How Much Can a VAD Services Owner Make on $30M First-Year Revenue

Ventricular Assist Device Services

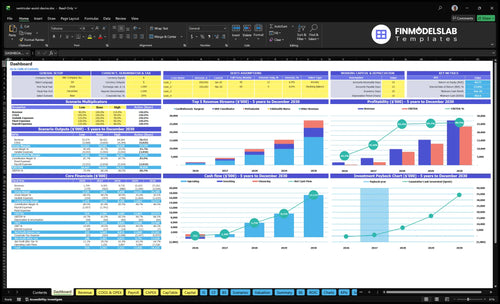

A VAD services owner could model about $10 million of first-year EBITDA on $30 million of revenue, before personal taxes, debt service, required reserves, and any owner-specific salary decision These are researched planning assumptions, not guaranteed take-home income By the mature year, the same model reaches $402 million of revenue and about $328 million of EBITDA, driven by higher clinical capacity, more service volume, and lower direct cost percentages Actual ventricular assist device services profit can differ materially by state, hospital affiliation, payer mix, reimbursement contracts, clinical scope, staffing model, and complication burden

Owner income$319k to $23.6MNet margin18.7% to 86.5%Revenue for target pay$1.7MBusiness difficultyHard

Want to test your VAD services owner income?

VAD Owner Income

Estimate owner take-home from monthly revenue, margin, staffing, overhead, reserves, and a target pay goal for Ventricular Assist Device services.

!

Planning note Researched planning estimate only; it is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Ventricular Assist Device Services model?

Ventricular Assist Device Services makes money by billing for implantation-related clinical work and ongoing patient management, so the model is based on service fees, not just the surgery itself. In the first-year assumptions, a cardiothoracic surgeon service is $25,000, a perfusionist service is $3,500, a VAD coordinator service is $1,500, a telehealth nurse contact is $450, and a clinical specialist service is $2,200. This is collected revenue in the model, not a payer promise, and actual cash depends on coding, authorization, site of service, contract terms, denial management, and clinical scope.

Revenue drivers

$25,000 surgeon service

$3,500 perfusionist service

$1,500 coordinator service

Pre-implant and outpatient support

Collection risks

Depends on payer rules

Needs clean coding and authorization

Varies by site of service

Denials can cut cash collected

Can a ventricular assist device services business be profitable?

Yes—under the researched assumptions, a Ventricular Assist Device Services business can be profitable, but owner cash comes after volume, payer contracts, clinical staffing, debt service, and reserves; see How Much To Open Ventricular Assist Device Services Business? for startup cost context. The model shows $30 million first-year revenue and about $10 million EBITDA, then $402 million mature-year revenue and about $328 million EBITDA; EBITDA means earnings before interest, taxes, depreciation, and amortization.

Profit Math

$30 million first-year revenue

$10 million first-year EBITDA

$402 million mature-year revenue

$328 million mature-year EBITDA

Owner Reality

105% first-year COGS assumption

90% first-year variable expense assumption

$474,000 fixed overhead

Separate owner income from surgeon pay

What operating costs reduce VAD services owner income?

Ventricular Assist Device Services loses owner income mainly to clinical labor, surgical kits, sterile logistics, malpractice, telehealth data and security, compliance, and billing support. Here’s the quick math: first-year COGS is 105% of revenue from surgical kits, consumables, sterile logistics, and handling, while first-year variable costs add another 90% from malpractice premiums and telehealth data/security; see How Increase Ventricular Assist Device Services Profitability? for the margin side. Fixed overhead is $39,500 per month ($474,000 a year), plus $915,000 in first-year wages, led by a $350,000 Chief Medical Officer and a $180,000 VP Operations, so every denied dollar or added complication reserve cuts cash.

Big cost drains

105% COGS to revenue

90% variable cost load

$39,500 monthly overhead

$915,000 first-year payroll

Where it hits margin

Clinical staffing and surgical kits

Malpractice, telehealth, and security

Compliance, legal, and billing support

Hospital relations and emergency coverage

Ventricular Assist Device Services Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six drivers behind VAD owner income?

1

Implant Volume

$1.7M-$27.3M

More VAD implants at $25K-$28K each drive the biggest jump in owner take-home as surgeon capacity rises from 45% to 85%.

2

Patient Census

40-60/mo

A larger active census keeps coordinator, telehealth nurse, and clinical specialist work flowing, so recurring management revenue scales faster than fixed overhead.

3

Payer Collections

High

Cleaner authorization and fewer denials speed cash from Medicare, Medicaid, and commercial payers, which protects reserves and payback.

4

Hospital Deals

High

Better operating room access, ICU support, call coverage, and subsidy terms improve margin because the hospital shares more of the load.

5

Staff Utilization

45%-90%

As surgeons, coordinators, and telehealth nurses move from low to high capacity, the same team can support more treatments before overhead jumps.

6

Complication Costs

16%-20%

Lower readmissions, infection costs, and malpractice exposure keep more cash in the business instead of funding claims and rework.

Ventricular Assist Device Services Core Six Income Drivers

VAD Implantation Volume

Volume Spreads Cost

Higher VAD implantation volume can spread fixed overhead and clinical leadership costs, but only when the hospital can support the work. The first-year model assumes 2 cardiothoracic surgeons, 4 monthly treatments each, $25,000 per case, and 45% capacity, producing $108 million in surgeon-service revenue.

Year One

Here’s the quick math: the mature-year model raises capacity to 85%, uses 10 surgeons, and assumes 6 monthly treatments each at $28,000. That lifts surgeon-service revenue to $171 million. The gain is real only if staffing, collections, and clinical control scale with the case load.

Hold OR blocks before adding cases.

Keep ICU and call coverage ready.

Review denials and outcomes monthly.

Scale Safely

Volume helps when it is matched to care coordination, reimbursement, and quality control. If any one of those slips, more implants can raise overtime, denials, and strain instead of profit. The hard part is not finding cases; it is keeping the operating room, ICU, and follow-up team in sync.

Capacity First

Push volume after the base is ready: staffed OR time, ICU support, call coverage, and clean documentation. If those pieces are thin, the added cases may look good on revenue but still erode margin through delays, burnout, and quality risk. The model’s upside comes from scale with control.

Active VAD Patient Census

Active Census

Active VAD patient census is the recurring revenue engine, separate from one-time implantation economics. With 4 VAD coordinators at 10 monthly treatments each, 3 telehealth nurses at 40 monthly contacts each, and 2 clinical specialists at 12 monthly treatments each, year-one service revenue is about $164 million before collection risk.

Monthly Load

Here’s the quick math: that staffing plan supports 184 monthly service events before any growth. By mature year, the same roles reach about $1,847 million in revenue. The job is to keep the census active enough to fill care slots without overloading high-risk follow-up.

Watch coordinator capacity first.

Match nurse load to contacts.

Keep specialist time booked.

Margin Control

Margin depends on utilization, not headcount alone. Keep coordinators, nurses, and specialists busy, but don’t push so hard that missed follow-up or adverse events rise. Churn, missed follow-up, and underpriced care coordination can quietly cut the cash left from each active patient.

Price coordination work explicitly.

Track follow-up completion weekly.

Flag overload before quality slips.

Cash Risk

The recurring base only stays valuable if collections stay clean and follow-up stays tight. If active patients grow faster than staff can manage, revenue can look strong on paper while cash falls behind on missed visits, denials, or avoidable adverse events.

Payer Mix And Reimbursement Collections

Payer Mix

Your owner income moves when collected cash differs from modeled prices. For VAD services, the model uses pricing assumptions, not fixed reimbursement promises: $25,000-$28,000 for cardiothoracic surgeon services and $450-$510 for telehealth nurse contacts. Medicare, Medicaid, and commercial contracts can all pay differently, so collection risk is built into the forecast.

Collections Gaps

The swing comes from authorization rules, coding requirements, denial rates, collection timing, and site-of-service terms. If one payer needs more approval or pays slower, cash drops even when booked revenue looks fine. That changes margin, reserves, and how much the owner can safely take out.

Small Misses

Here’s the quick math: a small collection shortfall is material when first-year revenue is $30 million and mature-year revenue is $402 million. A 2% miss is about $600,000 in year one and $8.04 million at scale. That is direct pressure on revenue, margin, reserves, and owner cash.

Cash Control

Track payer mix by contract, not just by case count. Watch denial rates, days in accounts receivable, and whether the service site matches contract terms. If collections slip, trim spend fast and hold more reserve until cash timing proves out.

Hospital Partnership And Contract Structure

Contract decides

Same patient volume can produce very different owner income. The contract decides who keeps revenue and who carries risk across privileges, OR access, ICU support, perfusion coverage, call coverage, revenue sharing, subsidies, service-line management fees, and quality obligations.

Setup overhead

The model carries $8,500 per month for marketing and hospital relations plus $6,000 per month for legal and Centers for Medicare & Medicaid Services liaison. That is $14,500 a month, or $174,000 a year. Estimate it as monthly spend times months of coverage, then add it into the startup cash plan.

Count months, not one-time quotes.

Price compliance help separately.

Reserve cash for contract delays.

Cut risk

Keep the scope tight and price extra obligations. Standardize privilege packets, call schedules, and quality reporting, and push legal review into one contract path. The savings are usually in fewer outside counsel hours and less rework, not in cutting compliance. If a hospital adds coverage demands, build them into the fee.

Use one term sheet first.

Track change orders in writing.

Don’t absorb free call coverage.

Keep the margin

A physician-owned group may keep more upside but also carry staffing, malpractice, and working-capital risk. A management company may earn a fee with less downside, while a hospital-contracted service can trade margin for access and subsidies. The contract choice is the profit model, so cash needs and risk limits should be set before the first case.

Clinical Staffing And Coverage Utilization

Utilization first

Owner take-home rises when staffed hours track referrals. A first-year team of 2 surgeons, 4 coordinators, 2 perfusionists, 3 telehealth nurses, and 2 clinical specialists can cover launch volume, but the mature plan expands to 10, 20, 10, 20, and 10; underused labor drains margin fast.

Payroll load

This payroll line is the core startup cost. The plan carries $915,000 in year one and $1.48 million in the mature year, so the estimate starts with headcount × fully loaded wage rates × months staffed. It sits near the top of the budget because it funds coverage, call response, and patient continuity.

Use loaded wages, not base pay.

Model staffing by launch month.

Separate launch and mature years.

Keep margin safe

Margin improves when capacity use rises from 45% to 85% for surgeons, 50% to 90% for coordinators, and 40% to 80% for perfusionists. The hard part is balance: understaffing high-acuity patients can hurt outcomes, but paying the team before referrals arrive ties up cash.

Coverage risk

If demand ramps slowly, payroll can outrun revenue; if coverage runs thin, the program risks missed care and poor handoffs. The practical move is to staff to the referral pipeline, then add capacity only when case flow and managed-patient load can keep the team busy.

Complication Costs And Reserves

Cash Shield

Complication reserves keep a VAD service from turning one bad month into a cash crisis. This model already loads medical malpractice insurance at 60% of revenue in year 1 and 40% in a mature year, so the first question is not profit, it’s whether collected cash can cover claims, care follow-up, and overhead.

Fixed Oversight

Here’s the quick math: quality assurance monitoring is $4,000/month and regulatory compliance oversight is $5,500/month, for $9,500/month in fixed oversight before malpractice, readmission support, or device problem work. Size reserves with months of coverage, expected claim timing, and delayed collection risk.

Reserve Uses

Use reserves for readmission support, infection management, device issues, denied claims, claims exposure, delayed collections, and reinvestment. One clean rule: if the reserve can’t survive a bad payer month, it’s too thin. Treat this as required planning capital, not leftover profit.

Owner Cash

That reserve choice lowers distributable owner cash, but it makes the business harder to break. If collections slip or complications rise, the buffer protects payroll, compliance, and patient care instead of forcing a panic draw. Owners should model cash available after reserves, not before them.

Ventricular Assist Device Services Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high VAD owner-income scenarios

Owner income scenarios

Referral flow, payer collections, and clinical coverage drive large swings in owner income. The same service line can stay thin in launch, then expand fast as volume and staffing stabilize.

Low, base, and high income paths for the service line.

Scenario

Low CaseReferral-dependent

Base CaseContract-dependent

High CaseQuality-dependent

Launch model

Launch-year earnings stay modest when referral flow is thin and utilization is still ramping.

Modeled earnings land at the year-three operating scale once contracts and case flow stabilize.

Stronger earnings show up in the mature year when quality, coverage, and contract depth all hold.

Typical setup

Year 1 reaches $1.709 million revenue and $319,000 EBITDA, with 2 cardiothoracic surgeons, 4 VAD coordinators, and 3 telehealth nurses supporting low volume.

Year 3 reaches $9.735 million revenue and $8.109 million EBITDA, with 6 surgeons, 12 coordinators, 6 perfusionists, and 10 telehealth nurses carrying more cases.

Year 5 reaches $27.252 million revenue and $23.573 million EBITDA, with 10 surgeons, 20 coordinators, 10 perfusionists, and 20 telehealth nurses supporting higher throughput.

Cost drivers

Referral flow

payer collections

clinical coverage

fixed overhead

utilization

Hospital contracts

payer mix

staffing depth

case volume

compliance load

Referral depth

contract renewal

quality outcomes

clinical coverage

utilization

Owner income rangeBefore owner reserves

$319kThin launch band

$8.1MModeled base band

$23.6MMature upside band

Best fit

Best for teams stress-testing a slow referral start, weaker collections, or slower hospital adoption.

Best for operators planning around steady hospital affiliation and workable payer collection strength.

Best for a business with strong hospital affiliation, reliable payer collections, and enough clinical coverage to keep quality tight.

!

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

A researched first-year model shows about $10 million of EBITDA on $30 million of revenue before debt service, reserves, distributions, and personal taxes That is not a guaranteed salary Mature-year assumptions reach $402 million of revenue and $328 million of EBITDA, but actual owner income depends on contracts, payer mix, clinical scope, and complication costs

The model can support owner pay in the first year if cash collections, staffing, and reserves hold First-year revenue is $30 million against $915,000 of wage payroll and $474,000 of fixed overhead Still, a prudent owner would reserve cash for malpractice exposure, delayed reimbursement, care quality, and the $250,000 telehealth platform build

In practice, hospital affiliation or contracts are central to the economics VAD services depend on operating room access, intensive care support, perfusion coverage, call coverage, care coordination, and payer authorization The model includes $8,500 per month for marketing and hospital relations plus $6,000 per month for legal and Centers for Medicare & Medicaid Services liaison

Volume, payer collections, staffing use, and reserves move margin the most First-year EBITDA margin is about 341% after 105% COGS, 90% variable expenses, $474,000 fixed overhead, and $915,000 payroll Mature-year margin rises in the model because capacity improves and COGS plus variable expenses fall to 135% combined

Build a monthly forecast that starts with provider count, monthly treatments, service prices, capacity, and collection rate Then subtract COGS, malpractice, telehealth security, fixed overhead, payroll, debt service, and reserves Use first-year values like $25,000 surgeon services, $1,500 coordinator services, and $450 telehealth contacts, then test low, base, and high scenarios

About the author

Patrick Hughes

Small Business Writer

Patrick Hughes is a small business writer who focuses on business affordability analysis for side-hustle builders planning with limited capital. He researches how small businesses launch, operate, and earn money, with a practical eye on business idea evaluation. His writing highlights common costs new founders often miss, helping readers make clearer, more realistic decisions before they start.

Choosing a selection results in a full page refresh.