How Much Shadow Box Framing Owners Can Make: $85K Plus Profit

You’re pricing custom displays before you know what the owner can safely take out This estimate uses a five-year US planning model with 500 completed orders and $563,000 revenue in the first year, then separates revenue, direct costs, overhead, planned owner pay, reserves, and profit It excludes taxes, financing, depreciation, personal benefits, and guaranteed distributions

Owner income$85kNet margin31%Revenue for target pay$275kBusiness difficultyMedium

Want to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it excludes taxes, debt service, depreciation, and owner benefits.

Want to see the owner income model?

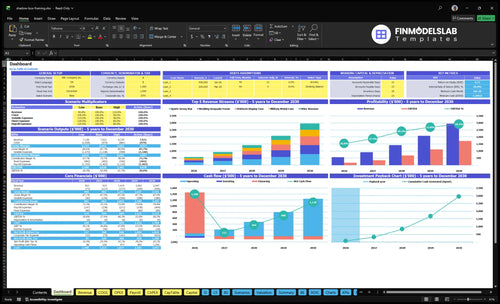

Dashboard: revenue build, income statement, COGS, variable and fixed expenses, payroll, scenarios, and owner pay. Assumptions cover ticket, materials, marketing, fees, overhead, and salary. Open the Shadow Box Custom Framing Service Financial Model Template.

Owner-income model highlights

Revenue: $563k to $295M

Orders: 500 to 2,300

Breakeven, pretax, reserve cash

Can a solo shadow box framer make good money?

Yes—a solo Shadow Box Custom Framing Service can make good money if pricing, throughput, and rework stay tight. In this model, one Master Framer and Owner can be paid $85,000 while the first year reaches 500 orders. The catch is simple: solo work keeps payroll lean, but capacity gets capped by design, quoting, mounting, assembly, and delivery hours.

Money drivers

500 orders is the first-year target

$85,000 supports one owner-framer

Solo payroll stays simple

Pricing must protect margin

Growth levers

Use better templates to cut rework

Batch workflow to raise output

Sell premium heirloom displays

Build repeat referral sources

How many shadow boxes per month to pay yourself?

For a Shadow Box Custom Framing Service, you need about 17 orders per month to pay yourself an $85,000 salary and cover $165,400 in annual fixed overhead. At a $1,126 average ticket, that equals 207 orders a year, and the first-year plan of 42 orders per month clears that base case. Still, reserves, taxes, and rework push the real need higher, so ticket size and margin quality matter before volume.

Base case

$1,126 average ticket

207 orders per year

17 orders per month

Covers $165,400 fixed plus salary

What raises it

First-year plan: 42 orders monthly

Reserves need extra cash

Taxes cut usable profit

Rework lifts required volume

What margins matter most in custom shadow box framing?

For a Shadow Box Custom Framing Service, the margin that matters is after direct job costs, not markup. On $563,000 revenue and $72,895 in direct job costs, gross margin is about 87.1%; add 15.9% more for shipping, marketing, referrals, and payment processing, and owner cash tightens fast. If you’re mapping How To Write A Business Plan For Shadow Box Custom Framing Service?, track waste and rework on every order.

Direct job costs

Museum-grade acrylic protects items.

Hardwood frame stock drives build cost.

Acid-free mounting board adds archive value.

UV glass, matboard, hardware all hit margin.

Cash drains to watch

Shipping cuts cash on every order.

Marketing and referrals add variable spend.

Payment processing trims collected revenue.

Waste and rework reduce owner cash fast.

Shadow Box Custom Framing Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six owner income drivers?

1

Order Volume

500

At 500 first-year orders, revenue reaches about $563K, so missed jobs cut owner income fast.

2

Ticket Size

$1,126

The first-year average ticket sets cash per job, and upsells lift take-home without adding the same labor.

3

Material Margin

871%

The material spread is the main profit cushion, so scrap, remakes, and waste can still swing income.

4

Production Efficiency

$174K

Year 1 EBITDA is about $174K, and faster throughput turns the same shop hours into more owner cash.

5

Fixed Overhead

$6.7K/mo

That monthly overhead sits before profit, and the $85K owner salary makes break-even tighter if volume slips.

6

Customer Mix

$1.9K

More premium and repeat work pushes the mix toward higher-priced jobs, which lifts revenue and smooths demand.

Shadow Box Custom Framing Service Core Six Income Drivers

Average Order Value

Average Order Value

Average order value (AOV) is the dollars earned per completed shadow box order. In this model, first-year AOV is $1,126, rising to $1,281 in the mature year. That $155 lift is about 13.8%, and at 42 orders per month it adds about $6,510 in monthly revenue before costs. One low-ticket job can pull down take-home pay fast.

AOV includes what you charge for complexity, design time, preservation materials, acrylic or glass choice, mounting difficulty, and perceived value. First-year examples show the spread: sports jersey boxes at $1,250, military medal cases at $850, wedding keepsake frames at $1,100, corporate award boxes at $950, and heirloom display cases at $1,650.

Raise Ticket Size

Track AOV by job type, not just total sales. If the mix shifts toward lower-priced pieces, revenue quality drops even when order count stays flat. The owner should review quoted price versus final invoice, discount rate, and the share of jobs above $1,250. That keeps pricing tied to labor and materials, not guesswork.

Price for design time and mounting difficulty.

Separate premium and standard product lines.

Test add-ons like upgraded glazing.

Block underpriced custom work early.

Here’s the quick math: if AOV rises by $100 on 42 monthly orders, revenue improves by about $4,200 per month. That lifts cash flow without adding shop hours. What this hides is rework risk: if complex jobs are underpriced, the extra revenue can vanish in labor and material waste.

1

Completed Order Volume

Completed Order Volume

Completed order volume is the number of jobs the shop finishes, ships, and bills. Here, year one is about 500 orders, or 42 orders per month, and the mature year rises to 2,300 orders. Owner income only climbs if jobs move through approvals, mounting, drying, fragile handling, and final check without backlog or rework.

Here’s the quick math: first-year breakeven for fixed overhead plus the $85,000 owner salary is about 17 orders per month at first-year economics. That leaves room above break-even, but delays in approvals or rework can still trap cash in work-in-progress and slow owner pay. One late job can tie up time from several new orders.

Keep Jobs Moving

Track WIP (work in progress) by stage: waiting on approval, in mounting, drying, inspection, and rework. That shows where volume stalls and where labor gets buried. The owner should watch completed orders per month, average days in each stage, and the share of jobs sent back for fixes. More completed jobs with the same staff lift take-home income.

Use simple controls that protect throughput: get design sign-off before build, batch similar mounts, and flag fragile pieces early. If approvals slow down, the shop’s monthly output falls below the 17-order breakeven line fast. At 500 annual orders, every extra completed job helps spread fixed overhead and supports the owner salary without adding another payroll layer.

Count completed jobs, not booked jobs.

Measure rework on every order.

Separate fragile jobs from standard work.

2

Material Margin

Material Margin

If direct job costs run hot, owner pay shrinks fast. Material margin is what stays after materials and job-level COGS, so it decides how much of each order can fund overhead and the owner’s draw. In this shop, that includes moulding, acrylic, glass, matboard, backing, mounting hardware, preservation supplies, lighting kits, engraved plates, waste, and vendor pricing.

The model’s first-year note says direct job costs are about 130% of revenue, so that figure needs a definition check; the mature-year note shows about 87.9% gross margin. Either way, custom waste and rework can wipe out planned profit before fixed overhead or owner pay.

Control Waste and Rework

Track each job’s parts list, scrap rate, and rework time. Here’s the quick math: if approvals slip after cutting starts, you pay twice, once in materials and again in labor. Lock specs before production, and use one approved supplier list so vendor price swings do not quietly eat margin.

Quote from approved parts only.

Track waste by job type.

Flag rework before assembly.

On 500 orders, even $5 of avoidable waste per job means $2,500 lost. That is cash that should be covering overhead and helping the owner take money home.

3

Production Efficiency

Labor Hours Per Job

The same $563,000 revenue can pay out very differently when each shadow box takes more shop time. With only the Master Framer and Owner paid at $85,000, unpaid owner labor is the real capacity limit. If quote, design, mounting, fitting, assembly, inspection, and rework run long, owner draw gets squeezed.

Hours are the hidden lever. Faster flow means more completed jobs from the same labor base, so the owner can keep salary fixed and still raise profit. If approvals lag or rework spikes, the shop sells revenue but gives up cash to wasted time.

Measure Stage Time

Track labor hours by stage, not just by order. Use separate buckets for quote time, design consultation time, object mounting time, fitting, assembly, inspection, and rework. That shows which jobs burn the most labor and which ones protect owner pay.

Log hours for every job step.

Cut touches with templates.

Batch cut common parts.

Require clear client approvals.

Keep shop flow organized.

Here’s the win: fewer labor hours per finished box means more jobs completed before adding payroll. That lifts gross profit and leaves more cash for owner pay, even when revenue stays flat.

4

Fixed Overhead

Fixed Overhead

Fixed overhead is the monthly nut you pay before owner pay. Here, it is $6,700 per month or $80,400 per year, led by $4,500 for workshop rent, plus utilities and climate control, hosting, insurance, photography, and design software. These costs hit whether you sell one shadow box or ten.

This matters because every order has to cover that base cost first. With this overhead level, the first-year model says breakeven before owner pay is about 8 to 9 orders per month. If order volume or gross profit slips below that pace, owner pay gets squeezed fast. One line says it all: the rent clock never stops.

Control the monthly nut

Track each fixed line monthly: $4,500 rent, $850 utilities and climate control, $250 hosting, $350 insurance, $600 photography, and $150 design software. Then compare total fixed overhead to gross profit per completed order, not just sales. That tells you how many jobs the shop needs before owner pay starts.

Test the setup that lowers the nut without cutting quality. A storefront needs more gross profit than a home-based or appointment-based shop, so use the space only if it adds enough completed orders or higher ticket work. If overhead stays at $6,700, plan cash around that floor and keep a monthly buffer for slow booking periods.

Review fixed costs every month.

Map orders needed to cover rent.

Compare storefront versus appointment-only costs.

Hold cash for slow booking months.

5

Premium And Repeat Customer Mix

Premium and Repeat Mix

Owner income improves when the shop sells more high-value, repeat work instead of filling the calendar with low-dollar one-offs. Source pricing shows $1,650 heirloom display cases and $1,250 sports jersey boxes, both above the $1,126 average ticket, so mix can lift revenue without more orders.

The cash effect is simple: repeat demand from collectors, schools, teams, veterans, wedding clients, local businesses, and award programs lowers pressure on paid marketing, which starts at 80% of revenue. The risk is crowding out premium jobs with smaller orders that use time but not enough margin to pay the owner well.

Raise Premium Share

Track revenue by category, not just total sales. Split out repeat versus one-off jobs, then compare each group against the $1,126 average ticket and the higher-priced lines at $1,250 and $1,650. That shows which jobs actually support owner pay and which ones just keep the shop busy.

Use a simple filter before quoting: if a job is low value and blocks a premium order, price it high or pass. Keep a monthly log of paid-lead revenue versus repeat revenue, because every returning customer reduces the need for expensive ad spend and leaves more gross profit for the owner draw.

Measure repeat rate monthly.

Price premium work first.

Protect capacity for high-ticket jobs.

Cut low-value jobs that clog flow.

6

Shadow Box Custom Framing Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner income cases

Owner income scenarios

Owner income moves with order count, ticket size, and staffing load. The low, base, and high cases show how fast fixed workshop costs get spread across more custom jobs.

Three planning cases for owner take-home at different operating scales.

Scenario

Low CaseLean launch

Base CaseScaled shop

High CaseHigh-volume custom operation

Launch model

The shop stays lean in the first year and earns the lower modeled owner income path.

The shop reaches the modeled middle path and turns steadier volume into stronger owner income.

The shop reaches the stronger upside path and converts high volume into the top owner income case.

Typical setup

Year 1 runs at 500 orders, about $563,000 revenue, one owner framer, an $85,000 owner salary, and $80,400 fixed overhead.

Year 3 reaches 1,180 orders, about $1.419 million revenue, a 1.0 FTE owner, 2.0 FTE apprentice labor, and one customer design consultant.

In the mature year, the model reaches 2,300 orders, about $2.947 million revenue, 3.0 FTE apprentices, and 2.0 FTE design consulting support.

Cost drivers

500 orders

$1,126 ticket

15.9% variable expenses

$80.4k fixed overhead

$85k owner salary

1,180 orders

$1,202 ticket

apprentice and consultant staffing

lower shipping rate

fixed overhead spread

2,300 orders

$1,281 ticket

higher labor scale

more marketing reach

fixed costs diluted

Owner income rangeBefore owner reserves

$235kLow income

$870kTarget income

$2.04mUpside income

Best fit

Use this to stress-test a slow launch and see if the shop still covers core costs.

Use this as the working plan for a shop that has repeat demand and a fuller bench.

Use this to test what the business can do if demand stays strong and capacity keeps up.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The researched model includes $85,000 in planned owner pay before tax That sits on first-year revenue of $563,000 from 500 completed shadow boxes at a $1,126 average ticket Any extra draw depends on taxes, reserves, debt, benefits, and whether the owner keeps enough cash for materials and growth

At first-year economics, breakeven for fixed overhead plus $85,000 owner pay is about 17 completed orders per month The model plans about 42 orders per month in the first year That cushion depends on keeping contribution near 712% after direct job costs, shipping, marketing, referrals, and card fees

Not always, but this model assumes a workshop with $4,500 monthly rent and $6,700 total fixed overhead A home-based or appointment-based shop may lower overhead, but it can limit walk-in traffic, production space, storage, photography, and customer trust for fragile keepsakes The right setup depends on volume and local demand

Average ticket, completed order volume, material margin, workflow, overhead, and customer mix drive profit In the first year, the model uses a $1,126 average ticket, 500 completed orders, and about 871% gross margin after direct job costs Rework, waste, slow approvals, and weak pricing can quickly cut owner cash

Raise owner income by selling more premium work and finishing jobs faster without quality slips Heirloom display cases price at $1,650 and sports jersey boxes at $1,250 in the first-year model, above the $1,126 average ticket Pair that with repeat sources like teams, schools, veterans, wedding clients, and local businesses

About the author

William Hayes

Small Business Consultant

William Hayes is a small business consultant at Financial Models Lab who writes for early-stage founders building a basic plan before investing money. He focuses on business plan basics and practical everyday business finance, helping readers use realistic assumptions to understand revenue, expenses, and profit in simple terms. His direct, useful approach is designed to give new founders a clearer path from idea to informed decision.

Choosing a selection results in a full page refresh.