Owner income$95K

Owner income$95KHow Much Venetian Plaster Business Owners Make: $95K Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$95K  Net margin32% to 63%

Net margin32% to 63% Revenue for target pay$293K

Revenue for target pay$293K Business difficultyHard

Business difficultyHard

You’re pricing skilled finish work, not selling generic labor hours This estimate uses a five-year US planning case with $907K Year 1 revenue, a $95K founder salary, EBITDA from $294K to $3711M, and owner pay before taxes, debt service, and personal benefits

Owner income$95KNet margin32% to 63%Revenue for target pay$293KBusiness difficultyHardWhat could your owner pay look like?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, labor, overhead, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

Want to test the full income model?

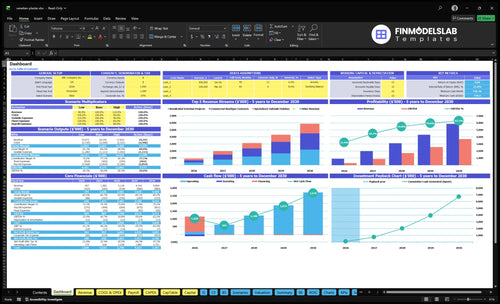

Open the Venetian Plaster Application Financial Model Template to see the dashboard screenshot with revenue, EBITDA, owner pay, cash runway, and breakeven.

Model tabs and key outputs

- $907K Year 1 revenue

- $294K Year 1 EBITDA

- $778K minimum cash

- Month 5 breakeven

- 11-month payback

- Assumptions and project mix

- Pricing, labor, and COGS

- Fixed costs and marketing

- Staffing, capex, cash flow

- Scenarios and distributions

Is a Venetian plaster business more profitable solo or with a crew?

Solo is usually more profitable early because it protects quality and keeps overhead light, but it caps owner income. A crew can raise revenue capacity fast, with Venetian Plaster Application growing from $907K in Year 1 to $5,869M in Year 5 as the owner shifts from installer to sales and project manager.

Solo keeps control

- Quality stays tight.

- Overhead stays low.

- Capacity stays capped.

- Owner income hits a ceiling.

Crew scales revenue

- Staff starts with 4 roles.

- Revenue can reach $5,869M.

- Owner moves to sales.

- Training and QC must hold.

What is a good profit margin for Venetian plaster?

A good profit margin for Venetian plaster application starts at the job level, not markup; researched direct costs are about 26% of revenue in Year 1 and 20% by Year 5, so contribution margin moves from 74% to 80%. For the cost detail, see What Are Venetian Plaster Application Operating Costs? Direct labor should be tracked separately from owner pay and fixed overhead, because underpriced rework cuts take-home fast.

Margin math

- 74% contribution in Year 1

- 80% contribution by Year 5

- Track direct labor on its own

- Keep owner pay out of job cost

Cost traps

- Lime plaster and pigments

- Primers, sealers, and abrasives

- Logistics, waste, and samples

- Scaffolding, prep time, and rework

How much should a Venetian plaster business owner pay themselves?

A Venetian Plaster Application owner should pay themselves the planned $95,000 annual Master Artisan and Founder salary from Month 1, or about $7,917 per month, then take extra owner draws only after job costs, overhead, reserves, taxes, capex, reinvestment, and working capital are covered; see How Much To Start Venetian Plaster Application Business? for the startup-cost context. Year 1 EBITDA, meaning earnings before interest, taxes, depreciation, and amortization, is $294,000, but that is not all distributable cash if slow collections tighten the bank balance.

Pay Rule

- Set salary at $95,000 per year

- Pay about $7,917 per month

- Separate salary from owner draws

- Draw only from true excess cash

Cash Guardrails

- Year 1 EBITDA is $294,000

- EBITDA is not owner cash

- Reserve for taxes and capex

- Protect cash if collections slow

What drives Venetian plaster owner income most?

1

10/moBooked Capacity

At about 10 Year 1 jobs a month, revenue reaches roughly $907K, which is the base that turns into owner pay before taxes.

2

$7.6KProject Value

The weighted Year 1 project value is $7,560, so even a small ticket lift pushes more cash to the owner with the same crew time.

3

74%-80%Premium Mix

Premium positioning keeps contribution margin in the 74% to 80% range before labor and overhead, and that is what funds owner take-home.

4

45-55hLabor Productivity

Raising billable hours per active customer from 45 to 55 spreads labor across more revenue, so each crew hour earns more for the owner.

5

20%-26%Direct Costs

Materials, logistics, waste, and abrasives sit near 20% to 26% of revenue, and every point saved drops straight into profit.

6

$778KOverhead Buffer

Monthly fixed overhead is $7,700, and the $778K Month 2 cash trough keeps owner draws tight until sales scale cleanly.

Venetian Plaster Application Core Six Income Drivers

Booked Install Capacity

Booked Install Capacity

Income rises when you book profitable install days without crowding prep, curing, travel, polishing, and punch-list time. The Year 1 plan implies about 120 projects a year, or 10 per month, from $907K revenue at $7,560 per project; by Year 5, volume rises to 482 projects, or 40 per month. If the calendar gets too tight, rework goes up and owner pay drops.

The key inputs are booked days, crew capacity, job length, and buffer time for samples and site delays. One clean one-liner: full calendars do not equal full profit. If skilled finish work is overbooked, quality slips, callbacks grow, and cash comes in slower because the crew is stuck fixing old jobs instead of starting new ones.

Protect Finish-Day Capacity

Track booked days by job type, not just by sales. Set a hard buffer for prep, curing, travel, polishing, and punch lists, then compare planned hours to actual hours each week. Here’s the quick math: if a project needs more unpaid time than expected, effective margin falls even when revenue looks strong.

Price and schedule around reality, not hope. Keep open slots for delays, and only add work when the crew can still deliver a clean finish. Utilization means the share of available labor time that is billable; if it runs too hot, rework and overtime eat owner draw.

1

Average Project Value

Average Project Value

Average project value is the fastest pricing lever in this business because well-scoped decorative plaster jobs carry strong direct margins. Year 1 weighted project value is about $7,560; Year 5 rises to about $12,180. At the same job count, that is roughly 61% more revenue, so owner pay improves only if scope stays tight and rework stays low.

This driver includes wall and ceiling size, substrate condition, finish level, color complexity, and access. A quoted price per square foot is just an input, not a universal market rate. Here’s the quick math: if you miss prep or access, a higher ticket can still produce weaker cash flow because labor hours and material use rise faster than the invoice.

Price Every Scope Variable

Track realized price by project type: $5,000 residential, $13,200 boutique commercial, and $9,600 specialized finish work. Then compare that to hours, material use, and change orders. If a 10% price lift adds $756 per job on the Year 1 average, that’s pure upside only when the crew does not absorb the extra scope for free.

Build estimates around triggers: substrate repair, ceiling work, difficult access, extra color layers, and sample boards. Charge for mockups and revisions, or margin leaks before you see it in the bank. Higher-value jobs can fund owner draw, but only when quote-to-close time, labor, and rework stay under control.

2

Premium Lead Quality

Premium Lead Quality

Premium leads are the jobs that come from high-end homeowners, interior designers, architects, and boutique commercial clients. They usually support better pricing, higher project value, and fewer price-only bids. In this model, the disclosed mix shifts from 60% residential and 20% boutique commercial in Year 1 to 40% residential and 40% boutique commercial by Year 5, which can lift weighted project value from $7,560 to $12,180.

The catch is sales friction. Better leads often ask for samples, mockups, and more design time, so margin only improves if that time is priced. If proposals stay free, owner pay gets squeezed even when revenue per job rises. The key test is simple: does each lead source produce enough closed work at a higher ticket to cover the extra pre-sale labor?

Track Lead Quality, Not Just Lead Count

Measure source mix, close rate, average project value, and proposal hours per win. Track which leads come from designers, architects, and boutique commercial referrals, then compare them with residential-only inquiries. A lead is premium only if it raises revenue and does not eat the gain through unpaid estimating time.

- Price samples and mockups up front.

- Track discount rate by source.

- Set a minimum project value.

- Cap unpaid proposal hours.

Use a simple rule: if a lead needs more design effort, samples, or site visits, charge for it or build it into the bid. Otherwise, the owner ends up doing more work for the same draw. Better-fit leads should raise take-home income by lifting ticket size, not by adding unpaid sales labor.

3

Labor Productivity

Labor Productivity

Labor productivity decides whether project revenue turns into owner pay. In this model, crew hours for prep, masking, base coats, burnishing, polishing, protection, travel, and punch-list work must stay separate from the founder’s $95K salary and other payroll, or the job can look profitable when it is not.

- 40 residential billable hours

- 120 boutique commercial billable hours

- 60 specialized finish billable hours

- Direct labor excludes founder pay

Here’s the quick math: if actual hours run above those Year 1 assumptions, gross margin falls and cash available for draws drops. Training can raise capacity, but it also pushes payroll up before crews hit full speed, so the owner may see more revenue with less take-home in the early ramp.

Track billable hours by finish type

Measure billable hours by job type, not just total labor. Compare actual hours to the Year 1 assumptions, then price for rework, travel, samples, and protection time. One clean rule: if a crew needs extra hours, the bid should pay for them, or the owner is funding the gap.

Watch rework, training time, and non-billable setup together. If those hours rise, owner income falls even when sales hold. Use a simple job sheet for each project with labor hours, direct labor cost, and delay reasons, so you can tighten scopes, schedule better, and protect margin before adding headcount.

4

Direct Cost Control

Direct Cost Control

Materials and job costs hit gross margin right away, so this driver decides how much of each project turns into owner pay. In Year 1, the direct cost stack is 14% premium lime and pigment materials, 4% consumables and abrasives, 6% logistics and transportation, and 2% waste disposal, for 26% total direct costs on $907K revenue.

Sample boards, mockups, sealers, tools, protection, and rework have to be covered in the price. By Year 5, direct costs fall to 20%, but even a 1-point margin miss on $907K revenue is about $91K before overhead, so small leaks can cut the owner’s draw fast.

Track Cost Leakage Early

Measure each job by materials, freight, waste, rework, and site protection. Compare the actual cost stack to the quote so you can see which finish types, access issues, or sample demands are eating margin.

- Price mockups and samples separately.

- Log freight on every project.

- Cap rework before it spreads.

If a job runs above the planned 26% direct cost in Year 1, fix the scope or reset pricing before the next bid. That keeps gross margin intact and protects cash for overhead and owner pay.

5

Overhead And Cash Reserves

Overhead And Cash Reserves

Owner pay comes after fixed overhead and cash reserves, not after job profit. Here, overhead is $77K per month for showroom rent, utilities, insurance, maintenance, software, and vehicle lease, plus $15K of Year 1 marketing. With $778K minimum cash needed in Month 2, even strong EBITDA, the operating profit before interest, taxes, depreciation, and amortization, won’t fund draws if collections slow.

Protect the cash floor

Track a 13-week cash forecast and tie owner draws to cash above $778K. Build in the $750 CAC and capex like the $45K showroom buildout, $38K delivery van, and $12K scaffolding, because those outflows hit before the owner gets paid. If sales dip, cut spend fast and hold distributions until the reserve is rebuilt.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner pay changes fast as utilization, pricing, and labor efficiency scale from Year 1 to Year 5. The table shows how the same business can move from founder-salary economics to much higher earnings.

| Scenario | Low CaseDownside path | Base CaseMiddle path | High CaseUpside path |

|---|---|---|---|

| Launch model | This is the lower earnings path, with Year 1 scale and the founder still carrying most of the operating load. | This is the modeled mid-case, where earnings rise as volume, pricing, and staffing settle into Year 3 scale. | This is the stronger earnings path, with Year 5 scale and better use of labor and pricing power. |

| Typical setup | About 10 jobs a month, $907K revenue, 74% contribution margin, and $294K EBITDA while fixed overhead stays heavy. | About 28 jobs a month, $3.118M revenue, 76.8% contribution margin, and $1.709M EBITDA with a more balanced crew mix. | About 40 jobs a month, $5.869M revenue, 80% contribution margin, and $3.711M EBITDA with commercial work at 40%. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $95,000 - $294,000Founder pay | $294,000 - $1,709,000Modeled pay | $1,709,000 - $3,711,000Upside pay |

| Best fit | Use this to stress-test early-stage owner pay before the crew and sales process are fully stable. | Use this as the main planning case for budgeting owner pay, hiring, and cash use. | Use this to test what owner pay could look like if demand, pricing, and crew productivity all improve. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets.

Related Products

- Venetian Plaster Application Porter's Five Forces Analysis

- Venetian Plaster Application BCG Matrix

- Venetian Plaster Application Business Model Canvas

- What 5 KPIs Matter For Venetian Plaster Application Business?

- Venetian Plaster Application Business Plan Template in Pre-Written Word

- How Increase Venetian Plaster Application Profits?

- What Are Venetian Plaster Application Operating Costs?

- Venetian Plaster Startup Costs: $778K Funding Plan

- Venetian Plaster Application Financial Model Template in Excel

- How To Start A Venetian Plaster Business In 4 To 8 Weeks

- How To Write A Business Plan For Venetian Plaster Application?

- Venetian Plaster Application Marketing Mix

- Venetian Plaster Application Marketing Plan

- Venetian Plaster Application Business Proposal

- Venetian Plaster Application PESTEL Analysis

- Venetian Plaster Application Pitch Deck Example Editable PPTX

- Venetian Plaster Application Business SWOT Analysis

- Venetian Plaster Application Value Proposition Canvas

Frequently Asked Questions

In the researched planning case, revenue starts at $907K in Year 1 and reaches $5869M by Year 5 The increase comes from higher project volume, higher hourly pricing, and a mix shift toward boutique commercial work Revenue is not owner income because payroll, overhead, materials, reserves, taxes, and reinvestment still come first