How Much Posture Correction Service Owners Make At $48k Per Month

Posture Correction Services

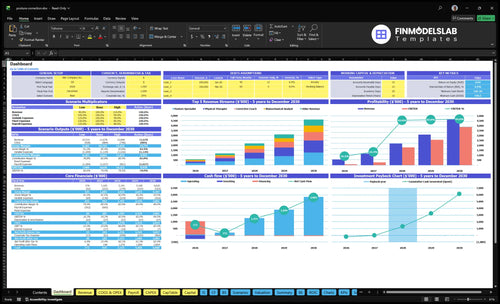

A posture correction business owner can plan around a modeled $145,000 annual owner salary, but first-year operations do not fully fund it under the researched assumptions Here’s the quick math: first-year revenue is about $48,035/month, contribution margin after listed variable costs is about 79%, and fixed overhead plus payroll is about $44,458/month That leaves roughly -$6,511/month after the modeled owner salary, before capex, taxes, debt service, reserves, and reinvestment By the mature year, modeled revenue reaches $385,000/month, but practitioner compensation rates are not supplied, so any extra owner distributions must be tested carefully

Owner income$145kNet margin79%-84%Revenue for target pay$1.18MBusiness difficultyHard

Want to test your own owner-pay number?

Owner income calculator

Estimate owner take-home from monthly revenue, gross margin, payroll, fixed overhead, reserves, and a target pay goal.

!

Planning note This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Posture Correction Services forecast?

How much revenue does a posture correction service need to pay the owner?

If Posture Correction Services wants to pay the owner $145,000 in Year 1, it needs about $56,276/month in revenue at a 79% contribution margin. With $44,458/month of fixed overhead and payroll, current Year 1 revenue of $48,035/month leaves an $8,241/month gap, so the clinic is close but not there yet.

Owner pay math

$56,276/month needed for owner pay

79% contribution margin used

$44,458/month fixed overhead and payroll

Separate profit from cash reserve needs

Current gap

$48,035/month current Year 1 revenue

$8,241/month short of target

$117 average realized treatment value

About 71 more treatments monthly

What is the posture correction service profit margin?

For Posture Correction Services, use margin as a planning output, not a universal benchmark. Year 1 gross margin is 91% because COGS are 9% of revenue, and contribution margin after marketing and payment fees is 79%; see What Are The 5 KPI Metrics For Posture Correction Services? for the KPI set behind that. Fixed overhead is $17,000/month, payroll including owner salary is $27,458/month in Year 1 and $46,583/month in Year 5, so no-shows, low utilization, high acquisition cost, or unmodeled practitioner pay can cut owner take-home fast.

Year 1 margin

91% gross margin

9% COGS of revenue

79% contribution margin

$17,000 fixed overhead monthly

Year 5 pressure

84% mature-year contribution

$27,458 Year 1 payroll

$46,583 Year 5 payroll

No-shows hurt take-home fast

How does solo vs staffed posture correction business income change owner pay?

Posture Correction Services gives a solo owner better margin per session, but pay is capped by the owner’s own clinical hours. In the staffed model, Year 1 runs at 45% to 60% utilization, so payroll and rent hit before the clinic is full; by Year 5, the model reaches 23 clinical roles and $385,000/month in revenue. So, separate owner wage replacement from true business profit.

Solo model

Keeps more margin per session

Caps income at owner hours

Needs no staff payroll

Scales slower than a clinic

Staffed clinic

Starts with 6 roles

Year 1 utilization is 45% to 60%

Payroll and rent hit early

Year 5 reaches $385,000/month

Posture Correction Services Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers that control owner income?

1

Assessments

$48K-$385K/mo

Track booked assessments and conversion, because they move revenue from about $48K/month in Year 1 to $385K/month in Year 5.

2

Capacity Use

45%-85%

Track therapist capacity, because moving utilization from 45% to 85% raises billable visits without adding the same overhead.

3

Overhead

$17K

Track fixed overhead and marketing rate, because $17K/month plus 9% to 6% acquisition spend can wipe out take-home.

4

Pricing Power

$117-$135

Track realized treatment value, because $117 to $135 per visit lifts cash on every sale.

5

Staffing

4-8 FTE

Track FTE growth, because adding staff too early pushes labor ahead of demand and trims owner draw.

6

Add-ons

7%-9%

Track add-on mix, because devices and software only add margin if the 7% to 9% product cost stays controlled.

Posture Correction Services Core Six Income Drivers

Assessment Volume And Conversion

Assessments drive revenue

More qualified assessments lift revenue before rent and admin catch up. In Year 1, the model depends on 412 delivered treatments per month across five service roles, so the real lever is getting assessment volume to convert into paid care. Volume matters, but only if the plan stays ethical and clear.

Track the funnel

Watch new assessments, show rate, conversion to paid programs, and cost per booked assessment. That’s the funnel that tells you whether growth is real or just busy work. If cost per booked assessment rises while conversion slips, owner pay gets squeezed fast.

Booked assessments

Show rate

Paid-program conversion

Cost per booked assessment

Keep onboarding tight

Use realistic care plans and plain-language recommendations, not aggressive medical claims. If onboarding takes too long, conversion and retention suffer, so the first visits should make next steps obvious, simple, and doable. Shorter setup usually helps more than adding extra promises. Simple wins here.

Close the Year 1 gap

The owner-pay gap is about $8,241 per month in Year 1, which equals roughly 71 more delivered treatments at the $117 realized average. That is the cleanest planning target: add treatments that convert, then protect margin with steady follow-up and tight scheduling.

Package Pricing And Client Value

Price for value

For posture correction services, Year 1 prices in research ranged from $85 to $180 per treatment, then moved to $105 to $200 by Year 5. The weighted realized value rose from about $117 to $135 per delivered treatment, so price is a planning lever, not a guarantee that every market will pay more.

Track realized value

Owner income improves when you track average realized treatment value, package close rate, sessions per client, and refund rate. Here’s the quick math: sticker price tells you less than what clients actually pay after discounts, refunds, and incomplete plans. One clean number: realized value is the number that pays labor and overhead.

Watch realized value, not list price.

Count sessions per client.

Log refunds fast.

Test market fit

Use assessments to sell structured packages, memberships, or multi-session plans only if the math still leaves room for labor and overhead. Test cash-pay affordability, visit frequency, and clear client outcomes before pushing rates higher. What this estimate hides: a weak close rate or high refunds can wipe out the gain from a higher posted price.

Margin first

Structured plans work only when package margin covers practitioner labor, rent, and admin time. If a multi-session plan is priced well but delivers too many low-margin visits, owner income stalls. If it’s priced right and clients stay on plan, you get steadier cash flow and less one-off selling pressure.

Utilization And Schedule Density

Filled slots pay

Owner take-home rises when paid visits fill the calendar without burning out providers. In year 1, 45% utilization is a realistic start for biomechanical analysis and 60% for physical therapy. In a mature year, target 75% to 85%. Keep one eye on $17,000 monthly fixed overhead, because empty slots still cost money.

Track the gaps

Watch appointment fill rate, provider hours, cancellations, no-shows, and admin time. Here’s the quick math: utilization is the share of paid time versus available time, so a full schedule does not matter if cancellations leave gaps. One clean rule: track the holes daily, not monthly.

Measure paid slots by provider

Log no-shows every week

Count admin hours separately

Protect owner time

Reserve blocks for assessments, follow-ups, documentation, and team management, or the owner ends up doing unpaid catch-up work. That time protects quality and keeps the schedule honest. If these blocks are ignored, provider burnout rises and utilization looks better on paper than it does in cash.

Every empty slot hurts

An empty visit loses revenue but still carries rent, software, staff time, and marketing spend. So the real job is schedule density: keep enough paid visits stacked into the week to cover fixed overhead, but leave enough space for admin, recovery, and clean delivery.

Staffing Costs And Owner Role

Owner Role

A solo owner keeps more gross margin per session, but a staffed model can grow revenue and cut delivery hours. The trade-off is simple: if the owner is still seeing clients, track revenue per provider, not just total sales. If training takes too long, margin slips fast.

Payroll Base

Year 1 payroll totals $329,500. The model includes $145,000 CEO and Clinical Director pay, $75,000 for operations, $42,000 for front desk, $65,000 sales, $55,000 marketing, and $70,000 IT support where used. Before hiring, enter practitioner compensation rates so true provider margin is clear.

Staffing Control

Watch payroll as a percent of revenue, utilization by role, and training time. That is the quick math. A role can look affordable on salary alone, but if a provider is underbooked or slow to ramp, the real cost rises. Trim payroll only where it does not hurt service quality or client flow.

Break-Even Check

Before adding staff, set a target for monthly provider hours and the minimum revenue per provider needed to cover wages, training, and overhead. If the owner also delivers sessions, separate owner pay from business profit so you do not mistake busy schedules for healthy margins.

Device And Product Add-On Margin

Add-On Margin

Devices, bands, ergonomic accessories, and home-exercise tools can lift revenue, but only when they boost attachment rate and average device sale. Here’s the quick math: researched inventory cost is 6% of revenue in Year 1 and 5% by Year 5; diagnostic software fees add 3% then 2%. Keep product sales secondary to service economics.

Startup Cost

This cost covers device stock, bands, fit kits, storage, and the software used to track add-on sales. Estimate it with units × unit cost, plus months of coverage and reorder frequency. Using the research inputs, inventory and software together start at about 9% of revenue in Year 1 (6% + 3%).

Model sell-through before reordering

Separate demo stock from clinic stock

Track returns by SKU

Cash Control

Buy in small lots and tie restocks to booked visits, not hopeful demand. Slow-moving inventory traps cash, so watch shelf age and returns. The margin stack improves by Year 5, when inventory is 5% and software is 2% of revenue, but only if product sales stay secondary to service economics.

Order only fast-turn items

Review shelf time monthly

Cut dead SKUs fast

Use, Don’t Push

Do not treat devices as medically necessary for every client. Use them when they support the plan and improve adherence, because the real win is better service margin, not retail volume. If returns rise or inventory turns slow, cash stays on shelves and owner pay drops.

Overhead And Acquisition Efficiency

Fixed overhead

$17,000/month in fixed overhead is the base load, and $12,000 of that is rent. That means rent is about 71% of fixed cost. Track overhead per treatment by dividing fixed overhead by monthly treatment volume, because owner take-home only works when recurring visits stay dense enough to absorb that base.

Acquisition spend

Digital marketing and lead acquisition run at 9% of revenue in Year 1 and 6% by Year 5. Payment processing stays at 3%. So the non-labor drag is 12% early and 9% later, before rent, software, insurance, and admin. Referrals and retention matter because they lower paid lead demand.

Cash reserve

A clinic can show accounting profit and still run short on cash if reserves, capex (equipment spend), and owner pay are not set aside. Use reserve-adjusted cash flow, not profit alone, to judge what is safe to draw. One missed equipment cycle can wipe out a good month.

Take-home rule

Owner take-home tracks recurring client volume more than gross revenue. If visits wobble, fixed overhead stays put, so the first job is to cover rent, software, insurance, admin, and processing; only then should marketing and owner draws scale. That’s the clean test for whether the model is paying the owner or just feeding the profit report.

Posture Correction Services Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, break-even, and growth owner-income scenarios

Owner income scenarios

Owner income swings with treatment volume, realized price, and practitioner payroll. Fixed clinic costs and no-shows keep even solid revenue from flowing straight to the owner.

Three income cases for planning staffing, pricing, and break-even.

Scenario

Low CaseDownside

Base CaseBreak-even

High CaseUpside

Launch model

This is the downside case, where early volume covers part of the clinic load but not full owner pay.

This is the modeled case, where the clinic reaches owner-pay break-even at stable treatment volume and pricing.

This is the stronger earnings path, where mature-month volume is high and margin improves if labor stays tight.

Typical setup

At $48,035 monthly revenue and 412 delivered treatments, the model runs at about 79% contribution margin, with $27,458 payroll including the owner and about -$6,511/month after owner salary.

At about $56,276 monthly revenue and 483 delivered treatments, the model reaches the break-even owner-pay point at the same 79% contribution margin with $44,458 fixed overhead plus payroll.

At about $385,000 monthly revenue and 2,852 delivered treatments, the model reaches 84% contribution margin, but owner income still depends on whether payroll, rent, marketing, and no-shows stay controlled.

Cost drivers

patient volume

realized treatment value

payroll including owner

fixed clinic overhead

no-show rate

treatment volume

pricing mix

practitioner staffing

rent and admin cost

no-show control

treatment volume

contribution margin

practitioner payroll

rent and marketing

no-show control

Owner income rangeBefore owner reserves

-$6,511/monthLoss case

Around break-evenCore case

Higher upside, cost-sensitiveUpside case

Best fit

Use this to stress-test early launch months, slower referrals, or heavier payroll before volume ramps.

Use this as the main planning case for budgets, hiring, and owner pay.

Use this to test what happens if volume scales fast without letting costs outrun margin.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or profit distributions.

The model includes $145,000 in annual CEO and Clinical Director salary, or about $12,083/month before taxes But first-year operations produce about $48,035/month in revenue and run about $6,511/month short after that salary, before capex, reserves, debt service, and taxes So the salary may need startup capital, slower draws, or more volume

Under the Year 1 assumptions, the clinic needs about $56,276/month in revenue to fund the modeled owner salary and listed payroll at a 79% contribution margin The forecast starts at about $48,035/month, so the gap is roughly $8,241/month That is about 71 more delivered treatments at the $117 realized average treatment value

The research context does not include insurance reimbursement assumptions, so profitability should be tested on the entered pricing and volume Year 1 treatment prices range from $85 to $180, and Year 5 prices range from $105 to $200 If you add billing, model collection delays, denials, admin labor, and payer-specific rates separately

Utilization, pricing, payroll, and fixed overhead move profit the most Year 1 utilization ranges from 45% to 60%, fixed overhead is $17,000/month, and marketing plus payment fees total 12% of revenue If appointments go empty or acquisition cost rises, owner take-home drops even when the clinic has good service pricing

Hire when demand is repeatable and schedule density can cover payroll, not just when leads increase The model starts with multiple clinical roles and $329,500 in Year 1 payroll, including owner salary Before adding staff, track revenue per provider, utilization, cancellations, and whether new hires will raise cash flow after training, supervision, and admin time

About the author

Anthony Ross

Independent Business Researcher

Anthony Ross is an independent business researcher at Financial Models Lab who writes practical guides for first-time entrepreneurs planning their first business. Focused on small business money management, he helps readers organize broad business ideas into clear planning assumptions, with straightforward revenue and profit examples that make financial thinking easier to apply.

Choosing a selection results in a full page refresh.