivity tests should show how a small drop in renewals changes monthly revenue and owner draw.

6

Compare lean, base, and mature owner-income scenarios

Owner income scenarios

Owner income rises as revenue moves from Year 1's $1.051M and -$193k EBITDA to Year 5's $12.192M and $7.140M EBITDA. Marketing, CAC, and cash reserves decide how much can be paid out beyond salary.

| Scenario | Lean CaseLean ramp | Base CaseBase scale | High CaseHigh upside |

|---|---|---|---|

| Launch model | This is the lower-income path, where the launch year still runs at a loss and owner pay stays tight. | This is the modeled middle path, where the business reaches operating scale and owner pay can start to improve. | This is the stronger earnings path, where scale, margin, and lower CAC support the most owner income. |

| Typical setup | Year 1 uses $1.051M revenue, -$193k EBITDA, 88% gross margin after field and cloud costs, $120k marketing, $2,500 CAC, Month 8 breakeven, and $519k minimum cash. | Year 3 uses $4.698M revenue, $1.820M EBITDA, 89.5% gross margin, $350k marketing, and $2,200 CAC, with more room for owner income after reserves. | Year 5 uses $12.192M revenue, $7.140M EBITDA, 91% gross margin, $650k marketing, and $1,800 CAC, with owner distributions still limited by reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary only, no distributionsLean case | Salary plus modest drawsBase case | Salary plus larger drawsHigh case |

| Best fit | Use this to stress-test a cash-tight launch before any owner draws beyond salary. | Use this as the main planning case for steady growth and controlled owner withdrawals. | Use this to test upside if sales scale fast and cash reserves stay strong enough for distributions. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Planogram Compliance Service Porter's Five Forces Analysis

- Planogram Compliance Service BCG Matrix

- Planogram Compliance Service Business Model Canvas

- What Are The 5 KPI Metrics For Planogram Compliance Service Business?

- Planogram Compliance Service Business Plan Template in Pre-Written Word

- How Increase Planogram Compliance Service Profitability?

- What Are Operating Costs For Planogram Compliance Service?

- Planogram Compliance Service Startup Costs: $519k Cash Need

- Planogram Compliance Service Financial Model Template in Excel

- How To Start A Planogram Compliance Service In 6–12 Weeks

- How To Write A Planogram Compliance Service Business Plan?

- Planogram Compliance Service Marketing Mix

- Planogram Compliance Service Marketing Plan

- Planogram Compliance Service Business Proposal

- Planogram Compliance Service PESTEL Analysis

- Planogram Compliance Service Pitch Deck Example Editable PPTX

- Planogram Compliance Service Business SWOT Analysis

- Planogram Compliance Service Value Proposition Canvas

Frequently Asked Questions

The model includes $185k in annual pre-tax CEO salary as owner-manager pay Year 1 EBITDA is -$193k, so that pay is not fully supported by operating profit early on By Year 2, EBITDA reaches $434k, but distributions still depend on reserves, taxes, debt, reinvestment, and cash policy