How Much Do Wellness Retreat Center Owners Make? 30-Room Case

You’re estimating owner income for a US destination wellness retreat center, not a guaranteed salary In this 30-room planning case, Year 1 revenue is about $643M, with modeled operating profit of about $349M before taxes, debt service, reserves, and owner distributions

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Occupancy, staffing, and property costs drive the biggest swings.

Want to see the Wellness Retreat Center income model?

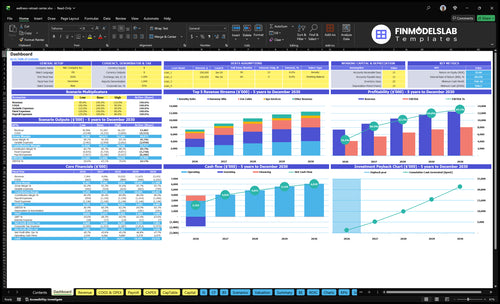

The dashboard ties rooms, occupancy, weekday and weekend ADR, add-ons, costs, payroll, fixed expenses, capex, and reserves into revenue, EBITDA, and owner cash; Year 1 shows $643M revenue, 543% operating margin, and $349M operating profit before tax and debt. Open the Wellness Retreat Center Financial Model Template.

Model highlights

Owner cash, clearly shown

Revenue and EBITDA split

Year 1, 3, 5 tested

Gross, profit, distributions separate

How does owner-operated wellness retreat center income compare with staffed growth?

Owner-operated Wellness Retreat Center income can be higher in the near term because it cuts management payroll, but the owner then absorbs hosting, scheduling, vendor, guest, and staff work. The staffed base case includes $830k in Year 1 payroll and supports 30 rooms at 55% occupancy, while the growth case reaches 82% occupancy by Year 5 with the same 30 rooms. So the tradeoff is simple: lower payroll can lift take-home now, while stronger staffing can protect guest experience, pricing, and repeat bookings.

Owner-operated cash

Lower payroll raises near-term cash

Owner covers daily operations

Workload shifts to one person

Service quality depends on capacity

Staffed growth

$830k Year 1 payroll base

30 rooms at 55% occupancy

Same rooms reach 82% by Year 5

Better staff support repeat bookings

What wellness retreat center profit margin and costs matter most?

The biggest margin issue for the Wellness Retreat Center is the cost stack, not demand. For the launch-cost view, see What Is The Estimated Cost To Open And Launch Your Wellness Retreat Center?—Year 1 variable costs already hit 150% of revenue. With fixed facility costs at $955k/month (about $11.46M/year) and payroll at $830k in Year 1, owner take-home is most exposed to occupancy, room yield, staffing, and property cost control.

Cost mix

60% premium food and beverage

30% practitioner fees

30% partner commissions

30% digital marketing

Margin levers

Push paid occupancy first

Protect room yield

Keep payroll design lean

Control property costs hard

How much can a wellness retreat center owner pay themselves?

A Wellness Retreat Center owner can pay themselves $180,000/year through payroll if they replace the general manager role; if passive, the model keeps $830,000 in Year 1 payroll, and owner pay should come from remaining cash distributions after taxes, debt, and reserves, which also ties to demand planning in What Is The Current Growth Rate For Wellness Retreat Center?.

Owner-operator pay

Replace GM role: $180,000 salary

Payroll falls, workload rises

Active host may justify payroll

Program director role needs clear duties

Passive owner cash

Keep Year 1 payroll: $830,000

Operating profit: about $349M

Pay taxes, debt, reserves first

Distributions are not salary

Wellness Retreat Center Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six main retreat income drivers?

1

Occupancy

30 rooms

Thirty rooms set the ceiling, but occupancy rising from 55% to 82% is what turns empty nights into cash.

2

Package Price

$750-$2.0K

A higher average daily rate (ADR) on the same beds lifts revenue fast, so each price step adds more take-home.

3

Calendar Fill

55%-82%

Filling more retreat dates and group blocks keeps premium nights sold and boosts room-night revenue without adding capacity.

4

Add-Ons

$85K-$148K

Spa, events, bar, consults, and retail rise from $85K to $148K a year, and those extras improve cash after room sales.

5

Payroll Mix

$830K-$1.12M

Payroll grows from about $830K to $1.12M as staffing expands, so demand must rise fast enough to protect margin.

6

Facility Costs

$1.146M

Fixed facility costs run about $1.146M a year, and reserves need to come before owner distributions, so cash control matters.

Wellness Retreat Center Core Six Income Drivers

Paid Occupancy And Guest Capacity

Paid Room Nights

Paid occupancy is the share of the 30 rooms that sell each night. This model moves from 55% in Year 1 to 82% in Year 5, so the business goes from about 6,023 paid room-nights a year to 8,979. More paid nights spread the $1.146M annual facility cost over more revenue, which lifts contribution dollars and cash before owner pay.

Here’s the quick math: 30 × 365 × 55% = about 6,023 room-nights, and 30 × 365 × 82% = about 8,979. That lowers facility cost per paid night from about $190 to about $128. The risk is filling rooms with deep discounts or low-margin stays, which can raise occupancy but still leave too little profit.

Track Net Occupancy, Not Interest

Measure occupancy by room type, date, and net rate after discounts. A sold room-night is one paid night, not an inquiry or a comp stay. Use a weekly forecast that ties paid rooms to cash available before owner pay, and set a floor rate so higher occupancy does not erase margin.

Track paid occupancy by room type.

Cap discount depth by stay length.

Reject low-margin filler nights.

Test occupancy against net contribution.

1

Average Package Price

Average Package Price

Average package price is the average daily rate (ADR), or what you collect per occupied room night. Here, Year 1 midweek pricing ranges from $750 to $1,500 and weekend pricing from $950 to $1,800; by Year 5, that lifts to $850 to $1,700 midweek and $1,050 to $2,000 on weekends. Higher rates raise revenue, contribution, and owner pay if occupancy holds.

The mix matters: premium rooms, private stays, longer programs, and high-value wellness packages push yield up. Here’s the tradeoff: pricing too high can cut demand and lower occupied room nights, so the real profit driver is not just rate, but rate times occupancy. One empty room night at a premium rate is still zero cash.

Price by room, day, and stay length

Track occupied room nights, weekend share, and package mix by room type. Test rate increases in small steps, then watch booking pace and cancellations before pushing higher. If demand weakens after a rate change, the owner loses more than discounting gains back.

Price premium rooms separately.

Measure weekday and weekend take-rate.

Watch fill rate after each change.

Bundle longer stays for higher yield.

2

Retreat Calendar Utilization

Retreat Calendar Utilization

This driver is the share of the year the property is actually open and selling room-nights. Revenue depends on occupied room-nights × blended ADR, so every empty night from cleaning, staff recovery, seasonal softness, repairs, or maintenance cuts income while fixed costs keep running.

The main inputs are retreats per year, downtime days, weekday versus weekend mix, and how many nights are sold to private groups or midweek programs. More sellable nights usually means smoother cash flow and more profit available for owner pay.

Raise Sellable Nights

Track calendar fill by month, not just bookings. If one retreat blocks extra recovery days, you are trading near-term revenue for lower stress, so measure whether that loss is offset by better service and repeat demand.

Push midweek programs and private group rentals into weak periods first. That adds revenue without new rooms, and it spreads fixed facility and staffing costs over more paid nights, which is the direct path to better cash flow.

3

Add-On Revenue Mix

Add-On Revenue Mix

Add-ons include spa services, event hosting, food and beverage, consultations, and retail. In this model, they rise from $85k in Year 1 to $148k by Year 5, with spa as the largest piece, growing from $35k to $55k. These dollars help owner pay only after labor, licensing, product, and service delivery costs.

The key inputs are guest count, attach rate, average spend per add-on, and service margin. If add-ons grow but staff time or product cost grows faster, cash flow can still tighten. One line: volume only helps when margin stays clean.

Protect Add-On Margin

Track attach rate by guest, spend per visit, and gross margin by service. Split spa, retail, and food by direct labor and product cost so you can see which add-on actually pays. Here’s the quick test: if a service adds sales but needs too much staff time, it can lower owner income.

Price by margin, not demand.

Cap low-margin service slots.

Forecast labor and product costs.

Keep the mix tight around higher-margin spa and consult upsells, and document what each offer needs in time, licensing, and supplies. That protects the guest experience and keeps add-ons from eating the core retreat business.

4

Staffing And Facilitator Economics

Payroll Load

Staffing and facilitator costs include the general manager, chef, spa director, wellness coordinators, housekeeping, marketing, front desk, and assistant practitioners. Year 1 payroll is $830k, and the model rises to $112M by Year 5. That cost only helps owner income if it supports higher occupancy, stronger pricing, and better guest spend.

Here’s the quick math: more labor can lift service quality, but it also pushes operating costs up fast. An owner-operated model can cut payroll, but it adds founder workload and service risk. Hiring managers costs more, yet it can protect consistency, which matters when guests pay for premium retreat experiences.

Keep Labor Tied to Booked Nights

Track payroll against paid room-nights, retreat count, and add-on sales, not just headcount. If staff costs rise faster than occupancy or package price, owner take-home falls. The key test is simple: does each added role raise revenue enough to cover its full cost plus overhead?

Build the staffing plan around the busiest booking periods and the services that sell the most, like spa care and guided wellness programs. Review whether managers are protecting quality and repeat bookings, because weak service can force discounting. If payroll does not support higher rates or fuller rooms, it is draining cash.

5

Facility Costs And Reserves

Facility Costs And Reserves

Retreat center overhead is heavy and mostly fixed, so owner pay depends on what is left after the building bills. The listed monthly costs are $50k lease, $12k utilities, $8k insurance, $10k property taxes, $7k maintenance, $15k software, $4k security, and $3k landscaping, or $109k per month before payroll and other operating costs.

Here’s the quick math: the plan lists $1.146M annual fixed facility cost, and the monthly lines you gave total $109k a month, or $1.308M a year. Because those bills are mostly fixed, owner pay only works after reserve funding; otherwise a good month can look safer than it is.

Reserve Before Owner Draws

Track facility cost as a share of gross profit, not just revenue. The key input is monthly fixed burn, then compare it with paid room nights and add-on cash flow. If occupancy slips, the same lease, tax, and utility bills hit harder, so owner distributions should wait until the reserve target is funded.

Watch fixed cost per sold room-night.

Set reserves before any owner draw.

Track repair and replacement timing.

Stress test slow booking months.

Watch fixed facility cost per sold room-night = annual fixed cost ÷ paid room nights. If occupancy or pricing softens, that ratio rises fast because the lease, taxes, and software do not shrink. Before owner draws, fund a reserve for the $1.0M launch capex total ($750k renovation + $250k spa equipment) and any repair spikes.

6

Wellness Retreat Center Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high wellness retreat income scenarios

Owner income planning

Occupancy, room rates, and add-on sales drive owner income more than room count alone. Fixed lease, payroll, and commissions keep the take-home spread wide across cases.

Compare the low, base, and high planning cases side by side.

Scenario

Low CaseLow planning case

Base CaseBase planning case

High CaseHigh planning case

Launch model

This is the lower-earnings path with Year 1 occupancy and pricing.

This is the modeled midpoint with Year 3 occupancy and pricing.

This is the stronger-earnings path with Year 5 occupancy and pricing.

Typical setup

30 rooms run at 55% occupancy, with Year 1 room rates, $85k add-ons, and a heavy fixed-cost base.

30 rooms run at 72% occupancy, with Year 3 room rates, $123k add-ons, and fuller staffing across wellness operations.

30 rooms run at 82% occupancy, with Year 5 room rates, $148k add-ons, and the fullest staffing and program mix.

Cost drivers

55% occupancy

$85k add-ons

15.0% variable cost rate

$830k payroll

$1.146M fixed costs

72% occupancy

$123k add-ons

14.2% variable cost rate

$1.09M payroll

$1.146M fixed costs

82% occupancy

$148k add-ons

14.0% variable cost rate

$1.12M payroll

$1.146M fixed costs

Owner income rangeBefore owner reserves

$3.49MLow planning case

$5.60MBase planning case

$7.03MHigh planning case

Best fit

Use this to stress-test launch-year cash and a slower booking ramp.

Use this as the main operating plan for lender, investor, or owner review.

Use this to test upside if occupancy stays high and add-on spend holds.

!

Planning note: Ranges are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or owner distributions; taxes, debt service, capex, reserves, and owner role can change take-home.

In this planning case, Year 1 operating profit is about $349M on $643M of revenue at 55% occupancy That is not guaranteed owner pay Taxes, debt service, reserves, capex, and reinvestment come out before distributions, so actual take-home can be much lower

Break-even depends on ramp speed, pricing, and fixed costs With Year 1 fixed facility costs of $1146M, payroll of $830k, and an 85% contribution margin, the model needs about $232M in annual revenue before owner pay, debt, taxes, or extra reserves

Not always, but the base case includes a general manager at $180k per year If the owner fills that role, payroll drops, but the owner takes on staffing, guest issues, vendor control, scheduling, and quality checks That can raise cash, but it is real work

Paid occupancy, room pricing, payroll, and property costs move cash flow the most The model uses 30 rooms, occupancy from 55% to 82%, annual fixed facility costs of $1146M, and payroll from $830k to $112M Reserves and capex reduce spendable cash

Protect owner income by filling paid rooms, holding price, controlling payroll, and reserving cash before distributions In this model, add-ons grow from $85k to $148k, but the main profit engine is room revenue Don’t treat operating profit as take-home until debt, taxes, and reserves are covered

About the author

Caleb Ross

Small Business Advisor

Caleb Ross is a small business advisor at Financial Models Lab who helps first-time entrepreneurs plan startup costs before launch. He studies common expenses, revenue drivers, and launch requirements, then turns broad business ideas into clear planning assumptions. His work focuses on pricing and profitability basics, with a practical, research-based approach to building realistic forecasts.

Choosing a selection results in a full page refresh.