How Much Swim School Owners Make: $3625M Year 1 EBITDA Case

Swim School Bundle

A swim school owner’s income depends on what cash remains after instructor payroll, pool costs, marketing, insurance, admin, reserves, and reinvestment In the supplied model, EBITDA is $3625M in Year 1, with 40% occupancy, 25 billable days per month, and a $883k minimum cash need Owner take-home should be planned below EBITDA because taxes, debt service, reserves, and growth spending are not the same as profit distributions If the owner also works as general manager or lead instructor, that labor pay should be separated from business profit

Owner income$3.6MNet margin31%Revenue for target pay$11.7MBusiness difficultyHard

Want to test your own swim school income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Taxes and debt are excluded unless you enter them.

Want to check owner income in the Swim School model?

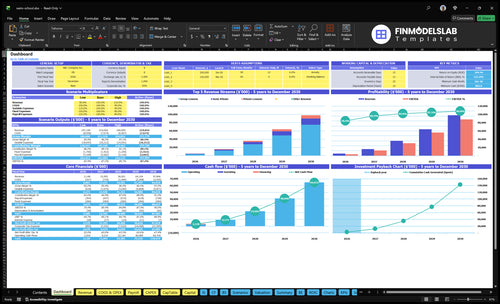

The screenshot shows revenue, EBITDA, break-even, cash, and owner-income scenarios. Open the Swim School Financial Model Template to see the math behind it.

Owner-income model highlights

Owner take-home scenarios

EBITDA ramps fast

Cash floor: $883k

Occupancy rises 40%-85%

Plan, don’t promise

How many students does a swim school need to make money?

At Swim School, the Year 1 mix points to about 260 filled spots at 40% occupancy across 500 group places, 100 semi-private, and 50 private places; at a weighted monthly price of about $150, that is roughly $39,000 in monthly revenue before billable-day mechanics. With $49,950 in monthly fixed payroll plus overhead and 78% contribution after listed COGS and variable costs, break-even is closer to 427 filled spots, or about 66% of capacity, before owner pay.

What drives break-even

Class fill rate changes revenue fast

$150 is the pricing basis here

78% contribution supports the math

427 spots cover fixed costs only

Why Month 1 can miss

Pool schedule limits billable days

Occupancy may start near 40%

$23,700 fixed overhead is already baked in

$26,250 payroll adds the pressure

What affects swim school profit margin most?

Swim School profit margin is driven most by instructor payroll and class fill rate. Fixed costs like the $15k lease, $3k pool maintenance, $12k insurance, and $1k fixed utilities keep pressure on profit, so underfilled classes hurt fast. If you’re sizing the model, How Much Does It Cost To Open A Swim School? is the right cost check because Year 1 payroll alone is $315k.

Top margin drivers

Payroll is the biggest lever.

Fill rate changes revenue per class.

Underfilled classes crush margin.

Safety coverage can’t be cut too far.

Cost pressure points

Year 1 payroll is $315k.

Variable costs fall from 17% to 9%.

Fixed costs stay in the base.

Labor cuts must keep quality and compliance.

Is owning a swim school profitable, and how do you scale income?

Yes, a Swim School can be profitable when enrollment, retention, class fill, and pricing grow faster than payroll and pool costs. The owner-operated model can save a manager or instructor salary, but it caps owner time; a manager-led model adds $75k in salary cost and frees the owner for sales, partnerships, and expansion. The scale math is simple: moving occupancy from 40% to 85% and instructor FTE from 3 to 7 can lift income, but it is not passive income.

Profit drivers

Enrollment drives monthly revenue.

Retention cuts refill costs.

Class fill lifts yield.

Pricing must outrun costs.

Scaling tradeoffs

Owner-operated saves salary.

Manager-led adds $75k cost.

Dedicated facilities raise fixed costs.

Multi-site growth adds risk.

Occupancy growth matters most, because more filled spots spread pool and labor costs across more students.

What improves margin

Push occupancy from 40% to 85%.

Raise instructor FTE from 3 to 7.

Use owner time for sales.

Track safety and scheduling tightly.

Cash risks

Dedicated sites need more cash.

Hiring takes time and money.

Safety errors can be costly.

Working capital gets tighter fast.

Swim School Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers that move swim school income most?

1

Enrollment Retention

40%-85%

Occupancy rises from 40% in Year 1 to 85% by Year 5, and that is the biggest swing in revenue per class.

2

Class Fill

25-28/mo

More billable days per month lift sales without much extra fixed cost, so empty lanes hit income fast.

3

Pricing Mix

$120-$410

Private lessons at $350-$410 bring far more revenue per seat than group lessons at $120-$140, so mix drives margin.

4

Payroll Efficiency

$315K-$560K

Annual wage load rises as swim instructor staff grows, so staffing control decides how much revenue stays in the business.

5

Facility Costs

$23.7K/mo

Fixed costs of $23,700 a month set the breakeven floor, so every underfilled class cuts into take-home.

6

Cash Reserve

$883K

Minimum cash starts at $883K in Month 1, so reserve discipline matters until occupancy and revenue catch up.

Swim School Core Six Income Drivers

Active Enrollment And Student Retention

Student Retention

Retention keeps weekly class revenue steady. In Year 1, the model starts with 650 total spots: 500 group, 100 semi-private, and 50 private. At 40% occupancy, that is about 260 filled spots. By Year 5, capacity rises to 1,690 spots and occupancy reaches 85%, or about 1,437 filled spots, so lost students matter a lot.

When students leave, revenue drops fast but lease and payroll stay due. That hurts cash flow and makes owner distributions less safe. Active enrollment covers renewals, make-up usage, trial-to-paid conversion, and cancellation reasons. If churn rises faster than new sign-ups, the school can look busy and still feel tight on cash.

Track Churn Early

Watch renewal rate, make-up usage, trial conversion, and cancellation reasons each week. These are the fastest signals that tell you whether the current class mix is holding or whether you need more marketing just to replace lost students.

Use those numbers to fix the leak before you add spend. Better retention keeps billing smoother, protects margin, and gives the owner a cleaner path to pay themselves without leaning on new enrollments every month.

Review renewals by cohort.

Check cancellations every week.

Measure trial-to-paid conversion.

Track missed make-up lessons.

1

Class Fill Rate And Pool Lane Utilization

Class Fill Rate

Owner income rises when paid students fill existing lanes before you add more pool time or instructor hours. In this model, occupancy moves from 40% in Year 1 to 55%, 70%, 80%, and 85%, while billable days increase from 25 to 28 per month. Same fixed cost, more paying swimmers, better margin, more cash for owner pay.

This driver depends on available class spots, enrolled students, lane blocks, and the monthly schedule. Underfilled classes still carry the same lease and payroll cost, so weak fill can drag profit fast. The limit is safety: improve utilization without unsafe class ratios or overcrowding.

Tighten Schedule Blocks

Build the schedule around age and skill level, then measure fill by class block, not just by month. If a class sits under target, move the block before adding another lane or extra instructor hours. A shift from 40% toward 55% occupancy can lift take-home income without new fixed cost.

Track fill rate by block.

Watch billable days monthly.

Flag empty lane slots.

Count make-up lesson load.

Check students per instructor.

Use those numbers to decide whether to open more capacity or keep tightening the current schedule. One clean rule: fill the lanes you already have before you buy more of them.

2

Pricing And Program Mix

Program Mix Raises Revenue Per Student

When the schedule shifts from more group lessons to more semi-private and private work, average revenue per student rises. In the model, pricing runs from $120 to $140 for group lessons, $200 to $240 for semi-private, and $350 to $410 for private lessons. That can lift owner pay only if instructor hours and lane time do not grow as fast.

Revenue per student is not the same as profit. A private lesson can bring more cash per booking, but it may also use more instructor capacity, so the margin depends on labor, pool time, and fill rate. Merchandise sales also matter, rising from $1,500 to $5,500 in the assumptions, but they stay small unless they sell at a healthy mark-up.

Track Mix, Not Just Headcount

Measure revenue by program type each month: group, semi-private, private, clinics, camps, and registration fees. The key check is simple: does the higher-priced mix raise revenue faster than payroll and lane use? If not, the extra sales may not reach owner draw.

Test schedule blocks by age and skill, and watch capacity by instructor hour. A better mix usually means more high-value bookings without crowding classes. Private lessons can help, but only if they do not push overtime, extra staffing, or wasted pool time.

3

Instructor Payroll And Staffing Efficiency

Instructor Payroll And Staffing Efficiency

When a swim school carries $315k of Year 1 payroll — $75k general manager, $60k head instructor, 3 swim instructors at $40k each, $35k admin, and $25k lifeguard — staffing becomes one of the biggest profit levers after facility costs. Empty classes still cost money.

By Year 5, instructor FTE rises from 3 to 7 and lifeguard FTE from 1 to 3, so pay has to grow with filled class time. If cancellations, training, substitutes, or low class fill leave paid hours idle, labor margin drops and owner draw gets thinner.

Staff to Filled Blocks First

Start with booked class blocks, then assign instructors around them. Track filled-block hours, paid hours, cancellations, substitute hours, and training time each week. That shows whether labor is supporting billable lessons or just sitting on the schedule. Keep the math simple: more paid hours should bring more taught classes, not more slack.

Track pay per billed lesson

Log cancellation and make-up rates

Separate training and substitute hours

Compare staffing to class fill

Use the data to cut dead time and stack lessons in the busiest windows. Safety, training, and compliance still set the floor, so do not understaff. But if low class fill is common, every extra paid hour without a swimmer lowers profit and delays owner distributions.

4

Pool Access, Rent, And Facility Costs

Facility Fixed Cost Load

When you rent or own pool space, the main income swing comes from fixed cost load. Here the monthly facility stack is $57,000: $15,000 lease, $25,000 property taxes, $3,000 pool maintenance, $12,000 insurance, $1,000 utilities, plus software, office supplies, and certifications. That cost hits before payroll, so owner pay stays shaky until enrollment and lane use are high enough.

Renting lanes can lower early risk because you avoid a full facility burden, but a dedicated site adds capacity and more control. The catch is simple: more space only helps if it fills. If you build out a site, the $375,000 pool, HVAC, and filtration spend also ties up cash, so distributions should wait until utilization is consistently strong.

Track Fixed Cost Coverage

Measure this driver as monthly facility cost ÷ monthly billable revenue and watch it by lane type and schedule block. If utilization is thin, the same lease and insurance stay due while revenue drops, so owner income swings hard. One clean rule: do not raise owner draws until the pool’s paid occupancy can cover the full fixed load, not just the class payroll.

Use the inputs that actually move this number: lease terms, property taxes, insurance renewals, maintenance contracts, utility bills, and billable lane hours. Also track whether rented lanes or a dedicated site gives better margin after all fixed costs. A simple test helps: if a new schedule block does not lift revenue faster than fixed cost growth, it is not safe to scale yet.

$57,000 monthly facility fixed costs

$375,000 build-out capex

Track paid lane utilization weekly

Delay draws until coverage is steady

5

Seasonality, Cancellations, And Cash Reserves

Seasonality, Cancellations, and Cash Reserves

This driver is the gap between planned lessons and cash collected in a month. At 25 to 28 billable days, a holiday week, storm, or canceled class can cut billings fast while payroll, lease, insurance, and maintenance still land. Monthly cash can look tight even if the year is strong.

The model’s $883k minimum cash need is the floor to watch. Inputs are billed days, missed lessons, make-up lessons, enrollment pace, and fixed costs. Simple rule: do not take owner distributions before the reserve target is met.

Set a Reserve Floor Before Owner Pay

Track cancellations by reason, make-up usage, and enrollment lag every month. If missed lessons rise, cash comes in later or not at all, but the cost base does not reset. Here’s the quick math: fewer billings plus fixed costs equals weaker owner pay.

Set reserve rules in writing: hold cash above the $883k floor, then pay owners. That keeps draw decisions cleaner during weather breaks and slower sign-up periods, and it lowers the chance of a cash crunch right after a busy month.

Track canceled lessons by reason

Monitor make-up lesson volume

Watch billable days each month

Hold cash above the reserve floor

6

Swim School Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high swim school owner-income cases

Owner income scenarios

Occupancy, billable days, and lesson pricing move owner income fast in this swim school. Fixed lease and payroll keep the downside meaningful until utilization rises.

From early ramp to mature utilization.

Scenario

Low CaseLow case

Base CaseBase case

High CaseHigh case

Launch model

This is the lower earnings path, built on the first-year ramp.

This is the modeled core case, built on scaled utilization.

This is the stronger earnings path, built on mature capacity.

Typical setup

It assumes Year 1 at 40.0% occupancy, 25 billable days, and lower lesson pricing, so fixed lease and payroll take a bigger share of cash.

It assumes Year 3 at 70.0% occupancy, 27 billable days, and mid-range pricing, with EBITDA rising as classes fill.

It assumes Year 5 at 85.0% occupancy, 28 billable days, and top-end pricing, with the schedule close to full use.

Cost drivers

40.0% occupancy

25 billable days

$120 group lessons

$200 semi-private

$350 private

70.0% occupancy

27 billable days

$130 group lessons

$220 semi-private

$380 private

85.0% occupancy

28 billable days

$140 group lessons

$240 semi-private

$410 private

Owner income rangeBefore owner reserves

$3.6M EBITDALow case

$30.5M EBITDABase case

$88.0M EBITDAHigh case

Best fit

Use this to stress-test the first operating year and cash pressure.

Use this as the main operating plan once enrollment and schedule fill in.

Use this to test upside from fuller classes and stronger pricing power.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

The supplied model shows $3625M in Year 1 EBITDA, but owner income should be lower after taxes, debt service, reserves, and reinvestment If the owner also works in the business, compare that labor to the $75k general manager salary or $60k head instructor salary Do not treat EBITDA as automatic take-home pay

This model shows break-even in Month 1 with a $883k minimum cash need That fast break-even depends on the supplied occupancy, pricing, payroll, and facility assumptions holding together In practice, slower enrollment, underfilled classes, or delayed opening costs can push owner distributions back even if accounting profit appears early

No, but teaching changes the economics If the owner teaches, they may replace some head instructor or swim instructor labor, which is modeled at $60k and $40k per FTE If the owner manages instead, compare their work to the $75k general manager role Keep owner labor pay separate from profit distributions

Occupancy, staffing, and facility costs move profit fastest The model ramps occupancy from 40% to 85%, while instructor FTE rises from 3 to 7 Fixed monthly costs include a $15k facility lease, $3k pool maintenance, and $12k insurance Underfilled classes hurt because those costs do not fall quickly

Fill existing class slots before adding fixed cost Start with retention, schedule density, and mix: group lessons at $120 to $140, semi-private at $200 to $240, and private lessons at $350 to $410 across the model period Then set a reserve rule so strong months do not create unsafe owner distributions

About the author

Simon Reed

Small Business Educator

Simon Reed is a small business educator at Financial Models Lab who helps service business founders understand the numbers behind everyday business ideas. He focuses on pricing and margin basics, common business costs, and the first months after launch, giving readers a clearer view of what it takes to build a healthy business. Simon brings a simple, confident approach that balances optimism with cost-aware planning.

Choosing a selection results in a full page refresh.