How Much Ventriloquism Lessons Owners Make: $65k Salary Plus Profit

A ventriloquism lessons owner can plan around a modeled $65,000 annual operator salary, plus possible profit distributions if cash, taxes, reserves, and reinvestment allow In the researched assumptions, revenue is $417,000 in the first year with $196,000 EBITDA, or about a 470% EBITDA margin By the fifth year, revenue reaches $6708 million with $5474 million EBITDA, driven by higher occupancy, more group seats, workshops, and instructor capacity These are planning assumptions, not guaranteed take-home pay

Owner income$5.4kNet margin47%–82%Revenue for target pay$34.8k–$559kBusiness difficultyMedium

Want to test your own ventriloquism lessons income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This output is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to see how Ventriloquism Lessons turns teaching slots into owner income?

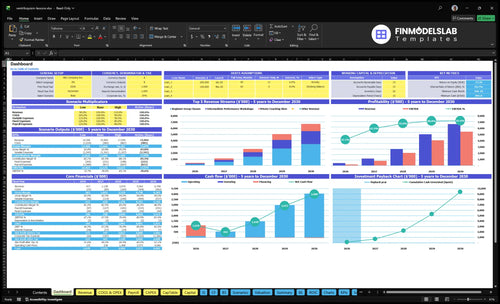

The screenshot shows the dashboard, assumptions, revenue build-up, cost schedule, payroll, capex, cash flow, and scenario outputs in the Ventriloquism Lessons Financial Model Template, so you can see how teaching slots turn into owner income. It shows $417k first-year revenue, $196k first-year EBITDA, $65k owner salary, $891k minimum cash in Month 2, and Month 1 break-even. Open the model.

Owner-income model highlights

Owner salary capacity

Revenue, EBITDA, occupancy

Scenarios and cash floor

How do you scale a ventriloquism lessons business?

Scale Ventriloquism Lessons by moving beyond one-on-one coaching into group classes and workshops, while keeping student results tight. In the model, beginner class capacity rises from 40 to 100, workshops from 20 to 60, and private coaching slots from 15 to 30, with occupancy moving from 45% to 90%. That pushes revenue from $417k to $6,708M, and junior instructor capacity climbs from 0 FTE to 20 FTE by year five.

Capacity moves

Grow beginner groups to 100

Lift workshops to 60

Double private slots to 30

Raise occupancy to 90%

Scale guardrails

Add junior instructors to 20 FTE

Use online cohorts last

Launch school workshops next

Keep outcomes and retention stable

What expenses affect ventriloquism lessons profit margin most?

For Ventriloquism Lessons, the biggest profit drag is the $3,680 monthly fixed overhead, and payroll is next. If you want the broader math, see How Increase Ventriloquism Lessons Profitability? Setup capex is another early hit at $30,000, while variable costs run 19% of revenue in year one and ease to 14% by year five.

Recurring costs

$2,800 studio lease

$350 utilities and internet

$150 insurance

$200 cleaning

Other margin hits

$65k owner salary

$38k coordinator salary at 0.5 FTE

Junior instructor starts in year two

$30k setup capex

Can you make a living teaching ventriloquism?

Yes, you can make a living teaching Ventriloquism Lessons if paid demand fills the schedule and startup cash is funded; see What Are Ventriloquism Lessons Operating Costs? before you price classes. In the owner-operated case, the model includes a $65k annual Lead Instructor and Director salary, with $417k first-year revenue and $196k EBITDA at 45% occupancy.

Living Wage Case

Pay owner salary: $65k/year

Hit first-year revenue: $417k

Produce EBITDA: $196k

Run at occupancy: 45%

Watch The Risks

Strong case: $6.708M revenue

Strong EBITDA: $5.474M

Occupancy target: 90%

Month 2 cash need: $891k

Ventriloquism Lessons Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want to see the six biggest income drivers?

1

Booked Hours

45%-90%

More filled lesson slots push revenue up fast, and the gain flows straight to take-home when quality stays tight.

2

Lesson Rate

$150-$550

Higher prices on classes, workshops, and coaching lift EBITDA without needing many more sessions.

3

Premium Mix

1.5x-3.7x

Shifting sales from beginner groups to workshops and private coaching raises revenue per slot and owner pay.

4

Retention Loop

40-100

Keeping students moving from beginner to advanced offers more repeat revenue and lowers the cost to refill classes.

5

Delivery Cost

14%-19%

Materials, guest facilitators, ads, and payment fees take a real cut, so lean delivery keeps more cash.

6

Workshop Bookings

20-60

Institutional and seasonal bookings fill off-peak days, smooth cash flow, and protect the 22-24 billable days.

Ventriloquism Lessons Core Six Income Drivers

Paid Teaching Utilization

Paid Teaching Utilization

Paid teaching utilization is the share of available lesson hours that get sold and paid for. In a class business, that matters because an empty room still carries rent and instructor time, so higher fill rates lift profit before you add new fixed costs. The model’s occupancy target moves from 45% in year one to 90% in year five, with billable days rising from 22 to 24 per month.

Here’s the quick math: more booked hours, higher paid attendance, fewer cancellations, and more repeat bookings push revenue up from $417k as capacity fills. The risk is assuming every open teaching hour becomes billable; it won’t. If no-shows or weak repeat rates keep seats empty, owner pay stays tight even when the schedule looks full.

Track Fill Before You Add Hours

Measure booked lesson hours, paid attendance, cancellations, and repeat bookings each month. Utilization is simple: paid hours divided by available teaching hours. If attendance is slipping, fix reminders, deposits, and make-up policies first, because those move cash flow faster than adding more class time.

Watch paid hours per teacher.

Flag no-show patterns by class.

Test make-up and refund rules.

Link renewals to next-level classes.

One clean rule: fill the schedule before you expand it.

1

Effective Lesson Rate

Effective Lesson Rate

Effective lesson rate is the real revenue you get per teaching hour after pricing, package mix, no-shows, and admin gaps. Here’s the quick math: beginner group classes rise from $150 to $190, intermediate workshops from $220 to $260, and private coaching from $450 to $550. If retention stays steady, those price gains can lift EBITDA, or earnings before interest, taxes, depreciation, and amortization, before most costs move.

The risk is simple: if conversion weakens or students push back on price, the higher rate can miss the mark and cash flow stays flat. What this estimate hides is the mix of group, workshop, and private hours. A cleaner skill path and fewer no-shows matter because they raise paid hours without adding rent or payroll. One clean one-liner: price only helps when it turns into paid teaching time.

Track rate by level, not just by booking

Measure booked hours, paid attendance, cancellations, repeat bookings, and price by class level. The key inputs are student count, lesson mix, and how many hours actually get paid. If packages reduce admin gaps and no-shows, effective hourly revenue rises even when the posted rate stays the same. That improves owner take-home because fixed overhead does not need to rise first.

Test small price moves against retention. Beginner classes moving from $150 to $190 is a 26.7% lift, intermediate workshops from $220 to $260 is 18.2%, and private coaching from $450 to $550 is 22.2%. If conversion holds, even modest gains can flow straight to profit. If onboarding or skill progression is unclear, price resistance usually shows up fast.

Track paid hours, not just scheduled hours

Watch no-show rate by program

Compare conversion by price level

Use packages to reduce admin gaps

Forecast owner pay from paid teaching hours

2

Group Classes And Workshops

Group Fill Rate

Group classes and workshops matter because one instructor can teach more people at once, so revenue per hour rises when seats fill. Beginner classes scale from 40 to 100 seats, and workshops from 20 to 60. Workshops also price higher, from $220 to $260, so the mix matters. The driver is seat fill, not just class count.

Inputs are capacity, enrollment, ticket price, and class-specific costs like curriculum, room setup, materials, and guest facilitator fees. If fill rates stay low, the class can earn less than private coaching because the same teaching hour supports fewer paying students. Strong occupancy lifts gross profit and gives the owner more room to pay themselves.

Fill More Seats

Track booked seats, paid attendance, and cancellations for each session. Here’s the quick math: students x price tells you the revenue side, then subtract session costs to see what’s left for owner pay. If workshops fill better than beginner classes, they often earn more per hour because the ticket is higher and the format scales.

Set a seat minimum before you run a class, then open more spots only after demand holds. Use beginner classes to feed workshops, and only add guest facilitators when enrollment covers the extra fee. If a session cannot cover its room and material costs at current enrollment, cut it or switch that slot to private lessons.

3

Student Retention And Repeat Bookings

Repeat Bookings

Retention is what keeps seats filled without buying every student again. In this model, marketing is 8% of revenue in year one and 5% by year five, so repeat bookings protect margin and cash flow. More renewals mean steadier occupancy, less ad pressure, and more take-home income from the same teaching hours.

The key inputs are repeat student rate, package renewal, referral source, and cancellation rate. Weak progression is the main risk: if students do not see a clear next step after the beginner stage, churn rises when the novelty fades, and revenue becomes harder to hold.

Build the next step

Use beginner-to-intermediate paths, monthly packages, referrals, and performance goals so students have a reason to stay. Here’s the quick math: every renewed student lowers replacement demand, which cuts the need for paid ads and helps keep occupancy stable.

Track renewals by class level

Measure repeat rate monthly

Log referral source at signup

Review cancellations by reason

Set a next-level goal early

4

Online Versus In-Person Delivery Cost

Online vs In-Person Delivery Cost

Online lessons can reduce travel and studio use, but they do not always raise profit. With fixed studio overhead at $3,680 per month, the real question is whether online students add margin on top of that cost or just replace higher-value in-person sessions.

In-person teaching still supports stage practice, puppet manipulation feedback, workshops, and local referrals. If online fills empty hours, it can lift owner pay; if it displaces strong in-person bookings, it can hurt take-home income even when delivery costs look lower.

Track the channel that pays

Measure online share, close rate, refund rate, and student outcomes by channel. That tells you if online is selling well, keeping students, and producing results that support repeat bookings and referrals.

Technology quality matters because weak video or audio can cut conversion and retention. Use online to fill otherwise unused capacity, and keep in-person slots for higher-touch teaching that protects revenue quality and margins.

Compare online and in-person margin

Watch refunds and repeat bookings

Protect workshop and feedback time

5

Institutional And Seasonal Bookings

School and Seasonal Bookings

Schools, libraries, camps, homeschool groups, and community centers can fill off-peak teaching days and lift cash flow fast. Treat them as supplemental revenue unless the business is built around group outreach, because pricing is often lower per student and sales cycles are longer.

Here’s the quick math: owner income depends on booking count, revenue per event, prep hours, and repeat contracts. If each event needs extra setup and travel, gross margin drops even when revenue looks strong. One clean rule: more events only help if the added margin beats the added labor.

Track event margin, not just bookings

Measure events booked, revenue per event, prep hours, and repeat rate. Then compare that to the instructor’s billable time and any setup or travel. A 10-event month can still underperform if each event takes too much prep. The owner’s take-home rises when these bookings fill empty slots without crowding out higher-rate private lessons.

Price by event, not by applause.

Log prep time for each group.

Separate one-offs from repeat contracts.

Watch season spikes and slow months.

If outreach takes months, keep these deals out of core forecasts. Use them to support group enrollment and smooth idle weeks, but don’t build rent or owner pay on them alone. The best case is useful upside with low cancellation risk and a clear path to repeat bookings.

6

Ventriloquism Lessons Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare lean, base, and high ventriloquism lessons income scenarios

Owner income scenarios

Income here moves with occupancy, billable days, and staffing. EBITDA scales fast, but take-home cash depends on how much stays in the business.

Compare lean, base, and high income paths.

Scenario

Lean CaseLow utilization

Base CaseHiring starts

High CaseCapacity tight

Launch model

The lean case assumes first-year demand at 45% occupancy, 22 billable days, $417k revenue, and $196k EBITDA.

The base case assumes year-three scale at 75% occupancy, 24 billable days, $2.67M revenue, and $2.04M EBITDA.

The high case assumes year-five scale at 90% occupancy, 24 billable days, $6.71M revenue, and $5.47M EBITDA.

Typical setup

The owner teaches most sessions, carries the studio costs, and operates without a junior instructor.

The studio supports one junior instructor, more group classes, and a fuller workshop mix.

The studio runs near full, adds two junior instructors, and pushes higher-volume coaching and workshops.

Cost drivers

Occupancy rate

22 billable days

fixed studio overhead

digital marketing

owner salary

75% occupancy

24 billable days

one junior instructor

class mix

digital advertising

90% occupancy

two junior instructors

higher class volume

premium coaching mix

higher cash demand

Owner income rangeBefore owner reserves

$196k EBITDALean income

$2.04M EBITDABase income

$5.47M EBITDAUpside income

Best fit

Use this to stress-test early demand, cash use, and the first-year load on the owner.

Use this as the mid-case plan if enrollment grows steadily and hiring stays on pace.

Use this to test upside if demand stays strong and staffing keeps up with bookings.

!

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The model includes a $65,000 annual Lead Instructor and Director salary, or about $5,400 per month before taxes Business profit is separate First-year EBITDA is $196,000 on $417,000 revenue, but distributions depend on cash, reserves, capex, debt, and reinvestment needs

The researched model shows break-even in Month 1 and payback in Month 1 That looks strong, but it also shows a $891,000 minimum cash need in Month 2 Treat break-even as operating math, not proof that the business is low-risk or self-funding

Not always, but this model assumes a studio Recurring studio-related overhead includes a $2,800 lease, $350 utilities and internet, $150 liability insurance, and $200 cleaning each month Online lessons can reduce some space pressure, but in-person classes may support workshops and local referrals

Utilization, pricing, payroll, and marketing have the biggest effect Occupancy rises from 45% to 90% in the model, while marketing drops from 8% to 5% of revenue Payroll adds a $65,000 owner salary, coordinator support, and junior instructors as capacity scales

Fill paid teaching slots before adding complexity Then raise revenue per hour with group classes, intermediate workshops, and private coaching packages The model grows beginner group capacity from 40 to 100 and workshops from 20 to 60, but quality control matters as instructors are added

About the author

Stephen Knight

Business Idea Researcher

Stephen Knight is a business idea researcher at Financial Models Lab who focuses on revenue and profit basics for founders building a simple business plan. He breaks down business model overviews in plain English, helping non-finance readers understand what it really takes to open a physical location and turn an idea into a workable plan.

Choosing a selection results in a full page refresh.