Owner income$120k

Owner income$120kHow Much Do Technology Start Up Owners Make?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k  Net margin60%

Net margin60% Revenue for target pay$610k

Revenue for target pay$610k Business difficultyHard

Business difficultyHard

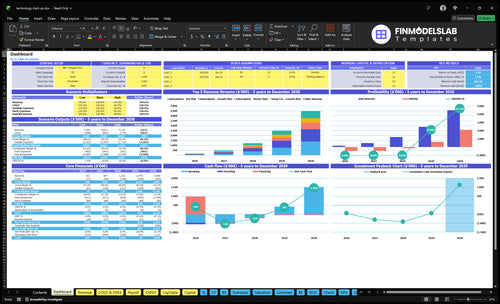

A tech startup owner can model a $120,000 founder salary here, but that pay depends on funding, cash reserves, and hitting the revenue plan The researched assumptions show EBITDA of -$473,000 in Year 1, -$473,000 in Year 2, -$143,000 in Year 3, then $643,000 in Year 4 and $2119 million in Year 5 Gross margin after hosting and third-party service fees improves from 87% to 91% Treat these as planning assumptions, not guaranteed salary, distributions, tax advice, or exit value

Owner income$120kNet margin60%Revenue for target pay$610kBusiness difficultyHardWant to test your founder pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Tech Startup model?

The Tech Startup Financial Model Template shows revenue, margin, costs, reserves, and founder take-home assumptions—open the model.

Founder-income highlights

- $120k founder salary

- Month 34 breakeven

- Month 37 cash low

- Year 4 EBITDA: $643k

- Year 5 EBITDA: $2119m

How much does a tech startup founder make?

In this Tech Startup model, the founder makes $120,000 per year from launch, but that pay is funded by runway, not profit; track it beside How Is The Growth Of Your Tech Startup's Core Business Metric Progressing? because EBITDA is -$473,000 in Year 1 and breakeven lands around Month 34.

Founder pay by stage

- Pre-revenue pay needs outside cash

- Launch salary: $120,000 CEO pay

- Year 1 EBITDA: -$473,000

- Breakeven target: Month 34

When pay loosens

- Year 2 pay stays constrained

- Year 4 EBITDA: $643,000

- Year 5 EBITDA: $2.119 million

- Raise pay after profit scales

How do costs affect a tech startup founder salary?

Costs squeeze founder pay fast at Tech Startup: hosting and third-party fees take 13% of revenue in Year 1 and 9% in Year 5, so gross margin stays at 87% to 91% before other spend. Add 7% in Year 1 and 3% in Year 5 for digital ads and sales commissions, plus $804k a year in fixed overhead, and salary only improves after those costs, reserves, and reinvestment are covered. For launch planning, see What Is The Estimated Cost To Open And Launch Your Tech Startup?

Margin math

- 13% fee drag in Year 1

- 9% fee drag in Year 5

- Gross margin stays 87%-91%

- Salary is not margin

Burn drivers

- Ads and commissions add 7% Year 1

- Ads and commissions add 3% Year 5

- Payroll drives burn: $4075k to $805k

- $804k annual fixed overhead stays in place

How should runway shape startup founder pay?

For Tech Startup, founder pay should follow runway, not pride: in a lean bootstrapped case, delay or cap it even if the model shows $120k; in a growth-funded case, financing can cover founder pay while EBITDA (earnings before interest, taxes, depreciation, and amortization) is still negative, but that is not profit. The clean break is Month 34 breakeven, and the main cash guardrail is the Month 37 low of -$349k. Keep salary, distributions, funding, and equity upside separate.

Lean pay rule

- Bootstrapped means survival first.

- Cap or delay founder pay.

- $120k is not a right.

- Protect cash through Month 37.

Funding pay rule

- Funding can cover pay.

- EBITDA can stay negative.

- Breakeven starts after Month 34.

- Year 4 and 5 get stronger.

Want the six income drivers?

1

$29-$199+Recurring Revenue

Starter, Growth, and Pro pricing plus usage fees lift revenue per customer and feed every take-home dollar.

2

$150->$120CAC Efficiency

A lower CAC on a bigger budget means more paid users for the same spend, so payback improves.

3

EditableChurn Control

Retention is a direct LTV lever, and without a churn input this stays the biggest model gap.

4

87%-91%Gross Margin

Cloud hosting and third-party fees take only a small slice of revenue, so most new sales stay in the business.

5

$408K-$805KPayroll Burn

Payroll rises fast as headcount grows, so hiring pace can wipe out profit before scale catches up.

6

M34/M37Runway Timing

Breakeven in Month 34 and the cash low in Month 37 show how much growth the business can fund before new capital.

Tech Startup Core Six Income Drivers

Recurring Revenue Per Customer

Recurring Revenue Per Customer

Recurring revenue per customer, or ARPA, is the monthly cash each paying account brings in. It includes subscription fees and transaction revenue, not free users. In Year 1, the weighted monthly ARPA is about $6,640, with a 60% Starter / 30% Growth / 10% Pro mix and plan prices of $29, $79, and $199.

As the plans rise to $35, $95, and $249 by Year 5, better packaging and more Pro mix should lift cash before costs and reserves. The risk is simple: low-price customers can soak up support and hosting capacity, so revenue per customer has to grow faster than service load if you want room for founder pay.

Track Paid Mix and ARPA

Track paid customers, ARPA by tier, and transaction revenue every month. Break revenue into Starter, Growth, and Pro so you can see which accounts actually fund payroll. Here’s the quick test: if the Pro mix rises, does cash per customer rise faster than support tickets and hosting use?

Use pricing and packaging to move customers into higher tiers. Keep Starter as the entry point, but watch for heavy-support accounts that make the tier expensive. If that happens, tighten onboarding, cap low-tier service, or push upgrades so recurring revenue per customer stays high enough to cover overhead and owner draw.

1

Customer Acquisition Efficiency

Customer Acquisition Efficiency

When CAC payback is short, marketing cash comes back fast and the founder can keep paying themselves. Here the model shows CAC improving from $150 in Year 1 to $120 in Year 5, while the annual marketing budget rises from $50k to $700k. That only helps if sales cycles stay tight and onboarding does not slow cash recovery.

Here’s the quick math: budget divided by CAC implies about 333 paid customers in Year 1 and 5,833 in Year 5. Visitor-to-paid conversion improves from 0.45% to 1.08%, so the funnel gets more efficient. What this hides is simple: if onboarding stretches or paid channels weaken, cash available for salary tightens fast.

Track Payback, Not Just Traffic

Measure CAC payback as the time to earn back acquisition spend from gross profit. Track visitor-to-paid conversion, sales cycle length, onboarding days, and spend by channel. If a channel buys leads but not paid customers fast enough, it hurts owner income even when top-line growth looks strong.

- Watch spend per paid customer.

- Split conversion by channel.

- Flag onboarding delays fast.

Keep the budget tied to cash, not vanity traffic. Faster follow-up, less drop-off in onboarding, and cleaner channel tests protect profit and keep salary room open. If one channel drives customers at $120 CAC but another burns cash and stalls closes, shift spend quickly.

2

Retention And Churn

Retention and Churn

Churn rate is the share of customers lost in a period. The source data gives no churn value, so keep it editable in the model. For this subscription business, lower churn means more monthly recurring revenue (MRR) stays in place, so the owner can pay themselves from growth instead of just replacing lost accounts.

Here’s the quick math: churn hits twice, once in lost revenue and again in slower CAC payback because each acquired customer earns back less over time. New sales can hide the problem for a while, but support load and reserve needs still rise if renewals slip.

Keep Churn Visible

Measure retention by cohort, not by total sales alone. A rising top line can hide churn, so track lost customers, lost MRR, and expansion MRR separately. That tells you whether the company is growing because customers stay longer or because new deals are filling a leak.

- Track customer churn monthly.

- Track MRR churn monthly.

- Split renewals from expansion.

- Watch support tickets by cohort.

- Keep reserves if churn worsens.

If churn climbs, founder pay gets squeezed because more cash must go to sales, support, and replacements. Keep the churn assumption editable until you have real renewal data, then test pricing, onboarding, and support load together so retention improves without bloating payroll.

3

Gross Margin After Hosting And Support

Gross Margin After Hosting

Gross margin after hosting and support is what’s left after direct delivery costs, before payroll and overhead. In this model, cloud hosting falls from 8% of revenue in Year 1 to 6% in Year 5, and third-party service fees fall from 5% to 3%, so combined gross margin rises from 87% to 91%.

Here’s the quick math: at $100,000 of revenue, direct costs drop from $13,000 to $9,000. That helps cash available for payroll and owner pay, but higher usage can push up infrastructure, API, data, payment, and support costs, so margin only holds if usage stays efficient.

Control Cost per Account

Track hosting as a % of revenue, third-party fees, and support tickets per paying customer. Also watch usage by plan, because low-price accounts can consume outsized API, data, and support capacity. If those ratios drift, gross margin slips even when revenue grows.

Set pricing and limits around heavy use, and review monthly gross margin by cohort. If a plan needs more support or third-party traffic than expected, reprice it or add usage fees. That keeps contribution cash high enough to fund payroll, reserves, and any owner draw.

4

Product And Payroll Burn

Product and Payroll Burn

Hiring pace is the big swing factor here. Payroll starts at $4075k in Year 1 and rises to $805k by Year 5, including the $120k founder salary, plus a $130k lead engineer, a $110k data scientist, and junior engineering later. Add $6,700/month of fixed overhead, and owner pay only stays safe if revenue grows fast enough to cover the ramp.

Here’s the quick math: more headcount can lift product reliability and growth capacity, but it also pulls cash out before sales catch up. Delaying hires protects runway and can keep founder income intact longer, while over-hiring can force the owner to cut pay or raise capital sooner. The key input is timing each hire against monthly revenue and cash balance.

Hire to runway, not ego

Build a monthly hiring plan and tie each role to a cash trigger. Track payroll burn, monthly overhead, and the month each hire starts contributing to product speed or support load. If a role doesn’t improve reliability, release cycle time, or customer retention, it’s probably too early.

- Model headcount by month

- Track founder salary separately

- Delay junior hires until demand

- Test cash burn after each hire

What this estimate hides is the lag between hiring and output. A $130k engineer or $110k data scientist can improve the product, but only if onboarding is fast and work is focused. If revenue is still uneven, keep the team lean so founder take-home doesn’t get crowded out by burn.

5

Runway And Reinvestment Policy

Runway And Reinvestment

Founder pay depends on how much cash stays in the company, not just profit on paper. Here’s the quick math : operating breakeven lands around Month 34, but cash still bottoms at -$349k in Month 37. So even if the business turns profitable, early cash may need to stay inside the company for support, reliability, hiring, and growth tests.

Salary is planned cash pay, while distributions are profit withdrawals after obligations. That means owner income should track cash runway, reserve targets, and the timing of reinvestment. If cash is tight, taking more out can force outside funding or slow product work, and that hits both growth and take-home pay.

Pay Yourself Without Breaking Runway

Track monthly cash balance, not just net income. Use Month 34 breakeven and the -$349k Month 37 low as stress points in the forecast, then set a cash floor before any owner draw. If the floor is missed, keep salary fixed and skip distributions until reserves recover.

- Model salary, then distributions.

- Hold back cash for support.

- Recheck runway after hires.

- Test growth spend against reserves.

6

Scenario objective: Compare lean, base, and growth income planning cases for founder pay

Owner income scenarios

Owner income moves with marketing efficiency, funnel conversion, and margin. Early losses can still fund the founder salary, but cash stays tight until breakeven.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | Owner pay is funded by cash or financing while the business is still in proof mode. | Owner pay follows the path to breakeven around Month 34. | Owner pay can include salary plus profit draws once scale improves in Year 5. |

| Typical setup | Year 1 uses a $50k marketing budget, $150 CAC, about 333 implied paid customers, 87% gross margin, and -$473k EBITDA. | Around the transition, gross margin sits near 89% to 90%, cash bottoms at -$349k in Month 37, and the model reaches breakeven in Month 34. | Year 5 uses a $700k marketing budget, $120 CAC, about 5,833 implied paid customers, 91% gross margin, and $2.119m EBITDA before taxes, debt, capex, reserves, and distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $120k salary onlySalary only | $120k salary, small upsideNear breakeven | $120k salary + distributionsProfit upside |

| Best fit | Use this to test the cash needed to keep founder pay on during the first year. | Use this if you want a realistic take on pay once the model crosses breakeven. | Use this for a scale case where profit can support salary plus owner draws. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Tech Startup Porter's Five Forces Analysis

- Tech Startup BCG Matrix

- Tech Startup Business Model Canvas

- 7 Essential Financial KPIs for a Tech Startup

- Tech Startup Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Tech Startup Profitability and Scale Growth

- How Much Does It Cost To Run A Tech Startup Monthly?

- Tech Startup Costs: Plan $88K CAPEX And 34 Months To Breakeven

- Tech Startup Financial Model Template in Excel

- How To Start A Tech Startup: 6 Launch Steps To First Revenue

- How to Write a Tech Startup Business Plan: 7 Steps to Financial Clarity

- Tech Startup Marketing Mix

- Tech Startup Marketing Plan

- Tech Startup Business Proposal

- Tech Startup PESTEL Analysis

- Tech Startup Pitch Deck Example Editable PPTX

- Tech Startup Business SWOT Analysis

- Tech Startup Value Proposition Canvas

Frequently Asked Questions

The model includes a $120,000 annual CEO/founder salary That is planned cash compensation, not guaranteed take-home EBITDA is -$473,000 in Year 1 and Year 2, then turns stronger after breakeven around Month 34, reaching $643,000 in Year 4 and $2119 million in Year 5 before taxes, debt, capex, reserves, and distributions