How Much a Python Training Course Owner Can Make: $0 to $23M

Key Takeaways

Price hikes help only if conversion stays strong.

Filled seats matter more than leads or traffic.

Instructor-heavy delivery lifts quality but squeezes margin.

Upsells help, but beginner completion comes first.

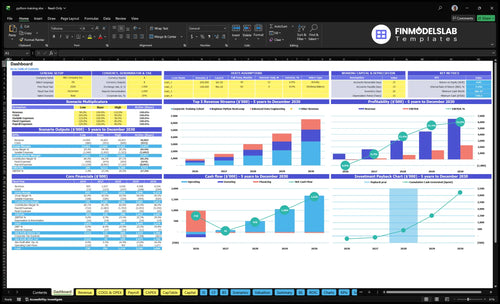

Owner income$0 to $2.29MNet margin-10% to 35%Revenue for target pay$1.64MBusiness difficultyHard

Want to test your own owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay. The base case reaches breakeven around Month 14 and needs about $730,000 minimum cash.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full Python training financial model?

How does scaling a Python training business affect owner income?

Scaling the Python Programming Training Course can lift owner income, but only if margin keeps up with payroll. Modeled capacity grows from 60 seats in Year 1 to 260 in Year 5, while occupancy rises from 65% to 88%, so revenue can expand fast. The catch is staffing and cash: instructors rise from 20 to 100 FTE, teaching assistants from 20 to 120 FTE, and minimum cash need peaks at $730K.

Income growth

60 seats in Year 1

260 seats in Year 5

Occupancy rises from 65% to 88%

More filled seats can boost owner pay

Risk and staffing

Instructors grow from 20 to 100 FTE

Teaching assistants grow from 20 to 120 FTE

Minimum cash need peaks at $730K

Use owner-taught, instructor-led, and hybrid support

How much revenue does a Python course need to pay the owner?

A Python Programming Training Course should start by backing into the owner’s pay target, then add fixed costs, payroll, marketing, reserves, and delivery costs. In the model, Year 2 revenue of $1,637M creates $152K EBITDA, which is the first clear pre-tax owner-income pool. By Year 3, $3,026M revenue drives $708K EBITDA, but actual take-home is lower after planned salary, distributions, taxes, debt service, and retained cash.

Revenue bridge

Year 2:$1,637M revenue

$152K EBITDA available pre-tax

First clear owner-income pool

Cover fixed costs first

Take-home reality

Year 3:$3,026M revenue

$708K EBITDA on the model

Salary and distributions are separate

Taxes, debt, and reserves cut cash

Can you make money running a Python course?

Yes, a Python Programming Training Course can make money, but under this staffed model it doesn’t pay the owner right away; How To Write A Business Plan For Python Programming Training Course? should plan for $905K Year 1 revenue and -$92K EBITDA. Meaningful owner income starts after Month 14 breakeven, if enrollment holds and cash reserves cover the ramp.

Money math

Year 1 revenue: $905K

Year 1 EBITDA: -$92K

Breakeven timing: Month 14

Cash gap needs reserves

Owner reality

Solo teaching may cash flow earlier

Solo capacity caps growth

Scale needs instructors and assistants

Career support and admin add cost

Python Programming Training Course Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main income drivers?

1

Enrollment volume

60-260

Total cohorts rise from 60 in Year 1 to 260 in Year 5, and that is the main top-line engine.

2

Pricing mix

$1.2K-$3K

Advanced and corporate tracks carry higher prices, so mix shifts can lift revenue without adding the same headcount.

3

Seat fill

65%-88%

Higher occupancy means more paid seats per class, which spreads fixed payroll and platform costs.

4

Instructor payroll

$625K-$2.49M

Instructor and support wages scale from $625K to $2.49M, so labor control decides how much revenue turns into EBITDA.

5

Acquisition spend

9%-7% rev

Digital student acquisition falls from 9% to 7% of revenue, and each point saved drops straight to margin.

6

Certification upsells

$150-$200

Certification fees add extra revenue per student with little added delivery cost, so they improve take-home on the same enrollments.

Python Programming Training Course Core Six Income Drivers

Pricing

Python Course Pricing

Pricing sets revenue per occupied seat, so it directly shapes how much cash each cohort can throw off. In Year 1, modeled prices are $1,200 for beginner training, $1,800 for advanced data engineering, and $2,500 for corporate cohorts. If pricing rises and occupancy holds, owner take-home improves; if conversion slips or refunds rise, the gain can disappear fast.

Here’s the quick math: a 20-seat beginner cohort at $1,200 brings in $24,000; at $1,400 in Year 5, that same seat count brings in $28,000. That extra $4,000 helps only if delivery costs, support, and refund rates stay controlled. Pricing is not just a number; it also sets student expectations for live teaching, feedback, and job-ready outcomes.

Track Price, Conversion, and Refunds

Measure net revenue per occupied seat, not sticker price alone. Use this formula: occupied seats × tuition × (1 - refund rate). If a higher price lowers fill rate, the owner may earn less, not more, because empty seats still absorb instructor pay, software, admin, and marketing costs.

Track conversion by cohort level.

Watch refund rate by price point.

Compare revenue per seat monthly.

Test price only with full cohorts.

Match price to support intensity.

For this model, price increases should be tied to clearer outcomes, stronger project work, and tighter service levels. If a cohort needs more live help, the higher fee should cover that labor so gross margin and owner draw do not get squeezed.

1

Enrollment Volume

Enrollment Volume

Enrollment volume is the count of paid seats across beginner, advanced, and corporate cohorts. The model grows from 25, 15, and 20 seats in Year 1 to 100, 60, and 100 in Year 5. At 65% occupancy, that is about 39 paid enrollments; at 88%, it is about 229. Revenue only rises if seats fill, because tuition is earned per occupied seat.

What this hides is the gap between leads and cash. Leads do not pay payroll, but empty seats still carry payroll, software, office, insurance, legal, and marketing tool costs. If the cohort calendar grows faster than demand, owner take-home gets squeezed even when the pipeline looks active. One empty seat is a lost tuition seat and a fixed-cost burden at the same time.

Track Paid Seats, Not Leads

Measure enrollment by cohort, stage, and cash collected. At 260 total seats, every 1-point change in occupancy is about 2.6 paid enrollments, so small miss rates move revenue fast. Build a monthly forecast by start date, and only add seats when the last two cohorts close near target fill.

Track lead to paid conversion.

Separate deposits from full payment.

Watch refunds and no-shows.

Trim class size if demand softens.

If beginner, advanced, or corporate cohorts miss target occupancy twice in a row, slow the next launch or push the start date. That protects cash flow, keeps fixed costs covered, and makes owner pay more stable.

2

Delivery Model

Delivery Model

Delivery model sets the ceiling on monthly revenue and how much of the work the owner can keep. Owner-led live teaching protects quality, but it caps capacity; instructor-led cohorts lift volume, but each added Python instructor FTE brings $110K of payroll and each teaching assistant FTE adds $55K, so the owner’s take-home rises only when extra seats cover the new labor.

Track capacity before hiring

Recorded lessons scale better, but they still need labs, support, updates, and student success, so they do not run on autopilot. Corporate workshops can charge more, but they need tight scheduling and service quality, or refunds and weak repeat sales will eat the margin.

Track cohort fill rate.

Watch labor per student.

Price workshops by service load.

Measure support hours weekly.

3

Student Acquisition Cost

Student acquisition cost

When paid seats depend on digital marketing, student acquisition cost eats cash before tuition turns into profit. In this model, digital acquisition is $81K on $905K revenue in Year 1 and $457K on $6,526M revenue in Year 5, so owner pay improves only if each channel brings in more paid students per dollar spent.

Track spend by channel, paid enrollments, conversion rate, and refund rate. SEO, referrals, webinars, partnerships, and employer channels help only when they convert to paid seats. If they bring leads but no deposits, CAC rises, cash gets tighter, and there’s less left for instructors, support, and the owner’s draw.

Cut cost per paid seat

Measure CAC as total marketing spend ÷ paid enrollments, not leads. Compare it by channel and cohort, and set a cap against tuition per seat. A full class can still be weak for profit if acquisition spend is too high.

Move budget to the channels that close. Pause sources that generate inquiries but not deposits, then test referrals, webinars, partnerships, and employer outreach on a per-seat basis. If conversion slips, owner take-home falls even when revenue looks strong.

4

Instructor And Support Cost

Instructor and Support Cost

This driver is the pay for instructors, teaching assistants (TAs), and program coordinators. In the model, payroll rises from $625K in Year 1 to $2.485M in Year 5 as staff scale from 20 instructors, 20 TAs, and 10 coordinators to 100, 120, and 50. That cost hits gross margin fast, so owner pay only improves if tuition revenue grows faster than labor.

Here’s the quick math: if staffing rises but class fill or retention stalls, the extra payroll shows up before the extra cash does. Cutting support can lift short-term profit, but it can also hurt completion, reviews, referrals, and refunds. So the real test is revenue per staffed cohort, not FTE count alone.

Track labor per cohort

Measure payroll per enrolled student, students per instructor FTE, and completion rate every month. If support gets thin, the savings may help this month’s margin, but refund pressure and weaker repeat sales can erase it later. One clean rule: staff to outcomes, not to a wage target.

Watch payroll per student.

Track completion and refunds.

Forecast seats per support FTE.

Use the inputs that move this cost: cohort count, seat fill, instructor FTE, TA FTE, coordinator FTE, and monthly payroll. If Year 5 staffing reaches 100/120/50, even small drops in occupancy matter more because fixed labor is higher. Owner take-home depends on keeping support efficient without hurting student success.

5

Repeat Revenue And Upsells

Repeat Revenue and Upsells

Repeat revenue means the course earns again from the same learner base through advanced data engineering, automation workshops, corporate renewals, certification processing, and alumni discounts. That matters because income is no longer tied only to new beginner seats. The certification fee rises from $150 in Year 1 to $200 in Year 5, so each repeat sale can lift revenue without a fresh acquisition cost.

This usually helps cash flow and owner pay because the student is already in the system. The key dependency is beginner completion: if the core Python cohort does not finish well, upsells weaken and support costs can rise. Keep the beginner offer as the main product, and treat repeat sales as extra margin, not the base plan.

Track Completion Before Selling the Next Step

Measure beginner completion, repeat purchase rate, and average upsell price by offer. Split out advanced classes, corporate renewals, certifications processed, and alumni discounts, then compare that revenue to extra instructor time and support load. If completion slips, repeat revenue will lag even when the upsell menu looks strong.

Price the next layer against the work it adds: advanced data engineering at $1,800 in Year 1 and corporate cohorts at $2,500, rising to $2,100 and $3,000 by Year 5. That keeps the math clean and protects margin. Use upsells to improve income quality, but keep them secondary to the core Python training offer.

6

Python Programming Training Course Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and strong owner income scenarios

Owner income scenarios

Owner income shifts fast here because Year 1 is cash-tight, Year 3 turns profitable, and Year 5 has strong EBITDA but still needs payroll and cash reserves.

Low, base, and high owner-income paths for the training business.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Year 1 is a launch case: $905K revenue, -$92K EBITDA, 65% occupancy, and 90% acquisition cost leave no owner distribution base.

By Year 3, $3.026M revenue, $708K EBITDA, 80% occupancy, and 80% acquisition cost can support owner pay before tax and reserves.

By Year 5, $6.526M revenue, $2.287M EBITDA, 88% occupancy, and 70% acquisition cost create the strongest owner-income path.

Typical setup

Demand is still building, staffing is fixed, and cash stays tight until breakeven in Month 14.

The business is past the launch dip, but payroll still grows across instructors, TAs, and support staff as scale improves.

The course is scaled, staffing is fully built out, and lower platform fees and better ad efficiency support more cash to the owner.

Cost drivers

Occupancy at 65%

acquisition cost at 90%

payroll ramp

fixed overhead

LMS and cloud fees

Occupancy at 80%

acquisition cost at 80%

payroll growth

pricing lift

fixed overhead

Occupancy at 88%

acquisition cost at 70%

full staffing

lower LMS and cloud fees

higher pricing

Owner income rangeBefore owner reserves

No owner drawNo draw base

Mid-six-figure drawBase income band

Upper-six-figure drawUpside income

Best fit

Use this to stress-test launch months and cash needs before any owner pay.

Use this as the most likely operating case for budgeting owner compensation.

Use this to test upside if demand stays strong and the program keeps filling cohorts.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In this model, revenue grows from $905K in Year 1 to $6526M in Year 5 Owner cash is tight early because EBITDA is -$92K in Year 1 The pre-tax income pool improves to $152K in Year 2 and $2287M by Year 5 before taxes, reserves, and distributions

The model reaches breakeven in Month 14 and payback in Month 28 That means the owner should plan for limited or no distributions during the early ramp-up Minimum cash need peaks at $730K in Month 13, so funding and reserve planning matter as much as sales

Yes, if the model uses live cohorts at this size Python instructors grow from 20 FTE in Year 1 to 100 FTE in Year 5, and teaching assistants grow from 20 to 120 FTE A solo founder can start leaner, but capacity, support quality, and student outcomes become bottlenecks

The biggest drivers are pricing, occupancy, payroll, and acquisition cost Year 1 occupancy is 65%, acquisition spend is 90% of revenue, and payroll is $625K By Year 5, occupancy reaches 88%, acquisition spend falls to 70%, and payroll rises to $2485M

A mix of beginner, advanced, and corporate training gives better revenue balance than one offer alone Year 1 prices are $1,200, $1,800, and $2,500 by program, with certification fees at $150 Corporate seats carry higher price points, but they need strong delivery, scheduling, and account management

About the author

Jonathan Bell

First-Time Founder Guide Writer

Jonathan Bell is a Financial Models Lab writer focused on launch budget planning, helping aspiring small business owners estimate startup needs before opening. As a first-time founder guide writer, he explains business costs in simple language and offers simple launch planning insights that help readers compare business opportunities realistically and make grounded real-world decisions.

Choosing a selection results in a full page refresh.