How Much Split-Level Renovation Owners Make: $115k+ Planning View

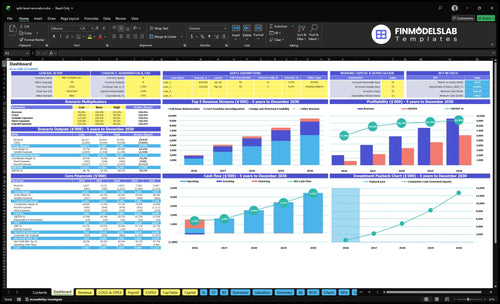

A split-level renovation business owner’s take-home depends on salary, profit distributions, reserves, and reinvestment In the researched assumptions, the owner-role salary is $115,000, while EBITDA ranges from $849,000 in the first year to $6049 million in Year 5 before taxes, debt service, reserves, and owner distributions Year 2 revenue is $4115 million, with a modeled gross margin of 727% after listed direct and variable project costs Treat these as planning assumptions, not promised income

Owner income$115k baseNet margin55%–64%Revenue for target pay$180k–$210kBusiness difficultyHard

Want to test your owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay for a split-level home renovation business.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Anchors include $115k owner-role salary, $45k-$95k marketing, $1,500-$1,300 CAC, and about $1.092M annual fixed overhead in the planning model.

Does a split-level renovation business make more when the owner stops doing field work?

No—stopping field work does not automatically make Split-Level Home Renovation more money. It can raise sales and project capacity, but only if added crews finish profitable jobs faster than overhead grows. Here’s the quick read: staffing rises from 2 master carpenters in Year 1 to 5 in Year 5, adds project management in Year 2, and increases designer capacity, so owner income improves only when payroll is matched by completed work; otherwise cash flow gets squeezed by payroll timing and unfinished jobs.

Why it can help

More crews can complete more jobs.

Project management starts in Year 2.

Designer capacity can lift project flow.

Owner income rises if margins hold.

Where it hurts

Payroll grows from 2 to 5 carpenters.

QC load rises with each new crew.

Unfinished work traps cash on site.

Cash flow tightens before invoices clear.

Can a split-level renovation business owner make a full-time income?

Yes, a Split-Level Home Renovation owner can make a full-time income in this model, with an owner-role salary of $115k, but only after project revenue covers direct job costs, overhead, payroll, reserves, and reinvestment; see How Do I Launch Split-Level Home Renovation Business? for the launch path. The model reaches breakeven in Month 4, payback in 8 months, and Year 2 shows $4.115M revenue with $2.257M EBITDA before taxes, debt service, and reserves.

Income Test

Owner salary modeled at $115k

Breakeven reached in Month 4

Payback modeled at 8 months

Year 2 EBITDA margin: 54.8%

Distribution Rules

Pay crews before owner draws

Fund reserves before distributions

Delay draws if permits slip

Protect cash during crew gaps

How much revenue does a split-level renovation business need to pay the owner?

For Split-Level Home Renovation, the Year 2 cost stack is already $1.742M before you even count completed-work costs, so the owner-pay target has to be built into revenue from day one. That means you should work backward from the $115k owner-role salary, not from signed contracts, because booked sales, deposits, progress billings, and collected cash are different buckets. Here’s the quick math: the business must clear the full cost stack first, and then the revenue floor has to support the owner’s pay on top of real job costs.

Year 2 cost floor

$1,092k fixed overhead

$60k marketing

$475k total payroll

$115k owner-role salary

Track revenue the right way

Recognize revenue on completed work

Keep signed contracts separate

Track deposits in a separate bucket

Track billings and cash separately

Split-Level Home Renovation Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six owner income drivers?

1

Project Volume

$4.1M-$9.5M

High confidence: more signed jobs, helped by $45K-$95K of annual marketing, push revenue from $4.1M in Year 2 to $9.5M in Year 5.

2

Gross Margin

71%-78%

Direct costs drop from 29.0% to 22.2%, so more cash from each job stays with the owner.

3

Change Orders

120-140h

Tighter scope control keeps more work billable, with active-customer hours rising from 120 to 140 per month.

4

Price Rate

$115-$170

Higher hourly rates across the job mix lift revenue per booked hour and make each project more profitable.

5

Owner Load

$115K

The principal project director stays at 1.0 FTE with a $115K salary, so hands-on owner work can cap take-home.

6

Fixed Overhead

$109K

Fixed overhead is about $109.2K a year, so leaner overhead drops straight to owner income.

Split-Level Home Renovation Core Six Income Drivers

Completed Projects Per Year

Completed Projects

Completed projects are what turn estimates into recognized revenue. In this model, revenue rises from $4,115M in Year 2 to $9,467M in Year 5, but the completed project count is not supplied, so the real question is throughput, not just leads. Revenue only shows up after work is completed, billed, and collected.

The main bottlenecks are permits, crew availability, inspections, project duration, homeowner decisions, and the owner’s project-management bandwidth. If any one of those slows down, cash comes in later and owner pay gets pushed out, even when booked work looks healthy. One stalled job can tie up labor, materials, and attention.

Track Completion Flow

Track each job from estimate to closeout: sold, started, completed, billed, collected. The owner should watch completion rate, days in process, and the gap between completion and cash collection. That gap matters because costs hit before the customer pays.

Use weekly capacity planning to protect output. Don’t start more work than permits, crews, and inspections can finish on time. If homeowner choices stall the job, lock selections early and document them. That keeps the project count moving and helps protect overhead coverage and owner draw.

1

Average Project Value

Average Project Value

Average project value is the revenue from one completed split-level job, and it rises when scope stays tight. At 160 to 180 hours for full modernization and $115 to $170 per hour, that work bills about $18,400 to $30,600 before materials. Level transitions run 80 to 100 hours, or $9,200 to $17,000; feasibility work at 20 hours bills $2,300 to $3,400.

Higher project value lifts cash per job, but only if labor, permits, and design changes stay inside the estimate. If scope drifts, gross margin drops even when sales look strong. So the real test is simple: did you bill every approved hour and every change, or did unpaid extras eat the owner’s take-home profit?

Price by scope, not guesswork

Track project value by service line: full modernization, level transition reconfiguration, and design and structural feasibility. Build every estimate from hours × rate, then add materials and approved changes. That keeps each job tied to real labor and gives you a cleaner forecast for revenue, gross margin, and owner pay.

Watch the gap between estimated and billed hours. If a 20-hour feasibility turns into unpaid design time, margin disappears fast. Tight scope notes, signed selections, and change-order pricing help protect the $115 to $170 hourly rate and leave more cash for overhead and distributions.

2

Job-Level Gross Margin

Job-Level Gross Margin

Job-level gross margin is what’s left after direct job costs: subcontractor labor pass-through, material markup costs, project insurance and bonding, municipal permits, and inspections. In this model, direct and variable costs total 290% of revenue in Year 1 and 222% in Year 5, so gross margin is still negative before overhead. That means pricing errors, weak allowances, and missing contingencies cut EBITDA and shrink the owner’s draw.

Track Job Cost Hard

Measure each project as sold price minus direct cost, not just hours booked. Track labor, materials, permits, inspections, insurance, bonding, and a contingency before work starts. If the job cost ratio stays above 100%, that project cannot fund owner pay; it only adds volume. Tight estimating and clean change control are the fixes.

3

Change Order Control

Change Order Control

In split-level renovations, change orders only protect margin when the extra work is documented, priced, approved, and scheduled. Stair moves, entryway changes, basement finishing, and homeowner selections can all add scope fast, and if that work is not billed, the owner absorbs the hit in labor, materials, permits, and subcontractor costs.

The key inputs are change-order count, dollar value per change, approval speed, and added days on site. More approved changes can lift revenue, but late or loose changes usually slow billing and cash collection. One clean rule: if it is not signed, it is not free.

Track extras before they hit profit

Use a simple workflow: stop the job, price the change, get written approval, then reset the schedule. Track pending changes, approved dollars, and days added on every project so you can see which jobs are leaking margin and which clients are driving rework.

Build allowances for structural feasibility and finish selections into the base scope, then review them at each site walk. If one project type keeps generating changes, raise the base price or tighten the scope language. That keeps owner pay cleaner and reduces trust damage from surprise invoices.

4

Fixed Overhead Discipline

Fixed Overhead Discipline

Fixed overhead is the cost that stays on the books whether you finish 2 jobs or 12. Here it is $9,100/month, or $109,200/year, before marketing: $4,500 rent, $1,200 liability insurance, $650 software, $1,800 vehicle maintenance and fuel, $400 dues, and $550 utilities and internet. This comes out before owner distributions, so weak volume cuts take-home fast.

Keep marketing separate from direct job costs. With marketing at $45k in Year 1 and $95k in Year 5, total annual overhead rises to $154.2k and $204.2k. Here’s the quick math: overhead climbs before a single profit dollar reaches the owner, so pricing and project flow have to cover both burn and draw.

Track Fixed Cost Burn

Build a monthly fixed-cost sheet and keep direct job costs out of it. Track rent, insurance, software, truck costs, dues, utilities, and internet against $9,100 per month. Then add marketing as its own line, since $45k in Year 1 and $95k in Year 5 can move cash burn far more than small office savings.

Review overhead monthly, before owner pay.

Separate job costs from fixed costs.

Cap vehicle and software creep.

Test marketing spend against booked projects.

Forecast owner draw after fixed overhead, not before it. If project revenue slips, this $109.2k base cost still hits cash, so every delayed collection delays pay. The clean test is simple: does added marketing produce enough finished, billed, and collected work to cover the extra overhead and still leave profit for the owner?

5

Owner Role And Capacity

Owner Role And Capacity

Owner income depends on role design, not just revenue. In this model, owner-role payroll is $115k, so the real question is whether the owner’s time goes to sales, estimating, design oversight, and customer management or gets trapped in hands-on field work. If the owner stays in every task, labor may look cheaper early, but growth slows and take-home pay gets capped.

Income rises only when added staff increases profitable completed work. A project manager at $70k or a carpenter at $75k should pay off through more finished jobs, fewer delays, and better control of margin. If the hire does not lift completion, billing, and collection, it adds payroll without improving owner draw.

Right-size the owner role

Track where the owner spends time. Split hours between sales, estimating, design reviews, client calls, and jobsite labor. The owner should spend less time on tasks that can be delegated and more time on the work that closes deals and protects margin. One clean rule: if the owner is the bottleneck, profit stalls.

Test hires against completed work, not busyness. Before adding a $70k project manager or $75k carpenter, forecast how many more profitable jobs the team can finish and collect. Measure completed projects, gross margin, and owner draw after payroll. If staffing does not raise completed work, it lowers cash flow.

Track owner hours by task

Measure completed jobs per month

Compare payroll to gross margin

Review overdue estimates weekly

Watch client delays and rework

6

Split-Level Home Renovation Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare owner income scenarios for planning

Owner income scenarios

Owner income shifts with project mix, contract value, staffing, and marketing. Lean uses Year 2 scale, base uses Year 3, and high tests Year 5 capacity.

Compare lean, base, and high owner-income cases for a split-level home renovation firm.

Scenario

Lean CaseLean Case

Base CaseBase Case

High CaseHigh Case

Launch model

Lean case uses the lower modeled earnings path and keeps the owner near Year 2 scale.

Base case reflects the middle path and assumes steady scaling into Year 3.

High case reflects the stronger earnings path and tests Year 5 scale.

Typical setup

Revenue tracks Year 2 at $4.115M, EBITDA is $2.257M, marketing is $60k, gross margin is 72.7%, and project count and contract value stay editable.

Revenue reaches $5.839M, EBITDA is $3.486M, marketing is $75k, and the team grows enough to support a fuller delivery load.

Revenue reaches $9.467M, EBITDA is $6.049M, marketing is $95k, payroll rises to about $855k, and gross margin reaches 77.8%.

Cost drivers

project mix

contract value

$60k marketing

staffing load

utilization

project mix

contract value

$75k marketing

staffing mix

delivery capacity

project mix

contract value

$95k marketing

$855k payroll

utilization

Owner income rangeBefore owner reserves

$2.26MLean Case

$3.49MBase Case

$6.05MHigh Case

Best fit

Use this to stress-test a smaller book of work and slower ramp.

Use this as the most likely planning case and budgeting anchor.

Use this if lead flow stays strong and the team keeps utilization high.

!

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model includes a $115,000 owner-role salary and EBITDA of $849,000 in the first year, rising to $6049 million in Year 5 That EBITDA is not owner take-home Taxes, debt service, reserves, warranty costs, and reinvestment still come out before distributions

The researched model reaches breakeven in Month 4 and payback in 8 months It also shows a $740,000 minimum cash need in Month 2, so cash timing matters Early payroll, vehicles, tools, marketing, and project deposits can strain cash before profit appears

Yes, reserves should come before discretionary owner draws This model has $158,000 of startup capex, $45,000 of first-year marketing, and $109,200 of annual fixed overhead It does not provide a specific reserve percentage, so add one in the forecast before estimating distributions

Completed project volume, gross margin, and scope control matter most The model’s gross margin moves from 710% in Year 1 to 778% in Year 5 Subcontractor labor, material allowances, permits, inspections, and unpriced change orders can quickly reduce owner take-home

Plan owner pay with a forecast that separates salary, EBITDA, cash flow, reserves, and distributions Start with the $115,000 owner-role salary, then test revenue from $4115 million to $9467 million and marketing from $60,000 to $95,000 Do not treat booked sales as collected cash

About the author

Oscar Bryant

Startup Planning Writer

Oscar Bryant is a startup planning writer at Financial Models Lab, where he helps early-stage founders make a business idea easier to evaluate through simple financial projections. He breaks down revenue, expenses, and profit in a clear, practical way, with a focus on cost and income assumptions that help readers understand the numbers behind everyday business ideas.

Choosing a selection results in a full page refresh.