How Much Vendor Management Owners Make: $150K Pay, Month 30 Breakeven

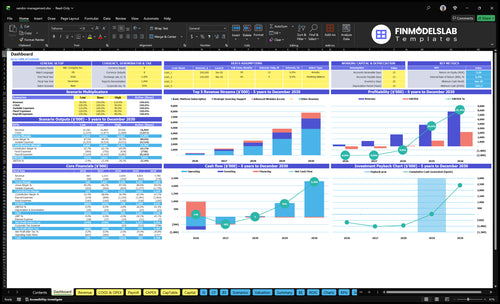

A vendor management business owner can plan around a modeled $150,000 annual founder salary in this case, but distributions should not be assumed early The researched plan shows Year 1 EBITDA of -$603,000, a minimum cash position of -$503,000 in Month 30, and breakeven in Month 30 Revenue per active customer is about $639/month in Year 1 and rises to about $1,410/month by Year 5 based on the provided service mix Owner take-home comes after delivery costs, software, sales commissions, payroll, overhead, reserves, and any tax planning

Owner income$150KNet margin-918% to 54%Revenue for target pay$909KBusiness difficultyHard

Want to test your vendor management owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How does the vendor management pricing model affect owner income?

Vendor Management owner income is driven mostly by recurring retainers, not one-time work. With $499 basic, $299 advanced, and $1,500 strategic support in Year 1, at 80%, 30%, and 10% attach rates, the mix produces about $639 per active customer each month; by Year 5, the same model rises to about $1,410 a month with $600, $360, and $1,900 pricing and 95%, 75%, and 30% attach rates. Recurring fees make income more predictable, while project work and savings-based fees can lift earnings but need extra labor and proof; no separate onboarding revenue is given, so don’t count it as steady income.

Recurring income

$639 monthly in Year 1

$1,410 monthly by Year 5

Retainers improve cash predictability

Higher attach rates lift owner income

Upside and risk

Project work adds one-time revenue

Savings fees need proof and tracking

Labor rises with custom support

Do not count onboarding as steady income

How does scaling a vendor management business change owner income?

If you pay the owner $150K from Month 1, Vendor Management is still funding that pay before it is profit-funded, because Year 1 EBITDA is -$603K. As it scales, the owner moves from delivery into sales, account oversight, hiring, reporting quality, and systems, while wages rise from about $500K in Year 1 to $1.425M in Year 5. Owner distributions should wait for breakeven, reserve coverage, and payback, not just revenue growth.

Owner pay

$150K starts in Month 1

-$603K Year 1 EBITDA

Year 1 wages are about $500K

Pay is not profit yet

Scaling risks

Client concentration can squeeze cash

Weak renewals hit owner income

Poor supplier reporting hurts trust

Staffing reaches $1.425M by Year 5

How many clients does a vendor management business need to pay the owner?

Average revenue per active client rises from $639 a month in Year 1 to $1,410 in Year 5, so each account adds more owner take-home.

2

Contract Retention

$1.5K-$800

Longer client life spreads CAC from $1,500 in Year 1 to $800 in Year 5, which protects payback and cash flow.

3

Delivery Efficiency

6%-4%

Direct expert delivery cost falls from 6% to 4% of revenue, so more sales drop to gross profit.

4

Project Fees

3%-2%

Setup and training cost falls from 3% to 2%, so charging project fees can cover early work and lift margin.

5

Strategic Support

$1.5K-$1.9K

Strategic sourcing support climbs from $1,500 to $1,900 a month, adding the highest-value upsell per client.

6

Overhead Discipline

$800K-$2.6M

Payroll, fixed costs, and marketing start near $800K a year and rise to about $2.6M, so spend control decides owner cash.

Vendor Management Core Six Income Drivers

Average Revenue Per Managed Client

Average Revenue Per Managed Client

This driver is the monthly revenue earned per active customer. At the stated mix, it is about $639/month in Year 1 from $499 basic, $299 advanced, and $1,500 strategic support with 80%, 30%, and 10% attach rates. If scope stays flat, higher revenue flows into owner pay; if service work grows faster, it turns into payroll pressure.

By Year 5, weighted revenue rises to about $1,410/month as prices and attach rates increase. That is the real test: price has to move with supplier count, reporting cadence, issue volume, compliance work, and service level risk. One complex account can look good on revenue but still hurt cash if it needs too much expert time.

Price for scope, not just seats

Track the inputs that drive service load: supplier count, reporting cadence, issue volume, compliance work, and service level risk. Here’s the quick math: if price rises but support hours rise faster, gross margin gets squeezed and owner income falls.

Use tiered pricing tied to complexity, and review each account’s margin monthly. If a client needs more manual work than the plan covers, reprice it or reduce scope before it starts draining delivery labor. Underpricing complex accounts turns revenue growth into payroll pressure.

Measure hours per account monthly

Flag high-complexity clients early

Reprice when scope expands

1

Recurring Contracts And Retention

Recurring Contracts And Retention

Retention is what turns vendor management subscriptions into owner cash. With $1,500 CAC in Year 1 and about $457/client/month contribution before fixed overhead, the model only works if clients stay long enough to cover acquisition and service work; the stated payback is about 33 months before overhead allocation.

This driver includes renewal rate, churn, contract term, and monthly contribution after delivery labor, support, and payment work. If churn rises, the firm buys the same revenue again, marketing spend climbs, and breakeven can slip beyond Month 30.

Protect Renewal Revenue

Track renewal rate, gross churn, and client contribution per month by cohort. Then separate accounts by support load, since clients that need more reporting, compliance help, or issue handling are usually the first to leave if value is not obvious.

Renewal rate by client cohort

Churn after 90 days

Contribution per active client

Reporting completion each month

Keep renewals tied to proof: vendor performance results, compliance support, and clear relationship management notes. One clean rule: if clients cannot see savings, risk reduction, or time saved each month, retention weakens and owner pay gets squeezed.

2

Delivery Labor Efficiency

Delivery Labor Efficiency

Delivery labor is the expert time used for supplier onboarding, issue resolution, compliance checks, reporting cadence, contractor coordination, and stakeholder meetings. In Year 1, direct expert service delivery is 6% of revenue; by Year 5 it falls to 4%. That helps owner income only if account growth outpaces staffing, because labor stays lean while recurring revenue scales.

Here’s the quick math: for every $1,000,000 of revenue, direct delivery labor is about $60,000 in Year 1 and $40,000 by Year 5. If the team adds people before account capacity is proven, payroll rises faster than gross margin, and owner draw gets squeezed.

Track capacity before adding headcount

Measure workload per active account: onboarding hours, open issues, compliance checks, reporting cycles, and meeting load. The model grows procurement expert staffing from 10 FTE at $110K to 30 FTE, and customer success from 0 to 30 FTE at $75K each, so the key test is whether one FTE can hold margin steady.

Set hiring gates on managed accounts, not hope. If labor per client rises faster than revenue per client, service margin falls and cash available for owner pay shrinks. Keep a simple ratio: labor cost as a share of revenue, plus accounts per expert, plus issue volume per month.

3

Onboarding, Implementation, And Project Fees

Price Setup Work Up Front

Upfront setup fees help cash flow only when they cover the work. The model carries customer success onboarding and training at 3% of revenue in Year 1, easing to 2% by Year 5. If you do supplier data cleanup, workflow setup, compliance files, and reporting dashboards for free, that cost hits margin and slows owner pay.

Because there is no separate onboarding revenue line, steady-state income should not count it unless you add it. So the real test is cash: free implementation delays owner distributions and turns project work into a subsidy for the client.

Track Setup Hours Before You Quote

Track setup hours, scope, and fee by client. Price the project so it covers vendor count, data cleanup, compliance work, and dashboard builds, then keep the recurring plan for ongoing support. That protects gross margin and makes owner profit easier to forecast.

Setup hours per client

Fee versus labor cost

Scope creep on dashboards

Unbilled compliance tasks

4

Spend-Based Or Savings-Based Upside

Spend-Linked Upside

Larger supplier spend can raise owner income only when the fee is tied to strategic sourcing support or measured savings. The closest priced upside here is $1,500/month in Year 1 and $1,900/month in Year 5, with attach rate rising from 10% to 30%. That helps revenue, but only the accounts that buy the service add real cash flow.

Savings-based fees are variable upside, not guaranteed recurring income. They need a clean baseline, client approval, negotiation work, and proof that the savings came from the work. If the data is weak or the client pushes back, the fee lands later or not at all, so owner pay should not depend on it.

Bill Only What You Can Prove

Track managed spend, attach rate, and documented savings by client. Managed spend means the dollars the team actively sources or negotiates on behalf of the client. If the baseline is messy, don’t forecast the savings fee as steady income. Treat it as upside tied to proof, not as core subscription revenue.

Log baseline costs before work starts

Get client sign-off on savings claims

Separate module fees from savings fees

Forecast only contracted strategic support

That keeps cash flow cleaner and protects margin, because the owner can see which dollars are recurring and which depend on one negotiation win.

5

Overhead, Software, And Sales Discipline

Fixed Overhead Discipline

$125K/month of fixed overhead comes out before the owner takes a draw. That includes rent, software, professional services, insurance, utilities, marketing tools, compliance, and admin supplies, so every client must cover more than service labor alone. If overhead stays fixed while revenue is still building, cash burn rises fast and owner pay gets pushed back.

Here’s the quick math: marketing spend rises from $150K in Year 1 to $1M in Year 5, while commissions fall from 8% to 6% and CAC drops from $1,500 to $800. That only helps if recurring revenue grows faster than the fixed base. If software and compliance costs scale with account needs, not vanity tools, the owner keeps more take-home.

Control Burn Before It Controls You

Track fixed overhead, CAC, commission rate, and software spend by active account each month. Tie tools and compliance work to actual vendor counts, service modules, and reporting load, not extra features. If a product line does not reduce work or protect margin, cut it. That keeps overhead aligned with the business, not with internal taste.

Watch the breakeven clock closely. With fixed costs this high, the risk is locking in cash burn before Month 30 breakeven. Push sales discipline hard: lower CAC toward $800, keep commissions near 6%, and raise marketing only when retention and margin are proven. Otherwise growth just buys more overhead.

6

Vendor Management Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high-growth owner-income scenarios

Owner income scenarios

Income stays thin until breakeven because wages, marketing, and support staff eat most early revenue. Stronger attach rates and more clients help, but distributions only make sense after reserves.

Shows when salary is safe and when distributions can start.

Scenario

Low CaseCash constrained

Base CaseBreakeven

High CaseDistribution-ready

Launch model

The business stays below breakeven, so owner pay is limited or paused.

The model tracks the plan and reaches Month 30 breakeven before any owner distributions.

The business grows faster, clears reserves, and adds owner pay through distributions after salary.

Typical setup

Active clients stay light, attach rates lag, CAC improves slowly, and fixed wages plus marketing keep EBITDA under pressure.

Year 1 client revenue runs about $639 per month per active customer, gross margin is about 85%, EBITDA is -$603K, and minimum cash reaches -$503K.

More active clients, stronger advanced and sourcing support attach rates, and lower CAC improve monthly cash, while added payroll supports the larger book.

Cost drivers

Fewer active clients

lower attach rates

slower CAC improvement

no distributions

Year 1 client revenue

85% gross margin

$500K wages

$150K marketing

Month 30 breakeven

More active clients

stronger attach rates

lower CAC

higher billable hours

distributions after reserves

Owner income rangeBefore owner reserves

Reduced salary onlyNo distributions

$150,000 salarySalary only

Salary plus distributionsAfter reserves

Best fit

Use this to stress test a slow launch and weak conversion.

Use this as the core planning case for salary and cash timing.

Use this for upside planning once cash reserves and payback are in place.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions.

In this researched plan, the owner has a modeled $150,000 annual founder salary That is not the same as profit distribution Year 1 EBITDA is -$603,000, breakeven is Month 30, and payback is Month 51, so extra owner take-home should wait until cash reserves are funded

The model reaches breakeven in Month 30 That matters because the minimum cash position also falls to -$503,000 in Month 30 Early owner pay may be possible as salary, but distributions are risky until client revenue, margins, payroll, and marketing spend cover the full operating base

Yes, recurring retainers make owner income easier to plan The model uses monthly revenue from a $499 basic service, $299 advanced access, and $1,500 strategic support in Year 1 The weighted revenue is about $639 per active customer per month before delivery costs, sales costs, payroll, overhead, and reserves

Payroll, marketing, and delivery workload drive the biggest pressure Year 1 wages are $500,000, marketing is $150,000, and fixed overhead is $12,500 per month Direct COGS equal 15% of revenue in Year 1, while sales commissions, payment fees, and onboarding add another 135%

Raise revenue per managed client without letting service scope sprawl Moving customers into advanced modules and strategic support lifts weighted revenue from about $639/month in Year 1 to about $1,410/month in Year 5 Keep delivery labor efficient, protect renewals, and delay distributions until after breakeven and reserves

About the author

Anthony Ross

Independent Business Researcher

Anthony Ross is an independent business researcher at Financial Models Lab who writes practical guides for first-time entrepreneurs planning their first business. Focused on small business money management, he helps readers organize broad business ideas into clear planning assumptions, with straightforward revenue and profit examples that make financial thinking easier to apply.

Choosing a selection results in a full page refresh.