How Much Does A Yacht Charter Owner Make At 35% Occupancy?

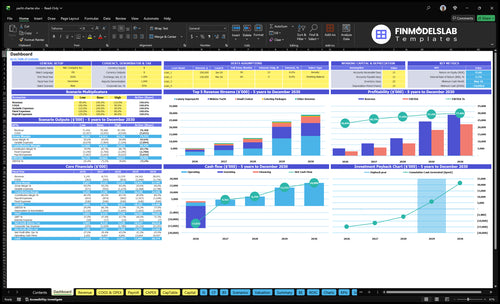

Using the researched assumptions, a yacht charter business can produce about $3064M in Year 1 EBITDA on a 3-vessel fleet at 35% occupancy That is not the same as owner take-home, because debt service, taxes, maintenance reserves, reinvestment, and any owner draw still come after EBITDA The model’s early cash need is severe, with minimum cash of negative $14048M in Month 5, driven by vessel acquisitions and setup costs Treat owner income as an adjustable distribution, not a guaranteed salary

Owner incomeNot modeledNet margin52.2%Revenue for target pay$1.35MBusiness difficultyHard

Want to test your yacht charter income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Yacht Charter model?

Yacht Charter margins can look strong, but the real answer depends on whether you mean gross margin or net margin. In Year 1, after food and beverage, fuel, broker commissions, and digital marketing, gross margin is about 82%; by Year 5, modeled variable costs fall to 15%, so gross margin reaches about 85% before payroll, fixed overhead, debt, taxes, and reserves. With fixed costs at $45k a month and Year 1 payroll at $565k, profit gets squeezed fast if crew, insurance, dockage, refits, or financing run above plan, and the startup cost context is here: What Is The Estimated Cost To Open And Launch Your Yacht Charter Business?

Gross margin drivers

Gross margin means trip-level profit.

Year 1 is about 82%.

Year 5 variable costs fall to 15%.

That implies about 85% before overhead.

Net margin pressure

Fixed costs run $45k per month.

Year 1 payroll is $565k.

Crew, insurance, and dockage bite hard.

Refits and financing can compress EBITDA.

How much revenue can a yacht charter business make?

Yacht Charter revenue can scale fast because it depends on vessel count, charter days, rate mix, and add-ons. In Year 1, with 1 small cruiser, 1 midsize yacht, 1 luxury superyacht, and 35% occupancy, revenue plus extras is about $432M on all-midweek trips, $591M on all-weekend trips, and $512M at a 50/50 mix. By Year 4, base revenue is about $2,481M with 7 vessels and 65% occupancy, but heavy debt, crew, repairs, and reserves can still cut take-home.

Year 1 revenue

1 small cruiser, 1 midsize, 1 superyacht

35% occupancy across the fleet

$432M all-midweek plus extras

$591M all-weekend plus extras

Year 4 scale

7 vessels in the fleet

65% occupancy by Year 4

$2,481M base revenue

Debt, crew, repairs, reserves can shrink take-home

Is a yacht charter business profitable if owner operated?

Yacht Charter can make money owner-operated, but it is not passive income. Here’s the quick math: the listed Year 1 team already totals $465k before the two hospitality staff, so if the owner steps in as captain or operator, payroll can drop fast. But that tradeoff can hurt availability, compliance, customer service, and the ability to scale.

Owner-led

$120k captain cost can be replaced

$465k team base shrinks

Cash flow improves if the owner works

Less room for days off or growth

Managed crew

Supports growth from 3 to 8 vessels

Keeps service more consistent

Helps with compliance and coverage

Payroll rises to $126M

Yacht Charter Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six yacht charter income drivers?

1

Booked Days

35%-70%

Occupancy rises from 35% in Year 1 to 70% in Year 5, so each vessel earns on more of the calendar.

2

Charter Rate

$4.5K-$34K

Rates move from $4,500 on a small cruiser to $34,034 on a luxury superyacht, so price changes hit owner cash fast.

3

Fleet Finance

$16.4M

The $16.43M fleet build and any debt on it sit ahead of owner pay, so financing terms shape what is left to take home.

4

Trip Costs

15%-18%

Food, fuel, broker fees, and marketing take about 18% of revenue in Year 1 and 15% by Year 5, so each point saved lifts margin.

5

Fixed Costs

$45K/mo

Marina, insurance, staff, software, and maintenance run at about $45,000 a month, so weak utilization cuts owner take-home hard.

6

Channel Mix

8%-7%

Broker commissions fall from 8% to 7%, and more direct bookings keep more cash after reserves and debt service.

Yacht Charter Core Six Income Drivers

Booked Charter Days

Booked Charter Days

Booked days are the paid days that actually make money: charter trips, events, and repeat rentals. More booked days spread fixed costs like docking, insurance, and office overhead over more revenue, so owner take-home rises. In this model, occupancy climbs from 35% in Year 1 to 70% in Year 5, and the fleet grows from 3 vessels to 8 vessels.

Do not count every calendar day as sellable. Weather, maintenance downtime, seasonality, and owner use reduce availability, so short-season markets need tight turnover planning and rate discipline. More paid days matter most when the schedule stays full without raising repair, crew, or cleaning chaos.

Track Sellable Time

Measure occupied days, lost days, and turnover days by vessel. That shows where revenue leaks out of the calendar and where extra bookings still fit before service slips. If one yacht sits idle for weather or maintenance, the lost income hits profit fast because fixed costs still run.

Track owner-use days separately.

Count weather losses by month.

Review downtime before pricing.

In a short season, use faster cleaning, earlier rebooking, and tighter handoffs to protect paid days. That keeps occupancy moving toward 70% without discounting the calendar and cutting owner income.

1

Average Charter Rate

Average Charter Rate

Average charter rate is the price per booked day, split by yacht class, weekday versus weekend, and season. In Year 1, midweek rates are $4,500 for a small cruiser, $9,000 for a midsize yacht, and $20,000 for a luxury superyacht; weekend rates rise to $6,000, $12,000, and $28,000. One higher-rate booking can add a lot of cash, but it also raises the service bar.

Here’s the quick math: revenue equals booked days × average rate. If rates grow into Year 5, the provided range reaches $5,469.80 to $34,034.20. What this hides: premium events can lift sales, but crew, food, cleaning, and guest handling must match the promise or margin falls fast.

Price to the trip, not just the boat

Track rate by vessel class, weekday versus weekend, and event type. Keep a simple sheet for quote, booked rate, add-ons, and trip cost so you can see which pricing wins actually raise take-home income. If a higher rate needs more catering, staff, or cleanup, bake that into the quote before you accept the booking.

Test whether weekend and premium-event pricing covers the extra labor and provisioning. With Year 1 direct trip costs already at 18%, a rate increase that does not lift margin just creates a busier calendar, not more profit. One clean rule: if the guest promise changes, the price must change too.

Track rate by yacht class.

Separate weekday and weekend quotes.

Log event add-on costs.

Check net margin per booking.

2

Vessel Ownership And Financing

Asset Cost and Financing

This driver is the cash tied up in yachts, refits, and launch setup before the first charter runs. The model stacks $15M for a small cruiser, $4M for a midsize yacht, $10M for a luxury superyacht, plus $150k office fit-out, $80k water sports gear, $200k booking system development, and $500k major refit; the supplied model says total listed capex is $1643M.

That matters because financing terms decide how much EBITDA — earnings before interest, taxes, depreciation, and amortization — turns into owner cash. The model shows minimum cash going negative in Month 5, so weak debt terms or thin reserves can block owner pay even if bookings start to build.

Track Cash Before Distributions

Measure the full funding stack, not just yacht price. Track vessel capex, refit spend, setup costs, debt service, and reserve balance each month so you can see when cash will tighten before charter revenue catches up.

Stress-test financing terms, draw timing, and reserve policy against the Month 5 cash gap. If the business can’t hold enough cash for early losses, owner income gets delayed even when the fleet is booked.

3

Direct Trip Costs

Direct Trip Costs

Direct trip costs are the variable costs tied to each booking: 3% food and beverage, 4% fuel, 8% broker commissions, and 3% digital marketing, or 18% total in Year 1. On a $20,000 charter, that is about $3,600 before fixed overhead and reserves. One weak trip margin can wipe out owner pay even when revenue looks strong.

This cost pool also includes captain and crew pay, guest provisions, laundry, cleaning, dockage during trips, and premium service touches. The source note says Year 5 total falls, but the figure is written as 155%, so that input needs a clean check before forecasting. Keep these costs separate from fixed overhead and maintenance reserves, or you will overstate profit.

Track costs per charter, not monthly.

Watch fuel, crew, and provisioning.

Separate trip costs from fixed overhead.

Track Gross Margin Per Booking

Measure direct trip costs as a percent of charter revenue and by vessel class. Here’s the quick math: at 18% direct cost, every $100 of revenue leaves $82 before fixed costs. If booked days, charter rate, or channel mix change, update the cost model the same week so owner draw stays real, not assumed.

Set trip-level targets for food, fuel burn, commissions, and service scope. If a booking runs hot, raise price or trim extras on the next one. One clean rule: price the trip, then police the trip.

4

Fixed Costs And Reserves

Fixed Costs And Reserves

Fixed costs hit cash flow even when a yacht sits idle. Modeled monthly burn is $45k before payroll: $15k marina docking, $12k fleet insurance, $4k office lease, $15k booking software, $10k routine maintenance, and $25k professional services. That means owner pay depends on keeping enough booked days to cover the burn, not just posting strong gross bookings.

Reserves matter because haul-outs, repairs, inspections, and refits are normal, not rare. Payroll adds $565k in Year 1 and $126M in Year 5, so cash planning has to happen before any owner draw. The key inputs are monthly fixed cost, payroll, downtime, and a reserve target for unplanned yard work. One missed refit can wipe out months of take-home income.

Build The Reserve First

Track fixed burn, then fund reserves before paying yourself. Here’s the quick math: $45k monthly fixed cost equals $540k a year before payroll, and that’s before any haul-out or repair shock. If cash on hand cannot cover downtime plus planned maintenance, owner draws should wait. Cash, not booked revenue, is the test.

Measure three things every month: reserve balance, days out of service, and fixed-cost run rate. Keep a separate line for routine maintenance versus surprise repair work, so you don’t hide real burn inside profit. If bookings are seasonal, keep more cash in the reserve because off-season idle days still carry docking, insurance, software, and payroll costs.

Track cash burn monthly.

Fund reserves before owner pay.

Separate routine and surprise repairs.

Watch downtime against booked days.

5

Booking Channel Mix

Booking Channel Mix

Channel mix is a margin driver, not just a sales choice. Year 1 broker commissions are 8% of revenue and fall to 7% by Year 5; digital marketing is modeled at 3% in Year 1 and 25% by Year 5. Direct bookings can lift owner income, but only if ad spend, sales follow-up, content, reviews, and repeat-client work stay below the fees saved.

This also shapes cash flow. Corporate events, weddings, premium private trips, catering packages, and water sports can raise revenue, but they only help if crew, food, cleaning, and guest-service costs stay controlled. One clean rule: more bookings do not help if the channel mix turns every sale into a low-margin sale.

Measure Net Profit by Channel

Track each source by gross profit per booking, not just revenue. Compare broker fees at 8% to 7% against paid media, sales labor, and content spend. Here’s the quick math: if direct sales cost more than the broker fee you avoid, the mix is hurting profit.

Bookings by source

Ad spend by source

Broker fee per charter

Sales follow-up time

Add-on fulfillment cost

Split reporting by corporate events, weddings, private trips, catering, and water sports. That shows which offers add margin and which ones add work. Keep the mix that fills dates, protects service quality, and leaves more cash for owner pay.

6

Yacht Charter Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high yacht charter owner income scenarios

Owner income scenarios

Owner income moves fast here because vessel count, occupancy, and add-on sales lift revenue, while docking, crew, fuel, and maintenance keep costs heavy.

Low, base, and high cases show how fleet size and utilization drive owner income.

Scenario

Low CaseReserve risk

Base CaseUtilization case

High CaseCapital heavy

Launch model

This is the lower-earnings path built on the Year 1 ramp.

This is the modeled middle case built on the Year 3 operating run.

This is the stronger-earnings path built on the Year 4 scale-up.

Typical setup

The model uses 3 vessels, 35% occupancy, about $5.12M revenue, an 82% gross margin, and $3.064M EBITDA before debt, taxes, and reserves.

The model uses 5 vessels, 55% occupancy, about $12.36M revenue, an 83.1% gross margin, and $8.777M EBITDA as add-on sales grow.

The model uses 7 vessels, 65% occupancy, about $24.81M revenue, an 83.8% gross margin, and $18.181M EBITDA with heavier staffing and upkeep.

Cost drivers

3 vessels

35% occupancy

base charter rates

broker fees

fixed crew and marina costs

5 vessels

55% occupancy

higher ADR mix

catering and event fees

expanded crew and maintenance

7 vessels

65% occupancy

premium charter mix

larger sales team

higher maintenance and refit spend

Owner income rangeBefore owner reserves

$3.1MRamp year

$8.8MCore case

$18.2MPeak case

Best fit

Use this to stress test the startup year when fixed costs are still high and reserve needs can bite.

Use this as the planning baseline for budgeting, hiring, and debt service.

Use this to test upside when utilization stays strong and more boats stay charter-ready.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions.

The researched case shows $3064M in Year 1 EBITDA at 35% occupancy with 3 vessels That is not owner take-home Debt service, taxes, reserves, reinvestment, and retained cash come after EBITDA The early cash gap is large, with minimum cash of negative $14048M in Month 5

The model shows breakeven in Month 1 on an EBITDA basis, but that does not mean the owner has recovered vessel capital Listed launch capex totals $1643M, including $15M, $4M, and $10M vessel purchases Cash planning matters more than accounting breakeven here

The model assumes a professional crew and operating team from the start Year 1 payroll is $565k across operations, sales, captain, engineering, chef, and hospitality roles An owner-captain could reduce payroll, but that trades cash savings for personal labor, lower scale, and less scheduling flexibility

Utilization, rates, financing, trip costs, fixed costs, and booking mix drive profit In Year 1, occupancy is 35%, variable costs total 18%, and fixed overhead is $45k per month Broker commissions alone are 8%, so channel strategy has a real margin impact

Fill more paid charter days before adding more fixed cost In Year 1, the fleet earns about $326k contribution per fully booked fleet day after 18% trip and booking costs Direct repeat clients, premium events, tight fuel control, and funded maintenance reserves improve the odds that EBITDA becomes distributable cash

About the author

Daniel Brooks

Practical Business Analyst

Daniel Brooks is a practical business analyst at Financial Models Lab, where he writes about small business budgeting and estimating what a new business can realistically earn. He creates clear, beginner-friendly content for people planning to open a physical location, with a focus on realistic assumptions, break-even explanations, and what it really takes to get a business off the ground.

Choosing a selection results in a full page refresh.