How To Open A Bell Foundry: 12–24 Month US Launch Plan

To open a bell foundry, secure compliant industrial space, permit furnace operations, install casting and ventilation equipment, hire skilled foundry staff, prove molds and tuning, and build institutional demand before launch A realistic bell foundry launch timeline is 12–24 months, mainly driven by zoning, fire approvals, furnace commissioning, utilities, and test pours The researched planning case assumes Year 1 output of 125 total units across large bells, restoration work, and table bells, producing about $1071 million in modeled revenue The practical first revenue step is to collect deposits or signed purchase orders from churches, campuses, municipalities, or institutions before full production capacity is live

Time to Open12-24 monthsSetup windowLaunch Sequence9 stagesFacility firstKey BottleneckBuildout delayApproval pathFirst Revenue StepSigned PODeposit or PO

Bell foundry launch timeline

This is a short web summary of the launch plan; the XLSX export includes the full Gantt chart with task sequencing.

Why test Bell Foundry launch assumptions before you spend?

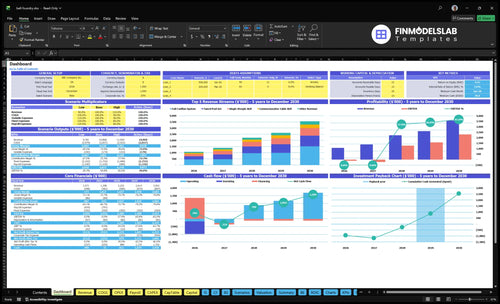

Before launch, use the Bell Foundry Financial Model Template to test timing, ramp, cash, and break-even. It shows $1.071M Year 1 revenue from 12 single steeple bells, 4 tuned peal sets, 1 full carillon, 8 restorations, and 100 table bells, plus $29.2k monthly fixed overhead before wages. The dashboard also tracks revenue ramp, gross margin, cash runway, and capacity use. Open the model now.

Financial model highlights

Staffing schedule and raw buys

Fixed overhead before wages

Runway and breakeven path

Deposits, installs, commissioning delay cash

How does a bell foundry get its first customers?

A Bell Foundry gets its first customers by selling institutional work before full production is live: churches, universities, municipalities, architects, restoration firms, historic building consultants, and bell installation partners. The quickest first revenue is deposits on steeple bells, tuned peal sets, or a carillon system, and you can track the right metrics here: What Are The Top 5 KPIs For Bell Foundry?

First buyers

Quotes come before orders.

Site review is often required.

Approvals and fundraising slow buys.

Use restoration jobs as proof.

Year 1 targets

8 historic restorations at $12,000.

100 table bells at $850.

Start with signed purchase orders.

Use smaller bells to build trust.

What mistakes should founders avoid when starting a bell foundry?

The biggest mistakes in a Bell Foundry are picking the wrong site, underestimating compliance, and treating tuning as a final touch. With $29,200 in monthly fixed overhead, a bad launch can burn cash fast, and Year 1 revenue gets very sensitive if large institutional orders shift.

Launch gates

Approve the site before signing.

Commission the furnace first.

Validate molds with test pours.

Document tuning, then ship.

Readiness risks

Check ventilation and utility capacity.

Set PPE and inspection steps.

Back up metal suppliers.

Line up rigging and installers.

How long does it take to open a bell foundry?

12–24 months is the practical startup window for a Bell Foundry if the site already has industrial zoning, enough power or gas, a clear fire review, and available furnace gear. The fastest path still depends on site approvals, utility upgrades, furnace delivery, refractory install, ventilation, and crane or hoist work, so test pours can’t start until every safety and casting system is in place. First customer delivery should wait until repeatable casting, finishing, and tone testing are proven.

Fastest path

12–24 months is the target range

Use existing industrial zoning

Secure power or gas early

Keep experienced staff on hand

Main delays

Site approvals can slow launch

Utility upgrades add months

Furnace and vent work must finish first

Test pours wait on full readiness

Bell Foundry Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Confirm whether the bell casting facility is ready for orders

Launch readiness checklist

Use this go-live approval checklist before opening to confirm the foundry is ready.

1Permits

Zoning approvedCritical

The site must allow foundry work before you spend on equipment or labor.

Environmental review clearedCritical

Open metal casting needs all local review closed before launch.

Fire marshal signed offCritical

Fire clearance has to be done before furnace heat and test pours.

2Safety

Ventilation commissionedCritical

Exhaust and air flow must control heat and fumes before melting.

Air handling testedHigh

Stable air flow protects workers and keeps the shop within spec.

PPE and spill controls setHigh

Staff need protective gear and a clear spill response before first melt.

Waste disposal approvedHigh

Metal waste and residues need a legal removal path from day one.

3Equipment

Induction furnace commissionedCritical

The furnace must run cleanly before any production pour.

Crane and hoist ratedCritical

Heavy bells need verified lift capacity before handling starts.

Floor loading and access clearedHigh

Trucks and casting loads need safe access and floor support.

Test pour passedCritical

A clean test pour proves the core process works before launch.

4Supply chain

Bronze suppliers confirmedCritical

Bronze ingot supply must be locked before the first order.

Casting and refractory stock securedHigh

Sand, clay, and refractory materials need backup stock.

Freight, rigging, installers lined upHigh

Big moves can slip, so backup crews protect delivery and install.

5Team

Roles assignedCritical

Foundry, tuning, safety, and sales tasks need named owners.

Core staff trainedCritical

People must know mold, melt, finish, and handoff steps.

Quality logs liveHigh

Logs prove each bell meets spec and tuning targets.

6Revenue

Commercial pipeline mappedHigh

Build leads from church, university, municipal, architect, restoration, and installer channels.

Quote-to-deposit flow testedCritical

No signed order or deposit means no safe launch cash.

Overhead and variable load setCritical

Load $29.2k fixed, 5% commissions, and 3% project R&D against the Year 1 ramp.

Month 25 runway coveredCritical

The model hits minimum cash at Month 25, so runway must bridge it.

Go-live signoff completeCritical

Final approval should close any gap before the first order ships.

Want to check the six bell foundry launch drivers?

1Facility Readiness

12-24 mo

Zoning, floor load, utilities, and freight access decide whether the foundry can open on time.

2Furnace Commissioning

Test pour

A stable test pour proves furnace, ventilation, and handling can run without rework.

3Bell Design and Tuning

Tone pass

Repeatable tone testing keeps bad molds and tuning errors from reaching first delivery.

4Compliance and Safety

Permit gate

Approved procedures and inspections protect the opening date and keep insurance in place.

5Supplier and Logistics

Lead times

Locked lead times for bronze, sand, rigging, and freight keep high-value orders moving.

6Team and Sales Pipeline

125 units

Trained founders, tuners, and sales staff help convert deposits into $1.07M in Year 1 revenue.

Industrial Facility Readiness

Site Fit First

Facility readiness decides whether the bell foundry can open at all. If the site cannot handle furnace heat, mold movement, finishing work, storage, and safe deliveries, you are not launching on time—you are fixing a building problem after rent starts.

Check industrial zoning, ceiling height, floor loading, ventilation routes, crane or hoist access, power, gas, water, waste handling, loading doors, and freight access before you sign. The bad outcome is a space that later fails fire, environmental, or utility review.

Verify Before You Lease

Treat landlord approval, utility review, and the inspection path as pre-close items, not afterthoughts. Site screening, layout planning, and utility checks should happen before equipment orders so you do not pay to redesign the shop later.

Map furnace and pour routes.

Confirm rigging and delivery access.

Reserve mold and bell storage.

Document fire and utility sign-off.

A ready site shortens commissioning and protects cash. If opening slips, deposits and materials can sit idle, including $1,800 in bronze alloy ingots for a single steeple bell or $55,000 for a full carillon system.

1

Furnace And Casting Equipment Commissioning

Commission the Casting Line

For a bell foundry, opening day is not when the lease starts. It is when the shop can run a documented test pour with stable heat, safe handling, and acceptable mold fill quality without rework. Until that works, the facility is still a buildout, not a production shop.

This launch driver covers furnace selection, crucibles, refractory work, mold handling, pouring tools, ventilation, hoists, finishing tools, and safety controls. One failed test pour can hold customer delivery because the bell still has to be poured, finished, tuned, and inspected before it can leave the shop.

Prove the Test Pour

Sequence the start-up around the test pour, not the install date. Verify that the furnace is delivered, the refractory has cured, ventilation changes are done, and hoists and cleanup tools are in place before you commit to first production. If any one of those slips, opening moves too.

Keep the first run narrow and controlled. Use one bell size, one pour plan, and one acceptance checklist so you can prove heat control, mold fill, finish quality, and cleanup repeatability. The goal is simple: a single steeple bell that can be poured, tuned, and inspected without rework.

Furnace and crucibles installed

Refractory cure complete

Ventilation and hoists ready

Pour tools and safety controls set

Test pour passed and documented

What this hides is the waiting chain: furnace delivery, ventilation changes, refractory cure time, and failed test pours can all push the opening date and delay the first revenue order.

2

Bell Design, Molds, And Tuning Capability

Bell Tone Readiness

The bell has to sound right, not just look right. Bell profile design, alloy consistency, pattern accuracy, mold making, controlled pouring, finishing, and bronze bell tuning all affect whether the shop can ship a bell that passes first review.

For launch, the key gate is repeatable acoustic testing with documented acceptance standards before delivery. That matters because year 1 output includes 12 single steeple bells, 4 tuned peal sets, 1 carillon system, 8 restorations, and 100 table bells, so tone work has to be ready on day one, not fixed later.

Lock Tone Testing Before Sales

Before opening, confirm who owns the tuning step, where the acoustic test happens, and how results are recorded. A foundry cannot treat tone as a late-stage fix, because weak tuning can hold up finishing, delay shipment, and create rework that ties up molds, labor, and cash. One single steeple bell can carry about $1,800 in bronze alloy ingots, while a full carillon system can reach $55,000 in alloy input.

Assign tuning labor before deposits.

Test every bell against standards.

Record results for each casting.

Reserve finishing stations for rework.

That sequence keeps first orders realistic. If mold makers, tuners, or quality records are missing, delivery dates slip fast and the shop may open with capacity on paper but not enough finished bells to serve churches, schools, or civic buyers from day one.

3

Compliance And Safety Approvals

Compliance and Safety Approvals

Compliance is what keeps the foundry open on schedule. Before the first pour, the team needs approved procedures for furnace work, PPE, fire prevention, ventilation, air handling, hazardous materials, waste disposal, and emergency access. The readiness signal is simple: trained staff, posted controls, and completed local inspections. If these checks happen after equipment install, launch risk jumps and the opening date can slip.

This driver also protects the insurance position. A bell foundry depends on site layout, furnace installation, environmental review, and insurer sign-off lining up in the right order. One clean path to first production orders means fewer shutdowns, fewer reworks, and no scramble to fix safety gaps while customers are waiting for the first bell.

Verify approvals before the first install

Start with a launch checklist that ties each safety item to one owner: training, PPE, furnace procedures, fire controls, ventilation, waste handling, and inspection prep. Get the operating procedures approved before equipment arrives, so layout changes do not break compliance. That keeps the opening plan realistic and avoids expensive rework.

Use a simple gate: no production until the site passes local inspection, the insurance file is complete, and staff can show they know the rules on day one. Approved procedures + trained staff + posted controls is the minimum bar for opening without delay.

Confirm furnace and ventilation placement first.

Document hazardous-materials and waste rules.

Train staff before test pours.

Post emergency access and fire controls.

Close inspection gaps before shipment work.

4

Supplier And Logistics Readiness

Supplier Readiness

Supplier and logistics readiness decides whether the first bells can ship on time. This business needs bronze suppliers, and where applicable copper and tin inputs, plus casting sand, clay, refractory materials, cleaning agents, packaging, freight, rigging, and installation partners. If one item slips, the whole order can stall before day one revenue starts.

Here’s the quick math: a single steeple bell may need $1,800 in bronze alloy ingots, while a full carillon system can carry $55,000 in input value. That means lead times, backup vendors, receiving space, and delivery plans are not admin work; they are launch control. One missing alloy, rigging crew, or freight plan can delay a high-value install.

Lock Inputs Before First Orders

Before opening, confirm lead times in writing and assign a backup for each critical input. The shop should know what lands first, where it lands, who inspects it, and how it moves to casting or installation. If receiving space is tight, stagger deliveries so materials do not block production or create safety issues.

Confirm backup vendors for every key input.

Book freight and rigging before deposits.

Match delivery dates to production slots.

Reserve receiving space for bulky materials.

Document install plans for each customer site.

Test one full path from inbound material to shipped bell. If packaging, freight, or installation is late, the customer still experiences a delay even if casting is finished. That’s the real readiness check: no single missing delivery should stop the first order from leaving the shop.

5

Skilled Team And Institutional Sales Pipeline

Skilled Team and Sales Pipeline

A bell foundry can’t open on time if the craft team is hired after deposits land. The launch gate is having a trained master founder, metallurgist support, mold makers, foundry technicians, finishers, tuners, a safety owner, installers, and a sales lead ready before first pour, plus a live pipeline of churches, campuses, municipalities, architects, and restoration firms.

The Year 1 load is real: 12 single steeple bells, 4 tuned peal sets, 1 carillon system, 8 restorations, and 100 table bells. If hiring trails demand, deadlines slip, tuning gets rushed, and first revenue moves later, even when the shop and equipment are ready.

Hire Before You Sell Too Far

Match staffing to the production ramp before you take serious deposits. Here’s the quick math: every job type needs both craft labor and a buyer who can keep the pipeline moving, so the first check is whether each role has a named person, start date, and backup.

Confirm each core role

Document training and signoff

Map pipeline by customer type

Test install and handoff steps

If the team is not trained before orders hit, deposits turn into backlog, not ship-ready revenue.

Start with a phased scope, not a half-ready furnace shop A lean launch can focus on restoration units, table bells, vendor-supported casting, and deposits for larger bells while permits and equipment ramp up The base model still assumes Year 1 output of 125 units, so capacity, tuning, and fulfillment must match the sales plan

First revenue can start before full launch through deposits, signed purchase orders, and restoration work The practical opening window is 12–24 months, but sales outreach should begin during site and equipment setup In the researched case, Year 1 includes 8 restoration units at $12,000 and 100 table bells at $850

Yes, the business needs real foundry and tuning expertise from day one If the founder is not the technical lead, hire or contract a master founder, mold maker, furnace operator, finisher, and tuner before taking production orders A failed test pour or poor tone can delay delivery and damage institutional referrals

The usual delays are zoning, fire review, environmental approvals, utility upgrades, furnace delivery, refractory work, ventilation, hoist installation, and failed test pours The key bottleneck is a compliant industrial site that can support furnace operations safely If site approval slips, the whole 12–24 month launch schedule can move

Build a project pipeline before the furnace is fully commissioned Start with churches, universities, municipalities, architects, restoration firms, and installers, then seek deposits or signed purchase orders Use the model to test whether those orders support $29,200 in monthly listed fixed overhead plus sales commissions and project-specific development costs

About the author

Nathan Ellis

Independent Business Researcher

Nathan Ellis is an independent business researcher who writes practical guides for people planning their first business. He focuses on small business money management, helping online business beginners turn business assumptions into a clear plan. His work uses simple revenue and profit examples and explains business costs without unnecessary jargon, keeping the numbers realistic and easy to follow.

Choosing a selection results in a full page refresh.