How Much Does a Seafood Truck Owner Make? $359K Year 1 EBITDA

Key Takeaways

Volume sets revenue capacity before margins can help.

Higher ticket baskets grow revenue without extra service days.

Seafood waste can erase gains from strong pricing.

Fixed overhead and payroll raise the break-even bar.

Owner income≈$29.9k/moNet margin16.2% → 51.7%Revenue for target pay$2.2MBusiness difficultyHard

Want to test your seafood truck owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check Seafood Truck owner income in the model?

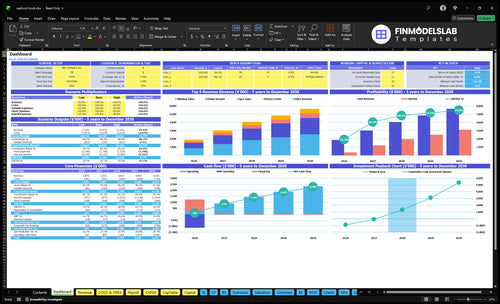

This dashboard shows revenue, EBITDA, owner income, cash runway, and payback; open the Seafood Truck Financial Model Template to review the assumptions and plan next steps.

Owner-income model highlights

Owner pay is shown clearly

Revenue and margin track together

Low, base, strong cases

Does a seafood truck make more money owner operated?

For a Seafood Truck, owner-operated can raise owner cash because the owner replaces paid labor, but it is not passive income. Here’s the quick math: payroll is still sized at $690K in Year 1 and $965K by Year 5, so pulling labor onto the owner can lower cash outflow, but it also raises burnout and missed sales risk if prep, cooking, dispatch, and events pile up.

Owner cash edge

Owner labor cuts payroll cash.

Prep and cooking stay in-house.

Dispatch stays under control.

Cash flow can look stronger.

Staffing tradeoff

Longer hours need staffed shifts.

Festivals need extra hands.

Private events need coverage.

Flexible staffing fits season swings.

Are seafood trucks profitable?

Yes, Seafood Truck can be profitable when premium pricing covers seafood cost, spoilage, packaging, labor, and fixed overhead; for startup cost context, see How Much Does It Cost To Open Your Seafood Truck Business?. The provided Year 1 model shows $359K EBITDA on $2,215M revenue, or about 162%. But the cost stack is heavy: COGS is 150% in Year 1, and processing plus supplies add 43%.

Profit drivers

Charge premium prices for fresh seafood.

Keep portion control tight on each plate.

Use specials to move near-spoilage inventory.

Watch labor, packaging, and overhead daily.

Margin leaks

Over-prep creates waste fast.

Fryer oil, sauces, and sides add cost.

High packaging can squeeze each order.

Weak sell-through hurts cooked seafood margins.

How much does a seafood truck need to sell per day?

Seafood Truck daily sales need to match the service plan: in the provided case, Year 1 source schedule supports about $426K a week, or roughly $61K per day across 7 service days. That level has to absorb $298K in monthly fixed expenses and $690K in annual payroll, and the case reaches break-even in Month 3. Owner pay is extra cash need, so add it separately and divide it by contribution margin and service days.

Sales drivers

Orders drive daily revenue.

Ticket size sets the check.

7 service days shape output.

$61K/day is the case level.

Cash needs

$298K monthly fixed cost.

$690K yearly payroll.

Month 3 break-even in case.

Owner pay stays separate.

Seafood Truck Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six seafood truck income drivers?

1

Service Volume

20-70/day

Year 1 runs 20 to 70 daily covers and Year 5 reaches 50 to 140, so more served customers lifts revenue fastest.

2

Menu Mix

$120/$180

Midweek checks at $120 and weekend checks at $180 push revenue up without extra trips, so mix matters a lot.

3

Food COGS

5.0%

Food cost and spoilage hit gross margin directly, so tighter prep and storage protect take-home on every order.

4

Private Events

10%-11%

Private events can add larger tickets in one stop, but the income lift depends on booking enough of them.

5

Labor Model

$690K

Year 1 payroll is $690K, so staffing to real cover levels is key to keeping margin from getting squeezed.

6

Fixed Overhead

$29.8K/mo

Lease, utilities, insurance, and admin costs hit every month, so weak sales days cut owner income fast.

Seafood Truck Core Six Income Drivers

Service volume and operating schedule

Service Volume and Schedule

Service volume sets the revenue ceiling before margin math matters. Moving from 20 covers on Monday to 70 on Saturday helps because weekend demand is higher, but the extra sales only reach owner income after seafood cost, packaging, card fees, event staff, and prep labor are paid.

Here’s the quick math: the source schedule shows about $426K in weekly revenue. Lunch, dinner, festivals, breweries, offices, beach markets, and high-traffic routes matter because they lift order count; if those slots stay thin, truck time and crew time can still drain cash.

Track Volume by Shift

Measure orders per day, daypart, and location. Separate walk-up sales from events, because private events and high-traffic routes usually carry better volume and less idle time than a weak curbside lunch.

Track orders by hour.

Tag each sales location.

Compare labor to sales.

Watch contribution after variable costs.

If weekday volume drops, shorten hours or move to better routes instead of chasing low-value open time. The goal is not just more covers; it’s enough volume per shift to cover variable costs and leave cash for owner pay.

1

Average ticket and menu mix

Average Ticket and Menu Mix

Average order value (AOV) is the money per customer. In Year 1, it is $120 midweek and $180 on weekends, then rises to $160 and $220 by Year 5. That is a 33% lift midweek and 22% on weekends, so the truck can grow revenue without adding another service day.

Menu mix is the split between baskets, combos, add-ons, drinks, and premium specials. A higher ticket helps owner income only if seafood cost, packaging, and labor stay under control. If premium ingredients rise faster than price, gross margin falls and less cash is left for owner pay.

Raise the Check, Protect the Margin

Track AOV, add-on rate, and item-level food cost every week. Test bundles that pair seafood baskets with drinks or premium sides, then keep the mix that lifts revenue per ticket without pushing portions past what local customers will pay.

Track AOV by day and event

Measure add-on attach on each ticket

Compare price to food cost weekly

Drop weak-margin specials fast

If the check goes up but waste also climbs, owner income still gets squeezed.

2

Seafood cost, waste, and gross margin

Seafood Cost and Waste

Seafood cost can make or break take-home pay because spoilage is higher than in many mobile food models. With COGS at 150% in Year 1 and 130% by Year 5, gross margin is still under pressure, so the truck must control purchase price, thawing loss, prep waste, fryer oil, sides, sauces, and packaging just to get to break-even.

Here’s the quick math: if cost runs above sales, gross margin is negative before labor and fixed overhead. A high average ticket only helps if portions stay tight and unsold seafood moves fast. Waste from a slow day can wipe out the profit from a busy lunch rush.

Control Portion Loss

Track purchase price, yield after thawing, and sell-through by daypart. The inputs that matter are orders, average check, portion size, and leftover inventory. If the truck sells 100 covers but trims and waste eat too much product, owner income drops fast even when revenue looks strong.

Measure yield after thawing.

Set portions by recipe.

Count leftovers each shift.

3

Catering, events, and route mix

Catering and event mix

If private events are 100% of sales in Year 1 and stay near 100% through Year 5, owner income depends less on foot traffic and more on contract quality. The big win is predictability: set minimums before prep so food, travel, and staff are covered before the truck leaves the commissary.

Event revenue improves cash flow when the quote includes event fees, commissions, travel, prep labor, extra staff, and weather risk. Private parties, corporate lunches, festivals, and seasonal events can raise order density, but if the minimum does not cover those add-on costs, the owner pays for the event out of profit.

Price the minimum, then staff to it

Track minimum spend, service fee, travel charge, and labor hours per event. Here’s the quick test: if the booking can’t cover seafood, labor, and a fair margin before service starts, don’t treat it as a real profit job. Guaranteed minimums protect owner pay better than foot-traffic-only vending.

Quote every cost before prep.

Use weather clauses for outdoor jobs.

Price extra staff into the contract.

Compare event margin to walk-up sales.

4

Labor model and owner involvement

Labor model and owner involvement

Labor is a big cash drain, so owner income depends on whether each staffed shift pays for itself. The source payroll line shows $690K in Year 1 and then $7375K, $8275K, $9175K, and $965K by Year 5, so labor is a major swing factor in cash flow and take-home pay.

Owner-run shifts can cut cash payroll, but the owner’s time still has value. If the owner works prep, service, or driving, the truck saves cash now, yet profit only improves if those hours create enough extra sales to cover food, packaging, and staff needs.

Track labor by shift, not just month

Watch labor dollars per open hour, covers per shift, and sales per labor hour. Hire cooks, cashiers, drivers, or event staff only when extra hours or events lift revenue enough to pay the wage and still protect owner draw.

Use the owner on the most flexible shifts first. If a shift does not add enough covers to beat its wage burden, it lowers cash flow even if sales look busy. The clean test is simple: labor should buy more sellable hours or more event volume.

5

Fixed overhead, truck costs, and compliance

Fixed overhead and owner pay

Fixed overhead gets paid before the owner does. Here, the monthly run rate is $298K, including $20K lease, $15K cleaning, $12K marketing, $3K utilities, $800 licenses and permits, and $600 POS subscriptions, so a weak month can wipe out draw fast.

Truck financing, generator fuel, propane, parking, commissary rent, health permits, repairs, and insurance all reduce cash before profit reaches the owner. The key test is simple: fixed overhead ÷ contribution margin = break-even sales. If sales miss that line, owner pay gets pushed back.

Cut cash drag on every shift

Track each route day by sales, fuel, parking, commissary fees, and permit costs. A stop that covers seafood cost but not overhead still lowers owner income. One clean rule: if the day does not add margin after cash costs, it is not helping take-home pay.

Measure sales per shift.

Track cash cost per route.

Log monthly fixed overhead.

Review break-even weekly.

Keep the forecast tied to actual truck use, not hope. If repairs, fuel, or permit costs rise, update break-even sales right away so owner draw is based on real cash left, not booked revenue.

6

Seafood Truck Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and strong seafood truck owner income scenarios

Owner income scenario table

Owner income swings with daily order volume, weekend ticket size, and a heavy fixed-cost base. Small changes in labor or traffic can push the plan from tight cash to very strong profit.

Lean, base, and strong cases show how volume, pricing, and fixed costs change owner pay.

Scenario

Lean CaseLean

Base CaseBase

Strong CaseStrong

Launch model

This is the lower-earnings path, with volume below the source model and the owner stepping in on more shifts.

This is the source operating model, with Year 1 volume and ticket assumptions carrying the plan.

This is the stronger earnings path, with later-year volume and higher tickets driving much more owner income.

Typical setup

About 7 service days, fewer orders per day than Year 1, lower ticket size, tighter labor, and the same heavy fixed-cost base keep cash pressure high.

Year 1 runs about 39 orders a day on 7 service days, uses $120 midweek and $180 weekend tickets, holds about 15% combined COGS plus 4.3% variable fees, and carries about $29.8k in monthly fixed costs.

By Year 5, revenue is about $6.0M with EBITDA near $3.113M, supported by 600 weekly orders, higher weekend tickets, and the same fixed-cost base spread over more sales.

Cost drivers

Lower orders

smaller tickets

owner-run labor

15% COGS

thin reserves

39 orders/day

$120-$180 tickets

15% COGS

4.3% fees

$29.8k fixed

Higher volume

higher tickets

13% COGS

3.5% fees

fixed costs spread wider

Owner income rangeBefore owner reserves

Under $359kLean case

$359kBase case

$3.1MStrong case

Best fit

Use this to stress-test seasonality, slow weeks, and how much owner pay can wait.

Use this as the main planning case for budgeting, hiring, and lender talks.

Use this to test what happens if demand and pricing both hold up into the mature years.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Keep enough cash to cover slow weeks, repairs, permits, and seafood spoilage In the provided case, minimum cash is $46K in Month 10, while fixed expenses run $298K per month That means one major repair or weak event month can matter fast, so reserves should be planned before owner draws

This plan reaches break-even in Month 3 and shows a 26-month payback That is based on the provided sales ramp, $2215M Year 1 revenue, and $359K Year 1 EBITDA If opening volume is weaker, permits drag, or event bookings start late, break-even can move out quickly

Catering is not required, but it can make revenue more predictable The provided plan includes private events at 100% of Year 1 sales, which helps smooth demand beyond street vending The key is pricing events with minimums, travel, prep labor, event fees, and weather risk included

Owner pay moves most with sales volume, average ticket, food cost, labor, and fixed overhead In this case, Year 1 covers range from 20 to 70 per day, AOV is $120 to $180, payroll is $690K, and fixed costs are $298K monthly Small misses in volume can cut cash fast

Raise profit by improving order density, protecting portion control, and booking higher-certainty events The source plan grows EBITDA from $359K in Year 1 to $3113M in Year 5 as covers and AOV rise Do not chase sales that add waste, extra staff, or event fees without enough margin

About the author

Robert Spencer

Startup Planning Writer

Robert Spencer is a startup planning writer at Financial Models Lab who focuses on simple financial projections that make business ideas easier to evaluate. He helps readers compare opportunities by breaking down the cost and income assumptions behind everyday business ideas. With a clear, grounded style, he explains how small businesses operate day to day and gives beginners a practical way to understand the numbers before they commit.

Choosing a selection results in a full page refresh.