How much revenue does a sports bar need to pay the owner?

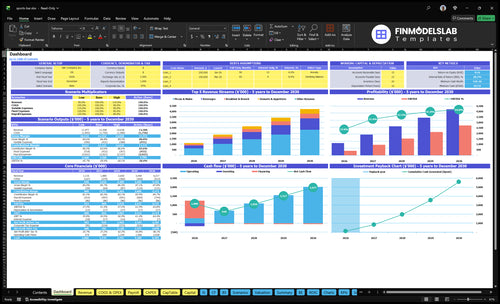

There is no single revenue target for a Sports Bar. Here’s the quick math: with $7,200 in fixed monthly costs and $355,000 in Year 1 payroll, you need about $45,100 in monthly sales before debt, reserves, and owner pay, using the model’s 81.5% contribution margin. That is roughly $541,600 a year, and the model says breakeven lands in Month 3.

What moves the target

Labor changes the target fast.

Rent adds fixed pressure.

Debt raises required sales.

Owner pay sits on top.

Quick revenue math

18.5% direct variable costs.

81.5% contribution margin left.

$36,783 monthly fixed plus payroll.

$45.1k monthly sales before extras.

Can a sports bar owner make money?

Yes, a Sports Bar owner can make money if recurring traffic covers payroll, rent, food cost, beverage cost, and cash reserves; the Year 1 model shows 710 weekly covers and about $24.38k in weekly revenue. The source case reaches Month 3 breakeven and $413k EBITDA, but owner take-home depends on debt, taxes, reserves, and reinvestment; track the demand side here: How Is The Customer Engagement Level For Your Sports Bar?.

Profit Drivers

710 weekly covers

$24.38k weekly revenue

Month 3 breakeven

$413k EBITDA case

Profit Risks

Slow weekdays offset Saturdays

Overtime cuts margins fast

Waste raises food cost

Licensing costs hit cash

How does owner-operated income compare with manager-run profit?

Manager-run profit is lower unless sales volume is strong, because this Sports Bar model already carries a $70,000 General Manager cost from Month 1 through Month 60. That is about $5,833 per month, or $350,000 over 5 years. An owner-operator can save that pay only if they truly cover the work; semi-absentee ownership needs stronger revenue, tighter controls, and enough cash reserves because weak oversight can hurt service and raise theft risk.

Manager-run math

$70,000 GM cost starts in Month 1

Runs through Month 60

Equals about $5,833 monthly

Total cost is $350,000

Owner-operator tradeoff

Save pay only if you do the work

Needs stronger revenue

Needs tighter controls

Needs cash reserves

Sports Bar Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers that move owner pay?

1

Weekly Sales

$24.4K-$84.6K/wk

Year 1 sales average about $24.4K a week and reach $84.6K by Year 5, which is the biggest lift to EBITDA and owner cash.

2

Beverage Mix

25%-26%

Beverages hold 25%-26% of sales, and drink ingredient cost drops from 3.0% to 2.2%, so a stronger pour mix adds margin without more seats.

3

Food Margin

10%-12%

Food is 55%-58% of sales, and food ingredient cost falls from 12.0% to 10.0%, which directly lifts gross profit and speeds break-even.

4

Labor Scheduling

$355K-$580K

Staffing grows from 9 FTE to 16 FTE, so tight peak-night scheduling protects EBITDA instead of paying for empty hours.

5

Occupancy Costs

$5.0K/mo

Rent and utilities sit at $5,000 a month, so this fixed cost matters most in slow months and on the path to Month 3 breakeven.

6

Game-Day Sales

$38-$45

Weekend AOV rises to $38-$45 and Saturday and Sunday covers reach 540 and 450 by Year 5, so game-day nights push ticket size and owner take-home.

Sports Bar Core Six Income Drivers

Weekly Sales Volume

Weekly Sales Volume

Weekly sales volume is the biggest income lever. At 710 covers and about $2,438k in Year 1 weekly revenue, then 2,030 covers and about $8,455k by Year 5, the owner earns more only if traffic is steady, not just event-driven. Weak Monday-through-Thursday sales still drag down pay, even when playoff nights are packed.

Weekly volume comes from covers, seat turns, average check, open days, and late-night traffic. Here’s the quick math: more recurring midweek demand spreads payroll and rent over more sales, so cash flow improves and more profit can reach owner distributions. What this estimate hides is simple: a busy night can still miss the goal if labor, comps, and waste rise too fast.

Track Midweek Demand

Track Monday-through-Thursday covers separately from game nights. If weekday checks stay low, the bar may look full but still miss the cash needed for payroll and rent. Set daily targets for covers and average check, then test reservations, late-night menus, and small promos that bring guests back.

Use seat turns to find dead time. Faster turns on slow nights raise revenue without adding much labor, while the wrong schedule can erase the gain. Forecast weekly sales from the calendar, not just big events, because steady revenue is what funds reserves and owner pay.

1

Alcohol Mix And Beverage Margin

Beverage Mix and Margin

Bar sales can raise owner income fast, but only the margin after ingredients and loss reaches cash. In this plan, beverage mix is 250% in Years 1-4 and 260% in Year 5, while beverage ingredient cost falls from 30% of sales to 22%. If waste, comps, or weak pricing rise, the extra drink volume won’t fully flow to take-home pay.

Track Pour Cost and Waste

Measure beverage sales, pour cost, shrinkage, comps, pricing, and licensing costs together, not one by one. Use the 30% to 22% ingredient-cost path as the benchmark, then test pricing and portion control weekly. A drink menu only helps owner pay when staff follow recipes, log spills and voids, and keep responsible service tight.

2

Food Margin And Menu Economics

Food Margin and Menu Economics

Food only adds to owner pay when a ticket covers ingredients, kitchen labor, spoilage, and ticket-time pressure. In the planning case, food ingredients run 120% of food sales in Year 1 and improve to 100% by Year 5, so food starts negative before overhead. If pizzas and mains scale to 550% of Year 1 sales and 580% by Year 5, the menu mix has to fix the math.

Watch the items that look popular but hide weak contribution: wings, burgers, and appetizers. Here’s the quick math: if ingredient cost stays at 120% of sales, every $1.00 of food revenue loses $0.20 before prep labor and waste. Menu pricing, portion control, and plate builds decide whether food helps fund payroll, rent, and owner draws, or just drives more kitchen work.

Track Food Contribution, Not Just Sales

Measure each menu item by ingredient cost, prep labor, waste, and ticket time. If a plate takes longer on game nights, it can hurt both throughput and owner income even when the item sells well. Price and portion against the full recipe cost, not the sticker food cost alone.

Track recipe cost per item

Log waste and comps weekly

Test portion sizes and plate builds

Watch ticket times on peak games

Raise prices when cost drifts up

What this estimate hides is the kitchen load behind busy nights. A strong seller only helps if it clears ingredient cost, labor, and waste fast enough to keep service moving. If the menu slows the line, you can lose more in missed covers than you gain in sales.

3

Labor Scheduling And Payroll Control

Payroll Control

Payroll is a cash-flow driver here because Year 1 staffing totals $355k a year, or about $29.6k a month. That includes a $70k General Manager, $60k Head Chef, plus 20 cooks, 30 servers, 10 bar staff, and 10 dishwashers. If labor runs ahead of sales, owner pay gets squeezed fast.

By Year 5, staffing rises to 160 FTE, so labor control matters more, not less. The risk is simple: understaffing hurts speed, and slow service can cut repeat visits, tabs, tips, and game-day revenue; overstaffing burns cash before the door opens.

Staff to Demand

Schedule to covers and game nights, not weekly averages. Track covers per labor hour, labor dollars by daypart, and sales by shift so you can flex cooks, servers, and bar staff before service breaks down. One clean rule: if the room fills, staffing must rise before wait times do.

Use a daily roster tied to brunch, dinner, late-night, and event traffic. The inputs are covers, open days, daypart mix, and role counts. The goal is enough labor to protect check size and repeat visits, while keeping payroll inside the cash the week actually brings in.

Track sales by shift.

Staff to demand peaks.

Watch wait times closely.

Protect fast table turns.

4

Rent And Occupancy Cost

Rent And Occupancy Cost

Rent and occupancy cost is the monthly price of the location: rent, utilities, and lease-linked space charges. Here’s the quick math: $5,000 per month for rent and utilities, with $7,200 in total fixed monthly costs. Against $1.056 million average monthly Year 1 revenue, that is about 0.5% for rent and 0.7% for all fixed costs.

This matters because a strong room can still pay the owner less if the lease is too rich. Bigger square footage, parking, patio space, visibility, and lease terms can raise sales, but they also raise break-even if rent grows faster than checks. What this estimate hides is traffic volatility: weak weekdays can drag profit even when game nights are packed.

Keep Lease Cost Tied To Sales

Track occupancy cost each month as rent, utilities, and fixed site costs divided by sales. Use the Year 1 benchmark of 0.7% for total fixed monthly costs as the control line. If that ratio climbs while covers and average check stay flat, the location is costing too much for the revenue it brings in.

When you negotiate or renew, price the space against seat count, visibility, parking, and patio use, not just the headline rent. A high-traffic corner helps only if it adds enough covers and check size to cover the lease. Test the lease against a slow month, so owner pay does not vanish in weak weeks.

5

Game-Day And Event Monetization

Game-Day Covers and Checks

On event nights, income comes from more covers and higher checks. In Year 1, weekend covers are 450 versus 260 midweek, and AOV is $38 versus $28. That puts weekend sales at about $17,100 per night versus $7,280 midweek, so the gap is real. But one strong game day only helps owner pay if the rest of the week stays busy too.

What this driver includes is reservations, group packages, cover charges, private watch parties, and promotions. It also includes the costs that show up with the crowd: extra servers, kitchen coverage, security, licensing, discounts, and food waste. If those costs rise faster than sales, the owner’s take-home drops even when the bar looks packed.

Protect Event Margin

Track each event night by covers, AOV, labor hours, security cost, comps, and waste. A full house is not enough if the extra staff and giveaway discounts eat the gain. Here’s the quick math: 450 × $38 = $17,100 on a strong weekend night, but that only matters after direct event costs are covered.

Measure weekend vs midweek covers

Price groups and watch parties tightly

Cap discounts on low-margin nights

Staff to demand, not averages

Use promotions to fill seats, not to buy unprofitable traffic. If a game night needs heavy overtime, deep comps, or extra waste, raise the cover, trim the offer, or cut the event type. The goal is simple: turn event traffic into contribution dollars that can pay payroll, rent, and the owner’s draw.

6

Sports Bar Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner income cases

Owner income scenarios

Owner income moves with weekly covers, check size, and food-and-beverage mix. The same bar can swing a lot from a slow opening year to a fuller, higher-volume run.

Low, base, and high cases show how traffic changes owner cash.

Scenario

Low CaseDownside case

Base CaseCore case

High CaseUpside case

Launch model

Owner cash stays in a lower opening-year pattern while the bar builds traffic.

Owner cash follows the modeled middle path as the bar gets more regular traffic.

Owner cash reaches a stronger run rate as volume and check size keep climbing.

Typical setup

Year 1 is about $1.268M revenue with $413k EBITDA and 710 weekly covers, while breakeven lands in Month 3.

Year 3 is about $2.748M revenue with $1.524M EBITDA and 1,370 weekly covers.

Year 5 is about $4.397M revenue with $2.731M EBITDA and 2,030 weekly covers.

Cost drivers

Weekly covers

$28 midweek checks

$38 weekend checks

labor build

fixed rent and utilities

Weekly covers

stronger weekend mix

higher check size

staffing scale

ingredient and fee load

Weekly covers

higher weekend volume

menu mix

labor intensity

reinvestment needs

Owner income rangeBefore owner reserves

$413kYear 1 cash

$1.524MYear 3 cash

$2.731MYear 5 cash

Best fit

Use this to stress-test a slower launch and tighter early traffic.

Use this as the main planning case for budgeting and staffing.

Use this to test upside if the bar sustains high traffic and strong spend.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Keep reserves separate from owner draw because sports bars have payroll, rent, inventory, and event-driven swings This model shows $818k minimum cash in Month 2, $171k in listed buildout and setup costs, and $7,200 in fixed monthly costs Treat reserves as working capital first, not extra owner income

In this researched planning case, breakeven occurs in Month 3 and payback takes 8 months That result depends on hitting about $1056k average monthly revenue in Year 1 and controlling $355k annual payroll If launch sales miss plan or hiring runs ahead of traffic, breakeven can move out quickly

You don’t have to model owner pay as a fixed salary, but you should plan it before opening The cleaner approach is to start with EBITDA, then subtract debt service, taxes, reserves, and reinvestment before any draw Year 1 EBITDA is $413k here, but that is not guaranteed take-home pay

Weekly sales volume, beverage mix, payroll, and rent move cash flow the most Year 1 has about $2438k in weekly revenue, a 250% beverage mix, $355k payroll, and $5,000 monthly rent and utilities A small margin miss matters because 1 percentage point of Year 1 sales is about $127k

Grow repeat traffic before adding fixed cost In this model, revenue rises from $1268M in Year 1 to $4397M in Year 5 as weekly covers increase from 710 to 2,030 The best path is higher recurring covers, controlled staffing, stable food cost, and profitable game-day packages, not just more one-off promotions

About the author

Ryan Spencer

First-Time Founder Guide Writer

Ryan Spencer writes for Financial Models Lab, where he focuses on launch budget planning and simple launch planning for first-time founders. He helps readers estimate startup needs before opening a physical location, breaking down business costs in clear, practical language. His work is built for people who want a realistic view of what it really takes to open a business, so they can plan with more confidence and fewer surprises.

Choosing a selection results in a full page refresh.