Pool Plaster Resurfacing Owner Income: $598K Year 1 Model Case

Key Takeaways

Crew capacity, not leads, sets owner income.

Better finish mix helps only with tight cost control.

Payroll growth can quickly eat gross margin.

Cash reserves protect against rework and slow seasons.

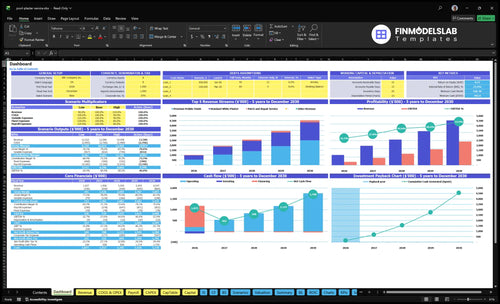

Owner income$336KNet margin32.7%Revenue for target pay$1.03MBusiness difficultyHard

Want to test your pool resurfacing profit calculator?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, taxes, debt, and reinvestment.

Want to see the pool plaster resurfacing financial model?

How does scaling a pool plaster resurfacing business change owner income?

Scaling a Pool Plaster Resurfacing Service can lift owner income, but it also adds payroll, supervision, and quality-control risk. Here’s the quick math: payroll rises from $258K in Year 1 to $732K in Year 5, while revenue grows from $148M to $625M as CAC drops from $450 to $350; an owner-operator may protect early margin, but a crew-managed model usually needs tighter reserves.

Owner-Operator

Protects early margin.

Keeps labor lean.

Stays close to quality.

Limits payroll growth.

Crew-Managed

Frees owner for sales.

Needs more supervision.

Adds scheduling risk.

Requires stronger reserves.

Can a pool plaster resurfacing business support a full-time owner?

Yes, a Pool Plaster Resurfacing Service can support a full-time owner under the model case, but only after job flow covers payroll, overhead, materials, and cash reserves; see How To Start Pool Plaster Resurfacing Service Business? for the setup path. Year 1 shows $1.48M revenue against $436.7K job-variable costs, $258K payroll, $78K fixed overhead, and $12K marketing.

Owner Pay Test

Revenue: $1.48M

Variable costs: $436.7K

Payroll: $258K

Fixed overhead plus marketing: $90K

Risk Check

Owner as General Manager shifts $85K

Profit depends on completed jobs

Weather delays slow cash collection

Callbacks can erase take-home pay

What affects pool plaster business profit margin most?

For the Pool Plaster Resurfacing Service, materials, disposal, and the finish mix move margin fastest; the source data shows Year 1 job-variable costs at 295% of revenue, including 18% plaster and aggregate materials, 5% subcontracted labor, 4% fuel and vehicle maintenance, and 25% disposal, and the weighted hourly price rises from $19,275 to $25,575 as premium pebble mix goes from 30% to 55%. See How Increase Pool Plaster Resurfacing Service Profits? for the profit levers that matter most.

Warranty callbacks are not separately priced in the source data, so add a reserve before taking distributions. That reserve protects owner pay.

Top margin drivers

18% materials cost

25% disposal premium

5% subcontracted labor

4% fuel and maintenance

Pricing changes

Pe pebble mix rises to 55%

Year 1 mix starts at 30%

Hourly price lifts to $25,575

Set a callback reserve first

Pool Plaster Resurfacing Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main pool resurfacing profitability drivers?

1

Owner Take-Home

$336K-$2.4M

EBITDA grows from $336K in Year 1 to $2.4M in Year 5, so every lift in sales and margin flows to owner take-home before tax.

2

Job Volume

$1.0M-$4.5M

Revenue scales from $1.0M to $4.5M as more resurfacing jobs and billable hours get completed.

3

Price Mix

$185-$290/hr

Premium pebble rises from 30% to 55% while hourly rates move from $185 to $290, lifting revenue per job.

4

Crew Productivity

24-28.5 hrs

Billable hours per active customer rise from 24.0 to 28.5 a month, so the same crew can clear more work.

5

Direct Costs

24%-30%

Direct job costs run about 30% of sales in Year 1 and ease toward 24%, which widens contribution margin.

6

Lead Cost

$450 CAC

At a $450 CAC, lead flow must stay efficient, and the $78K fixed overhead plus reserves decide how much cash survives the Month 5 breakeven stretch.

Pool Plaster Resurfacing Service Core Six Income Drivers

Completed resurfacing jobs per month

Completed Jobs That Invoice Cleanly

Completed resurfacing jobs per month is the revenue throttle. The source model assumes 267 Year 1 acquired customers from $12K marketing at $450 CAC, but owner income only rises when crews finish quality work, inspect it, and invoice on time.

Each active customer needs about 24 billable hours per month in the model, and that time has to cover prep, application, curing, travel, disposal, and punch-list work. If weather, crew limits, or callbacks delay completion, revenue slips and cash gets stuck in work-in-progress.

Track Finished Jobs, Not Just Leads

Measure completed jobs, average job hours, callback rate, and days from start to invoice. One clean rule: more booked work helps only when the crew can finish it.

Track jobs closed per week.

Track hours lost to weather.

Track punch-list rework.

Track invoice lag days.

Use those numbers to cap new bookings when capacity tightens. If completion slips, gross margin and owner draw drop even when lead flow looks strong.

1

Average job price and finish mix

Average job price and finish mix

When more jobs shift from patch work to premium pebble, revenue per billable hour rises fast. Year 1’s disclosed blend is $192.75 per hour from 45% standard white plaster at $185, 30% premium pebble at $240, and 25% patch and repair at $150. The owner wins only if crews keep labor hours tight and material waste low.

By Year 5, the weighted rate reaches $255.75 per hour as premium pebble rises to 55%. That helps gross profit and cash flow, but it also raises risk if prep takes longer, repair add-ons pile up, or materials outrun the quote. What this estimate hides: any slip in labor hours or job costing can erase the higher ticket.

Track mix before you chase more volume

Price each job from the inputs that matter: pool size, finish type, surface condition, prep scope, and repair add-ons. The quick math is simple: higher mix of premium pebble should lift revenue per hour, but only if material cost and labor hours stay in line. If bids do not cover extra prep, the owner pays for the gap through lower take-home pay.

Track quoted rate by finish type.

Split jobs by prep scope.

Watch labor hours per pool.

Flag repair add-ons before work starts.

Compare quoted versus actual materials.

Use job-level gross margin, not just revenue, to judge the mix. A premium job that needs more chip-out, bonding prep, or rework can still hurt cash if the quote is thin. The clean benchmark is revenue per billed hour minus direct labor and materials, then test whether the remaining margin can cover overhead and owner pay.

2

Crew productivity and labor model

Crew Productivity and Labor Load

Labor productivity decides whether revenue becomes owner cash or payroll drag. In Year 1, payroll is $258K for a General Manager, Lead Plaster Technician, two Skilled Laborers, and a half-time Office Administrator. By Year 5, it rises to $732K as field, sales, and admin staffing expands, so every idle day, callback, or weak schedule hits owner pay fast.

This model also uses subcontracted specialized labor at 5% of revenue in Year 1, falling to 3% by Year 5. That can reduce owner workload, but it still cuts gross margin. The key inputs are billable hours, crew size, utilization, rework, and subcontract share.

Track labor per finished job

Measure labor hours per completed job, callback rate, and payroll per booked project. If crews spend too much time on prep, curing, travel, or punch-list fixes, payroll grows faster than cash. Here’s the quick read: the tighter the crew schedule, the more of each dollar stays available for owner draw.

Track billable hours by crew

Watch rework and punch-list time

Hold subcontract labor near 3%-5%

Compare payroll to completed jobs

3

Material, prep, and repair costs

Material and Prep Cost Control

When chip-out, bonding prep, acid wash, disposal, and repair surprises run hot, gross margin — the money left after direct job costs — shrinks before overhead. In Year 1, plaster and aggregate materials run 18% of revenue and fall to 16% by Year 5, while fuel and vehicle maintenance run 4% in Year 1.

Waste disposal adds another cost layer, so a strong ticket can still produce weak owner take-home if prep or repair work is underbid. Track direct cost per job and set a reserve for unplanned surface fixes, because every extra rework dollar comes straight out of cash available for payroll, taxes, and the owner draw.

Track Direct Cost per Job

Measure materials as % of revenue, fuel and maintenance, and disposal per job by job type. Split jobs into standard plaster, premium finish, and repair work, then compare planned vs actual cost. If prep hours or callback labor rise, raise price or reserve before owner pay gets squeezed.

Build a job-cost sheet that logs mix usage, haul-off, acid wash, and repair time. The input list is simple: job size, prep scope, repair surprises, disposal volume, and travel miles. If any of those moves up, margin drops fast, and cash collection can lag the work.

4

Lead flow and close rate

Booked Jobs Beat Leads

Lead flow and close rate, the share of leads that turn into booked jobs, decide how much revenue is actually bankable. The key inputs are qualified leads, estimate speed, close rate, and CAC (customer acquisition cost). The source plan uses $12K in Year 1 marketing at $450 CAC, then $25K at $350 CAC by Year 5, so lower selling cost matters as much as higher traffic.

Profitable booked jobs matter more than raw leads. If the schedule fills with low-margin repair-only work, gross margin and owner pay can fall even while the phone rings. Faster estimates, better photos, and stronger reviews help win full resurfacing jobs, which are the jobs that most improve cash flow and keep cash available for payroll, overhead, and the owner draw.

Lower CAC, Raise Close Rate

Track lead source, estimate-to-close rate, and booked-job margin by job type. Referrals, pool service partnerships, fast estimates, before-and-after photos, reviews, and seasonal timing should lower CAC and lift close rate. The source plan ties 267 acquired customers to the Year 1 budget path and 714 acquired customers to the Year 5 path at $350 CAC, so even small conversion gains can move owner income.

Quote same day on hot leads.

Track close rate by source.

Reject weak repair-only jobs.

Use photos to build trust.

What this estimate hides: weather, pool season, and crew capacity can delay booking even when lead volume looks strong. If estimates take too long or the calendar fills with small repairs, invoicing slows and cash gets trapped in busy, low-value work instead of reaching the owner.

5

Overhead, reserves, and cash-flow discipline

Fixed overhead and reserve load

If jobs are busy but the bank balance stays thin, $65K/month of fixed overhead is eating the spread before the owner gets paid. The named costs total $48,800 — $35K rent, $12K insurance, $450 utilities and internet, $200 licensing, $350 software, and $800 accounting and legal — so another $16,200 sits in other fixed costs.

That means revenue must cover overhead, then still leave cash for warranty, slow-season, debt-service, and tax reserves. The listed $972K startup capex also raises the cash bar, so operating profit is not owner income until those buckets are funded.

Pay yourself after the reserve check

Track monthly fixed overhead on collected revenue, not booked sales, because slow collections can make a profitable month look safe when it is not. Here’s the quick math: if overhead stays near $65K, the business needs enough gross margin and cash conversion to clear that number before owner draw starts.

Use collected revenue, not booked jobs.

Track overhead every month.

Set warranty, tax, and slow-season reserves.

Match debt payments to cash timing.

Set reserve buckets in the cash forecast and fund them before distributions. Review them weekly against actual jobs, collections, and payment dates, and keep owner pay last in line. One clean rule: no owner distribution until the reserve balance is funded for the month.

6

Pool Plaster Resurfacing Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high pool plaster income scenarios

Owner income scenarios

Owner income moves with job mix, staffing, and capacity. Use these cases to see how a pool plaster resurfacing service can shift from a Year 1 buildout to a Year 5 scale-up.

Low, base, and high owner income cases for planning.

Scenario

Low CaseLean case

Base CaseBase case

High CaseUpside case

Launch model

Lower case assumes a Year 1-style ramp with lighter volume and early-stage capacity.

Base case assumes the Year 3 model with a steadier booking pace and fuller crew use.

High case assumes the Year 5 model with stronger close rates and more capacity on the road.

Typical setup

Revenue is closest to Year 1 at $1.027M, EBITDA is $336K, and the business is still carrying startup overhead and the first equipment buildout.

Revenue reaches $2.592M, EBITDA is $1.157M, and mix shifts toward premium pebble finish as the sales role is in place.

Revenue reaches $4.547M, EBITDA is $2.406M, and premium pebble finish makes up most jobs while the crew is fully built out.

Cost drivers

Lower job volume

higher CAC

fixed payroll load

yard and office overhead

Premium job mix

higher billable hours

added sales coverage

stable fixed overhead

Premium job mix

higher utilization

larger crew

more sales coverage

lower unit CAC

Owner income rangeBefore owner reserves

$336KYear 1 case

$1.157MYear 3 case

$2.406MYear 5 case

Best fit

Fits founders stress-testing the first operating year and slower booking ramps.

Fits owners planning a steady-state operating year once the shop and crew are running at scale.

Fits teams testing upside if demand, pricing, and staffing all hold together.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In the researched Year 1 model, pre-tax cash after listed startup capex is about $598K That comes from $148M revenue, 705% contribution margin before payroll, $258K payroll, $78K fixed overhead, $12K marketing, and $972K startup capex Taxes, debt, warranty reserves, and owner distributions are not included

Seasonality can affect cash flow as soon as booked work, weather, and collections become uneven The model uses annual figures, including $148M Year 1 revenue and $29K monthly fixed burden before job-variable costs If a slow month still carries payroll, rent, insurance, and marketing, the owner needs cash reserves before taking full distributions

This model assumes a crew from launch month, not a solo plaster operator Year 1 payroll includes one General Manager, one Lead Plaster Technician, two Skilled Laborers, and a half-time Office Administrator for $258K total That staffing supports revenue capacity, but it also raises the break-even bar before owner take-home is safe

Full resurfacing usually drives more revenue per customer because it carries more billable hours In the model, standard plaster uses 32 hours, premium pebble uses 48 hours, and patch and repair uses 8 hours Patch work remains 25% of mix across the five years, so too much repair-only work can lower average ticket and crew utilization

Hire sales help when estimates, follow-up, and close rate are limiting profitable booked work The model adds one Sales and Estimating Representative in Year 2 at $55K and grows to two by Year 4 That makes sense only if the added booked revenue covers payroll, CAC, materials, subcontracted labor, and reserve needs

About the author

Michael Porter

Entrepreneurship Researcher

Michael Porter is an entrepreneurship researcher at Financial Models Lab who helps founders opening a new small business turn big questions into clear planning steps. He focuses on expense and revenue planning for the first year, keeping attention on useful numbers and realistic expectations. His work gives business plan writers practical guidance without sugarcoating the challenges ahead.

Choosing a selection results in a full page refresh.