Snow Plowing Owner Income: $85k Pay And Year 2 Profit Potential

Key Takeaways

Contract type shifts weather risk and cash flow.

Dense routes cut costs and raise truck output.

Commercial jobs lift tickets but add complexity.

Reserves protect profit when storms and repairs hit.

Owner income$85k plannedGross margin82%Revenue for target pay≈$104kBusiness difficultyHard

Want to test your snow plowing income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, staffing, taxes, debt, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Snow Plowing Service model?

How much money can you make with a snow plowing business?

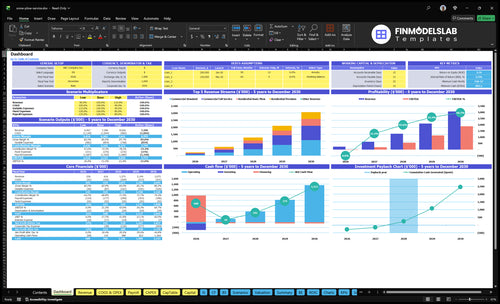

A Snow Plowing Service can create strong winter cash flow, but the modeled annual owner pay is $85,000 while business EBITDA moves from -$34,000 in Year 1 to $1.868 million in Year 5. For the operating goal behind those numbers, see What Is The Primary Goal Of Snow Plowing Service?, because per-push work rises during frequent storms while seasonal contracts smooth revenue.

Modeled Earnings

Year 1 EBITDA: -$34,000

Year 2 EBITDA: $192,000

Year 3 EBITDA: $556,000

Owner pay: $85,000 annualized

What Drives It

Account count sets route density

Commercial mix lifts contract value

Service time controls labor capacity

Reserve policy protects slow winters

How many snow plowing customers do you need to make money?

There isn’t one fixed customer count for a Snow Plowing Service, because the answer depends on active winter months and storm count. Use this formula: required revenue ÷ (average monthly account price × active months). On the Year 1 mix, the weighted monthly account price is $471 and the business needs about $250,000 in revenue before taxes, reserves, capex, and debt service at 73% contribution, with route time and service windows capping accounts per truck.

Revenue need

$85,000 owner pay

$22,500 admin pay

$55,200 fixed overhead

$20,000 marketing

Pricing mix

45% at $180

25% at $320

20% at $800

10% at $1,500

Is a snow plowing business profitable?

A Snow Plowing Service can be profitable, but Year 1 is tight; for startup cost context, see What Is The Estimated Cost To Open And Start Your Snow Plowing Service Business?. In Year 1, direct job costs are 18% of revenue, variable expenses add 9%, and the contribution margin is 73% before overhead. With $4,600 in monthly fixed expenses before payroll, EBITDA is -$34,000 in Year 1 and $192,000 in Year 2.

Year 1 price points run $180 basic, $320 premium, $800 commercial standard, and $1,500 full service, so the contract mix you sell sets revenue per account and payback speed.

2

Customer Mix

45%→30%

Basic residential falls from 45% to 30% while premium and commercial shares rise, so average monthly revenue climbs even if stop count stays flat.

3

Route Density

$4.6K/mo

With $4,600 of fixed overhead each month, tighter routes spread that base across more billable work and protect owner take-home.

4

Labor Model

18%

Direct job cost starts at 18%, and with $85,000 owner pay, tighter dispatch and less overtime keep more of each storm dollar.

5

Equipment Cost Control

4%

Equipment maintenance is 4% of revenue in Year 1, and every breakdown can hit the broader 9% variable-expense layer too.

6

Salt Add-ons

3%

Salt and de-icing fluids start at 3% of revenue, so clean add-on billing can lift ticket size without much extra labor.

Snow Plowing Service Core Six Income Drivers

Contract Structure And Weather Risk

Contract Structure Drives Weather Risk

Per-push pricing puts weather risk on the owner: more plowable storms mean more revenue, but mild winters cut cash fast. Seasonal contracts do the opposite. Billing is steadier, yet a heavy storm stack can squeeze margin because labor, fuel, and salt hit before the month’s money is fully earned.

Track per-push jobs, seasonal accounts, commercial retainers, and salting add-ons separately. That mix drives gross margin, reserve needs, and how much the owner can safely draw. No model can assume guaranteed snowfall or an exact local storm count, so cash planning has to stay flexible.

Measure Weather Risk By Contract Type

Build the forecast around contract type, not one blended number. The key inputs are account count, service frequency, add-on rate, and how much revenue is fixed versus storm-based. That shows whether the business is paid for risk or just taking it on. One clean rule: if seasonal billing stays flat while storm volume rises, margin pressure shows up first in labor and fuel.

Watch the cash gap between service dates and customer billing dates. If per-push volume spikes, invoices rise with the storm cycle; if winters are mild, the issue is underused crew time and lower take-home pay. The owner should set reserves from each storm season, since weather does not pay on schedule.

1

Route Density And Truck Capacity

Route Density

Route density is how many accounts one truck can clear inside a storm window. Denser routes cut windshield time, fuel, labor hours, and missed service calls, so more of each monthly service dollar turns into owner take-home. In Year 1, the model’s service-time assumption is 15 hours per active customer per month, rising to 18 hours by Year 5, so capacity has to be checked against actual route time, not just sold accounts.

Here’s the quick math: more accounts per truck can lift revenue without adding a second unit, but only if route travel time, service window, storm timing, and equipment limit still allow on-time completion. If routes get too full, the hidden cost is overtime, re-dispatch, and missed windows, which hits margin and can delay owner draws.

Track Truck Load

Build the route plan around accounts per truck, average service time, route travel time, and the service window. A simple control test is whether total booked hours stay below what the truck can clear in the storm cycle, with room for travel and weather delays. If you don’t leave slack, you risk overbooking routes that can’t be cleared on time.

Use a route sheet that shows each stop, expected minutes on site, and the latest acceptable arrival time. One clean rule: if a route only works when everything goes right, it’s already too tight. Tight routes usually improve cash flow and profit; overloaded routes do the opposite by creating call-backs, fuel waste, and labor spikes.

Accounts per truck by storm

Minutes per stop and travel time

Storm timing and service window

Equipment limit for each route

2

Customer Mix And Average Ticket

Customer Mix

Average ticket is the weighted blend of job types. In Year 1, pricing runs from $180 for Residential Basic Plow to $1,500 for Commercial Full Service, so one commercial account can equal 8.3 basic residential jobs. More commercial work lifts revenue fast, but it also raises response pressure and proof-of-service needs.

That mix changes take-home income because commercial lots usually need de-icing, dispatch coverage, and tighter timing. Year 5 prices rise to $220, $380, $1,100, and $2,000, but the higher ticket only helps if added insurance, labor, and liability do not eat the spread.

Track Mix by Job Type

Measure revenue by each service line, not just total jobs. Watch the share of Residential Basic, Residential Premium, Commercial Standard, and Commercial Full Service, plus add-on salting. The key question is simple: does the higher ticket cover the extra dispatch, proof, and insurance work?

Track revenue per stop

Separate commercial from residential

Test add-on attach rate

Watch gross margin by account

If commercial jobs slow routing or require standby crews, cash can fall even when sales rise. Keep a job-level margin view so the next storm gets priced with real data, not guesswork.

3

Labor Model And Owner Involvement

Owner-Operator Labor Mix

If you plow the routes yourself, the business can look stronger because your labor replaces paid driver hours. That still is not true profit. For this model, treat $85,000 as owner pay, then separate it from labor replacement cost, driver payroll, subcontractor cost, and after-reserve distributions.

Here’s the quick math: seasonal labor is 10% of revenue in Year 1 and 8% by Year 5. Hiring drivers or subs can lift capacity, but it also cuts margin and adds scheduling risk on storm days. The owner’s take-home only improves if labor stays below that band and routes stay covered on time.

Track Pay After Labor

Measure labor in three buckets: owner replacement hours, paid driver wages, and subcontractor spend. If you mix them together, you can overstate profit and underprice routes. The key input is hours worked per storm, plus the labor rate tied to each route type.

Set owner pay at $85,000

Track labor as % of revenue

Separate subs from payroll

Reserve cash before draws

Test whether one owner-run truck or a mixed crew gives better after-reserve income. If subcontractors raise coverage but push labor above 10% in Year 1, owner income may look busy but still land lower after reserves and storm delays.

4

Equipment, Insurance, Repairs, And Reserves

Equipment, Insurance, Repairs, and Reserves

This driver is the cash load behind the fleet: $238,000 of starting equipment, plus $1,200 a month for commercial general liability insurance and $800 a month for vehicle registrations and fixed insurance. Repairs run at 4% of Year 1 revenue, so every $100,000 sold needs about $4,000 set aside just to keep trucks and attachments working.

That upfront $238,000 ties up cash before profit shows up. One breakdown in a storm can stop revenue and owner draws at the same time, because the missed route, the repair bill, and the labor still standing by all hit cash flow at once.

Build the storm reserve first

Track equipment uptime, repair spend, and reserve balance by truck and by storm. The real inputs are revenue, active vehicles, storm count, and service volume, because wear rises with use and bad weather speeds it up. With $2,000 a month in fixed insurance and registrations before repairs, the fleet has to stay busy just to cover carrying costs.

Set a reserve rule tied to revenue and route risk, not gut feel. Here’s the quick math: 4% of revenue for repairs, plus a cash buffer for storm downtime, so owner distributions should wait until the reserve is funded. If the fleet is overworked or maintenance slips, take-home pay drops fast because the first cash goes to keeping the equipment alive.

5

Salting, De-Icing, And Sidewalk Add-Ons

Salting And Sidewalk Add-Ons

When a snow job adds salt, de-icing fluid, or sidewalk clearing, the invoice gets bigger without needing a full new plow stop. The model assumes these materials run at 3% of revenue in Year 1, easing to 2% by Year 5. That lifts average revenue per account, especially on premium residential and commercial full-service jobs.

The catch is margin. You still pay for labor, storage, spreaders, documentation, and slip-risk control. One late call or wasted load can turn a good add-on into extra cost, so the real gain shows up only when material use stays tight and service timing is reliable.

Track Attach Rate And Material Waste

Measure how many accounts buy salting or sidewalk clearing, then compare that extra revenue to salt, de-icer, and labor time. Keep a simple log by stop: pounds used, minutes spent, and whether the job was billed as an add-on. That tells you if the add-on is padding ticket size or just adding work.

Price for response speed and liability, not just material cost. If storage loss, re-visits, or missed documentation push materials above the 3% to 2% range, owner take-home drops fast because the add-on is supposed to support profit and retention, not absorb it.

6

Snow Plowing Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: Compare lean, base, and high snow plow owner pay scenarios

Owner income scenarios

Owner income moves with snow volume, account mix, and how fast fixed overhead is covered. These cases show a ramp year, a scaled year, and a mature year.

Compare early ramp, scaled, and mature owner income paths.

Scenario

Low CaseRamp

Base CaseScaled

High CaseMature

Launch model

This is the early ramp case, where owner income stays close to salary while the book of work builds.

This is the modeled scale case, where owner income improves as the customer base and route density grow.

This is the stronger mature-year case, where owner income rises with premium commercial pricing and better job economics.

Typical setup

Year 1 is a ramp year: owner pay is $85,000, EBITDA is -$34,000, and the business is still absorbing $4,600 of monthly fixed overhead and $238,000 of initial capex.

Year 2 scales with CAC down to $220, EBITDA up to $192,000, and a 32-month payback path as staffing and account mix improve.

Year 5 is the mature case: full-service commercial accounts reach $2,000 per month, direct job costs fall to 14%, and EBITDA reaches $1,868,000.

Cost drivers

82% direct gross margin

73% contribution margin

$250 CAC

$20,000 marketing

$4,600 monthly fixed overhead

$220 CAC

$192,000 EBITDA

32-month payback

growing commercial mix

$35,000 marketing

$1,868,000 Year 5 EBITDA

$2,000 full-service monthly price

14% direct job costs

$180 CAC

mature commercial mix

Owner income rangeBefore owner reserves

$85,000 salaryEarly ramp

Salary plus scale profitScale path

Salary plus mature profitMature upside

Best fit

Use this to stress-test the first season and cash pressure.

Use this for second-year planning and hiring decisions.

Use this to test upside if pricing and commercial mix stay strong.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model carries $85,000 in annual Owner / Operations Manager pay That is planned owner pay, not guaranteed take-home or tax salary advice Business EBITDA is -$34,000 in Year 1, then $192,000 in Year 2, so early cash discipline matters before distributions make sense

The model reaches breakeven in Month 9, with payback in 32 months That assumes the planned pricing, customer mix, labor percentages, fixed costs, and startup capex hold If storms are light, routes are spread out, or repairs spike, breakeven can move later

You don’t need only commercial accounts, but the mix matters Year 1 pricing is $180 per month for basic residential, $320 for premium residential, $800 for standard commercial, and $1,500 for full-service commercial Commercial work can raise revenue, but it can also raise insurance, response, documentation, and liability demands

The biggest drivers are contract structure, route density, customer mix, labor model, equipment cost, and salting or de-icing add-ons In Year 1, direct job costs are 18% of revenue and variable costs add 9% That leaves 73% contribution before fixed overhead, payroll, reserves, taxes, and debt service

Build reserves before taking extra draws This model has $4,600 in monthly fixed expenses, $85,000 in owner pay, $238,000 in initial capex, and a Month 14 minimum cash point shown in the core metrics Seasonal contracts, dense routes, repair reserves, and clear salting pricing reduce cash surprises

About the author

George Lawson

Small Business Advisor

George Lawson is a small business advisor at Financial Models Lab who focuses on startup cost planning for local business owners preparing to launch. He studies common expenses, revenue drivers, and launch requirements to help turn a business idea into a basic, workable plan. George also writes about pricing and profitability basics in a practical, plain-spoken way, with a focus on helping readers make smarter decisions before they open their doors.

Choosing a selection results in a full page refresh.