How Much Does a Taco Truck Owner Make? $476K EBITDA Case

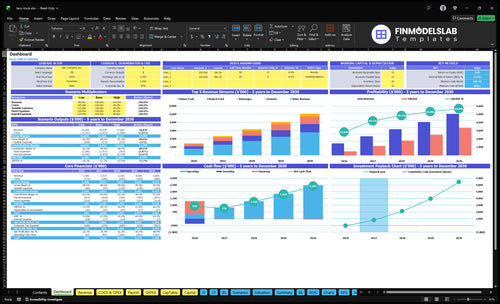

You’re trying to turn taco sales into owner take-home, not confuse busy days with real profit This five-year planning view uses researched assumptions for covers, average order value, food cost, payroll, fixed costs, EBITDA, cash need, break-even timing, and payback, with $476K Year 1 EBITDA before personal taxes, debt service, reserves, and owner distributions

Owner income$476K to $3.34MNet margin29% to 58%Revenue for target pay$658K/moBusiness difficultyHard

Want to test your taco truck take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target owner pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. The source model shows a $684k minimum cash need, Month 3 break-even, a 13-month payback, and EBITDA from $476k in Year 1 to $3.338m in Year 5.

How do you check owner income in the Taco Truck financial model?

The dashboard shows revenue assumptions, covers/day, AOV, sales mix, costs, cash flow, EBITDA, break-even, payback, and owner take-home. Open the Taco Truck Financial Model Template.

Owner-income model highlights

Owner take-home scenarios

Revenue and margin drivers

EBITDA chart from $476K to $3,338M

How much revenue does a taco truck need to make money?

A Taco Truck needs about $658K per month in revenue to break even under the Year 1 model. That assumes $1.785M in monthly fixed costs, about $371K in payroll, and a cost mix of 12% COGS plus 45% variable expenses. At an $80 weighted AOV, that is about 821 monthly covers, or 27 covers per day, before debt, reserves, and owner pay.

Break-even math

$658K/month hits break-even

$80 AOV drives the math

821 covers needed monthly

27 covers/day before extras

Cost pressure

$1.785M fixed cost load

$371K monthly payroll

12% COGS hits margin

45% variable expenses stay high

What taco truck profit margin should an owner expect?

A Taco Truck owner should expect a margin that follows the model, not a generic restaurant average, and the startup-cost guide at How Much Does It Cost To Open And Launch Your Taco Truck Business? shows why the cash math matters. In this model, Year 1 EBITDA (earnings before interest, taxes, depreciation, and amortization) is about 289% from about $476K EBITDA on about $165M revenue, and Year 5 reaches about 634% from about $3.338M EBITDA on about $527M revenue. The risk is cost sensitivity: food ingredients, beverage ingredients, marketing, and card fees all move with sales, and payroll plus fixed costs get tight if covers miss plan.

More daily covers from the right stop, route, or event schedule lifts sales fast because each extra order adds gross profit with little extra fixed cost.

2

Menu Pricing

$65-$110

Higher average order value on weekends and with add-ons raises revenue per stop, so small price moves have a big effect on owner take-home.

3

Open Capacity

395-1,015/wk

More service days and longer selling windows push weekly covers higher, but only if the line stays fast enough to keep throughput up.

4

Food Cost

12%

Keeping food and beverage COGS near the Year 1 12% level protects margin, and waste or over-portioning cuts straight into take-home.

5

Owner Labor

$445K

Year 1 payroll totals about $445K, so tight scheduling and hands-on owner work matter if you want operating profit to stay strong.

6

Fixed Overhead

$18K/mo

About $18K a month of fixed costs means weak sales months hit cash hard, so reserves and lean overhead protect the owner's draw.

Taco Truck Core Six Income Drivers

Customer Volume and Location Demand

Daily Covers and Location Demand

Daily covers drive the whole income model, because every extra customer adds revenue without a matching jump in fixed costs. In Year 1, the plan ranges from 30 covers on Monday to 90 on Sunday; by Year 5, it rises to 90 to 230. At a modeled $80 AOV, each missing 10-cover day cuts about $800 of revenue before food, labor, and fuel.

Location is the real constraint. Lunch routes, dinner spots, nightlife, festivals, and private events can lift covers, but permitting, queue speed, prep capacity, and parking limits cap output. If the truck can’t serve fast enough, demand turns into lost cash, not just slower service. One line: more foot traffic only helps when the truck can actually process it.

Track Covers by Stop and Daypart

Measure covers per hour, not just total sales, and split them by lunch, dinner, weekend, festival, and private event. Compare each stop to the modeled range: 30 to 90 covers in Year 1 and 90 to 230 in Year 5. Then cut weak stops, extend strong ones, and size prep and staffing to the busiest window.

Track covers by location.

Watch queue time and parking.

Test high-demand routes first.

Match prep to peak covers.

What this estimate hides: if service slows, some demand disappears before it hits the register. So the best forecast ties covers to real capacity, not just the size of the crowd.

1

Average Order Value and Menu Pricing

Average Order Value and Menu Pricing

Menu pricing moves revenue without adding the same fixed cost. In Year 1, $65 midweek and $90 on weekends works out to a weighted about $80 AOV across the week, so each extra 10 covers adds about $800 before food, labor, and fuel. By Year 5, the plan lifts AOV to $85 and $110, but only if value stays clear and covers do not fall.

This driver depends on covers, menu mix, and add-on attach rates: combos, beverages, desserts, premium proteins, sides, and catering trays. Local competition limits how fast prices can rise, so the real test is whether higher checks keep volume steady. If AOV rises but orders drop, owner take-home can shrink because the truck still carries the same labor and fixed cost base.

Track AOV by daypart

Measure covers per day, check size, and item mix by midweek, weekend, and event sales. Split revenue from tacos, drinks, desserts, and trays so you can see what lifts the ticket and what just adds low-margin volume. A simple weekly report should show AOV by day, because a strong Friday can hide a weak Monday.

Test small price moves on the highest-traffic items first, then watch whether covers hold. If a $1 to $2 lift on combos or premium proteins keeps volume stable, it raises gross profit with little added overhead. If price changes push cover count down, keep the value message tight and use add-ons to raise the bill instead of the base price.

2

Service Days, Hours, and Capacity

Service Days and Hours

Schedule quality matters more than just staying open. This model assumes daily cover patterns across seven days, with the strongest demand from Friday through Sunday. If each modeled day is worked, Year 1 weekly revenue is about $317K, so the real driver is how many high-volume service windows you can actually capture.

That income is fragile if prep time, weather, truck downtime, staffing gaps, or event rules cut selling hours. Long low-volume shifts can hurt profit because labor and prep still happen, but sales do not. A short lunch rush or event slot can pay better than a full slow day, which lifts cash flow and owner take-home pay.

Protect the best selling windows

Track covers per service hour, blocked hours, and sales by daypart. The inputs that matter are covers, average check, usable hours, staffing fill rate, and lost time from weather or truck issues. If one shift is thin, cut it fast and reassign labor to the Friday-to-Sunday windows that carry the week.

Here’s the quick test: compare revenue from a full shift with the labor and prep cost behind it. If a four-hour event slot outperforms an eight-hour weak shift, keep the shorter window. Profitable hours beat more open days when fixed labor and prep are already paid.

Measure revenue per open hour.

Track canceled or blocked hours.

Prioritize peak demand days.

3

Food Cost and Gross Margin

Food Cost and Gross Margin

Food cost is the share of sales spent on ingredients and packaging. In this model, model food ingredients run 10% of revenue in Year 1 and improve to 8% by Year 5; beverage ingredients start at 2% and rise to 15% by Year 5. Every 1 point of food cost on $165M Year 1 revenue cuts about $165K before owner pay.

The inputs are portion control, meat pricing, tortillas, toppings, salsa, packaging, waste, and menu mix. If those costs drift up, gross profit drops first, then cash flow and owner draw. A tighter mix helps margin; waste and promo-heavy beverage sales do the opposite. That’s the line between healthy take-home income and a thin month.

Track Cost by Recipe and Daypart

Measure food cost by item, shift, and daypart, not just monthly. Here’s the quick math: if ingredients stay near 10% of revenue, more sales turn into gross profit; if they move up one point, owner income falls by roughly $165K on the Year 1 revenue base. That hit lands before labor or rent.

Use recipe cards, scale checks, and waste logs to catch drift in meat portions, tortillas, and toppings. Watch beverage cost separately, since it can move from 2% in Year 1 to 15% by Year 5 in the model. If yield slips or packaging runs hot, reset pricing or portions fast.

4

Labor Model and Owner Involvement

Payroll and Owner Shifts

Payroll is a direct take-home lever. Year 1 staffing totals $445K, including a $90K general manager, $80K head chef, $50K certification labor, plus two line cooks, three servers, one bartender, and one dishwasher. That is about $37.1K per month before owner pay. If the owner works every shift, cash outlay falls, but the true labor cost is still there.

This driver includes scheduled labor, overtime, event staffing, and owner hours. The main inputs are covers, service hours, wage rates, and event count. Hiring can support longer hours and more sales, but it also raises the sales needed to break even. If labor runs ahead of traffic, owner income gets squeezed fast.

Track Labor by Shift

Measure labor as a share of sales by day and by event. Here’s the quick math: more staffed hours only help if they produce enough covers to cover the added payroll. Track actual hours, overtime, and owner hours each week, then compare them with covers served and event revenue.

Use a simple labor plan: staff for peak windows, cut slow hours, and log every unpaid owner shift. If hiring adds capacity for dinner or events, price and forecast for the higher break-even sales, not just the extra cash going out.

5

Fixed Costs, Repairs, and Reserves

Fixed Costs and Reserves

Fixed costs hit owner pay before a single taco is sold. This model puts monthly fixed expenses at $17.85K, including $12K rent or lease, $2K utilities, $750 certification fees, $1K property taxes, $600 insurance, $800 maintenance, and $700 accounting and legal. If sales are weak, these costs still cash out, so distributable income drops fast.

Cash reserves matter just as much. The plan calls for $684K minimum cash in Month 2 to cover repairs, downtime, and slow periods before owner draws. Here’s the quick math: owner income only starts after fixed costs and reserve needs are funded, so a truck with thin cash can look profitable on paper but still leave the owner unpaid.

Track Fixed Burn Before Owner Pay

Track monthly fixed burn, not just sales. The key inputs are rent, utilities, certification fees, property taxes, insurance, maintenance, and accounting and legal. A simple check is fixed cost as a share of monthly revenue; if that share rises, owner draw should wait until cash coverage improves.

Keep a separate reserve for repairs and slow weeks. Monitor cash weekly, flag any truck repair, permit lapse, or weather-driven sales dip, and hold owner draws until the reserve target is met. If Month 2 cash falls below the $684K plan, the business is paying the owner too early.

6

Taco Truck Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high taco truck owner-income cases

Owner income table

Income moves with daily covers, ticket size, and weekend mix. The same truck looks tight in Year 1 and much stronger by Year 5 as volume scales.

Low, base, and high cases show how traffic and average ticket shape owner income.

Scenario

Low CaseDownside

Base CaseBase

High CaseUpside

Launch model

This is the lower earnings path using Year 1 demand and pricing.

This is the modeled operating path around the mid-plan year.

This is the stronger earnings path using Year 5 demand and pricing.

Typical setup

About 56 daily covers, $80 weighted AOV, and Year 1 economics with higher launch pressure.

About 94 daily covers, roughly $330M revenue, and Year 3 economics with stronger volume and mix.

About 145 daily covers, roughly $527M revenue, and Year 5 economics with higher traffic and ticket size.

Cost drivers

56 daily covers

$80 weighted AOV

Year 1 EBITDA

$684K cash need

slower ramp

94 daily covers

$330M revenue

Year 3 EBITDA

weekend mix

staffing scale

145 daily covers

$527M revenue

Year 5 EBITDA

premium mix

peak traffic

Owner income rangeBefore owner reserves

$476K EBITDALow earnings

$1.79M EBITDAModel case

$3.34M EBITDAUpside case

Best fit

Use this to test a slow launch, soft traffic, or a longer ramp to steady service.

Use this as the main planning case for hiring, cash use, and day-to-day ops.

Use this to test what happens if the truck hits peak demand and holds it.

!

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; they also exclude personal taxes, debt service, and reserves.

In this model, Year 1 daily revenue ranges from about $1,950 on Monday to $8,100 on Sunday The weighted daily average is about $4,521 from 56 covers and an $80 average order value That is revenue, not owner take-home Payroll, food cost, fixed costs, reserves, and taxes come out after sales

The model reaches break-even in Month 3 and shows a 13-month payback period That depends on hitting the cover and pricing plan early, including 30 to 90 daily covers in Year 1 If opening demand is slower, or repairs and permits take more cash, break-even can move later

This model includes staff from the start, with $445K of Year 1 payroll That includes management, kitchen, service, beverage, cleaning, and certification roles An owner can work shifts to save cash, but unpaid owner labor is not the same as profit Sustainable take-home should account for real labor needs

Volume, ticket size, payroll, and fixed costs move profit the most Year 1 uses 56 daily covers, a weighted $80 AOV, $445K payroll, and $2142K annual fixed costs Food and beverage ingredients total 12% of revenue in Year 1, so portion control matters, but missed traffic hurts faster

Raise income by improving high-margin sales windows first In this model, weekend covers and AOV are stronger, with Sunday at 90 covers and $90 AOV in Year 1 Book better locations, add event sales, lift ticket size with drinks and sides, and protect cash for repairs before increasing owner draws

About the author

Max Cooper

Founder Support Writer

Max Cooper is a founder support writer at Financial Models Lab, helping local business owners understand how small businesses make a profit. He focuses on practical planning before money is invested, with clear guidance on startup cost estimates and basic business planning. His work helps readers move from an idea to a simple, workable plan with confidence.

Choosing a selection results in a full page refresh.