How Much Skin Care Clinic Owners Make: $297K Year 1 Owner Benefit

You’re trying to separate clinic sales from what the owner can actually keep In this 5-year model, Year 1 revenue is $702k per month, listed operating profit is $1769k per year, and owner benefit can reach $2969k before tax if the owner fills the $120k Clinic Director role This excludes tax advice, legal guidance, debt service, and reserve policy

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, reserves, and reinvestment. This is not guaranteed salary, tax advice, or owner distribution advice.

Want the full forecast view for Skin Care Clinic?

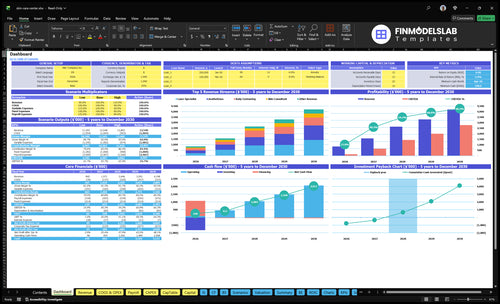

The screenshot shows dashboard, revenue build, assumptions, staffing, expenses, capital spending, scenarios, and owner-income outputs tied to $702k Year 1 monthly revenue and $3,499k Year 5; open the Skin Care Clinic Financial Model Template.

Owner-income model highlights

Owner take-home outputs

Revenue and margin drivers

Low, base, high cases

How much revenue does a skin care clinic need to pay the owner?

A Skin Care Clinic needs about $515k per month in revenue to cover the modeled $120k owner-director pay before debt and reserves. Here’s the quick math: $178k fixed overhead plus $129k non-owner payroll plus $100k owner salary, and the same model also points to about $653k per month for more cushion. Revenue alone does not guarantee owner pay if capacity, debt, or staffing costs move.

Core cost stack

$178k fixed overhead

$129k non-owner payroll

$100k owner salary

$515k/month revenue target

What can move it

$653k/month adds cushion

Debt reduces owner cash

Staffing changes break-even

Capacity limits sales fast

What affects skin care clinic profit margins?

Skin Care Clinic profit margins are driven mostly by utilization, service mix, staffing, marketing efficiency, fixed overhead, and equipment financing. Year 1 is tight: listed COGS is 90%, variable costs are 120%, fixed overhead is $178k/month, and payroll is $2.75M/year, so even small capacity gains matter. A 5-point lift across Year 1 service lines adds about $64k in monthly revenue and $51k in monthly contribution before fixed costs; if you’re sizing the buildout, see How Much Does It Cost To Open, Start, And Launch Your Skin Care Clinic?.

Main levers

Utilization drives revenue fast.

Service mix lifts ticket size.

Marketing shifts revenue by $84k/year per 1 point.

Capacity gains add $51k monthly contribution.

Cost pressure

COGS is listed at 90%.

Variable costs are listed at 120%.

Payroll is $2.75M/year.

Equipment-heavy services raise supervision and debt pressure.

How much can a skin care clinic owner make after expenses?

A Skin Care Clinic owner can make about $296.9k in Year 1 owner benefit before tax if they also fill the $120k Clinic Director role; for growth context, see What Is The Current Growth Rate Of Clientele At Skin Care Clinic?. Pure business profit after listed expenses is $176.9k, so the extra $120k is pay for work performed, not passive owner profit.

Year 1 Math

Revenue: $842.4k

Fixed overhead: $213.6k

Payroll: $275.0k

Business profit: $176.9k

What It Hides

COGS: 9.0%

Variable costs: 12.0%

Excludes debt service and taxes

Reserves and reinvestment still matter

Skin Care Clinic Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Room Utilization

500%-800%

Higher room use is the biggest lever; it lifts monthly revenue from about $702K to $3.5M and spreads rent and staff over more visits.

2

Service Mix

$100-$800

Shifting from low-ticket consults to body contouring and laser sessions raises revenue per visit and improves margin.

3

Staffing Model

$2.75M-$4.4M

Payroll and owner role choices set the labor load, so staffing too heavy or too thin hits take-home fast.

4

Retention & Retail

30%-25%

Packages, memberships, and retail repeat sales improve cash timing, and lower product cost helps protect margin.

5

Marketing Efficiency

95%-50%

Cutting client acquisition cost from 95% to 50% of revenue keeps more gross profit after each new booking.

6

Fixed Overhead

$178K/mo

Rent, staff, and equipment need cash up front, and the $790K build list makes reserves matter before take-home shows up.

Skin Care Clinic Core Six Income Drivers

Treatment Room Utilization

Treatment Room Utilization

Appointment volume only turns into revenue when rooms, providers, and turnover can keep up. In Year 1, modeled utilization sits at 500% to 600% by service line, then rises to 700% to 800% by Year 5 as provider count, capacity, and pricing increase. Monthly revenue moves from $702k to $3,499k, so owner income is capped by real throughput, not lead volume.

Here’s the quick math: a 5-point utilization lift across Year 1 services adds about $64k in monthly revenue before quality limits. What this hides is the cost of no-shows, longer treatments, cleaning time, room turnover, and provider burnout. Full rooms with weak results can hurt repeat bookings and reduce take-home profit later.

Track Capacity, Not Just Bookings

Measure booked hours, completed visits, no-show rate, treatment length, and turnaround time by service line. Use those inputs to set a hard capacity cap per room and per provider, then forecast revenue from completed visits only. If utilization is already near the top of range, raise prices or add staff before pushing more volume.

Watch repeat bookings and recovery time too. If cleaning, charting, or burnout slows the schedule, the extra slots won’t reach owner pay. The clean target is simple: more completed visits per hour without losing outcomes.

1

Service Mix And Average Ticket

Service Mix And Average Ticket

Your income here is not just visit count. It depends on which services fill the schedule. Year 1 prices run from $100 for skin consults to $800 for body contouring, with aesthetician visits at $150, laser services at $400, and dermatologist visits at $300.

At the modeled $236 average ticket across 298 monthly utilized visits, gross revenue is about $70,328 a month. Busy schedules do not equal healthy profit. If the mix shifts toward higher-ticket services, owner income can rise, but only if labor, supervision, and fixed costs stay in check.

Price The Mix, Not Just The Visit

Track average ticket, gross margin, and utilization by service line each month. Compare consults, aesthetician visits, laser, dermatologist, and body contouring separately so you can see which services actually fund rent, payroll, and owner draw. Here’s the quick math: higher ticket helps only when the added margin beats the added service cost.

Measure revenue per service line.

Watch labor and supervision cost.

Price for maintenance and training.

That matters because equipment-heavy or regulated services need licensing, supervision, training, maintenance, and capital. With listed equipment and build-out items at $790k, pricing must cover more than supplies. If consults dominate and conversion stays weak, the clinic can stay booked and still leave too little cash for owner pay.

2

Staffing Model And Owner Role

Staffing Cost And Owner Seat

This driver is the labor stack: provider pay, commissions, front-desk coverage, and management time. In Year 1, provider count is 6 and listed payroll is $2.75m; by Year 5, headcount rises to 17 and payroll to $4.4m. That gap decides how much revenue stays as owner income after wages are paid.

The $120k Clinic Director seat can be owner compensation if the owner works it. Year 1 separate operating profit is $1.769m, but replacing paid labor raises owner workload too. One line: more payroll relief can mean more owner hours, not just more profit.

Track Labor by Role

Measure labor by role every month so payroll lines up with booked visits and service mix. If commissions, hourly support, and director duties blur together, you can’t tell whether profit is paying for growth or just replacing work the owner now does.

Provider hours by service line

Commission and hourly support pay

Front-desk coverage hours

Clinic Director workload

Net profit after labor

If staffing grows faster than booked capacity, owner pay gets squeezed even when revenue rises. Forecast labor against visit volume before you add heads.

3

Retention, Memberships, Packages, And Retail

Retention, Packages, and Retail

This driver is about turning a first treatment into the next visit, the next package, and the next home-care sale. The model’s retail inventory cost is 30% of retail revenue in Year 1, easing to 25% by Year 5, but it does not show a separate product attachment rate, so retention and product sales need their own forecast lines.

Here’s the quick math: more repeat bookings and prepaid packages means steadier monthly visits, fewer empty slots, and better use of fixed provider time. But prepaid revenue also creates future service obligations, so cash comes in now while labor is delivered later. If visits fall, owner income gets hit twice: less service revenue and weaker retail pull-through.

Track Repeat Visits and Attach Rate

Track repeat booking rate, package sales, memberships, prepaid services, and product attachment by provider and treatment type. The key question is whether each consult creates a next appointment and a home-care sale. Stable monthly visits are what protect owner pay.

Measure 30-day rebook rate.

Track retail units per visit.

Separate cash from earned revenue.

Price packages above single visits.

Watch future fulfillment capacity.

What this estimate hides is the lag between cash collected and services still owed. If prepaid volume grows faster than capacity, margins can look fine while future schedules get crowded. That is where owner draw gets squeezed, because the clinic has cash now but no room later.

4

Marketing Efficiency And Local Demand

Local Demand Efficiency

If local demand is weak, marketing burns cash before it becomes clinic income. In Year 1, Marketing and Client Acquisition is 95% of revenue, about $800k annually, so the clinic needs consults that fit capacity and turn into booked treatments fast. One extra lead does nothing unless it becomes a paid visit and then a repeat visit.

By Year 5, marketing drops to 50% of revenue, about $2,099k annually on a much larger base, so owner income improves only if local search demand, reviews, referrals, and consultation conversion stay strong. Payment Processing and Referral Fees stay at 25%, so weak conversion or low repeat bookings hits cash flow and leaves less profit to draw.

Track Leads to Repeat Visits

Measure the full path: leads, consult bookings, show rate, treatment conversion, and repeat bookings. That is the real marketing cost per paying client. If leads rise but consults or repeats do not, spend is not buying owner income. Leads are not revenue until they fit capacity, convert to visits, and come back.

Keep a weekly eye on local search rankings, review count, referral share, and conversion by source. Cut channels that bring cheap leads but poor follow-through, and fund the ones that produce booked treatments. Here’s the quick math: lower cost per booked visit and higher repeat rate lift gross profit, which is what pays the owner after ads and fees.

5

Fixed Overhead, Equipment, And Reserves

Fixed Overhead And Owner Pay

With $178k per month in fixed overhead, this clinic has a heavy cash burn before the owner takes anything home. $120k rent is about 67% of that load, so even a busy month can still leave thin distributable profit if staffing, utilities, software, and other fixed costs stay high.

What this hides: debt service and cash reserves sit outside operating profit. So a clinic can show profit on paper and still limit owner draws while paying loans or rebuilding cash. One clean rule: if fixed overhead rises faster than booked visits, owner pay gets squeezed first.

Track Cash Burn Before You Fund Draws

Watch fixed overhead as a share of monthly revenue, and split it by rent, payroll support, software, insurance, cleaning, security, and office supplies. Here’s the quick math: the $790k launch capital is mostly tied up in $520k of devices and diagnostic equipment, or about 66% of the total, so cash recovery depends on steady utilization, not just booked sales.

Set owner pay after you fund loan payments and a reserve target, not before. If bookings soften or collections lag, the first fix is usually overhead control, lease terms, and equipment pacing, because those choices decide whether profit turns into distributions or stays trapped in the business.

6

Skin Care Clinic Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with ramp-up speed, provider count, visit volume, and equipment use. Payroll and fixed overhead still set the floor, so the gap between cases is wide.

Low, base, and high owner income cases for a skin care clinic.

Scenario

Low CaseRamp-up risk

Base CaseCapacity risk

High CaseEquipment risk

Launch model

This lower case uses Year 1 ramp-up with 6 providers and 298 monthly utilized visits at a $236 average ticket.

This middle case uses Year 3 scale with 12 providers and 834 monthly utilized visits at a $264 average ticket.

This upside case uses Year 5 maturity with 17 providers and 1,350 monthly utilized visits at a $259 average ticket.

Typical setup

The clinic brings in about $702k in monthly revenue, carries $178k fixed overhead and $229k monthly payroll, and the owner is acting as Director.

The clinic reaches about $2.205M in monthly revenue with a $367k monthly payroll and a fuller operating team.

The clinic reaches about $3.499M in monthly revenue and depends on heavy equipment use and a larger staffing load.

Cost drivers

Year 1 ramp-up

6 providers

298 utilized visits

$236 ticket

$229k payroll

Year 3 scale

12 providers

834 utilized visits

$264 ticket

$367k payroll

Year 5 maturity

17 providers

1,350 utilized visits

$259 ticket

equipment load

Owner income rangeBefore owner reserves

$2.97MDebt reserves off

$1.65MDebt reserves off

$3.04MDebt reserves off

Best fit

Use this to stress-test slow opening months and early staffing ramp.

Use this as the core plan if execution lands near the model.

Use this to test what happens if demand fills capacity and equipment stays busy.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions, and they exclude debt reserves.

Under the model, Year 1 owner benefit is about $2969k before tax if the owner fills the $120k Clinic Director role That includes $1769k operating profit after listed costs plus the Director salary It does not include debt service, reserves, taxes, or any provider pay not listed separately

The model shows stronger owner economics after the early ramp-up, not in the launch months Monthly revenue rises from $702k in Year 1 to $1309k in Year 2 and $2205k in Year 3 Stability depends on utilization, repeat visits, marketing efficiency, staffing coverage, and keeping enough cash for equipment and reserves

Retail can help, but the model does not provide a separate retail sales attachment rate It does include retail product inventory cost at 30% of revenue in Year 1 and 25% by Year 5 Add retail sales, gross margin, and reorder timing to see whether products raise owner take-home or just tie up cash

Utilization and service mix have the biggest visible impact in this model Year 1 capacity runs 500% to 600%, while Year 5 reaches 700% to 800% Prices also vary widely, from $100 consultations to $800 body contouring visits Payroll, rent, marketing, equipment debt, and reserves decide how much profit becomes owner cash

Use a target that fits contribution margin and cash needs In Year 1, about $515k in monthly revenue covers listed fixed overhead, non-owner payroll, and the $120k Director salary at a 790% contribution margin The modeled clinic reaches $702k monthly revenue, but owner distributions still need room for debt, reserves, and reinvestment

About the author

Samuel Price

Launch Planning Specialist

Samuel Price is a launch planning specialist at Financial Models Lab who helps side-hustle builders test whether a business idea is financially realistic. He turns business questions into clear planning steps, with a focus on operating cost estimates for opening and running small businesses. His research-based writing highlights the common costs new founders often miss.

Choosing a selection results in a full page refresh.