Owner income$120k

Owner income$120kHow Much Production Company Owners Make: $120K Salary Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k  Net margin70% to 79%

Net margin70% to 79% Revenue for target pay$152k to $171k

Revenue for target pay$152k to $171k Business difficultyHard

Business difficultyHard

In the provided five-year model, production company owner take-home starts with a modeled $120,000 founder salary before personal taxes Extra owner distributions are not supported in the early years because modeled operating cash is negative after direct costs, payroll, fixed overhead, and marketing Using the provided assumptions, revenue grows from about $79,850 in Year 1 to about $166 million in Year 5, while gross margin improves from 70% to 79% By Year 5, modeled operating cash is about $593,000 before reserves, taxes, debt service, and reinvestment, but that is not guaranteed owner income

Owner income$120kNet margin70% to 79%Revenue for target pay$152k to $171kBusiness difficultyHardWhat would your owner pay be?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, payroll, fixed overhead, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, reserves, taxes, and timing. This is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the owner-income model?

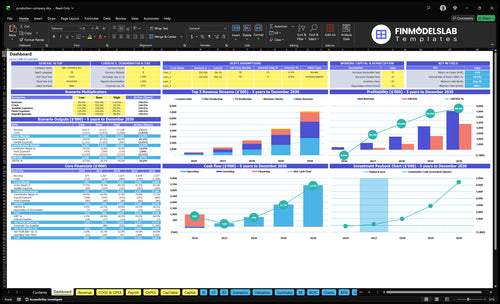

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Production Company Financial Model Template; open it.

Owner-income model highlights

- Owner pay comes last

- Revenue scales to $166M

- Gross margin stays 70%–79%

- Payroll runs $215k–$530k

- Cash turns positive later

How much revenue does a production company need to pay the owner?

A Production Company that wants to pay the owner $120,000 in Year 1 needs about $456,857 in revenue, using 70% gross margin and $319,800 in costs. Revenue is not income, so the real target depends on margin, payroll, overhead, marketing, and any cash reserve you want to keep. By Year 4, the target rises to about $826,563 at 76.8% gross margin with $350k non-owner payroll, $79,800 overhead, $85k marketing, and the same $120k owner salary.

Year 1 revenue math

- $120k owner salary

- $95k lead producer payroll

- $79,800 fixed overhead

- $25k marketing spend

Year 4 scale target

- 76.8% gross margin

- $350k non-owner payroll

- $79,800 overhead

- $85k marketing plus $120k owner pay

What affects production company profit margin most?

For a Production Company, profit margin is hit hardest by crew, talent, and payroll, not by the creative work itself. If you’re sizing the business, How Much Does It Cost To Open And Launch Your Production Company? is the right starting point. Direct costs run from 15% in Year 1 to 11% in Year 5, while fixed overhead stays at $6,650 a month, or $79,800 a year.

Biggest margin drains

- Crew and talent start at 15% of direct costs.

- Equipment and locations sit at 8%, then 6%.

- Software drops from 3% to 2%.

- Event marketing falls from 4% to 2%.

What to watch

- Fixed overhead is $6,650 per month.

- Annual overhead totals $79,800.

- Payroll grows from $215k to $530k.

- Keep pass-through spend separate from profit.

How does rights income change production company owner pay?

If a Production Company earns rights income, owner pay can rise on the upside, but only after contracts, recoupment terms, investor participation, and distribution timing are clear. In this model, there’s no separate rights-income amount, so base owner pay should come from client fees and service margins, not assumed royalties.

Cash first

- Client work pays sooner.

- Service margins fund payroll.

- Base pay stays more predictable.

- No rights income is modeled.

Upside later

- Owned content can add licensing upside.

- Distribution can lift library value.

- Royalties are not guaranteed income.

- Financing may be needed first.

Which income drivers matter most?

1

10-69 clientsProject Pipeline

Marketing grows from $25K to $110K while CAC drops from $2.5K to $1.6K, which can push new clients from about 10 to 69 and feed owner cash.

2

$110-$200/hrProject Economics

At $110 to $200 an hour and 30 to 160 billable hours, small scope and rate gains move take-home fast.

3

70%-79%Gross Margin

Keeping crew, rentals, software, and event spend tight lifts gross margin from 70% to 79%, and that drops more cash to the owner.

4

Month 8Cash Timing

Breakeven lands in month 8, and payroll rises from $215K to $530K, so slow collections can squeeze owner cash before profit shows up.

5

$79.8KOverhead

Fixed overhead runs $79,800 a year, so every extra admin dollar comes straight out of take-home.

6

UncertainRights Upside

Rights income is not modeled, so treat it as upside only until contracts prove repeat cash.

Production Company Core Six Income Drivers

Project Pipeline and Annual Production Volume

Project Pipeline and Annual Volume

More qualified projects can lift owner income only if gross margin holds and clients pay on time. In this model, the pipeline proxy is acquired clients = marketing budget ÷ CAC; that rises from 10 clients in Year 1 to 6,875 in Year 5. More work helps revenue, but late cash or weak margins can still shrink take-home pay.

One clean rule: volume without control is just busier cash burn. Commercials take 60% of Year 1 allocation, while film and TV scale later, so the owner should match project mix to cash timing. If scope creep, reshoots, or slow collections absorb cash, the extra jobs may raise top-line revenue but lower profit draw.

Track CAC, mix, and collections

Use the pipeline formula each month: acquired clients = marketing budget ÷ CAC. A drop in CAC from $2,500 to $1,600 improves acquisition efficiency by about 56% at the same budget. That means more booked work without needing a bigger marketing spend, which helps owner pay only if delivery stays tight.

- Track qualified leads, not just clicks.

- Separate commercials, film, and TV.

- Set payment milestones before shoot day.

- Cap revisions and reshoots in writing.

- Watch days sales outstanding closely.

What this estimate hides: more projects can still hurt cash if production overruns or invoices sit unpaid. Keep the mix weighted to paid, near-term work first, then expand into film and TV only when crew, post, and collections are stable.

1

Average Project Value and Producer Fee Income

Average Project Fee Retained

This driver is the fee the company keeps after direct project costs. A bigger project only lifts owner income if the retained margin stays intact. In this model, billable rates run from $110 per hour for Year 1 retainers to $200 per hour for Year 5 film work, with 30 to 160 billable hours per project. Gross project size matters less than the fee you actually keep.

Here’s the quick math: project revenue = hours × rate, then subtract crew, gear, locations, post, and revisions. A high-budget project can still be thin if those costs pass through at low markup. Loose scope and unpaid revisions can erase producer fee income, so owner pay depends on contracts that protect fee, change orders, and collection timing.

Protect the Fee Per Hour

Track hours sold, rate realized, direct cost pass-through, and revision count on every job. Separate retainer work from film production, because a 30-hour retainer behaves very differently from a 160-hour project. If the realized fee per hour slips, revenue can rise while take-home cash falls.

- Billable hours

- Realized hourly rate

- Direct costs

- Revision count

Use fixed scopes, capped revision rounds, and signed change orders. The goal is simple: keep a clear markup after crew, locations, gear, and post. If the contract does not protect the producer fee, the project may look big on paper but still leave little owner profit.

2

Gross Margin and Production Cost Control

Gross Margin Control

Gross margin is what’s left after direct production costs like freelance talent and crew, equipment rental, location costs, project-specific software, and industry event spending. If margin rises from 70% in Year 1 to 79% in Year 5, more cash reaches owner pay. On $166M of Year 5 revenue, a 1-point margin move is about $1.66M of gross profit.

The risk is simple: overruns, reshoots, and unpaid scope changes hit owner take-home first. A nine-point move from 70% to 79% adds about $14.94M of gross profit at Year 5 revenue, but only if direct costs stay tight and client billing covers added work before it starts.

Protect Every Margin Point

Track each job’s direct cost rate by project and by line item. Here’s the quick math: revenue minus direct costs = gross profit, then divide by revenue for margin. If a project needs extra edits, gear days, or location time, use an approved change order before the work starts. No signed change order, no extra work.

- Cap revision rounds in contracts

- Plan crew before booking

- Schedule rentals to avoid idle days

- Control post-production hours and handoffs

- Review event spend against booked work

What this estimate hides: if revisions, reshoots, or vendor delays grow faster than revenue, the owner’s draw falls even when sales look strong. Keep a weekly margin report, not a monthly surprise.

3

Licensing, Distribution, and Owned Rights

Licensing Cash Upside

Licensing, distribution, and owned rights can add upside beyond client project profit, but only after recoupment is cleared and any investor shares are paid. Since no rights-income amount is provided, model $0 in base owner-pay planning until the contract proves real cash. Distribution revenue can look big on paper, but fees and participation can cut owner cash fast.

Track minimum guarantees, distribution fees, recoupment balance, and payment timing. One-liner: if cash lands after payroll and production bills are due, owner draws need to wait.

Track Rights Cash, Not Gross Sales

Build a simple rights model with three inputs: expected license checks, fee stack, and when cash actually arrives. Include library revenue sensitivity so you can see what happens if old content earns less than planned. A deal only helps owner income if it produces cash after fees, expenses, and any participation split.

- Log minimum guarantee per deal

- Subtract distribution fees first

- Track unpaid recoupment monthly

- Flag delayed royalty statements

If the cash date is unclear, don’t count it in owner pay. That keeps draws tied to real money, not paper revenue.

4

Overhead, Payroll, and Fixed Cost Discipline

Fixed Overhead and Payroll

For a production company, this driver is the fixed overhead and base payroll that must be covered before owner pay. Here’s the quick math: fixed overhead is $6,650 per month or $79,800 per year, and payroll rises from $215k in Year 1 to $530k in Year 5 as post-production, marketing, junior production, and admin are added.

That mix matters because slow shoot gaps and slow collections still hit cash every month. Even with a 70% gross margin, hiring before revenue lands can push the business into losses, which means less cash for owner draws. The risk is simple: fixed payroll turns a quiet month into owner-pay pressure.

Track Headcount Before You Hire

Measure payroll against booked work, not hope. Track monthly fixed overhead, payroll by role, and the number of covered project months in the pipeline, then hire only when expected gross profit can absorb the new cost. One open role can be fine; two too early can wipe out owner take-home.

Use a simple rule in planning: if new staff don’t create enough billable work or margin to cover their loaded cost, delay the hire. Also watch collection timing, since a profitable project on paper can still starve cash when invoices sit unpaid. Tight overhead keeps owner pay steadier between shoots.

5

Cash Flow, Reserves, and Collections

Cash Flow and Owner Pay

Cash flow is what decides if the owner can actually pay themselves. In this model, operating cash after payroll, fixed overhead, direct costs, and marketing is negative through Year 3, then rises to about $63k in Year 4 and about $593k in Year 5 before reserves and taxes.

That means profit on paper is not enough if clients pay late. The key inputs are deposits, milestones, receivables, financing costs, and vendor payment terms, plus the reserve level the owner sets before any distribution.

Track Cash Before Draws

Build the forecast from cash collected, not just booked revenue. Track how much comes in at kickoff, at each milestone, and at final delivery, then compare that to payroll, the $6,650 monthly fixed overhead, project costs, and marketing spend.

Keep a reserve rule in the calculator before owner pay starts. If receivables stretch or a client misses a milestone payment, hold draws and protect vendor terms first; otherwise the business can show profit and still run short of cash.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income here changes fast because payroll, marketing, and fixed overhead move before distribution cash does. Early ramp-up looks very different from a mature pipeline.

| Scenario | Low CaseEarly ramp-up | Base CaseCapacity tested | High CaseMature pipeline |

|---|---|---|---|

| Launch model | This is the early ramp-up case where the owner pays for growth, not distributions. | This is the modeled case where the business can support owner pay plus some cash. | This is the stronger case where a mature pipeline can fund owner pay and larger distributions. |

| Typical setup | Year 1 is about $79,850 revenue with 70% gross margin, $215k payroll, $79,800 fixed overhead, $25k marketing, and no supported distribution base. | Year 4 is about $909k revenue with $470k payroll, $85k marketing, and about $63k operating cash before reserves plus a $120k salary. | Year 5 is about $166M revenue with 79% gross margin, $530k payroll, $110k marketing, and about $593k operating cash before reserves plus a $120k salary. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No supported distribution baseNo draw support | About $183k capacityModeled pay | About $713k capacityUpside capacity |

| Best fit | Use this to stress-test the launch year when cash is tight and owner pay stays limited. | Use this as the planning case for a working production pipeline with steady client flow. | Use this to test upside when volume is high and the pipeline can support broader owner take-home. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Production Company Porter's Five Forces Analysis

- Production Company BCG Matrix

- Production Company Business Model Canvas

- 7 Core Financial KPIs to Drive Production Company Profitability

- Production Company Business Plan Template in Pre-Written Word

- How to Increase Production Company Profitability with 7 Financial Strategies

- Calculating Monthly Running Costs for a Production Company

- Production Company Startup Costs: $97K CAPEX To $806K Cash Need

- Production Company Financial Model Template in Excel

- How to Start a Production Company in 6 to 12 Weeks

- Production Company Business Plan: 7 Steps for Financial Clarity

- Production Company Marketing Mix

- Production Company Marketing Plan

- Production Company Business Proposal

- Production Company PESTEL Analysis

- Production Company Pitch Deck Example Editable PPTX

- Production Company Business SWOT Analysis

- Production Company Value Proposition Canvas

Frequently Asked Questions

In this model, the owner salary is $120,000 before personal taxes That does not mean the company can always afford it Year 1 revenue is about $79,850, while payroll is $215k and fixed overhead is $79,800, so early owner pay may need funding, cuts, or slower hiring