For Sound Bath Experiences, the biggest income drains are event-level leakage and fixed overhead: 8% practitioner fees, 1% consumables, 8% marketing, and 2% booking software cut into each session, while fixed monthly costs still run about $4,800. If you want the full startup picture, see How Much Does It Cost To Open And Launch Your Sound Bath Experiences Business?Low attendance hurts fast because rent and payroll do not fall when seats go empty.

Year 1 leakage

8% practitioner fees

1% consumables

8% marketing

2% booking software

Fixed cost drag

$4,800 monthly fixed costs

Studio rent, utilities, insurance

Permits, website, cleaning

Payroll: $1.675K Year 1, $3.025K Year 5

How many sound bath sessions are needed to pay the owner?

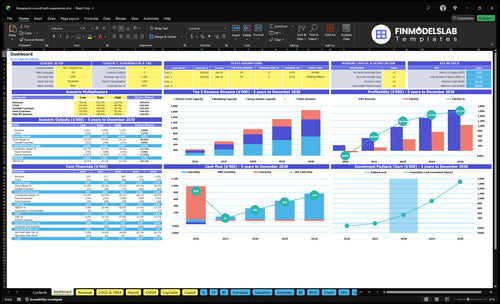

In Year 1, Sound Bath Experiences needs about 765 group sessions a month just to cover the $188K monthly overhead before any owner draw, because each session brings in about $246 of contribution from $304 of revenue. If you mean actual owner pay, keep that separate from distributable EBITDA and reserves. By Year 5, the math improves fast: each session contributes about $895, so the break-even load drops to about 210 sessions a month.

Year 1 break-even

$188K monthly overhead

$246 contribution per session

~765 sessions per month

Owner draw is not included

Owner pay timing

$990 revenue per Year 5 session

$895 contribution per session

~210 sessions per month

Pay owner from EBITDA, then reserves

How much can a sound bath owner make per month?

A Sound Bath Experiences owner can make -$5.3K/month in Year 1, then about $11.6K/month in Year 2, and about $86.9K/month by Year 5 on modeled EBITDA, not guaranteed salary. EBITDA means earnings before interest, taxes, depreciation, and amortization, so owner cash depends on taxes, reserves, distributions, and whether the owner also takes a staff salary; What Is The Most Important Metric To Measure The Success Of Sound Bath Experiences? is tied to keeping paid seats full.

Modeled EBITDA

Year 1: -$64K, or -$5.3K/month

Year 2: $139K, or $11.6K/month

Year 5: $1.043M, or $86.9K/month

Math: annual EBITDA divided by 12

Upside Drivers

28 billable days per month

90% group session occupancy

$55 average group ticket

$650 private events; $95 workshops

Sound Bath Experiences Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Booked Volume

22-28/mo

More billable days mean more sessions sold, and this is the fastest way to lift owner income.

2

Fill Rate

45%-90%

Higher occupancy turns the same studio time into more revenue, so empty seats hit take-home hard.

3

Price Mix

$45-$650

Group tickets, private events, and workshops set how much each booking earns before costs.

4

Overhead Load

$4.8K/mo

Studio rent, utilities, and other fixed costs decide how much gross cash is left for profit.

5

Memberships

$120-$140

Recurring memberships smooth cash flow and reduce the pressure to fill every session from scratch.

6

Payroll Load

$168K-$303K

Staff pay rises from about $167.5K to $302.5K a year, so the delivery model has a big effect on EBITDA.

Sound Bath Experiences Core Six Income Drivers

Booked Session Volume

Booked Session Volume

Booked session volume is the count of paid sound bath sessions on the calendar. The base model rises from 22 billable days per month in Year 1 to 28 in Year 4 and Year 5, so more bookings create more revenue chances. One clean rule: more sessions only help if each one clears staffing, setup, cleaning, marketing, and room use.

This driver matters a lot because breakeven depends on enough paid activity to cover $4,800 in monthly fixed costs plus payroll. A busy calendar with weak attendance still misses the mark, since the room, labor, and prep cost money even when seats are thin. Track booked days, paid seats, and profit per session together, not in isolation.

How to manage booked sessions

Track booked days, paid attendance, and profit per session every month. If volume grows but attendance stays soft, revenue may rise slower than labor and cleaning costs. Set a minimum attendance rule before opening more dates, and cancel or combine weak sessions early so the calendar does not look full while cash stays tight.

Measure paid sessions, not just holds.

Watch session profit after direct costs.

Compare booked days to the 22-to-28 day plan.

Cut low-fill dates before payroll swells.

The main test is simple: each added session should help cover fixed overhead and owner pay. If a new booking only fills the room but does not beat staffing, setup, cleaning, and marketing, it adds work without adding income. Keep the schedule tight, then expand only when repeat demand supports it.

1

Attendance And Capacity Use

Attendance And Capacity Use

When seats stay half full, owner income gets squeezed fast. Here, occupancy is the key input: it rises from 45% in Year 1 to 90% in Year 5, and group session revenue climbs from about $304/session to $990/session. The math works because setup, rent, and guidance costs do not rise much per extra attendee.

The main inputs are capacity, ticket price, and occupied seats. Fuller sessions lift gross margin and cash flow, so the owner has more room for pay after fixed costs. The risk is weak demand, then discounting too early instead of protecting price. A better move is to hold a clean minimum-attendance rule and fill late seats with a waitlist.

Fill Seats Before Cutting Price

Track occupancy by session, not just total bookings. If a class runs at 45% to 60% full, test cancellation rules, waitlists, and booking cutoffs before discounting. That protects revenue quality, because every extra attendee adds cash with little added rent or setup cost.

Use a simple floor: do not run below the minimum seats needed to cover the session. If demand is soft, push bundles, memberships, or off-peak fills first. The goal is a steadier 90% occupancy path, since higher seat use raises owner income without forcing payroll or space costs to rise in step.

Measure fill rate per session.

Set a minimum-attendance threshold.

Use waitlists to catch late demand.

Limit discounts until demand is fixed.

2

Pricing And Offer Mix

Offer Mix

Pricing and offer mix raise income by pushing each booking into a higher-value format. A group ticket move from $45 to $55 is +22.2%; private events from $450 to $650 are +44.4%; workshop tickets from $75 to $95 are +26.7%; memberships from $120 to $140 are +16.7%. The gain shows up fastest when the same room hours sell at a higher average ticket.

The tradeoff is demand quality. Premium offers only work with local demand, clear positioning, strong facilitation, and a consistent customer experience. If the mix shifts upmarket but fill rates fall, revenue can stall and owner pay gets less reliable. So the key metric is revenue per session type, not just total bookings.

Raise Ticket Value

Track each offer separately: tickets sold, fill rate, refund rate, and revenue per hour. That shows whether workshops, memberships, or private events are lifting average order value and filling off-peak slots. The best mix is the one that turns otherwise empty time into paid sessions without adding much extra labor.

Test workshop dates first

Sell private events off-peak

Raise price with demand

Keep facilitation consistent

Compare each offer against the same time block. If a $650 private event replaces a low-fill group class, cash flow improves fast because the room is already staffed and booked. If the higher-price offer cuts attendance too much, the take-home gain disappears, so keep minimums and cancellation rules tight.

3

Venue And Direct Event Costs

Venue and Direct Event Costs

$3,500 monthly studio rent and $4,800 total fixed overhead set the floor for this business. Empty seats still carry rent, utilities, insurance, permits, website, cleaning, and payroll, so break-even attendance matters more than headline demand. In Year 1, direct and variable costs are 19% of revenue, so the early model keeps 81% contribution before fixed costs and owner pay.

Here’s the quick math: when venue costs stay fixed, every added attendee lifts cash flow fast, but weak occupancy leaves the owner covering the room from the first dollar of revenue. If Year 5 variable costs really rise to 96% of revenue, take-home income gets squeezed hard, and the business needs much fuller sessions just to protect profit.

Track break-even seats, not just bookings

Measure attendance per session, ticket price, and direct event cost per class. Break them into venue costs, cleaning, payroll, and any session-level spend so you can see which costs move with volume and which do not. That tells you the minimum paid seats needed to cover the $4,800 fixed overhead before the owner can draw profit.

Set a minimum-seat rule.

Track cost per filled seat.

Cut empty-room sessions fast.

Test pricing before adding dates.

If attendance stays soft during ramp-up, reduce low-fill sessions, use waitlists, and protect margins with fewer but fuller events. The goal is simple: keep venue cost per attendee low enough that each class helps, not hurts, owner income.

4

Marketing And Repeat Bookings

Marketing And Repeat Bookings

This driver covers paid marketing, booking software, and how much demand comes back without paying to reacquire it. Marketing is 8% of revenue in Year 1 and 4% by Year 5; booking software drops from 2% to 1%. Stable repeats cut customer acquisition cost (CAC) and make attendance easier to forecast, which helps protect Month 14 breakeven and owner cash flow.

Track total revenue, marketing %, software %, repeat-booking rate, and channel mix. One clean rule: more repeat demand means more profit from the same calendar. If seats keep filling through partners, memberships, and referrals, the owner keeps more of each dollar instead of spending it to refill the room.

Track Repeat Demand By Channel

Measure bookings by source so you know which channels bring back paying clients, not just clicks. Focus on wellness studios, therapists, spas, employers, retreat hosts, and memberships. If a channel brings repeat guests at lower CAC, keep it; if it only creates one-off fills, it’s expensive revenue.

Wellness studios

Therapists and spas

Employers and retreat hosts

Memberships

Use the Year 1 to Year 5 path as the target: 10% total for marketing plus software in Year 1, then 5% by Year 5. That gap flows straight into operating profit and owner draw. If repeat rates slip, forecast more spend to keep attendance stable.

5

Owner-Operated Delivery Model

Owner-Led vs Hired Delivery

Owner-led sessions can keep gross margin higher because you avoid paying a lead practitioner, but they also cap how many billable sessions you can run and can push burnout. The key inputs are session count, prep time, attendance, and whether the owner is the only delivery engine. If the calendar is full but the owner is exhausted, the business may still be profitable on paper and weak in take-home pay.

Once the model scales, hired delivery can open more dates, but it adds real payroll: a $60K lead practitioner, a $70K studio manager, and part-time practitioner capacity moving from 0.5 FTE to 2.5 FTE. Here’s the clean math: owner labor should be separated from EBITDA and distributions, or you can overstate profit and underpay the owner.

Track Capacity Before You Hire

Measure sessions per week, owner hours per session, attendance, and supervision time. That tells you when owner-led delivery is hitting its ceiling and whether hired staff will actually lift owner income. A simple test is whether extra sessions cover the added payroll and quality-control load without weakening repeat bookings.

Track billable sessions weekly

Price owner labor separately

Model payroll before adding staff

Watch burnout and service quality

Use EBITDA for business profit, then subtract fair owner pay to see true take-home income. If you add practitioners too early, margins can drop faster than revenue grows. If you wait too long, the owner becomes the bottleneck and the calendar stops scaling.

6

Sound Bath Experiences Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income changes fast with occupancy, ticket mix, and billable days. The low case is a ramp loss, while later years support strong EBITDA if volume holds.

Low, base, and high cases show how fill rate and pricing change owner income.

Scenario

Lean CaseRamp

Base CaseStable

High CaseScaled

Launch model

A ramp case with 22 billable days a month, 45% occupancy, and -$64K EBITDA.

A modeled case with 24 billable days a month, 60% occupancy, and $139K EBITDA.

A stronger earnings path with 28 billable days a month, 90% occupancy, and about $1.043M EBITDA.

Typical setup

The studio runs 22 billable days a month at 45% occupancy, with $45 group tickets, $450 private events, $75 workshops, and about 81% contribution margin, but Year 1 EBITDA is still -$64K.

The model lifts to 24 billable days a month and 60% occupancy, with $48 group tickets, $500 private events, and $139K EBITDA as volume spreads fixed costs.

By Year 5, 28 billable days a month, 90% occupancy, $55 group tickets, $650 private events, and $95 workshops push EBITDA to about $1.043M.

Cost drivers

22 billable days

45% occupancy

$45 group tickets

$450 private events

81% contribution margin

24 billable days

60% occupancy

$48 group tickets

$500 private events

higher session volume

28 billable days

90% occupancy

$55 group tickets

$650 private events

$95 workshops

Owner income rangeBefore owner reserves

-$64KRamp case

$139KStable case

$1.043MScaled upside

Best fit

Use this to stress test a slow ramp, weak fill rates, or slower word-of-mouth.

Use this for planning around a normal Year 2 operating pace.

Use this to test owner income once the studio is near full and pricing has moved up.

!

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In this model, Year 1 is not yet distributable because EBITDA is -$64K Breakeven arrives in Month 14, and Year 2 EBITDA reaches $139K, or about $116K/month before taxes, debt, reserves, and owner distributions By Year 5, EBITDA reaches $1043M under higher occupancy and pricing assumptions

The modeled breakeven point is Month 14, with payback in 27 months That timing depends on 22 billable days per month in Year 1, 45% occupancy, $45 group tickets, and startup capex of $66K If attendance ramps slower, the owner may need more cash cushion

Not always, but this model assumes a studio with $3,500 monthly rent and $4,800 total fixed monthly overhead A lighter venue model could reduce fixed risk, while a studio can support memberships, repeat classes, workshops, and higher capacity The right choice depends on booking consistency

Attendance, pricing, payroll, and fixed costs drive profit most In the model, occupancy rises from 45% to 90%, group ticket prices rise from $45 to $55, and payroll grows from $1675K to $3025K Empty seats hurt because rent and staff costs continue

Build owner pay from cash flow, not hope Start with revenue by session type, subtract practitioner fees, consumables, marketing, software, $4,800 monthly overhead, payroll, and reserves Then compare the result with target owner draw Use the first year as a ramp period, not a guaranteed paycheck

About the author

Sofia Reed

First-Time Founder Guide Writer

Sofia Reed writes for Financial Models Lab, helping first-time founders plan launch budgets with clarity and confidence. She focuses on estimating startup needs before opening, translating business costs into simple language for service business founders. With a practical approach to simple launch planning, she balances optimism with cost-aware thinking so new owners can prepare for opening day with a clearer view of what it takes to start strong.

Choosing a selection results in a full page refresh.