Owner income$165k

Owner income$165kHow Much A Power Factor Correction Service Owner Can Make At $350k Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$165k  Net margin25%–62%

Net margin25%–62% Revenue for target pay$665k

Revenue for target pay$665k Business difficultyHard

Business difficultyHard

A power factor correction service owner may draw an estimated $165,000 before personal taxes in this model, but that is modeled owner salary, not guaranteed profit The business produces $350,000 in Year 1 revenue and $228 million by Year 5, with contribution margin improving from 687% to 756% After payroll, fixed overhead, and marketing, EBITDA remains negative in the researched base case, so distributable profit is modeled at $0 Revenue is not income, and reserves reduce cash the owner can safely take home

Owner income$165kNet margin25%–62%Revenue for target pay$665kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It excludes financing approvals and guaranteed savings.

Want to see the full financial model for Power Factor Correction Service?

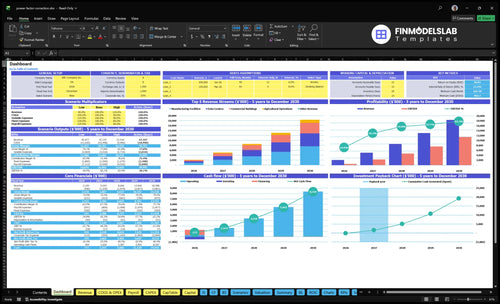

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Power Factor Correction Service Financial Model Template. Open the model to test scenarios.

Owner-income model highlights

- Owner pay scenario views

- Revenue and margin charts

- Test close rate, CAC

Can a power factor correction service support a full-time owner?

Yes, a Power Factor Correction Service can support a full-time owner, but not from true operating profit in Year 1. In the researched base case for How Do I Write A Business Plan To Launch Power Factor Correction Service?, revenue is $350,000 while owner pay is modeled at $165,000, so payroll, marketing, and fixed overhead need outside funding or retained cash during the ramp.

Base Case

- Year 1 revenue: $350,000

- Owner CEO/lead engineer pay: $165,000

- Payroll, marketing, fixed overhead: $854,000

- Overhead equals about 244% of revenue

Owner Pay Reality

- Pre-direct-cost funding gap: $504,000

- Owner pay equals 47% of revenue

- Salary is separate from business profit

- Distributions need positive EBITDA after reserves

How does scaling a power factor correction business change owner income?

Power Factor Correction Service can grow revenue much faster than owner income at first, because owner-installed work keeps margins cleaner. In the model, revenue rises from $350,000 to $228 million, while payroll climbs from $434,000 to $1,398 million; fixed overhead stays at $300,000 a year and marketing grows from $120,000 to $350,000.

Early margin helps

- Owner-led installs keep labor lean

- Less supervision cuts overhead pressure

- Fewer vehicles means lower cash use

- Simpler scheduling reduces delay risk

Growth adds drag

- Add electricians and project managers

- Hire field techs, sales, and quality roles

- Safety controls and licensing add cost

- Working capital needs rise fast

How much revenue does a power factor correction business need?

Power Factor Correction Service needs about $1.24 million in Year 1 revenue to cover the modeled $854,000 cost base at a 68.7% contribution margin; actual Year 1 revenue is $350,000. By Year 5, the $2.048 million cost base and 75.6% margin point to about $2.71 million in break-even revenue, and the $165,000 owner salary is part of that load. Here’s the quick math: cost base divided by contribution margin equals break-even revenue.

Year 1 break-even

- $854,000 modeled cost base

- 68.7% contribution margin

- Break-even near $1.24 million

- Actual revenue is $350,000

Year 5 break-even

- $2.048 million modeled cost base

- 75.6% contribution margin

- Break-even near $2.71 million

- Lead conversion and project size drive the gap

Want the six main income drivers?

1

50-200Site Surveys

More qualified surveys and better close rates turn the 50 to 200 customer pipeline into booked work, which moves revenue and owner pay fastest.

2

$7K-$11.4KProject Value

Each sold job sits around $7,000 to $11,388 per customer, so better pricing lifts revenue and EBITDA without more trucks or heads.

3

30-70 hrsTechnician Use

Keeping crews busy across 30 to 70 billable hours by segment spreads labor over more revenue and protects EBITDA.

4

74%-79%Equip Margin

Capacitor bank equipment and install costs run about 26% in year 1 and 21% by year 5, so tighter buying and install control drops straight to margin.

5

$1.75K-$2.4KCAC Cycle

Lower CAC and a shorter sales cycle cut cash needed to land each project, so more of the budget turns into profit.

6

UpsideRecurring Add-ons

The base model has no separate recurring revenue, so any service add-on adds high-margin income after the initial install.

Power Factor Correction Service Core Six Income Drivers

Qualified Site Surveys And Conversion

Qualified Site Survey Conversion

Qualified commercial and industrial site surveys are the gate to installation revenue. Here’s the quick math: $120,000 marketing budget ÷ $2,400 CAC = 50 customers in Year 1, and $350,000 ÷ $1,750 = 200 customers by Year 5. The best-fit sites are manufacturing plants, commercial buildings, data centers, and farm operations where demand charges or utility penalties are real.

Weak qualification burns unpaid estimating time and slows owner pay. A bad-fit lead can still take bill review, a site visit, and proposal work, but never close. Better conversion raises revenue without the same fixed overhead jump, so each installed job carries more of the office cost. Don’t use residential-style lead assumptions; one industrial win can be worth many small leads.

Qualify Before You Survey

Ask for utility bills, penalty history, peak kW, and the monthly bill swing before you book the truck. If there is no demand-charge pain, the lead is usually low value. That keeps the team from spending hours on sites that won’t produce enough margin to justify the trip.

Track survey-to-close rate, hours per estimate, and cost per qualified opportunity. Improve scripts, referral targets, and pre-site screening so the team spends time on sites with a real ROI case. Fewer weak surveys means more cash from the same labor and less working capital tied up in unpaid proposals.

- Marketing budget

- CAC and close rate

- Demand-charge pain

- Estimate hours

1

Average Project Value

Average Project Value

Average project value is the revenue you book per installation, driven by facility type, billable hours, and hourly rate. In Year 1, it ranges from $4,200 for agricultural operations to $10,175 for data centers. That spread matters because it changes how fast revenue grows without adding the same number of leads.

Bigger kVAR jobs, meaning larger correction loads, can lift contract value, but they also raise engineering, equipment, scheduling, and working capital needs. A larger ticket only helps owner pay if gross margin and cash timing stay strong; otherwise, the job can look big on paper and still pinch cash.

Price by scope, not by average

Build each quote from the site survey, not a flat guess. Track facility type, billable hours, hourly rate, and kVAR size. The model shows Year 5 revenue per customer of $7,200 to $15,750, so mix matters. If more jobs are data centers, revenue per project rises, but labor and cash tied up in equipment can rise too.

- Track billable hours per job

- Track equipment deposit timing

- Track change orders and rework

- Track gross margin by facility type

If a project needs more engineering or a longer install window, price that in. Bigger jobs should pay for the extra work and working capital, not just add top-line revenue.

2

Capacitor Bank Equipment Margin

Capacitor Bank Equipment Margin

Capacitor bank margin is the spread between what the customer pays and what the equipment, materials, and subcontractors cost. In this model, equipment and capacitor banks cost 180% of revenue in Year 1 and 150% in Year 5, while install materials and subcontractors add 80% and 60%. That puts direct COGS at 260% in Year 1 and 210% in Year 5, so gross profit before overhead is under pressure.

One clean rule: if procurement slips, owner pay shrinks fast. Here’s the quick math: every extra point of supplier price, freight, warranty reserve, or change-order leakage hits cash before overhead is covered. Equipment gross margin is not total business profit, so the owner has to protect markup on each job, not just win the bid.

Control Purchase Price and Scope

Track three inputs on every job: equipment cost, install labor and subcontractor cost, and freight or change-order recovery. If the quoted price does not cover all three, the job can create revenue but still reduce take-home income. Keep a simple job sheet that compares planned margin to actual margin after delivery.

- Quote freight before signoff.

- Price change orders in writing.

- Reserve for warranty callbacks.

- Review supplier quotes each job.

Use the same margin check on every facility type, because bigger kVAR jobs can also mean more engineering and more working capital. Markup discipline matters more than size: a larger install with weak pricing can drain cash faster than a smaller one with clean scope control.

3

Technician Utilization And Labor Control

Technician Utilization

For power factor correction work, owner income rises when more tech time is billable and less time is lost to rework. The model’s billable hours run from 30-55 for agricultural operations, 35-45 for commercial buildings, 45-55 for manufacturing facilities, and 55-70 for data centers, so the facility mix changes margin and cash flow fast.

As licensed electricians scale from 20 FTE to 60 FTE, scheduling, commissioning, the final test-and-signoff step, and callback control become the profit levers. Safety, licensing, testing, and quality checks are constraints, not optional costs. Cut labor too hard, and you invite rework, liability, and lost trust that can shrink owner take-home.

Control Labor Hours

Track survey hours, install hours, commissioning hours, and callback rate by facility type. Compare each job to the benchmark range before you approve the work. If a project needs extra travel, testing, or a second visit, the extra revenue can disappear into labor even when the contract looks strong.

- Price repeat visits separately.

- Schedule testing before crew release.

- Use a closeout checklist.

- Flag callbacks by cause.

That keeps more crew time billable and protects owner draw.

4

Customer Acquisition Cost And Sales Cycle

CAC and Sales Cycle

Customer acquisition cost (CAC) is the cash spent to win one new customer, including marketing, proposal work, utility bill analysis, site visits, and trust-building with facility managers. Here’s the quick math: $120,000 of Year 1 marketing at $2,400 CAC implies about 50 customers; by Year 5, $350,000 at $1,750 CAC implies about 200 customers. If close rates lag, unpaid estimating time cuts owner take-home pay before any installation cash lands.

This driver matters because B2B sales cycles are cash-hungry. A longer cycle means more labor is spent on bids and visits before revenue closes, so gross profit has to cover that delay. Better qualification, referrals, and repeat facility groups lower CAC and improve cash conversion, which helps the owner pay themselves sooner instead of funding slow sales work out of pocket.

Cut Waste in the Sales Cycle

Track lead source, proposal hours, site visits, close rate, and days to close by facility type. The best-fit leads are plants, commercial buildings, data centers, and agricultural sites with penalty or demand-charge pain. One clean filter is better than ten weak bids. If estimating time is high and close rate is low, CAC is not just a marketing issue; it is a labor and cash flow problem.

- Qualify before bill analysis.

- Push referrals from similar facilities.

- Price paid surveys when needed.

- Track win rate by facility type.

- Limit free design work on weak leads.

Use the Year 1 to Year 5 shift as a control point: $2,400 CAC down to $1,750 only helps if the sales team spends less time per win. If proposals keep piling up without closes, the owner funds the gap and income gets delayed. Faster qualification improves cash conversion, so more of the marketing dollar turns into install work, not dead time.

5

Recurring Service Add-Ons

Recurring service add-ons

Inspection, monitoring, and preventive maintenance can smooth cash between install-heavy months, but the base model does not show a separate recurring revenue line. So this should stay secondary unless you add contracts as an explicit input.

These add-ons can include capacitor bank inspections, power quality monitoring, periodic testing, and maintenance visits. The owner’s income depends on contract count, price per contract, visit frequency, labor hours, travel time, and documentation time. One-liner: if the fee does not cover field time and reserve coverage, it does not lift take-home pay.

Track the true recurring load

Measure recurring work by contract count, visit hours, callback rate, and miles per visit. Use a simple test: recurring revenue minus labor, travel, documentation, and reserve coverage must stay positive. If the service keeps technicians busy without enough margin, it can raise revenue and still cut owner draw.

Keep it tied to installs. Add monitoring or maintenance only when it improves retention and scheduling, not as a stand-alone growth bet. The clean metric is cash contribution per active contract; if that slips as volume rises, the work is adding sales but not real profit.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner pay depends on close rate, project value, staffing, and whether reserves cover growth. Early on, distributions can stay at $0 even when revenue is rising.

| Scenario | Low CaseOwner-operated | Base CaseStaffed ramp | High CaseGrowth case |

|---|---|---|---|

| Launch model | This is the lower-income path, with the owner still covering most sales and field work. | This is the modeled case, where the owner pays salary first and distributions stay at $0 until profit and reserves support them. | This is the upside path, where higher close rates and larger projects can support owner pay beyond salary. |

| Typical setup | It assumes fewer acquired customers, lower project values, tighter close rates, and lean overhead with no distributions. | It assumes 50 to 200 acquired customers, $25,000 monthly fixed overhead, $165,000 owner salary, and payroll plus marketing that support steady delivery. | It assumes stronger customer acquisition, bigger projects, more crews, and reserves that can fund distributions after operating profit. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $165,000 salary onlyConservative | $165,000 salary plus modest distributionsModeled case | Salary plus upside distributionsUpside case |

| Best fit | Use this to stress-test the business if demand is thin or sales cycles run long. | Use this as the working plan for a staffed operation with profits building after fixed costs. | Use this to test what happens if demand, pricing, and staffing all work in the owner's favor. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Power Factor Correction Service Porter's Five Forces Analysis

- Power Factor Correction Service BCG Matrix

- Power Factor Correction Service Business Model Canvas

- What Are The 5 KPIs For Power Factor Correction Service Business?

- Power Factor Correction Service Business Plan Template in Pre-Written Word

- How Increase Profits Power Factor Correction Service?

- What Are Operating Costs For Power Factor Correction Service?

- Power Factor Correction Service Startup Costs: $462K CAPEX Plan

- Power Factor Correction Service Financial Model Template in Excel

- How to Start a Power Factor Correction Service in 8–16 Weeks

- How Do I Write A Business Plan To Launch Power Factor Correction Service?

- Power Factor Correction Service Marketing Mix

- Power Factor Correction Service Marketing Plan

- Power Factor Correction Service Business Proposal

- Power Factor Correction Service PESTEL Analysis

- Power Factor Correction Service Pitch Deck Example Editable PPTX

- Power Factor Correction Service Business SWOT Analysis

- Power Factor Correction Service Value Proposition Canvas

Frequently Asked Questions

The researched model shows $165,000 in owner salary before personal taxes, but no modeled distributions Revenue rises from $350,000 in Year 1 to $228 million in Year 5 Because payroll, marketing, fixed overhead, and reserves absorb cash, owner salary and true business profit should be viewed separately