How Much Can A Sailboat Roller Furling Installation Owner Make At $85K Pay?

You’re planning owner pay before the job calendar proves it can carry the overhead This model uses researched assumptions for the first year through a mature year, including $85,000 owner/lead rigger pay, about 50 first-year installs, pricing, direct costs, payroll, marketing, fixed overhead, and reserves It is not guaranteed salary, tax advice, or a universal marine contractor benchmark

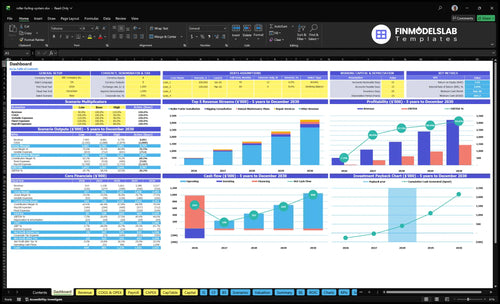

Owner income$1,028Net margin7.3%Revenue for target pay$438kBusiness difficultyHard

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How many roller furling installs are needed to make owner income?

There isn’t a universal job count for Sailboat Roller Furling System Installation, but the model is clear: at a $1,500 Year 1 ticket, each install contributes about $1,028 before overhead and payroll. That means covering $85,000 of owner pay alone takes about 83 install-equivalent jobs, while covering Year 1 non-owner payroll, fixed overhead, marketing, and owner pay needs about 292 install-equivalent jobs. The capacity check matters: 292 installs × 12 hours = 3,504 billable hours.

Owner pay math

$1,500 ticket per install

$1,028 contribution each job

83 jobs cover $85,000 pay

One job funds about 68.5% of ticket

Capacity check

292 jobs cover full Year 1 load

12 hours per install

3,504 billable hours needed

Schedule must support that load

Can a solo owner make money installing roller furling systems?

A solo owner can make money installing roller furling systems, but the ceiling is set by capacity, safety, marina access, and quality control. The plan you gave is not truly solo yet: it already includes a $62,000 marine technician in Year 1, a half-time sales role, and $85,000 of owner pay. Solo math lowers payroll, but it also lowers job volume, so don’t cut labor below what mast work, dock access, rig tuning, and callback control really need.

Solo cost side

Remove hired payroll first

Keep safe install labor

Protect dockside access time

Watch callback costs closely

Solo growth limit

One person caps daily jobs

Mast work raises safety risk

Rig tuning needs time

Quality loss hurts referrals

What is the roller furling installation profit margin?

If you’re pricing a Sailboat Roller Furling System Installation job, the model says a $1,500 install leaves about $1,028 before fixed overhead, payroll, marketing, and reserves, while Year 1 direct cost load runs 315%. For the KPI lens, see What Five KPIs Should Sailboat Roller Furling System Installation Business Track? because staffing and overhead still decide owner take-home. The model also shows the margin improving to 720% by Year 5.

Year 1 load

180% roller furler systems and hardware

80% installation parts and supplies

35% vehicle and mobile service costs

20% sales commissions and referral fees

Take-home

$1,500 install leaves $1,028

Model shows 685% before fixed overhead

Year 5 improves to 720%

Payroll and marketing still cap owner pay

Sailboat Roller Furling System Installation Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see what actually moves owner income?

1

Install Volume

50/yr

More completed installs lift cash fast, and year 1 starts at 50 jobs.

2

Ticket Size

$1.5K

A higher install ticket turns the same crew time into more revenue, so pricing discipline matters.

3

Parts Margin

68%-72%

Keeping hardware and supply costs tight protects contribution on every sale.

4

Labor Efficiency

12h

Cutting install hours lets the same crew finish more jobs and keeps payroll efficient.

5

Seasonal Use

8.5-11.5

Higher active-customer billable hours spread fixed costs across more work.

6

Overhead Buffer

$8.6K/mo

Monthly overhead comes off the top, so rework reserves and waste hit owner pay right away.

Sailboat Roller Furling System Installation Core Six Income Drivers

Completed Installs Per Season

Completed Installs Per Season

This driver is the count of completed, paid, low-callback installs in the season. The Year 1 model points to about 50 installs from 59 acquired customers at an 85% installation allocation. At roughly $1,028 contribution per install before overhead, that’s about $51,400 of contribution. More completed jobs means more cash to cover fixed costs and pay the owner.

The cap is seasonal, not demand alone. Weather windows, marina access, lead times, technician availability, and parts delivery all limit throughput, and one missed spring week can shove work into peak sailing season. The real risk is rework: callbacks eat time, delay payment, and cut take-home income fast.

Track Paid Installs, Not Leads

Measure booked jobs, completed jobs, callback rate, and days from deposit to install. If lead times stretch, the season slips even when sales look strong. A clean install calendar protects margin because every lost slot can mean about $1,028 less contribution before overhead.

Track weather-delay days.

Track marina access holds.

Track parts-on-hand date.

Track technician hours booked.

Track callback rate by job.

Use a simple season forecast: acquired customers × 85% = expected installs, then compare that to dock capacity and parts arrival. If spring capacity is tight, move training, inspections, or repairs into slower weeks so install slots stay open for the highest-margin jobs.

1

Average Installation Ticket

Average Installation Ticket

When a completed install is priced at 12 hours × $125 = $1,500 in Year 1, that ticket sets the ceiling on revenue per job before labor, parts, travel, and callbacks hit. By Year 5, the model uses 105 hours × $165 = $17,325, so the ticket can grow a lot if scope expands with line leads, hardware, tuning, maintenance plans, consultations, and repairs.

That price is not take-home pay. Direct costs, payroll, fixed overhead, and rework still come out, so a higher ticket only helps if the added work is priced before the boat visit and the gross margin stays intact.

Price the Scope Before You Go

Track hours sold per install, average labor rate, add-ons, and callback time on every job. The quick math is simple: ticket = billable hours × rate, plus any approved extras. If the job expands after arrival, margin usually leaks through unpaid labor and marina time.

Use a clear scope sheet for each quote: install labor, related hardware, tuning, and any follow-up service. If the ticket rises but callbacks also rise, owner pay can fall fast because the extra revenue is being spent on payroll, overhead, and redo work instead of profit.

2

Parts Margin And Supplier Economics

Parts Cost Pressure

This driver is the gap between what the customer pays and what the roller furling system, hardware, parts, and supplies cost. In Year 1, the model puts hardware at 180% of revenue and installation parts and supplies at 80%; by Year 5, those drop to 160% and 65%. That means supplier economics can swing gross profit hard, and if pricing is not built right, owner pay gets squeezed fast.

What matters is not just the invoice price, but freight, returns, warranty handling, wrong sizing, and cash tied up in inventory. Here’s the quick math: if you bill $10,000 in project revenue, the model implies $18,000 of hardware cost in Year 1 plus $8,000 of parts and supplies before labor and overhead. The key risk is simple: a good sourcing deal can raise gross profit, but a bad spec can erase it.

Track Cost Per Install

Measure this by job: hardware cost as % of revenue, parts and supplies as % of revenue, freight per install, and warranty credits per job. Also track inventory days and deposit timing, because cash leaves before the install is complete. If a quote assumes the Year 5 ratios of 160% and 65%, but your actual landed cost is higher, margin and owner draw fall.

Improve it by sizing systems before ordering, locking specs in writing, and separating labor from pass-through parts on the quote. Tight supplier control matters most when boats, mast setups, or customer requests change late. One clean rule helps: no order goes in until the part list, freight, and return terms are confirmed. That keeps the gross margin from leaking into rework and dead stock.

3

Labor Efficiency And Crew Cost

Labor Efficiency and Crew Cost

Labor is a double lever here: it sets job margin and how many installs you can complete. Year 1 assumes 120 billable hours per roller furler install at $125 per hour, or about $15,000 in labor revenue per job. By Year 5, the model improves to 105 hours at $165 per hour, or about $17,325 per job.

The catch is simple: faster installs only help if safety and quality hold. A $62,000 marine technician in Year 1 adds fixed payroll pressure, so poor prep, dock delays, missing parts, mast complications, and callbacks can quickly eat owner take-home. One clean install beats one rushed, rework-heavy job.

Track Hours, Delays, and Rework

Measure billable hours by job, not just jobs closed. Track planned hours versus actual hours, callback time, dock wait time, and parts misses. If a job runs over 120 hours, find the cause fast: bad prep, scope creep, or install complexity. That is where margin leaks out and crew cost rises.

Use the plan to protect capacity. Price for hard boats up front, stage parts before launch day, and assign the technician only when the work site is ready. Lower non-billable time raises effective hourly yield and helps the fixed $62,000 payroll turn into more owner profit instead of overtime and rework.

4

Seasonal Utilization

Peak-Season Fill Rate

Seasonal income depends on filling the short refit and launch window, then keeping slow months busy with maintenance plans, repairs, consultations, and training. With Year 1 marketing at $25,000 and $425 CAC, you need enough booked installs before weather turns; one missed spring week can push jobs into peak sailing season and delay cash that funds owner pay.

Book the shoulder months

Track booked jobs by month, lead time, and the share of off-season revenue. Here’s the quick math: $25,000 at $425 CAC implies about 59 customers. By Year 5, CAC falls to $300 while marketing rises to $65,000, so the calendar still has to stay full for income to hold.

Measure weeks booked ahead.

Sell slow-month services.

Set deposit and lead time.

5

Overhead, Travel, Insurance, And Rework Reserves

Fixed Overhead and Rework Reserves

$8,625/month in fixed overhead, or $103,500/year, hits income before marketing, payroll, direct job costs, debt, and taxes. The listed pieces alone total $6,750/month from $3,200 rent, $1,850 business insurance, $1,200 vehicle insurance and maintenance, and $500 training, so the business starts with a heavy base load.

For a mobile install shop, travel and rework matter just as much. Year 1 mobile service costs add 35% of revenue, and underpriced travel, marina access delays, tool replacement, and warranty callbacks shrink owner take-home fast. One clean rule: if the job price doesn’t cover travel and rework, the owner is funding the service.

Price Travel and Rework Up Front

Track travel time per job, callback rate, marina delay time, and rework cost per install. Then set a minimum charge that covers the 35% mobile cost load plus a reserve for warranty work. If volume is still low, every unpaid drive or repeat visit cuts owner pay right away.

Quote travel before the boat visit.

Hold a callback reserve per install.

Log access delays by marina.

Replace tools before failure stops jobs.

Use the fixed cost base of $8,625/month as the floor for pricing and cash planning. If the month is light, overhead does not slow down, so the business needs tight scheduling, fast access checks, and clear scope notes to protect margin and owner draw.

6

Sailboat Roller Furling System Installation Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner income scenarios using the researched model

Owner income scenarios

Owner income moves with install count, mix shift into maintenance and repair, and how fast payroll and overhead scale. More revenue helps only when service costs stay controlled.

Low, base, and high cases show how volume and staffing change owner income.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This is the lower earnings path with thin coverage and little room for owner draw.

This is the modeled path with steady utilization and a modest owner draw.

This is the stronger earnings path, but it still depends on tight cost control.

Typical setup

About 50 installs drive $75,000 in installation revenue and $84,934 in total service revenue, but 315% direct costs and fixed payroll and overhead keep operating coverage negative.

About 96 installs support $153,804 in installation revenue and $212,978 in total service revenue, with 295% direct costs and a larger team that still leaves cash tight.

About 141 installs lift installation revenue to $243,994 and total service revenue to $439,021, but 280% direct costs plus more staffing and overhead can absorb the upside.

Cost drivers

50 installs

315% direct costs

$85k owner salary

fixed overhead

base marketing

96 installs

295% direct costs

more staff

higher overhead

marketing

141 installs

280% direct costs

larger team

higher overhead

marketing

Owner income rangeBefore owner reserves

Salary onlyLow Case

Salary plus modest drawBase Case

Salary plus larger drawHigh Case

Best fit

Use this to stress-test a slow start, weak margin, and no distribution beyond the owner salary.

Use this as the working plan for a normal ramp with growing maintenance and repair work.

Use this to test upside if the shop stays full and the service mix keeps expanding.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The researched plan includes $85,000 annual owner/lead rigger pay before tax, but it is not guaranteed take-home Year 1 installation service revenue is about $75,000 from roughly 50 installs, and total modeled service revenue is about $84,934 That does not fully cover direct costs, staff payroll, fixed overhead, marketing, reserves, and taxes

It depends on install volume, service mix, and staffing pace Year 1 has about 50 installs and $8,625 monthly fixed overhead before marketing and payroll A simple install-only coverage test needs about 292 install-equivalent jobs to fund $85,000 owner pay plus Year 1 non-owner payroll, fixed overhead, and marketing

Yes, the researched cost structure includes business insurance at $1,850 per month and vehicle insurance and maintenance at $1,200 per month That is not legal advice, but it reflects the risk profile of dockside rigging work Insurance, training, vehicle costs, and callbacks directly reduce owner income if they are not priced into jobs

Completed installs, ticket size, direct cost control, labor hours, and rework drive profit Year 1 uses a $1,500 installation ticket, 12 labor hours, and 315% direct costs That leaves about $1,028 per install before payroll, fixed overhead, marketing, reserves, taxes, and debt service

Improve calendar density before adding overhead Book installs by marina or route, price travel and dock delays, reduce callbacks, and add maintenance, repair, and consultation revenue The model shows customer acquisition cost falling from $425 in Year 1 to $300 by Year 5, but payroll and fixed costs still need tight control

About the author

Julian Fox

Business Idea Researcher

Julian Fox is a business idea researcher at Financial Models Lab who focuses on revenue and profit basics for simple business planning. He helps non-finance readers compare business ideas by breaking down business model overviews and explaining how small businesses operate day to day. His work is grounded in real-world decisions and makes business plans easier to understand.

Choosing a selection results in a full page refresh.