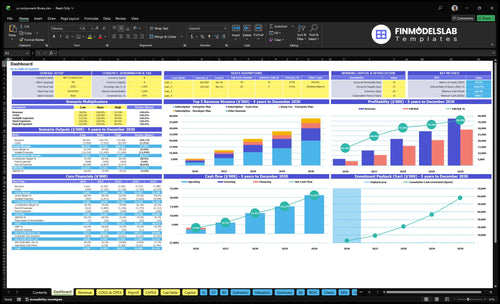

How Much UI Component Library Owners Make: $150K Salary Plus Profit

You’re estimating owner income, not an employee salary survey or a tax distribution plan This model shows a $150,000 annual owner salary, Year 1 revenue of $5441 million, and Year 1 EBITDA of $3540 million These are planning assumptions for a US software owner and exclude personal taxes, financing, and guaranteed distributions

Owner income$150kNet margin65%-76%Revenue for target pay$230kBusiness difficultyEasy

What could you pay yourself?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It uses the model’s Year 1, Year 3, and Year 5 inputs to map revenue to contribution, EBITDA, reserves, and owner pay capacity.

Which six drivers matter most?

1

Recurring Revenue

$5.4M-$38.0M

Recurring subscriptions are the base engine: revenue climbs from $5.441M in Year 1 to $37.985M in Year 5, and EBITDA rises from $3.540M to $28.987M.

2

Pricing Mix

$29-$1.5K

Moving mix from the $29 developer plan to the $149 team plan and $999 enterprise plan lifts average revenue per account without adding the same number of users.

3

Retention

5.0%-7.0%

Churn is not modeled, so the 5.0% to 7.0% trial-to-paid rate is the closest gate on how much of the top of the funnel turns into recurring income.

4

Enterprise Sales

5%-15%

Enterprise share rises from 5.0% to 15.0%, and each deal adds a $2,500 to $3,500 setup fee plus higher monthly seats.

5

Dev Cost

$530K-$1.55M

The CEO line is $150K, and the product build team is the biggest fixed drag, with annual wages rising from about $530K to $1.55M as FTEs scale.

6

Support Load

3.0%-1.5%

Support tools take 3.0% of revenue in Year 1 and 1.5% by Years 4 and 5, so lower ticket load protects margin as sales grow.

Can you pressure-test owner pay in the UI Component Library Development model?

Can a solo founder make money with a UI component library?

For UI Component Library Development, a true solo founder can make money only if lower payroll does not slow feature velocity, compatibility work, documentation, design QA, or support. The Year 1 plan is not solo: it uses one owner, two senior frontend engineers, and one UI/UX (user interface and user experience) designer, with $530,000 in payroll, including $150,000 to the owner and $380,000 to nonowner staff. That means 72% of Year 1 labor sits outside the founder, so the savings from going solo help only if conversion, retention, and enterprise sales stay strong.

Year 1 mix

One owner, two engineers, one designer

$530,000 total payroll

$150,000 owner pay

$380,000 nonowner payroll

Solo tradeoff

Founder absorbs support load

Founder covers design QA

Compatibility work slows solo output

Slower delivery can hurt sales

How much revenue does a UI component library need to pay the owner?

UI Component Library Development needs about $186,000 in annual revenue to pay a $150,000 owner salary, based on a 80.5% Year 1 contribution margin; here’s the quick math: $150,000 / 0.805 = $186,335. For the full plan, How Much Does It Cost To Launch UI Component Library Development Business? needs about $942,000 per year, or $78,500 per month, before taxes and distributions.

Owner pay math

Target owner salary: $150,000/year

Contribution margin: 80.5%

Salary-only revenue: about $186,000/year

Monthly salary coverage: about $15,500/month

Full plan target

Nonowner payroll: $380,000/year

Fixed overhead: $108,000/year

Marketing budget: $120,000/year

Minimum cash reserve: $885,000

How does scaling affect UI component library owner income?

Scaling can raise owner income in UI Component Library Development when recurring revenue grows faster than support, payroll, and marketing. In the model, revenue rises from $5,441 million in Year 1 to $37,985 million in Year 5, while EBITDA margin improves from 651% to 763%; enterprise pricing also moves from $999 to $1,499 per month, with setup fees from $2,500 to $3,500.

Income lift

Revenue climbs hard with scale

Enterprise price rises to $1,499

Setup fees rise to $3,500

Margin expands as costs lag

Risk check

Churn is not provided

Test churn as a separate input

Enterprise sales add procurement work

Support and security costs rise too

Key Takeaways

Recurring revenue funds payroll, support, and owner pay.

Higher enterprise mix lifts revenue, but adds complexity.

Churn must stay low to protect monthly recurring revenue.

Support load can cap distributions if docs lag.

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income is anchored by a $150,000 salary, while revenue scale and margin improve room for cash flow and upside. Early ramp, scaled subscriptions, and enterprise mix drive the spread.

Comparison of early, modeled, and mature owner income cases.

Scenario

Low CaseEarly ramp

Base CaseModeled scale

High CaseMature scale

Launch model

This is the early-ramp case: Year 1 revenue is $5.441 million and EBITDA is $3.540 million.

This is the modeled case: Year 3 revenue reaches $21.505 million and EBITDA reaches $15.747 million.

This is the mature case: Year 5 revenue reaches $37.985 million and EBITDA reaches $28.987 million.

Typical setup

Year 1 stays developer-led, with 70% Developer Plan, 25% Team Plan, and 5% Enterprise Plan at $29, $149, and $999 monthly prices.

Year 3 runs a scaled subscription base with 60% Developer Plan, 30% Team Plan, and 10% Enterprise Plan at $35, $169, and $1,199 monthly prices.

Year 5 reflects the strongest mix, with 50% Developer Plan, 35% Team Plan, and 15% Enterprise Plan at $39, $199, and $1,499 monthly prices.

Cost drivers

12.0% trial starts

5.0% trial-to-paid

70% Developer mix

8.0% hosting cost

5.0% sales commission

15.0% trial starts

6.0% trial-to-paid

60% Developer mix

10% Enterprise mix

7.0% sales commission

18.0% trial starts

7.0% trial-to-paid

15% Enterprise mix

4.5% hosting cost

7.0% sales commission

Owner income rangeBefore owner reserves

$150,000Salary floor

$150,000Modeled salary

$150,000Upside salary

Best fit

Use this to stress-test early traction and slower enterprise uptake.

Use this as the main planning case for steady subscription growth.

Use this to test enterprise-led scale and hiring pressure.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

UI Component Library Development Core Six Income Drivers

Recurring Revenue

Stable Recurring Revenue

Recurring revenue here means subscription cash from developers, teams, and enterprise buyers. It matters because MRR (monthly recurring revenue) funds payroll, support, marketing, and reserves before the owner gets paid. Average monthly revenue is about $453,000 in Year 1 and $3.165 million in Year 5, so the pay pool gets safer as the base grows.

Here’s the quick math: once payroll and service costs are covered, more of EBITDA (earnings before interest, taxes, depreciation, and amortization) can become owner distribution. Stable MRR protects the $150,000 owner salary. If churn rises or support load climbs, cash gets pulled back into replacement sales and service work, and owner pay stays trapped in the business.

Track Churn and Support Load

Measure active subscribers, plan mix, average monthly price, churn, support hours, and reinvestment needs. A subscription base that grows from $453,000 to $3.165 million a month only lifts take-home pay if cancellations stay low and service costs do not outrun revenue. One clean rule: subscription cash has to cover the people who keep the product current.

Count paid seats every month.

Watch churn by plan.

Measure tickets per customer.

Price support-heavy accounts higher.

Forecast payroll before owner draw.

Maintenance And Development Cost

Maintenance Cost Pressure

Framework updates, accessibility fixes, documentation, and design QA are the hidden payroll drain in a UI component library. Here, senior frontend engineering FTEs rise from 20 in Year 1 to 60 in Year 5, and payroll climbs from $530,000 to $1.625 million. That is about $1.095 million more cash locked into upkeep, so less stays available for owner pay.

This is the payroll line that quietly eats profit. Product quality can protect retention, but if staffing outruns the revenue base, the owner funds polish before the business can afford it and EBITDA gets squeezed.

Control Engineering Spend

Model this cost from engineering hours, FTE count, and the share of time spent on upkeep versus new features. Here’s the quick math: $530,000 in Year 1 versus $1.625 million in Year 5 is roughly 3.1x payroll growth, so every extra rework cycle hits owner take-home fast.

Track update, docs, QA hours.

Cap FTE growth to demand.

Test whether fixes reduce churn.

Delay new builds until revenue needs them.

Track the backlog for compatibility work, WCAG fixes, and docs debt each month. If those jobs keep rising faster than recurring revenue, pause overbuilding and push the team back to the releases that protect retention and cash flow.

Support Burden

Support Burden

Support burden is the cash cost and founder time tied up in tickets, onboarding, and custom help. In this model, support ticketing and tools are 30% of revenue in Year 1 and 15% in Year 5, so weak docs can turn subscription sales into service work instead of profit. If the owner is answering product questions, less time and cash are left for growth and take-home pay.

The main inputs are monthly revenue, ticket volume, hours per ticket, enterprise mix, and whether help is included or billed. Support-heavy enterprise accounts can protect revenue, but if custom help becomes unpaid services work, margin drops and owner income gets squeezed even when bookings look strong.

Cut Repeat Tickets

Track tickets per active account, first-response time, and founder or engineer hours spent on support. Then fix the top repeat issues in docs and onboarding. Better docs cut the same setup and integration questions, which lowers support cost and keeps more revenue as profit instead of payroll-like work.

Measure tickets by customer tier.

Separate paid and free help.

Track founder support hours monthly.

Update docs after every release.

If support keeps rising with revenue, the business grows busier but not healthier. The goal is simple: add customers without adding a ticket load that eats owner pay.

Retention And Churn

Retention And Churn

Churn rate is a required input here because it decides how much MRR sticks. With subscription software, every cancellation forces the owner to replace lost revenue, even if CAC is only $15 in Year 1 and $25 in Year 5. Lower churn protects cash flow, keeps support load steadier, and makes the $150,000 owner salary safer.

For this business, retention depends on compatibility updates, documentation quality, support speed, and developer trust. If churn rises, the team has to spend more on marketing and service just to stay flat, and that cuts the cash left for profit and owner pay. The key inputs are active customers, renewals, cancellations, MRR, and CAC.

Measure Churn Before It Hits Pay

Track logo churn, revenue churn, and renewal dates by plan. Then tie each loss to the cause: framework breakage, missing docs, slow replies, or poor trust. That shows which fix protects the most MRR. One clean metric: net MRR retained after cancellations and expansions.

Review cancellations weekly.

Tag every loss by cause.

Fix docs before adding features.

Update compatibility on release day.

Shorten support response times.

Here’s the quick math: lower churn means fewer replacements, so the same revenue needs less paid acquisition and less founder firefighting. That improves margin and makes profit more predictable. If onboarding takes too long or updates break integrations, churn rises fast and owner draw gets less stable.

Enterprise And Team Sales

Enterprise and Team Mix

This driver is the share of revenue from Enterprise and Team licenses versus lower-priced developer plans. Enterprise pricing is much higher, so even a small mix shift can lift revenue per account and EBITDA. Here, Enterprise mix moves from 50% in Year 1 to 150% in Year 5, while Team mix rises from 250% to 350%, supporting EBITDA growth from $3,540 million to $28,987 million.

What this hides is the extra cost of procurement, security reviews, support expectations, contract terms, and sales commissions. If those costs outrun the price lift, owner pay can lag even when revenue grows. Bigger deals help most when the service work stays tight and the contract stays recurring.

Track Deal Economics by Plan

Measure enterprise share, team share, average contract value, commission rate, and support hours per account. A larger deal only improves owner income if annual value clears onboarding, legal redlines, and support time. If a contract needs heavy custom work, price it before you close.

Track revenue by plan type

Price onboarding and redlines

Cap unpaid support hours

Watch commission as % of ARR

Keep pushing mix toward higher-value accounts, but watch cash timing too. Enterprise contracts can lift EBITDA while slowing collections, so the owner still needs enough recurring cash to cover payroll and support load.

Pricing And Packaging

Plan Mix and Price Ladder

If most customers stay on $29 Developer, revenue per account stays thin. Moving mix toward $149 Team and $999 Enterprise lifts revenue before any cost change. By Year 5, prices rise to $39, $199, and $1,499, and Enterprise adds a one-time fee that grows from $2,500 to $3,500. The catch is sales calls, onboarding, support, and custom terms.

What this driver includes is plan mix, monthly price, and one-time fees. More higher-value accounts can improve owner pay, but only if service work stays controlled. If Enterprise needs too much custom help, the extra revenue gets absorbed by payroll and support instead of profit.

Track Mix, Fees, and Service Load

Measure customers by plan, upgrade rate, setup-fee collection, and support effort per account. Price new deals first, then compare revenue per customer and margin by tier. If Enterprise needs extra onboarding or custom terms, make sure the setup fee covers that work.

Count customers by plan.

Track upgrade and downgrade rates.

Log setup fees collected.

Watch support and custom-term load.

The simple rule is to keep the price ladder clear. If Team and Enterprise bring more revenue but also slow sales or pull engineers into service, owner income can fall. Protect margin by limiting custom terms to accounts that justify the load.