How Much Plumbing And HVAC Owners Make: $100K Salary Plus Profit

Plumbing and HVAC Bundle

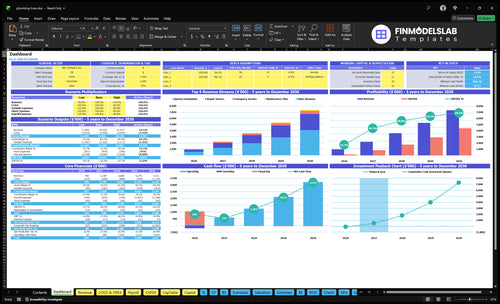

You’re deciding whether ownership beats field wages, so separate booked revenue from cash you can safely pull out This five-year model includes a $100,000 owner/general manager salary, EBITDA from $145,000 in Year 1 to $4402 million in Year 5, payroll, marketing, materials, fleet costs, and reserves It excludes personal tax advice and does not treat profit as automatic distributions

Owner income$245kNet margin17.4%Revenue for target pay$835kBusiness difficultyHard

What could you safely pay yourself?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only; not guaranteed salary, tax advice, or owner distribution advice.

Want to test owner income in the Plumbing and HVAC model?

How much revenue does a plumbing and HVAC business need to pay the owner?

For Plumbing and HVAC, there is no single revenue number that pays the owner. In the Year 1 model, cost support totals $514,300, made up of $372,500 payroll, $91,800 fixed overhead, and $50,000 marketing, and implied operating breakeven is about $704,500 before capex, taxes, debt, and reserves. The model hits breakeven in Month 6.

Year 1 cost stack

$372,500 payroll

$91,800 fixed overhead

$50,000 marketing

$514,300 total support cost

Breakeven read

$704,500 operating breakeven revenue

Before capex, taxes, debt, reserves

Month 6 model breakeven

One owner number won't fit all

What affects plumbing HVAC owner take-home the most?

Plumbing and HVAC owner take-home is driven most by labor productivity, material control, and subcontracted labor, then callbacks, fleet, insurance, dispatch, and marketing efficiency. If you want the setup-cost side of the picture, see What Is The Estimated Cost To Open And Launch Your Plumbing And HVAC Business? because $91,800 in annual fixed overhead means poor job costing can wipe out cash fast.

Biggest margin drains

Year 1 direct materials: 180%

Specialized subcontract labor: 40%

Fleet operating costs: 30%

Marketing support: 20%

What protects owner pay

Hold gross margin on every job

Keep crews booked and moving

Cut callbacks and rework

Use job costing before revenue grows

Does a plumbing and HVAC owner make more than a technician?

Yes, a Plumbing and HVAC owner can make more than a technician, but only when the company earns profit beyond the owner’s own field labor; see What Is The Most Critical Metric For Plumbing And HVAC Business Success? for the metric lens. In this model, the owner/general manager salary is $100,000 versus $75,000 for a lead technician and $50,000 for a junior technician, so the salary gap is real but not risk-free.

Owner Pay

Owner salary: $100,000

Lead tech salary: $75,000

Junior tech salary: $50,000

Lead tech gap: $25,000

Real Upside

Earn through crew leverage

Carry payroll and admin risk

Fund vehicles and insurance

Use EBITDA after reserves

Plumbing and HVAC Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What drives plumbing and HVAC owner income?

1

Service Mix

$120/$110/$180

More emergency and install jobs lift average ticket, and the $120 repair, $110 install, and $180 emergency rates are assumptions, not guarantees.

2

Tech Utilization

2.5-8h

Repair jobs run 2.5 hours and installs 8.0, so tighter dispatch raises paid hours per tech and spreads fixed cost.

3

Gross Margin

22%-16%

Direct project materials start at 18% and ease to 14%, plus subcontract labor falls from 4% to 2%, so margin discipline feeds take-home.

4

Maintenance Plan

15%-55%

The maintenance plan share climbs from 15% to 55%, which brings repeat work and steadier cash between repair spikes.

5

Overhead Control

$91.8K

The $91,800 fixed overhead floor sets the break-even load, so rent, fleet, software, and admin costs need tight watch.

6

Owner Scale

3-11 techs

A $100,000 owner salary sits on top of 3 to 11 field technicians, so owner time has to stay on sales, dispatch, and margin.

Plumbing and HVAC Core Six Income Drivers

Service Mix And Average Ticket

Service Mix and Average Ticket

Income here comes from the mix, not just volume. In Year 1, the disclosed workload is weighted to repair 600, installation 300, maintenance 150, and emergency 100. By Year 5 it shifts to 500, 500, 550, and 100, while rates move from $120 to $140 for repair, $110 to $130 for installation, and $180 to $200 for emergency.

That mix can lift revenue per hour, but only if labor, parts, and callbacks stay in line. Higher-ticket emergency and install work usually look better on paper, yet they can also bring overtime, more truck time, and bigger warranty risk. If margin slips, the owner’s draw gets squeezed even when sales rise.

Track Blended Ticket by Job Type

Here’s the quick math: a stronger blend of installs and maintenance plans should raise average ticket and smooth cash flow. But the owner should watch gross margin by job type, not just top-line revenue. A busier schedule with weak pricing still burns cash.

Track blended rate by job.

Watch maintenance plan close rate.

Measure callback rate on installs.

Log overtime per technician.

Review emergency share monthly.

Measure mix monthly, then price from the bottom up: technician pay, parts, subcontractors, and dispatch time first, markup second. If maintenance plans and installs carry the schedule in Year 5, the business gets more recurring revenue and better forecasting. If estimates lag, the mix can slide back toward low-value repair work fast.

1

Technician Utilization And Billable Hours

Technician Utilization And Billable Hours

This driver is about turning paid technician time into billed work. When routing is tight and callbacks fall, the same payroll produces more revenue and the owner keeps more cash.

Year 1 assumes 25 repair, 80 installation, 8 maintenance, and 20 emergency billable hours per job. By Year 5, those improve to 21, 70, 6, and 16. Idle time, routing gaps, callbacks, and overtime cut owner take-home fast.

Track Paid Hours by Job Type

Measure utilization as the share of paid labor that gets billed. The owner should compare actual job hours, drive time, unbilled time, and overtime against the Year 1 to Year 5 range, then see where time leaks out.

Track billed hours per tech each week.

Log callbacks by job type and technician.

Watch drive time and route gaps daily.

Review overtime against booked demand.

Use first-time fix rate and dispatch discipline to protect margin. If the wrong tech gets sent or the truck has to return, payroll cost rises and owner pay falls even when sales look busy.

2

Gross Margin Discipline

Gross Margin Discipline

If direct project materials run at 180% of revenue in Year 1 and subcontracted specialized labor at 40%, gross margin is already under heavy stress before technician wages, rent, and owner pay. By Year 5, moving those to 140% and 20% is the difference between a busy schedule and real cash flow. One bad pricing model can fill the board and still leave the owner short.

Gross margin discipline means pricing each job against technician wages, parts, equipment, subcontractors, and warranty risk. Use job costing on water heaters, HVAC replacements, drain work, emergency repairs, and warranty labor, because underpriced installs can look productive while quietly draining profit and cash. The key input is full job cost, not just the hourly rate.

Price From Full Job Cost

Track materials % of revenue, subcontracted labor %, and warranty hours by job type. If a quote misses target margin, raise price, cut scope, or walk away before the work starts. Here’s the quick math: every dollar lost in gross margin is a dollar that can’t help cover fixed overhead or owner draw.

Cost every water heater install.

Separate warranty labor from billable labor.

Review margin by job weekly.

Flag jobs below target margin.

3

Recurring Maintenance And Service Agreements

Recurring Maintenance Agreements

Maintenance plans smooth demand, bring repeat calls, seasonal tune-ups, and replacement leads. The model assumes maintenance-plan allocation rises from 150% in Year 1 to 550% in Year 5, while the maintenance rate moves from $90 to $100 per hour. But the plan only lifts owner income if each visit pays for labor, dispatch, reminders, parts, callbacks, and missed appointments.

Here’s the quick math: a visit that falls from 8 billable hours to 6 cuts revenue per visit from $720 to $600, even with the higher rate. That steadier cash flow helps, but it can still squeeze profit if pricing is too low or if free follow-up work piles up.

Price the Plan to Cover the Visit

Track plan count, visit frequency, billable hours per visit, labor time, dispatch time, parts used, callback rate, and missed appointments. The key test is simple: does each plan member pay enough to cover the full service cost and still leave margin for overhead and owner pay?

Test fee against total visit cost.

Watch callback and no-show rates.

Measure billable hours per visit.

Bundle seasonal tune-ups and reminders.

Use replacement leads as upside only.

If the plan fills the schedule but underprices the work, it creates busy months and weak draws. If it covers the real cost of service, it turns uneven demand into more predictable cash flow and steadier profit.

4

Overhead, Fleet, And Insurance Control

Overhead, Fleet, And Insurance Control

Income here is the gap between EBITDA and cash the owner can actually take home. Fixed overhead is $7,650 per month or $91,800 per year, with rent at $3,500, vehicle insurance at $1,200, and utilities, accounting, business insurance, software, admin supplies, and training making up the rest.

Fleet operating costs falling from 30% to 20% of revenue can add real cash, but only if the team keeps response time, safety, and quality intact. One clean rule: cut waste, not readiness. If overhead runs ahead of booked work, owner pay gets squeezed even when sales look fine.

Cut Burn Without Cutting Service

Track fixed overhead, fleet cost as a percent of revenue, vehicle insurance, and cash left after payroll. The right inputs are monthly revenue, job count, miles driven, repair hours, and any added downtime from slower dispatch. Here’s the quick math: every dollar saved in overhead or fleet waste moves straight toward owner draw.

Review overhead monthly against budget.

Measure fleet cost per revenue dollar.

Keep insurance and safety coverage in place.

Test routing before cutting vehicles.

5

Owner Role And Staffing Structure

Owner Role and Staffing

This driver is the shift from owner-as-technician to owner as general manager, dispatcher, estimator, salesperson, or service leader. In this model, the owner takes a $100,000 salary in all five years, while field technicians grow from 3 FTE in Year 1 to 11 FTE in Year 5. That means payroll rises from $372,500 to $945,000, so owner pay only improves if added labor creates more billed work than it consumes.

Here’s the quick math: staffing leverage can raise income, but it also adds supervision, training, scheduling, and quality-control risk. If the owner steps out of the truck but dispatch, estimating, or follow-up slip, callbacks and overtime can eat the gain fast. The key question is simple: does each added technician produce enough billable work to cover the higher payroll base and still leave cash for the owner?

Track Payroll Per Job

Measure payroll as a share of revenue, plus billable hours per technician, callback rate, and booked jobs per dispatcher or service leader. Those inputs tell you whether the owner role is creating real leverage or just adding overhead. If the owner becomes a GM, the schedule must hold up without daily rescue work, because unfilled time, poor routing, and weak estimating turn payroll into a cash drain.

Set a staffing plan that matches the owner’s role to demand. If the owner is selling and managing, document response times, pricing rules, and QC checks so the team can run without constant oversight. Growth should only continue when added technicians improve throughput faster than payroll rises from $372,500 toward $945,000.

6

Plumbing and HVAC Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare reserve-adjusted owner income scenarios

Owner income scenarios

Owner pay rises as the job mix shifts from repairs to installs and maintenance, staffing expands, and EBITDA scales. Distributions should come only after reserves, taxes, debt, and reinvestment.

Three planning cases show how owner income can change as the shop grows.

Scenario

Low CaseLow case

Base CaseBase case

High CaseHigh case

Launch model

This is the lean owner-income path, where pay stays close to the fixed salary and cash is kept tight.

This is the modeled middle path, where scale starts to create room for owner income above salary.

This is the stronger earnings path, where higher volume and staffing support larger owner draws and distributions.

Typical setup

Year 1-style operation with a $100,000 owner salary, $145,000 EBITDA, three field technicians, $372,500 payroll, $91,800 fixed overhead, and a repair-heavy mix that hits Month 6 breakeven.

Year 3-style operation with $1.748 million EBITDA, seven field technicians, a larger install and maintenance mix, and enough scale to pay the owner after reserves, taxes, debt, and reinvestment.

Year 5-style operation with $4.402 million EBITDA, 11 field technicians, and a fuller install and maintenance mix that supports higher owner distributions after business needs are covered.

Cost drivers

Repair-heavy jobs

three field technicians

$372,500 payroll

$91,800 fixed overhead

high materials and subcontract labor

Seven field technicians

more installs and maintenance

higher EBITDA

spread fixed overhead

lower CAC

Eleven field technicians

larger install mix

more maintenance plans

higher EBITDA

lower CAC

Owner income rangeBefore owner reserves

$100,000 salaryLow income

Salary plus distributionsBase income

Salary plus larger distributionsHigh income

Best fit

Use this to test what the owner can take home when growth is slow and cash stays tight.

Use this as the working plan for a growing shop with steady demand and better cash conversion.

Use this to test upside when the team is full, the schedule is dense, and profits can support owner payouts.

!

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The researched model includes a $100,000 annual owner/general manager salary EBITDA adds $145,000 in Year 1 and $4402 million in Year 5, but that is business profit before owner distributions Safe take-home depends on taxes, reserves, debt, replacement vehicles, inventory, and how much cash the company must keep

The model reaches breakeven in Month 6 and shows a 17-month payback period It also needs a minimum cash cushion of $673,000 in Month 5 That cash need matters because early payroll, vehicles, tools, inventory, marketing, and rent hit before every job turns into collected cash

You don’t need them, but they help smooth cash flow when priced correctly In the model, maintenance plan allocation rises from 150% in Year 1 to 550% in Year 5 The catch is simple: tune-up plans must cover technician time, dispatch, reminders, parts, and callbacks

Reserves, taxes, debt service, replacement equipment, and working capital affect distributions For example, Year 1 EBITDA is $145,000, but the business also carries $91,800 in annual fixed overhead and $372,500 in payroll Pulling too much cash too early can leave the company short during seasonal swings or slow collections

The best mix is the one that keeps crews booked and margins intact The model shifts from 600% repair and 300% installation in Year 1 toward 500% repair and 500% installation by Year 5, while maintenance plans rise to 550% Emergency service stays at 100% and carries the highest hourly rate

About the author

Nora Collins

Small Business Writer

Nora Collins is a small business writer for Financial Models Lab who focuses on business affordability analysis for entrepreneurs planning with limited capital. She researches how small businesses launch, operate, and earn money, helping online beginners evaluate business ideas with clear, practical guidance. Her work explains business costs without unnecessary jargon, making financial decisions easier to understand.

Choosing a selection results in a full page refresh.