How Much Does A Summit Platform Owner Make? $867K To $132M EBITDA

Key Takeaways

Paid organizers, not signups, drive recurring revenue.

Higher-tier mix lifts ARPA from $249 toward $470.

Usage revenue only works after event costs are covered.

Retention lowers CAC payback and protects monthly revenue.

Owner incomeEBITDA $867K–$13.2MNet margin38%–69%Revenue for target pay$19.0MBusiness difficultyMedium

Want to test your summit platform owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Summit Event Platform model?

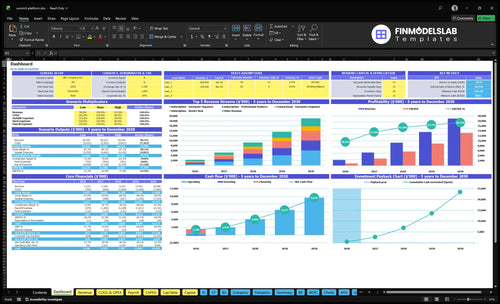

This dashboard in the Summit Event Platform Financial Model Template shows revenue, EBITDA, breakeven, payback, minimum cash, and owner take-home; charts also show $227M to $190M revenue, $867K to $132M EBITDA, 4-month breakeven, 7-month payback, and $809K cash need. Open the model.

Owner-income model highlights

Owner income at top

Revenue and EBITDA charts

Pricing, CAC, cost inputs

Can a virtual summit platform scale profitably?

Summit Event Platform can scale profitably, but more scale does not always mean more cash for the owner. In the model, revenue moves from $227M to $190M while EBITDA (earnings before interest, taxes, depreciation, and amortization) margin rises as cloud, payment, referral, and training costs fall. Still, payroll expands in core engineering, sales, customer success, and marketing, so owner-led growth can boost short-term take-home but also raise burnout and support risk.

Profit side

$227M to $190M revenue

Cloud, payment, referral, training % fall

EBITDA margin improves at scale

Scale can still be profitable

Owner tradeoff

Payroll grows with more customers

Engineering, sales, support, marketing expand

Owner-led growth raises short-term cash

Team-led growth protects retention and quality

How much revenue does a summit platform need to pay the owner?

If you’re asking how much revenue Summit Event Platform needs to pay the owner, the real answer is: enough to cover fixed overhead, marketing, support, reserves, and product work before any owner draw. In the model, $227M in Year 1 revenue supports $867K EBITDA before owner distributions, and Year 5 shows $190M revenue with $132M EBITDA. With $11K/month fixed overhead and marketing rising from $150K to $700K, owner pay only works after the business is fully funded.

Revenue comes first

$227M Year 1 revenue

$867K EBITDA before owner draws

$190M Year 5 revenue

$132M EBITDA in Year 5

Pay comes after funding

$11K/month fixed overhead

Marketing grows from $150K to $700K

Fund support coverage first

Keep cash runway in place

How much profit can a summit platform owner make?

A Summit Event Platform owner can show $867K EBITDA in Year 1, scaling to $13.193M by Year 5 in the researched model, but EBITDA is not the same as owner cash; see What Are The 5 Core KPIs For Summit Event Platform? for the KPI drivers behind that forecast. Early cash stays tight because minimum cash need reaches $809K in Month 2, so distributions should wait until payroll, churn, support, taxes, debt, and reinvestment are covered.

Modeled EBITDA

Year 1: $867K EBITDA

Year 2: $2.828M EBITDA

Year 3: $5.701M EBITDA

Year 5: $13.193M EBITDA

Owner Cash

Protect $809K Month 2 cash need

Separate EBITDA from distributions

Fund payroll and support load first

Set payouts after taxes and reinvestment

Summit Event Platform Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers at a glance?

1

Paid Organizers

$2.3M-$19.0M

More paid organizers drive the jump from year 1 revenue to year 5 revenue, and that is the cleanest path to higher take-home.

2

Pricing Mix

$99-$1,199

A richer mix of Starter, Professional, and Enterprise plans lifts ARPA, so the same customer base pays more each month.

3

Add-on Usage

$15-$150

Each active host adds subscription, one-time, and usage fees, so more event activity raises revenue without a matching jump in headcount.

4

Retention

8%-12%

Higher trial-to-paid conversion keeps more customers in the paid base, so churn hurts less and CAC payback improves.

5

Infrastructure Margin

87%-90%

Keeping cloud, video, API, and support costs lean leaves more of each dollar for EBITDA.

6

CAC and Payroll

$150->$125

Lower CAC and tighter hiring let marketing scale from $150K to $700K without letting labor costs eat the margin.

Summit Event Platform Core Six Income Drivers

Paid Organizer Count

Paid Organizer Count

Paid organizer count is the number of hosts who leave trial and pay each month. It drives monthly recurring revenue (MRR): paid organizers × monthly price. Vanity signups do not pay the owner model. In this case, free-trial starts rise from 120% to 180%, trial-to-paid conversion rises from 80% to 120%, and CAC improves from $150 to $125.

The real value depends on whether organizers renew, run more than one summit, and cost less to support than their gross profit contribution. If onboarding takes too long, support tickets climb, or churn stays high, paid count looks good on paper but owner cash gets squeezed. One clean test: paid customers should create recurring profit, not one-off demos.

Track renewals, not signups

Measure paid organizers, renewal rate, repeat-event count, and support tickets per account. If a host runs a second summit, the same CAC is spread over more revenue, and the account becomes more profitable. If they never return, the trial was just a marketing cost.

Forecast owner pay by comparing gross profit per organizer against onboarding and live-support time. Keep acquisition near $125 CAC, and watch for discounts or heavy hand-holding that eat the margin. That’s the point where MRR grows, but take-home income does not.

1

ARPA And Pricing Mix

ARPA and Pricing Mix

ARPA is the average monthly subscription revenue per paid account. It rises when more customers land in the higher tiers, so the same account base can produce more cash for payroll, support, and owner pay. With $249 weighted monthly ARPA in Year 1, 100 accounts imply about $24,900 MRR; at $470 in Year 5, that becomes about $47,000 MRR.

The mix shift matters because tier prices move from $99, $299, and $999 to $119, $349, and $1,199, while sales mix moves from 60% Starter Host and 10% Enterprise Organizer to 40% and 25%. But list price is not take-home revenue; discounts, churn, payment fees, and support burden cut realized income.

Track Net ARPA by Tier

Measure net ARPA by tier: list price minus discounts, churn, payment fees, and support time. Split it by Starter Host, Professional Producer, and Enterprise Organizer so you can see which accounts actually pay for themselves. If enterprise deals need heavy live support, the headline price can look strong while owner draw falls.

Track realized ARPA each month.

Compare support hours per account.

Watch renewals and tier upgrades.

Test price lifts on new sales.

A clean rule: if higher-tier mix lifts ARPA but also raises onboarding and event support, profit may stall. Keep cohort reporting by start month so you can see which accounts renew, expand, and stay above their gross profit contribution.

2

Usage And Add-On Revenue

Usage-Based Add-On Revenue

Usage revenue helps only when the fee on each summit event is bigger than the extra cloud, bandwidth, and live-support cost it creates. The model here uses 1 transaction at $15 for Starter Host, 2 at $45 for Professional Producer, and 5 at $150 for Enterprise Organizer, plus one-time fees of $0, $499, and $2,500.

That means owner income rises when premium recordings, sponsor tools, registration features, and analytics are priced to the right event load. One clean rule: if the add-on fee does not cover the extra hosting and support, it adds revenue but can still hurt profit and cash flow.

Match Price to Event Load

Track add-on revenue by event type, not as one lump number. Separate each premium feature from the support time, bandwidth, and cloud use it drives, so you can see whether the $15, $45, and $150 fee levels are actually profitable.

Log cost per summit session.

Tag support hours to each add-on.

Test one-time fee take-up rate.

Drop features that miss margin.

Keep the forecast tied to live-event load. If a larger summit needs more moderation, encoding, or help desk time, the fee must rise with it; otherwise usage revenue looks good on paper but cuts into owner pay after event costs hit.

3

Retention And Churn

Retention And Churn

Retention matters because many organizers may buy for one event and leave. When a customer runs multiple summits, renews annually, or adds attendees, the same CAC gets spread over more revenue, so owner income rises through more MRR and better cash flow. If churn is high, revenue resets each month and profit gets thin fast.

The main leak is bad live-event support. Watch trial-to-paid conversion, paid organizer count, annual renewal behavior, expansion usage, and support quality during live events. One clean rule: if organizers do not come back, acquisition spend never pays off twice.

Track Repeat Events First

Measure cohorts by first event date, then split them by renewed, upgraded, and churned. Add a simple event count per account report, because an organizer who runs 2 summits is far more valuable than a one-and-done buyer. If live support is slow, fix onboarding and staffing before spending more on ads.

Track paid organizers monthly.

Flag first-event-only customers fast.

Review support tickets during live days.

4

Gross Margin After Event Costs

Gross Margin After Event Costs

This driver is the cash left after cloud, video, API, payment, support, refund, and travel costs. It sets the pool for payroll, marketing, product work, reserves, and owner pay. The disclosed model shows Year 1 COGS of 85% cloud/video infrastructure plus 45% API and payment fees, leaving 870% gross margin.

Here’s the quick math: gross margin rises only if usage revenue grows faster than event load. Large summits can look profitable until bandwidth spikes, live support, refunds, and API costs are matched to revenue. The disclosed model shows Year 5 COGS at 65% and 35%, leaving 900% gross margin.

Track margin per event, not just bookings

Track ticket revenue, add-on revenue, and every event cost before owner draw. Separate cloud, video, API, payment fees, refunds, affiliate commissions, and customer success travel so you can see the real margin left after each summit.

Measure margin per summit

Match costs to attendee volume

Watch refund and support spikes

Price usage to cover live load

If margin drops as attendance rises, the platform is selling volume, not profit. If live support or bandwidth costs outrun usage revenue, keep the owner’s pay tied to contribution dollars, not top-line sales.

5

Payroll And Sales Efficiency

Payroll and Sales Efficiency

Payroll sets how much cash is left for founder pay after the team is staffed. A base team around a $145K CTO, $120K senior engineer, $85K sales/account manager, $65K customer success specialist, and $90K marketing manager totals $505K before benefits if staffed one deep. Every hire cuts near-term distributions. The tradeoff matters because the platform needs enough engineering and support to keep churn low and enterprise buyers confident.

Sales efficiency improves when CAC falls from $150 to $125, but the marketing budget also rises from $150K to $700K. So the owner has to watch cash burn, not just CAC. If payroll gets too lean, launches slow, support slips, and renewal risk goes up, which can erase the extra cash the founder hoped to take home.

Track payroll against paid growth

Track payroll as a share of gross profit, plus CAC, churn, and support tickets. If CAC is falling but the marketing budget is climbing, ask whether the extra spend is producing paid organizers, renewals, and add-on revenue. Here’s the quick check: if a hire does not lower churn, speed launches, or raise conversion, it is probably reducing owner pay more than it helps it.

Protect the core team first: engineering for uptime and launches, customer success for event-day support, and sales for renewal and expansion. The risk is simple: under-hiring can look good on monthly distributions, but one bad summit or delayed release can weaken retention and make the next dollar of sales much more expensive.

6

Summit Event Platform Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Scenario objective: Compare low, base, and high summit platform owner income cases using the researched model

Owner income

Revenue, conversion, and CAC drive owner take-home here, while hiring, cloud, and marketing spend pull cash back out. These cases show how much can reach the owner after reinvestment.

Owner income by operating case.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

This case assumes slower traction and a tight owner draw while the business absorbs launch costs.

This case assumes a modeled owner draw as the funnel, team, and pricing move in line with plan.

This case assumes a stronger owner payout path as enterprise mix and conversion both run ahead of plan.

Typical setup

Year 1 runs at $2.27M revenue and $867K EBITDA, with $150K marketing, $150 CAC, and early cash strain from a small team and launch spend.

Year 3 reaches $9.25M revenue and $5.70M EBITDA, with $400K marketing, $135 CAC, and a larger support team behind the sales mix.

Year 5 reaches $19.00M revenue and $13.19M EBITDA, with $700K marketing, $125 CAC, and a heavier enterprise mix.

Cost drivers

Marketing spend

CAC

trial conversion

early cash burn

reserve buildup

Marketing scale

CAC decline

enterprise mix

team growth

reinvestment

Enterprise mix

CAC decline

pricing lift

scale marketing

higher reserves

Owner income rangeBefore owner reserves

Tight founder drawLow Case

Moderate founder drawBase Case

Strong founder drawHigh Case

Best fit

Use this to test the owner payout if launch demand is weaker than planned and cash stays tight.

Use this as the most likely path for planning owner income, reserves, and reinvestment.

Use this to test upside if larger accounts close faster and the business can fund growth without squeezing owner take-home.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets.

The model shows EBITDA from $867K in Year 1 to $132M in Year 5, but that is not guaranteed owner pay Actual take-home comes after taxes, debt service, capex, cash reserves, and reinvestment The business also needs up to $809K in minimum cash in Month 2

The researched model reaches breakeven in 4 months and payback in 7 months That assumes the pricing, conversion, CAC, payroll, and cost structure hold If onboarding takes longer, churn rises, or live-event support costs spike, breakeven can move later even when revenue looks strong

You do not need only enterprise customers, but the mix matters The model shifts from 10% Enterprise Organizer in Year 1 to 25% in Year 5 Enterprise pricing is $999 to $1,199 per month, plus a $2,500 one-time fee and higher transaction usage, so support discipline is critical

Owner pay is most affected by paid organizer count, ARPA, churn, hosting costs, support load, and payroll Year 1 cloud and video costs are 85% of revenue, payment and API fees are 45%, and fixed overhead is $11K per month before payroll and marketing

The strongest model combines subscriptions, setup fees, and usage-based revenue In the assumptions, monthly plans run from $99 to $1,199, one-time fees run from $0 to $2,500, and transaction fees range from $15 to $150 Just match every usage fee to its cloud, bandwidth, and support cost

About the author

Jack Bennett

Business Model Writer

Jack Bennett is a business model writer at Financial Models Lab, where he explains startup planning and business model economics in clear, practical language. He focuses on the money questions new founders ask when comparing business ideas, with an eye on how small businesses operate day to day. Jack’s writing helps readers understand the numbers behind real business operations without heavy finance jargon, making complex decisions feel more manageable and grounded.

Choosing a selection results in a full page refresh.