How Much Can a Sandwich Panel Manufacturing Owner Make on $167M?

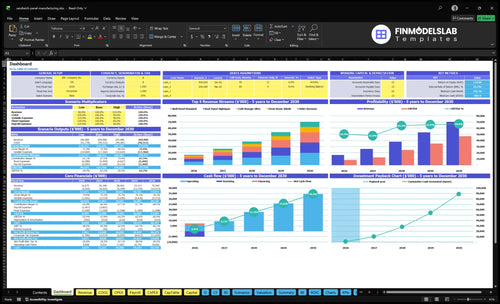

A sandwich panel manufacturing owner’s income depends on how much cash is left after production costs, payroll, overhead, debt, maintenance, and working capital reserves In the researched first-year assumptions, the plant produces 28,500 panels and generates about $167M in revenue After listed unit costs, product-specific revenue costs, and 60% freight, modeled contribution is about $115M before fixed overhead, financing, taxes, and reserves By the fifth year, modeled revenue reaches about $704M, but owner take-home still depends on utilization, pricing, material spread, and reinvestment needs

Owner incomeNot modeledNet margin50%–67%Revenue for target pay$16.7MBusiness difficultyHard

Want to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the financial model?

What affects sandwich panel manufacturing gross margin?

If you’re planning How To Start Sandwich Panel Manufacturing Business?, gross margin moves most with material spread, product mix, supplier pricing, yield loss, scrap, freight, and labor efficiency. Unit COGS runs from $92 for wall panels to $240 for data center panels, and product costs can take 35% to 55% of revenue. First-year freight can equal 60% of revenue, so margin compression hits owner take-home before it shows up in revenue headlines.

Main margin drivers

Material spread sets gross margin.

Product mix changes COGS fast.

Supplier pricing moves unit cost.

Yield loss and scrap cut take-home.

Where pressure shows up

Wall panels: about $92 COGS.

Data center panels: about $240 COGS.

Premium panels sell for $750 to $950.

Premium jobs need more testing cost.

Does scale increase sandwich panel manufacturing owner income?

Yes—scale can raise owner income in Sandwich Panel Manufacturing if demand, uptime, staffing, and cash controls keep pace. In the model, output rises from 28,500 panels in year 1 to 105,000 in year 5, and revenue climbs from $167M to $704M, so fixed overhead gets spread across more units. But automation can also add financing risk, maintenance downtime, and working capital needs, so owner work in quoting, purchasing, quality, and collections still matters.

Where scale helps

28,500 to 105,000 panels

$167M to $704M revenue

More volume spreads fixed overhead

Higher utilization can lift owner income

What can cap cash

Automation can need more financing

Maintenance downtime cuts output

Working capital rises with growth

Quoting and collections hit cash fast

Can a sandwich panel manufacturing business support a full-time owner?

Yes, Sandwich Panel Manufacturing can support a full-time owner, but only after gross profit funds fixed payroll, plant overhead, equipment payments, maintenance, and working capital; use What 5 KPIs Drive Sandwich Panel Manufacturing Business? to check the operating levers. First-year assumptions show $167M revenue from 28,500 panels and about $115M contribution before fixed costs, so owner salary is a planning output, not an entitlement.

Owner-pay test

Fund payroll before owner draw

Cover plant overhead first

Pay equipment debt on time

Protect working capital reserves

Volume reality

Tie output to confirmed orders

Do not trust nameplate capacity

Track reliable production daily

Validate the claimed 40% labor saving

Sandwich Panel Manufacturing Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers behind owner income?

1

Throughput

$16.7M

At 28,500 panels in Year 1, revenue is $16.7M and rises to $70.4M by Year 5, so every extra line hour lowers unit overhead.

2

Pricing Power

$450-$1,070

Shifting more sales to clean room and data center panels lifts the unit price mix, which moves revenue faster than volume alone.

3

Material Spread

$92-$240

Unit COGS runs from about $92 on wall panels to $240 on data center units, and tighter input buys protect gross margin.

4

Labor Efficiency

18-46 FTE

Headcount grows from 18 FTE in Year 1 to 46 FTE by Year 5, so cleaner runs, less scrap, and less rework keep take-home higher.

5

Fixed Overhead

$91.5K/mo

Fixed costs run about $91.5K a month, so steady output matters or overhead will eat the plant's operating leverage.

6

Order Pipeline

2 mo

A stronger pipeline gets the plant to breakeven in Month 2 and payback in 11 months, while slow collections press cash.

Sandwich Panel Manufacturing Core Six Income Drivers

Production Utilization And Throughput

Production Utilization

Utilization is the main income driver because it spreads fixed plant overhead across more sold panels. Here, volume rises from 28,500 panels in year 1 to 105,000 in year 5, and revenue climbs from $167M to $704M. More shipped panels can lift profit and owner pay, but only if demand, uptime, and scrap stay under control.

This driver includes panels produced per shift, shipped units, downtime, and backlog conversion. Here’s the quick math: fixed overhead per panel = fixed plant overhead ÷ shipped panels. If you add nameplate capacity before orders are confirmed, idle lines and slow collections can burn cash, so planned output is not the same as spendable profit.

Track Output and Order Conversion

Measure panels per shift, shipped units, and downtime every day. Separate produced panels from invoiced panels, because cash comes from shipment and collection, not machine hours. Watch backlog conversion risk closely: if orders slip, the plant can look busy while owner cash stays tight.

Track output by shift.

Compare shipped vs produced.

Log downtime by cause.

Refresh backlog weekly.

Match capacity to confirmed orders.

One clean rule: more throughput only pays when demand holds. If uptime drops or orders stall, fixed overhead stays put, contribution shrinks, and owner draw should wait.

1

Average Selling Price And Pricing Power

Average Selling Price and Pricing Power

Pricing power matters because higher-spec panels only lift owner income if the extra price covers the extra work. In year 1, prices range from $450 for standard wall panels to $950 for data center panels; by year 5, that range rises to $490 to $1,070. The spread is where profit lives, but only if quoting stays disciplined.

Quote quality depends on insulation core, thickness, fire rating, order size, finish, delivery terms, and certification needs. If the shop wins commodity-only jobs, the line stays busy but cash gets thin, and owner pay becomes harder to fund. Higher price should mean higher take-home income, not just more volume.

Price by Spec, Not Just by Panel

Track every quote against the spec drivers above and compare it to the added handling, documentation, and delivery work. One clean rule: if the job adds complexity, the price must rise too. That protects gross margin and keeps panel mix from drifting toward low-value work that fills capacity but weakens cash flow.

Track quote win rate by panel type.

Flag orders with special certification.

Test minimums for small order sizes.

Price delivery terms separately.

Here’s the quick check: a $500 gap between standard wall and data center panels in year 1 is only useful if the higher-spec job still leaves room after added labor, paperwork, and freight terms. If not, the owner is buying revenue, not profit.

2

Raw Material Spread

Raw Material Spread

Material spread is the gap between panel sale price and input cost, and it sets gross profit before overhead. Here’s the quick math: a $450 wall panel with $92 unit COGS leaves $358 before plant overhead, labor, debt service, and owner pay. A $950 data center panel with $240 COGS leaves $710, but only if the quote holds through purchase.

This driver gets tight when steel coil, insulation core, adhesive, facer, seals, coatings, or fire-rated parts move after the bid. Revenue-based COGS can add 35% to 55%, so quoting before input costs are locked can wipe out cash fast. One bad job can look busy and still pay poorly.

Protect the Spread

Track quoted price, locked input cost, and landed COGS per panel on every job type: wall, roof, cold storage, clean room, and data center. Use the spread to test whether the sale covers overhead and still leaves room for the owner. If the spread narrows after freight or supplier terms change, the job may still add revenue but not cash.

Build pass-through rules into quotes for market-sensitive materials and set a short pricing window. Watch supplier lead time, minimum order terms, and quote-to-order lag. If input costs are not locked, do not assume gross margin will hold. That protects contribution and keeps owner draws from being funded by hope.

Compare quote price to locked COGS

Reprice when supplier terms move

Separate margin by panel type

Flag jobs with delayed input locks

3

Labor Productivity, Scrap, And Rework

Labor Productivity, Scrap, And Rework

Labor cost per panel is the key number here: direct labor dollars divided by good panels shipped. Track scrap rate, quality failures, downtime, and rejected shipments, because this business has $167M in first-year revenue and material runs through every panel. Small yield losses cut gross margin fast, so weak line discipline shows up as less owner cash, more rework, and tighter pay draws.

Measure Yield Before You Cut Headcount

Start with good panels per labor hour, then tie it to scrap and rework by shift. If a crew makes more panels but rejects rise, labor is not improving. Training, setup checks, and in-line quality gates usually protect income better than staff cuts, because they reduce hidden waste. One clean rule: fix the process before you add labor.

4

Fixed Overhead, Financing, And Maintenance Reserves

Fixed Overhead and Cash Draw

In panel manufacturing, fixed overhead is the cash floor. Plant rent, utilities, insurance, salaried payroll, compliance, equipment loan payments, capex, loan principal, and the maintenance reserve all get paid before the owner can take cash out. First-year contribution is about $115M before those fixed items, so owner pay depends on what is left after debt and reserves.

The trap is treating EBITDA as spendable cash. EBITDA can look healthy, but it does not fund principal paydown or replacement parts. If financing is heavy or repairs spike, cash to the owner falls even when sales grow. One bad uptime month can erase a lot of draw capacity.

Watch Debt Service and Reserves

Measure the monthly fixed cost run rate against gross profit and cash from operations. Track each item separately so you can see the break-even load and the real cash left for owner pay. Equipment financing can lift capacity, but it also raises the cash hurdle before distributions can start.

Track monthly rent and utilities.

Separate loan principal from EBITDA.

Fund maintenance before owner draws.

Watch downtime and spare-part spend.

Keep the maintenance reserve funded first, because it protects uptime and stops repairs from hitting owner income all at once.

5

Customer Mix, Pipeline, And Cash Timing

Customer Mix And Cash Timing

Customer mix affects income stability as much as margin. In year one, the mix is 12,000 wall panels, 8,000 roof panels, 5,000 cold storage panels, 2,000 clean room panels, and 1,500 data center panels. If one customer type dominates, a delay in one project can slow collections and push out owner pay even when revenue is booked.

The key inputs are customer type, order size, payment terms, and backlog quality. Backlog quality means confirmed orders with real timing and collection dates. A factory can look busy and still burn cash if it ships into slow-paying jobs, so concentration risk and project timing matter as much as gross margin.

Track Mix, Terms, And Collections

Split the pipeline by customer type: repeat contractors, cold storage buyers, commercial projects, distributors, and specialty facilities. Track order size, payment terms, and how much of the backlog is already approved and schedulable. That shows which sales actually fund payroll, materials, and owner draws.

Push for a mix that balances volume and cash speed. A large order with slow payment can be worse than a smaller order with cleaner terms. Watch concentration too: if one customer or one project drives most of the backlog, a slip can leave the plant busy but the bank account thin.

6

Sandwich Panel Manufacturing Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios from operating assumptions

Owner income scenarios

Owner income moves with panel volume, mix, and plant use. The low case tests ramp-up, the base case matches year 3 scale, and the high case shows year 5 throughput.

Three owner-income views from ramp-up to scale.

Scenario

Low CaseLow case

Base CaseBase case

High CaseHigh case

Launch model

This is the lower owner-income path tied to first-year ramp-up.

This is the modeled mid-case owner-income path at year 3 scale.

This is the stronger owner-income path if the line runs at year 5 scale.

Typical setup

Year 1 output is 28,500 panels with $16.7M revenue, while freight, commissions, and fixed payroll still weigh on take-home.

Year 3 output reaches 61,000 panels and $38.3M revenue, with steadier utilization and a better spread of fixed costs.

Year 5 output reaches 105,000 panels and $70.4M revenue, with higher utilization and a larger sales and operations team.

Cost drivers

First-year volume

6.0% freight

3.0% sales commissions

heavy fixed overhead

ramping staffing

Higher throughput

5.6% freight

3.0% sales commissions

larger payroll

steadier yield

Higher utilization

5.2% freight

3.0% sales commissions

larger sales team

tighter quality control

Owner income rangeBefore owner reserves

Thin owner income bandThin take-home

Moderate owner income bandSteady take-home

Stronger owner income bandUpside take-home

Best fit

Use this to test the business if demand ramps slowly and the plant is still absorbing startup overhead.

Use this as the planning case for a scaled line with normal sales traction and more stable plant use.

Use this to test upside if demand stays strong, uptime holds, and the plant can keep pushing volume.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

Profit depends on fixed costs, debt, reserves, and owner pay policy The researched first-year assumptions show $167M revenue, 28,500 panels, and about $115M contribution after listed unit costs, revenue-based production costs, and 60% freight That is not owner income because payroll, overhead, financing, taxes, and reinvestment still come next

The owner can take cash only after the plant covers production costs, fixed overhead, debt service, and working capital In the first-year case, modeled contribution is strong at about $115M, but production growth from 28,500 to 61,000 panels by the third year can absorb cash for materials, labor, inventory, and receivables

Yes, a financial model is useful because revenue alone hides cash strain The model should test $450 to $950 first-year selling prices, $92 to $240 unit COGS, 35% to 55% revenue-based costs, freight, overhead, debt payments, and reserves It should show owner take-home after the factory funds operations

Margin quality often matters more than headline sales Steel, insulation core, adhesive, scrap, rework, freight, and labor efficiency can change cash available to the owner fast For example, first-year revenue is $167M, but listed variable costs total about $52M before fixed overhead A small cost miss can become a large cash miss

The best approach is to set owner pay after break-even and reserve funding, not before Use a target draw, then confirm the plant can cover overhead, equipment payments, maintenance, and working capital With fifth-year revenue modeled at $704M, the opportunity is large, but distributions should still follow cash flow, not booked sales

About the author

Matthew Clarke

Founder Support Writer

Matthew Clarke is a founder support writer at Financial Models Lab, where he helps non-finance readers understand practical profit planning and how small businesses make a profit. He focuses on clear, research-based guidance before money is invested, including startup cost estimates and early planning basics. His work makes business planning easier, more practical, and less intimidating.

Choosing a selection results in a full page refresh.