Owner income$1.78M

Owner income$1.78MHow Much VA Claim Assistance Owners Make: $1661M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.78M  Net margin56.8% → 72.1%

Net margin56.8% → 72.1% Revenue for target pay$2.93M

Revenue for target pay$2.93M Business difficultyMedium

Business difficultyMedium

You’re planning a VA disability claim assistance business where owner income depends on collected revenue, staffing, compliance costs, and reserves In the researched first-year model, revenue is $2925M with $1661M EBITDA, before taxes, debt service, reinvestment, or owner distributions The five-year model covers revenue, gross margin, operating expenses, payroll, marketing, cash needs, and target-pay planning in the US market

Owner income$1.78MNet margin56.8% → 72.1%Revenue for target pay$2.93MBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and your pay goal.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Cash collected is not profit, and profit is not take-home.

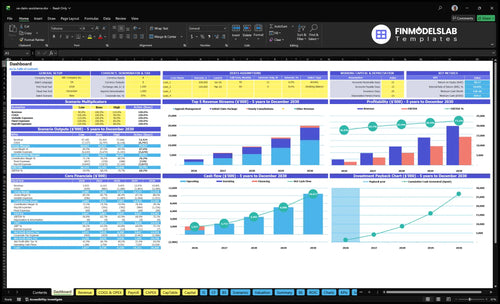

Can you check owner income in the financial model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the VA Disability Claim Assistance Financial Model Template. Open the model.

Owner-income model highlights

- $2.925M revenue, $1.661M EBITDA

- Month 2 cash need: $834,000

- Month 3 breakeven

- Month 4 payback

- Low, base, high scenarios

How many VA claim clients do you need to make a living?

You can’t size VA Disability Claim Assistance by lead count alone; you size it by collected revenue per paid matter after direct costs. Here’s the quick math: Year 1 direct costs are 150% and variable fees are 120%, so 730% remains before marketing, payroll, fixed costs, taxes, and reserves; fixed overhead is $5,650/month, payroll is $313,000, and marketing is $45,000. If the owner also fills the Lead Claims Consultant seat, the salary benchmark is $115,000.

What sets the client count

- Use collected revenue, not leads.

- Count paid matters, then subtract costs.

- Direct costs hit 150%.

- Variable fees hit 120%.

Year 1 cost load

- Fixed overhead is $5,650/month.

- Payroll totals $313,000.

- Marketing budget is $45,000.

- Owner pay benchmark is $115,000.

Can a VA claim assistance business scale?

Yes, VA Disability Claim Assistance can scale, but only if it moves beyond a solo founder model. A solo setup caps throughput because one person has to manage intake, evidence, and follow-up, while a team model adds capacity without breaking quality. By Year 5, the staffing mix can expand to 50 senior case manager FTE, 20 medical evidence coordinator FTE, and 30 intake/admin FTE, but trust, documentation quality, and compliance control set the real ceiling.

Small team model

- Owner-led work caps throughput.

- Add case managers for follow-up.

- Use evidence coordination to reduce errors.

- Use intake support to keep files moving.

Agency-style model

- Build outreach only with controls.

- Layer reviews to protect quality.

- Watch payroll growth closely.

- Keep compliance tight as headcount rises.

What costs reduce VA disability claim assistance profit margin?

The biggest profit-margin hits in VA Disability Claim Assistance are labor, case-level direct costs, and marketing; see What Are Operating Costs For VA Disability Claim Assistance? for the cost map. In Year 1, direct case costs equal 150% of revenue and variable expenses equal 120%, so pricing has to cover a lot before profit shows up. The biggest swing comes from labor efficiency, paid case mix, and CAC moving from $150 to $130.

Main cost drivers

- Medical examiner nexus fees raise case cost.

- Records retrieval adds direct spend.

- Secure CRM and portal fees stack up.

- Referral commissions cut take-home margin.

Overhead pressure

- Marketing rises from $45,000 to $140,000.

- Wages are $313,000 in Year 1.

- Wages reach $889,000 by Year 5.

- Fixed overhead is $67,800 per year.

Want the six income drivers?

1

$45KLead Flow

A $45K Year 1 budget at $150 CAC decides how many veterans enter the pipeline and whether revenue reaches the $2.925M plan.

2

2.8hClient Close

Each active customer averages 2.8 billable hours a month in Year 1, so better consult close rates lift revenue without adding as much headcount.

3

45%Appeals Mix

Appeals rise to 45% of the mix by Year 5, and that shift pushes more billed hours and fee value into the owner's pocket.

4

20hCase Throughput

Appeals take 20 to 25 billable hours, so faster file turnaround lets the same team carry more cases before capacity hits.

5

56.8%Labor Efficiency

With $313K of Year 1 payroll and a $45K marketing budget, margin discipline decides how much revenue turns into owner cash.

6

$834KCash Buffer

The model needs $834K minimum cash and only breaks even in Month 3, so tight reinvestment protects equity early on.

VA Disability Claim Assistance Core Six Income Drivers

Qualified Lead Flow

Qualified Veteran Leads

Qualified lead flow is the top of the funnel: how many eligible veterans book and show for consults. Here’s the quick math: $45,000 / $150 CAC = 300 acquired clients from that channel in Year 1. More qualified leads fill consultation capacity and raise paid matters, but only if intake can screen fast and the team can handle the added review work.

The risk is cheap traffic that looks busy but does not sign. Low-quality leads still consume intake time, and that can push payroll up without adding revenue. By Year 5, marketing rises to $140,000 and CAC improves to $130, so the same spend buys more efficient growth if lead quality stays high.

Track Quality, Not Just Volume

Measure qualified leads, consultation show rate, and signed matter rate together. A lead only helps income if it is eligible, responds, and moves through evidence review. If intake hours rise faster than signed cases, the funnel is leaking and owner pay will not keep up with marketing spend.

Use compliant, trust-based acquisition and test which sources produce the best conversion at the lowest CAC. One clean metric is qualified leads per $1,000. When that improves, you get more consultations without the same payroll load, so margin and owner distributions improve.

1

Consultation-To-Client Conversion

Consultation-to-Client Conversion

This is the share of consultations that turn into paid matters. It covers intake screening, clear engagement terms, meaning what the client is hiring you for and when payment starts, and plain timing expectations. When the team filters for eligibility and documents the scope well, more consult time becomes collected revenue, and less time gets burned on non-fit cases against the $5,650 monthly fixed overhead.

Track lead-to-consultation rate, consultation-to-client rate, paid case rate, no-show rate, and intake hours per signed matter. The risk is pressure selling or weak notes. That can lift short-term closes but hurt trust and case quality. Better conversion raises revenue per marketing dollar and protects owner pay because the same overhead is spread across more signed work.

Improve the Close Rate

Use a simple intake script: check eligibility, explain the engagement, and state timing in plain words. If no-shows are high, tighten reminders and booking windows. If consults are not closing, review whether prospects were screened too loosely or the next step was unclear.

- Count booked, attended, signed.

- Log no-shows by source.

- Measure hours per signed matter.

- Document why prospects were declined.

A cleaner process reduces wasted case review time and keeps more of each marketing dollar tied to paid work. What this hides: if the team spends too long on weak leads, intake becomes a cost center, not a profit driver.

2

Paid Case Mix And Collected Fee Value

Paid Case Mix Value

This driver is the blend of paid work across initial claim packages, appeals management, and hourly consultations. Using the stated hours and rates, a package is $1,500 (12 x $125), an appeal is $3,000 (20 x $150), and a consultation is $200 (2 x $100). Treat the mix as an assumption, not fee advice.

If Year 1 mix is 45%/30%/25% and Year 5 shifts to 35%/45%/20%, weighted revenue per paid matter rises from about $1,625 to $1,915, or 17.8%. Appeals lift collected value, but they also bring more review work and slower timing, so owner pay depends on cash collection speed as much as billable hours.

Track Mix by Matter Type

Measure three inputs every month: matter type share, hours billed per matter, and collected dollars per matter. A simple formula is (share x fee value) across the mix. That tells you whether the business is earning more because of better case mix or just more low-value consult volume.

- Track paid matters by service type

- Watch billed hours per case

- Compare collected fee per matter

- Flag slower appeal collections

Push more appeal work only if review time, staff capacity, and cash timing can hold. If appeals rise but unbilled admin time also rises, gross margin and owner draw can slip even when top-line revenue looks better.

3

Case Resolution Throughput

Case Resolution Throughput

Throughput is how many cases get reviewed, documented, filed, followed up, and resolved without quality slips. If one active customer moves from 28 billable hours a month in Year 1 to 35 in Year 5, that is a 25% lift in revenue work per case. It helps owner income only when the extra hours are collected, not trapped in rework.

The main leak is backlog. Missed follow-up, slow client replies, or weak evidence handling can stretch cycle time and delay cash. Clean case flow turns active files into collected revenue faster, which supports better gross margin, steadier cash flow, and a more reliable owner draw.

Tighten Case Flow

Track the few numbers that show whether cases are moving: open cases per manager, days to first follow-up, documents still missing, and billable hours per active customer. Here’s the quick test: if cases age while hours stay flat, you have a workflow problem, not a demand problem.

- Set follow-up deadlines in writing.

- Assign one owner per case.

- Use secure records from day one.

- Escalate stalled client responses fast.

4

Labor And Marketing Efficiency

Labor and Marketing Efficiency

Labor and marketing efficiency is how much revenue is left after payroll, CAC, marketing, software, referrals, and fixed overhead. In Year 1, payroll is $313,000, marketing is $45,000, CAC is $150, and fixed overhead is $67,800, so weak conversion or heavy rework can wipe out owner pay fast. One clean rule: if revenue per client does not outrun labor, margin gets squeezed.

By Year 5, payroll rises to $889,000 and marketing to $140,000, while direct and variable percentages improve from 270% to 210%. That means efficiency matters more as volume grows. Protect quality and compliance costs, but cut idle intake time, poor-fit leads, and repeat work. If each case needs less cleanup, more cash can reach the owner.

Track Cos t per Signed Case

Measure cost per signed case, intake hours per matter, and no-show rate. Here’s the quick math: CAC = marketing spend ÷ acquired customers, so a $150 CAC only works if the client’s billable hours cover payroll and overhead. Keep the team busy with qualified veterans, not broad traffic that never converts.

- Cut rework before hiring more.

- Filter leads before intake time.

- Protect compliance and quality costs.

Watch the gap between payroll growth and billable output. If payroll climbs toward $889,000 by Year 5, the owner’s draw depends on tighter scheduling, fewer dead-end reviews, and faster handoff from intake to paid work. The goal is simple: keep revenue quality high enough that fixed overhead and labor don’t swallow the margin.

5

Cash Reserves And Owner Distributions

Cash Reserves Control Owner Pay

Cash flow, not EBITDA, decides when the owner can take money home. In this model, the business needs at least $834,000 cash in Month 2, reaches breakeven in Month 3, and pays back in Month 4, because claim work and collections can lag the work already done.

Reserves have to cover payroll, marketing, compliance, and case timing gaps. EBITDA is profit before interest, taxes, depreciation, and amortization, so it can look healthy while cash is still tight. If reserves run thin, owner distributions get delayed or cut, even when active cases are building.

Build a Reserve Floor Before Drawing Profit

Track monthly cash balance, days of cash on hand, collections lag, and owner draw coverage. The key inputs are active client volume, billable hours, payroll, marketing spend, compliance costs, and the timing of receipts. If collections slip behind workload, cash should stay in the business instead of moving to owner pay.

- Hold cash through Month 2.

- Test draws after breakeven.

- Map payroll and fee timing.

- Block draws below reserve floor.

6

Compare low, base, and high VA claim assistance owner income scenarios

Owner income scenarios

Income swings with lead flow, conversion, case mix, staffing, and cash timing. Base tracks the modeled first-year run rate; high reflects Year 5 scale and tighter CAC.

| Scenario | Low CaseDownside case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | Lower earnings path with slower lead flow, weaker close rates, and more cash tied up before collections land. | Modeled earnings path using the first-year run rate from the financial model. | Stronger earnings path with Year 5 scale, better CAC, and a larger case mix. |

| Typical setup | The shop stays small, depends on paid leads with CAC above the modeled $150, and carries a lean team while reserves stay higher. | This case uses $2.925M revenue, $1.661M EBITDA, 56.8% EBITDA margin, $45,000 marketing, $150 CAC, $313,000 payroll, and $5,650 monthly overhead. | This case reflects $19.905M revenue, $14.361M EBITDA, 72.1% EBITDA margin, $140,000 marketing, $130 CAC, and a bigger staff model. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Lower 7-figure take-homeDownside band | Around $1.7M take-homeModeled band | Around $14.4M take-homeUpside band |

| Best fit | Use this to stress-test cash burn, intake delays, and a weak referral funnel. | Use this as the planning base for hiring, cash, and owner draws. | Use this to test upside capacity, hiring pace, and reserve discipline. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- VA Disability Claim Assistance Porter's Five Forces Analysis

- VA Disability Claim Assistance BCG Matrix

- VA Disability Claim Assistance Business Model Canvas

- What Are The Five KPIs For VA Disability Claim Assistance Business?

- VA Disability Claim Assistance Business Plan Template in Pre-Written Word

- How Increase Profits With VA Disability Claim Assistance?

- What Are Operating Costs For VA Disability Claim Assistance?

- VA Disability Claim Assistance Startup Costs: $834K Cash Need

- VA Disability Claim Assistance Financial Model Template in Excel

- How To Start A VA Disability Claim Assistance Business With A 3-Month Breakeven Plan

- How To Write A Business Plan For VA Disability Claim Assistance?

- VA Disability Claim Assistance Marketing Mix

- VA Disability Claim Assistance Marketing Plan

- VA Disability Claim Assistance Business Proposal

- VA Disability Claim Assistance PESTEL Analysis

- VA Disability Claim Assistance Pitch Deck Example Editable PPTX

- VA Disability Claim Assistance Business SWOT Analysis

- VA Disability Claim Assistance Value Proposition Canvas

Frequently Asked Questions

In the researched base model, Year 1 revenue is $2925M and EBITDA is $1661M, before taxes, reserves, debt service, or distributions The model also includes a $115,000 Lead Claims Consultant salary Actual owner take-home depends on whether the owner takes salary, distributions, or both