How Much Does a Turf Management Service Owner Make? $529K Year 5 EBITDA

A turf management service owner can move from no safe draw in the first year to meaningful take-home once recurring contracts cover payroll, equipment, and overhead In the researched model, EBITDA is -$142K in Year 1, improves to $167K in Year 2, and reaches $529K in Year 5 If the owner fills the Director of Operations role, the model already budgets $115K per year for that function Any extra owner draw should come after cash reserves, taxes, debt service, and equipment replacement needs

Owner income$115K baseNet margin-25% to 21%Revenue for target pay$548KBusiness difficultyHard

Want to test your turf service owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want the full Turf Management Service financial model?

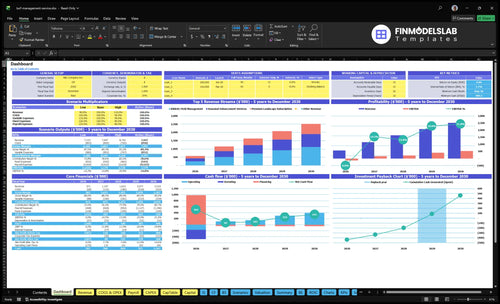

This screenshot shows owner take-home changing as contracts, crew hiring, fuel, consumables, and equipment costs move across the Turf Management Service Financial Model Template; it ties dashboard, revenue assumptions, customer mix, payroll, operating costs, capex, cash flow, scenarios, and owner income outputs. Open the model to review the projections.

Owner-income model highlights

Owner take-home shifts fast

Revenue and EBITDA swing

Cash and payback timing

How much can a turf management business owner pay themselves?

A Turf Management Service owner can plan $115K/year as pay if they personally fill the Director of Operations role modeled from Month 1 through Month 60; that’s wages for real field or management work, not a guaranteed profit draw. For the cost base behind that decision, see What Does It Cost To Run Turf Management Service?, because owner take-home should follow cash reserves, taxes, debt service, and equipment replacement needs.

Pay Structure

Separate wages from profit distributions

Use $115K for operations work

Pay distributions only from surplus cash

Set policy before hiring crews

Profit Guardrails

Year 1 EBITDA: -$142K

Year 2 EBITDA: $167K

Year 5 EBITDA: $529K

Retain cash for equipment replacement

How much revenue does a turf management business need?

For Turf Management Service, the revenue floor is about $948K a year if the goal is $100K of incremental owner pay in Year 2 before taxes and reserves. The model’s Year 2 run rate is $1.147M revenue with $167K EBITDA, so the business clears the target only if pricing, crew utilization, and retention stay tight. Add equipment reserves or debt service, and the required revenue goes up.

Revenue floor

$100K owner pay target

$504K payroll in Year 2

$1.086M fixed overhead

$60K marketing spend

What moves it

81.5% variable margin drives the math

$1.147M Year 2 model revenue

$167K EBITDA at model scale

Reserves and debt service raise the bar

What is a realistic turf management profit margin?

A realistic margin for a Turf Management Service is highly unstable at first because payroll and equipment costs are heavy, so if you’re planning one, start with How Do I Write A Business Plan To Launch Turf Management Service? and stress-test cash flow. The model shows -249% EBITDA margin in Year 1, then 146% in Year 2, 130% in Year 3, 199% in Year 4, and 210% in Year 5.

Margin swing

Year 1:-249% EBITDA margin

Year 2:146% EBITDA margin

Year 3:130% EBITDA margin

Year 4:199%; Year 5: 210%

Cost pressure

Consumables fall from 120% to 100%

Fuel and maintenance fall from 75% to 55%

Each 1-point cost rise adds about $57K in Year 1

Each 1-point cost rise adds about $252K in Year 5

Turf Management Service Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six turf management income drivers?

1

Field Count

$571K-$2.52M

More field and landscape contracts drive the biggest revenue swing, lifting owner take-home as sales scale from Year 1 to Year 5.

2

Pricing Power

$3.5K-$5.0K

Higher monthly rates on the $3,500, $2,200, and $5,000 service lines flow through fast because direct labor and materials do not rise one for one.

3

Crew Output

2-10 FTE

Better route and crew output lets the same core team cover more acres, which lowers labor per job and improves EBITDA.

4

Service Mix

20%-55%

Shifting work toward recurring field management and premium subscriptions supports steadier cash and better margins than one-off seasonal jobs.

5

Equipment Use

195%-155%

Higher truck and mower use cuts the variable cost load, so more revenue turns into take-home instead of fuel and upkeep.

6

Retention

9-49 mo

Stronger renewals and seasonality control help the business reach breakeven in Month 9 and payback in 49 months.

Turf Management Service Core Six Income Drivers

Contracted Field And Acreage Volume

Contracted Acreage Volume

More contracted fields and acres make revenue steadier because the work turns into monthly recurring revenue instead of one-off jobs. The key inputs are contract count, acres per crew, visits per year, and renewal rate. When those stay balanced, the owner gets better scheduling, cleaner labor planning, and more visible draw capacity.

Here’s the risk: the model shows $571K in Year 1 revenue and $2519M in Year 5, so volume growth carries the whole plan. If sales outrun crew and equipment capacity, you get missed visits, rework, and margin bleed. One clean rule: booked acres only help income if the team can service them on time.

Sell To Capacity, Not Past It

Track volume by customer type: schools, municipalities, athletic complexes, HOAs, and commercial sites. Watch acres per crew day against scheduled visits, then cap new sales when routes start slipping. A full route helps cash flow; an overloaded route cuts gross margin and delays owner pay.

Contract count by site type

Acres per crew each week

Visits per year per contract

Monthly recurring revenue

Renewal rate by account

Use renewal data and route density to forecast cash. Stable volume lowers selling pressure, but only if you leave room for weather delays and seasonal spikes. If onboarding takes too long or routes spread too far, owner draw gets less predictable fast.

1

Pricing Per Visit Or Contract

Scope-Based Contract Pricing

This driver is the monthly contract price or price per acre you charge for each visit plan. It has to cover visit frequency, turf condition, labor hours, materials, travel, equipment wear, and performance standards. If pricing misses those inputs, gross margin shrinks and owner pay gets squeezed even when revenue looks fine.

Here’s the quick math: the model uses $3,500 athletic field management, $2,200 premium landscape subscription, and $5,000 seasonal enhancement services in Year 1. Local bid pressure is real, but underpricing hits EBITDA before owner take-home. Change-order rate matters when scope expands after storms, play, or heavy wear.

Price to Scope, Not Just to Win

Track pricing by scope, not just by account. Use a simple model with visit frequency, acres, labor hours, materials, travel, and equipment wear, then compare planned margin to actual margin each month. If the field needs more work than the bid assumed, the price should move too. Better scope-based pricing protects margin without needing more accounts.

Planned vs actual gross margin

Change-order rate by contract

Travel hours and labor hours

2

Service Mix

Service Mix

Richer service mix raises revenue per client, but only if the crew can deliver the extra scope. In this model, athletic field management moves from 400% in Year 1 to 550% in Year 5, premium landscape subscriptions from 350% to 550%, and seasonal enhancement services from 200% to 400%.

More lines mean more billable visits, materials, and labor hours, so revenue can rise faster than field count. But consumables and rework also climb if scheduling slips. One clean rule: if a service add-on does not lift contract value enough to cover labor and inputs, it cuts EBITDA and the owner’s draw.

Raise Value Per Account

Track revenue by service line, seasonal enhancement attach rate, consumables %, and labor hours per service. That tells you whether mowing, fertilization, aeration, overseeding, topdressing, weed control, pest monitoring, and turf repair are making money or just adding work. If a bundle uses more material than planned, raise price or narrow the scope.

Test bundled pricing by customer type and keep regulated work separate until state and local compliance is clear. Athletic fields, premium landscapes, and seasonal add-ons do not carry the same labor curve. The goal is simple: price the scope, not the truck roll, so each added service pushes gross margin and cash flow up instead of flattening them.

3

Crew Productivity

Crew Productivity

This driver is the labor hours behind each field visit. It includes routing, training, supervision, overtime, and rework, plus how many visits a crew can finish in a day. When revenue per specialist and gross profit per labor hour rise, owner pay rises too, because the same labor base supports more billable work.

The model grows from 2 Turf Management Specialists in Year 1 to 10 in Year 5, while payroll rises from $388K to $1,074M as disclosed. Early labor savings are real cash, but they are not the same as scalable profit. If overtime and callbacks climb, revenue growth gets eaten by labor.

Track Labor Per Visit

Measure visits per crew day, overtime %, callbacks, and labor hours per field visit. Here’s the quick math: if a route takes more hours but doesn’t add billed work, margin drops. Higher gross profit per labor hour turns the same schedule into more EBITDA and more owner draw.

Use route clustering, pre-trip checklists, and training logs to cut rework. A crew that arrives prepared and finishes right the first time protects cash flow, because every callback adds unbilled labor. Watch staffing growth closely: adding heads faster than billable volume is how payroll outruns revenue.

4

Equipment Utilization

Equipment Utilization

When mowers, aerators, sprayers, spreaders, trailers, and trucks sit idle, your cost per field visit goes up fast. In this model, fuel and equipment maintenance eat 75% of revenue in Year 1 and 55% in Year 5, so the room for owner pay is tight until utilization improves. The real test is revenue per equipment hour, not just total sales.

Here’s the quick math: the plan includes $312K of capex across the mowing fleet, aeration gear, service vehicles, field marking, and diagnostic tools. That spend only pays back if hours are booked, routes are tight, and downtime stays low. Replacement reserves are cash, not fake profit, so underfunding them makes later capex hit owner draw.

Track Hours, Fuel, and Repair Burn

Track equipment hours, downtime, fuel % of revenue, repair cost %, and reserve funding by asset class. The goal is to see which machine is earning its keep and which one is dragging margin. If a truck or mower is spending time parked, it still carries depreciation and reserve pressure, so the owner gets paid less even when revenue looks fine.

Set a simple rule: every route should be priced to cover labor, fuel, repairs, and a replacement reserve before profit. Use visit-level data to spot weak utilization, then fill empty hours with more acreage, tighter routing, or bundled services. Higher utilization lowers cost per field visit, and that is what turns revenue into cash the owner can actually take home.

5

Retention, Route Density, And Seasonality

Retention, Route Density, and Seasonality

When contracts renew, jobs cluster by geography, and off-season work fills the calendar, owner pay gets steadier. The model shows a $489K minimum cash need in Month 8 and breakeven in Month 9, so late renewals or empty winter weeks can hit draws fast. Better retention also cuts replacement selling cost, with CAC improving from $1,500 in Year 1 to $1,200 in Year 5.

This driver includes renewal rate, travel hours, route density, off-season revenue, and cash reserve months. More retained contracts mean fewer sales calls just to replace lost work, while tighter routes reduce idle crew time and fuel waste. One missed renewal is not just lost revenue; it also creates extra selling cost and can push owner draw timing back.

Track renewals, miles, and off-season fill

Measure each account by renewal date, service area, and seasonal add-on potential. If crews are crossing town for one stop, route density is too low. If winter or shoulder months go quiet, sell seasonal services early so cash does not dip before Month 9. That protects margin and keeps payroll and owner pay on plan.

Track renewal dates monthly.

Group jobs by zip code.

Price winter add-ons early.

Watch travel hours per route.

Keep cash for Month 8.

6

Turf Management Service Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high turf owner income scenarios

Owner income scenarios

Launch costs and hiring keep Year 1 negative, but Year 2 turns profitable and Year 5 scales hard. Owner income moves with contract mix, staffing, and how fast cash needs fall.

Low, base, and high owner-income cases for a turf management service.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

Year 1 is loss-making, so owner income stays thin while the service base is built.

Year 2 turns positive, so owner income can start to work if collections and staffing stay on plan.

By Year 5, scale is stronger and owner income can support a much larger draw.

Typical setup

Revenue is $571K, EBITDA is -$142K, payroll is $388K, and marketing is $45K in the first operating year.

Revenue reaches $1.147M, EBITDA is $167K, payroll rises to $504K, and marketing is $60K.

Revenue reaches $2.519M, EBITDA is $529K, payroll is $1.074M, and marketing is $95K.

Cost drivers

Fleet build

$388K payroll

$45K marketing

19.5% variable costs

Month 9 breakeven

Higher contract mix

$504K payroll

$60K marketing

18.5% variable costs

larger account load

More crews

$1.074M payroll

$95K marketing

15.5% variable costs

larger contract density

Owner income rangeBefore owner reserves

Limited drawLow draw

Modest drawBase draw

Strong drawHigh draw

Best fit

Use this to stress-test launch cash and a year-one draw pause.

Use this as the core plan for a steady operating year after breakeven.

Use this to test upside if contract density stays high and staffing scales cleanly.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model shows no safe profit draw in Year 1 because EBITDA is -$142K on $571K revenue By Year 2, EBITDA reaches $167K, and by Year 5 it reaches $529K on $2519M revenue If the owner fills the Director of Operations role, the model also includes $115K of annual compensation for that function

This model reaches breakeven in Month 9, with the lowest cash point in Month 8 The minimum cash need is $489K, driven by payroll, equipment, marketing, and fixed overhead before contracts fully scale Payback takes 49 months, so early cash discipline matters more than headline revenue

You may need licenses when services include regulated pesticide, herbicide, or chemical applications Requirements vary by state, county, and service type, so check local rules before selling weed control, pest monitoring, or similar work Licensing can affect staffing, pricing, insurance, and the timing of higher-value turfgrass maintenance services

The biggest profit levers are contracted field volume, contract pricing, service mix, crew productivity, equipment utilization, and retention In the model, variable costs improve from 195% of revenue in Year 1 to 155% in Year 5 Payroll still grows from $388K to $1074M, so labor planning is the swing factor

A balanced start is safer than relying on one client type The model begins with athletic field management at 400%, premium landscape subscriptions at 350%, and seasonal enhancement services at 200% in Year 1 Athletic contracts support recurring revenue, while seasonal enhancements can lift ticket size when crews and equipment are already scheduled

About the author

Adam Fletcher

Small Business Writer

Adam Fletcher is a small business writer at Financial Models Lab who researches how small businesses launch, operate, and earn money. He focuses on business affordability analysis and helps readers evaluate business ideas with a practical eye, especially when planning a business with limited capital. His work connects new ventures to realistic startup budgets in a clear, plain-spoken way for people starting out with less money.

Choosing a selection results in a full page refresh.