How Much Power Bank Rental Owners Make With 50 First-Year Stations

A power bank rental business owner can make meaningful income, but only after revenue clears venue commissions, payment fees, replacements, logistics, marketing, and reserves In the researched first-year case, 50 acquired venue partners and 10,000 acquired buyers produce about $639,081 in revenue Direct and variable costs total 175%, leaving about $527,242 before acquisition marketing After $200,000 in seller and buyer marketing, pre-tax cash before unlisted overhead is about $327,242, which is not the same as guaranteed owner take-home

Owner income$327k/yrNet margin51%Revenue for target pay$53.3k/moBusiness difficultyHard

Could your station route pay your target owner draw?

Owner income calculator

Estimate owner take-home and the gap to your target pay from monthly revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you test owner income before rolling out Power Bank Rental stations?

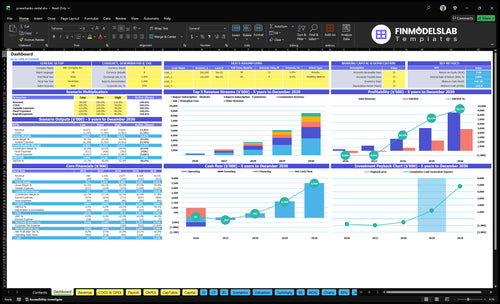

The Power Bank Rental Financial Model Template adds the dashboard, revenue forecast, assumptions, and owner cash outputs. It tests venue mix, buyer mix, repeat orders, AOV, commissions, subscriptions, fees, replacement costs, logistics, marketing, and scenarios; charts compare revenue, margin, costs, reserves, and cash available to the owner.

Owner-income model highlights

Owner cash take-home

Revenue and margin view

Scenario tabs test rollout

How many power bank rental stations do I need to make a living?

Power Bank Rental needs about 11 to 12 stations to support a $75,000 owner target, using the first-year average of $545 monthly pre-tax cash per venue. That’s a target draw, not a salary guarantee, because this is before payroll, debt, taxes, and other fixed overhead. If usage is weak or you reinvest cash, you’ll need more stations.

Base case math

$1,065 monthly revenue per venue

$545 pre-tax cash per venue

11 to 12 stations for $75,000

Uses first-year average venue economics

What can change it

Weak utilization raises the count needed

Reinvestment lowers owner cash today

Payroll and taxes cut take-home pay

Side income is not full-time income

What affects power bank rental profit margin?

Power Bank Rental margin gets squeezed by recurring costs, not startup spend. In year one, direct and variable costs total 175% of revenue, and you can check the launch side here: How Much Does It Cost To Launch Power Bank Rental Business?

That mix includes 60% venue partner commissions, 25% payment gateway fees, 50% power bank replacement, and 40% kiosk maintenance and logistics, plus $200,000 in first-year marketing. By mature-year assumptions, those costs ease to 135%, but weak venues, poor return rates, cable failures, longer service routes, and higher payment fees still hit owner take-home hard.

Year-one margin pressure

60% goes to venue commissions.

25% goes to payment fees.

50% is power bank replacement.

40% covers maintenance and logistics.

What cuts take-home

Weak venues demand higher commissions.

Users do not return units.

Cables fail and replacements rise.

Service routes stretch and fees climb.

Is power bank rental passive income?

No—Power Bank Rental is better viewed as semi-passive, not true passive income. The first-year model assumes 50 venue partners and $200,000 in acquisition marketing, so growth depends on active selling, station checks, and service work. You still have to replace lost or damaged units, fix payment issues, and move weak stations, and that’s where churn, shrinkage, route labor, and renegotiation risk show up.

Why it is not passive

Sell venue placements

Check station activity

Replace damaged units

Fix payment issues

What the model hides

50 partner target needs work

$200,000 marketing is front-loaded

Weak stations need moves

Churn and shrinkage hit returns

Power Bank Rental Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see what really drives owner take-home?

1

Rentals/Day

+$300K-$1.0M

With 50 first-year venues, 10,000 buyers, and 101 repeat orders, each extra rental per station per day feeds fee revenue straight through.

2

Placement Quality

+$200K-$800K

Better site fit lifts rentals and makes the later $200K marketing spend pay back instead of leaking into low-use stations.

3

Price & Time

+$120K-$500K

At a $375 weighted AOV, tighter pricing and rental timing can lift revenue per order, but weak conversion wipes out the gain.

4

Venue Share

-$150K-$225K

Venue revenue share cuts margin before owner profit, so even a small change in the split moves take-home.

5

Loss Rate

-$160K-$190K

Loss and replacement spend drains cash fast, and first-year direct and variable costs run at 175% before the model improves.

6

Route Overhead

-$85K-$150K

Fixed overhead is about $7.1K a month before wages, so route cost control matters as the network grows.

Power Bank Rental Core Six Income Drivers

Station Placement Quality

Station Placement Quality

Placement quality drives rental volume because the station only earns when people feel the need right now. The researched venue mix starts at 400% cafes, 350% bars, and 250% malls, then shifts toward 600% malls by the mature year. Best sites have foot traffic, dwell time, phone dependence, late-night urgency, and easy returns.

This affects owner income through both revenue and workload. Strong sites lift rentals and subscription value, while weak sites still create servicing work, replacement risk, and sales effort. One clean rule: if dead phones are common there, the station can earn there.

Track the sites that create urgent use

Measure each venue by rentals per station per day, return friction, and repeat use. Compare cafes, bars, and malls by actual orders, not by foot traffic alone. If a location gets attention but few rentals, it is costing route time without adding enough take-home income.

Rentals per station per day

Return friction

Repeat use by venue

Repair and replacement calls

Move units toward sites where phones die, people stay, and returns are simple. That improves revenue quality and makes fixed servicing costs easier to cover. If a site needs constant sales effort or repair visits, it is dragging down profit even when the map looks busy.

1

Rentals Per Station Per Day

Station Utilization

Rentals per station per day is the main activity metric. The first-year model assumes 10,000 buyers plus 101 weighted repeat orders, or about 10,100 orders. At about $1.06 per order, more daily turns lift revenue fast, but weak stations still create servicing work, so underused sites drag owner pay.

One extra order per day across 50 stations adds about 18,250 annual orders and about $19,391 in commission revenue before costs. Because route servicing, repairs, and restocking recur, even small usage drops can hit cash flow fast. Track low-volume stations by venue, hour, and neighborhood so you can move or cut them early.

Track daily turns, not just station count

Measure rentals per station per day, repeat orders, and revenue per order. Test placement and return friction together, because a busy kiosk only helps if the route cost per stop stays low. Forecast owner draw after servicing and replacement cash are reserved, then drop any site that misses target utilization for long.

Dense routes matter. If one trip can serve more stations, labor cost per rental falls and more of each order reaches profit.

2

Pricing And Rental Duration

Pricing and rental duration

Pricing changes both revenue per rental and how many people rent. In year one, weighted AOV is $375, built from tourists at $450, commuters at $300, and students at $350; by the mature year, it rises to about $445. Higher hourly fees, daily caps, deposits, late fees, promotions, and refunds all move that ticket up or down.

Here’s the catch: higher prices only help if they do not cut rentals per station per day. Longer rental duration can lift ticket size, but it can also slow turnover and reduce access for the next user. Owner income improves when the pricing plan raises average ticket without hurting adoption at busy stations.

Track price against usage

Measure average ticket, rental length, and rentals per station per day together. A price change is good only if the higher AOV does not weaken station activity. Watch customer mix too, since tourists, commuters, and students already price differently at $450, $300, and $350.

Track AOV by customer type

Test caps, deposits, and late fees

Watch refund and promo impact

Protect rentals per station per day

Keep the pricing rule simple: raise the ticket only when usage stays steady. If a higher rate lowers rentals, the lost volume can erase the gain fast. The owner’s take-home rises when pricing supports both cash per rental and steady turnover across stations.

3

Venue Revenue Share

Venue Revenue Share

This is the split paid to the host venue on each rental. With venue partner commissions at 60% of revenue in year one, only 40% is left before payment fees, logistics, replacement reserves, marketing, and owner pay; by the mature assumption of 40%, the business keeps 60% before those costs.

That gap matters fast. A site can look busy and still be weak if fixed placement fees, exclusivity, or minimum guarantees sit on top of a high commission. For example, $10,000 in monthly revenue leaves $4,000 at a 60% venue share, but that is still not free cash if servicing and loss reserves are heavy.

Protect the venue split

Track revenue per station, venue commission %, fixed fees, and cash margin after replacement costs, payment fees, logistics, and marketing. The key test is whether the station still leaves room for owner pay after all variable and fixed site costs.

Revenue by station

Venue share percentage

Fixed placement fees

Minimum guarantees

Net cash after servicing

Renegotiate weak stations fast. A site with strong traffic but bad terms can drain cash, while a lower-traffic site with a cleaner split can fund a real draw.

4

Loss And Replacement Costs

Replacement Loss Reserve

Lost and damaged power banks cut owner take-home because replacement needs are recurring, not one-time. Model 50% of revenue in year one, easing to 42% in the mature year. Include unreturned units, damaged cables, battery wear, and theft. If monthly revenue is $10,000, set aside $5,000 in year one or cash will look stronger than it is.

Here’s the quick math: owner pay should come after the reserve is funded. The inputs are revenue, loss rate, repair cost, theft rate, and battery life. Skip the reserve and profit can still be positive while cash gets tight, because the next batch of replacements arrives before the draw.

Fund the reserve first

Track loss by station and by device age, then compare it to the 50% to 42% benchmark. Separate replacement cash from operating profit in the forecast, and don’t count owner draw until the reserve is funded. If one route has higher theft or breakage, tighten return rules, inspect cables, and pull weak sites faster.

Measure return rate, damaged-unit rate, cable swaps, and battery fade every month. A simple rule works: revenue minus reserve, then owner pay. That keeps take-home tied to true cash left, not to accounting profit that ignores replacements.

5

Route Overhead And Servicing Efficiency

Route Overhead Efficiency

This driver is the gap between revenue and what it costs to keep kiosks working. In year one, kiosk maintenance and logistics run at 40% of revenue; in the mature-year case, that falls to 32%. That means better routing and fewer wasted trips can turn more gross margin into owner pay, but weak site density still burns cash on travel, cleaning, cable swaps, restocking, and repairs.

Here’s the quick math: every $100 of revenue keeps about $60 after servicing in year one, and $68 in the mature year before fixed overhead. The inputs that matter are station count, route density, stop count per trip, service frequency, and the split between fixed overhead like software, admin, insurance, and monitoring versus variable field work.

Track Route Cost per Station

Measure cost by route, not by guesswork. If one trip can service more stations, the cost per stop drops and owner income rises. Dense routes matter because the same drive can cover cleaning, cable swaps, restocking, and repairs across multiple kiosks. Lean operations help, but they do not guarantee profit if stations are spread out or underused.

Track stops per trip.

Track miles, labor, and parts.

Separate fixed and variable overhead.

Cut low-density, high-travel routes.

Budget for monitoring and insurance.

6

Power Bank Rental Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: Compare low, base, and high power bank rental income cases without implying guaranteed results

Owner income scenarios

Owner income moves with venue count, buyer volume, and cost control. Early cash can stay near zero, while scale improves the draw only if servicing, staffing, and reinvestment stay tight.

Low, base, and high cases show how placement sales and utilization change owner take-home.

Scenario

Low CaseCash tight

Base CaseModeled base

High CaseScale upside

Launch model

Owner draw can stay at $0 when the rollout is slow and cash is kept in reserve.

The modeled first-year case produces a solid pre-tax cash pool before unlisted overhead.

The upside case depends on mature-scale growth, but owner take-home still depends on taxes, debt, staffing, and reinvestment.

Typical setup

Weak venue sales, low utilization, and heavier servicing or overhead can force all cash back into the business.

About 50 acquired venues and 10,000 buyers support $639,081 revenue, 175% direct and variable costs, $200,000 marketing, and about $327,242 pre-tax cash before unlisted overhead.

About 857 acquired venues and 125,000 buyers support 135% direct and variable costs and $1,600,000 total marketing, with stronger volume but more cash tied up in growth.

Cost drivers

Placement sales

utilization

servicing

payroll pressure

cash control

Venue sales

buyer traffic

utilization

servicing

cash control

Placement sales

utilization

servicing

staffing

cash control

Owner income rangeBefore owner reserves

$0Zero draw

$327,242Cash flow base

Variable upsideReinvested upside

Best fit

Use this to stress-test a slow launch with thin cash and extra overhead.

Use this as the main first-year planning case for a funded launch.

Use this to test mature operations with heavy scale and reinvestment needs.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In the researched first-year case, the business produces about $53,257 in monthly revenue, based on $639,081 annually After 175% direct and variable costs and $200,000 annual marketing, cash before taxes, debt, payroll, and unlisted overhead is about $27,270 per month That is planning cash, not guaranteed owner pay

Profit timing depends on station placement speed and marketing efficiency The first-year assumptions acquire 50 venue partners at $1,000 seller CAC and 10,000 buyers at $15 buyer CAC With $200,000 total marketing and 175% direct and variable costs, the model shows positive pre-tax cash before unlisted overhead, but payroll or debt could delay owner distributions

You need enough venues to spread marketing, monitoring, and servicing work across a route The researched first-year plan assumes 50 acquired venue partners from a $50,000 seller marketing budget If each partner equals one station, revenue averages about $1,065 per station per month, but weak locations can fall below that fast

Owner take-home moves with utilization, venue terms, replacement costs, and marketing spend In the first-year assumptions, venue commissions are 60%, payment gateway fees are 25%, replacement is 50%, and maintenance and logistics are 40% Those costs hit cash before the owner can safely draw money

The model shifts toward malls over time, from 250% of venues in the first year to 600% in the mature year Cafes fall from 400% to 200%, and bars fall from 350% to 200% The best mix is the one with steady rentals, low loss, fair commissions, and efficient servicing

About the author

Arthur Grant

Startup Guide Author

Arthur Grant writes startup guide articles for Financial Models Lab, helping side-hustle builders think through realistic budget assumptions before launch. He studies common expenses, revenue drivers, and basic launch requirements, with a focus on rent, staff, equipment, and supplies. His small business startup guides also highlight the costs new founders often overlook.

Choosing a selection results in a full page refresh.