Why model the cement plant launch before you commit?

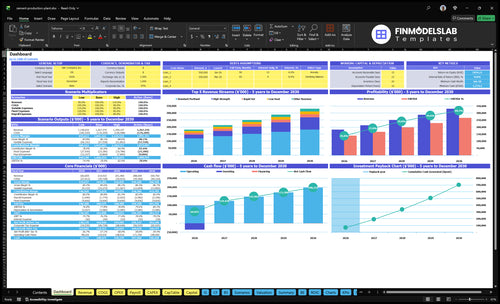

The screenshot maps launch timing, revenue ramp, runway, and break-even; Year 1 shows 136M units and $18,265M revenue, with Year 5 at 218M units and $33,075M revenue. Open the Cement Manufacturing Financial Model Template.

Financial model highlights

Launch timing and ramp

Capacity, staffing, downtime

Fuel, power, unit costs

Runway and break-even path

What do you need to start a cement manufacturing plant?

To start a Cement Manufacturing plant, you need industrial land with zoning, environmental approvals, raw material supply, production equipment, utilities, a quality lab, trained teams, dispatch capacity, and buyers; for the main operating risk, see What Is The Biggest Challenge Facing Your Cement Manufacturing Business Today?. Validate launch readiness against Year 1: 136M units, $18,265M revenue, five cement products, and $120–$180 pricing; this is not legal advice or a full cost breakdown.

Plant must-haves

Secure industrial land and zoning

Obtain environmental approvals

Lock limestone or clinker supply

Source gypsum and additives

Launch sequence

Install kiln or grinding mill

Add silos, conveyors, dust controls

Set power, fuel, water, air

Commission, run ASTM testing, onboard sales

How do you get customers for a cement manufacturing business?

You get customers for Cement Manufacturing by selling first to ready-mix producers, concrete contractors, masonry suppliers, infrastructure contractors, distributors, and negotiated offtake buyers. Sales usually open after ASTM International testing, trial loads, and delivery checks; if you want the setup cost side too, see What Is The Estimated Cost To Open Your Cement Manufacturing Business?First revenue starts when approved cement ships under buyer terms, and the Year 1 model assumes 136M units across Standard Portland, High Strength, Rapid Set, Low Heat, and Sulfate Resistant cement.

First buyers

Target ready-mix producers first

Sell to concrete contractors next

Pitch masonry suppliers for steady volume

Bid infrastructure and distributor accounts

Deal close points

Pass ASTM International cement testing

Use samples and trial loads first

Prove delivery reliability and dispatch speed

Set bulk loading, bagged packs, credit, logistics

What are the biggest cement plant launch risks?

The biggest launch risks in Cement Manufacturing are missed permits, weak fuel access, delayed kiln commissioning, and incomplete emissions controls. The clean launch path is permits to stable production to approved buyer shipments, and if buyer onboarding takes longer than commissioning, inventory and cash pressure rise before revenue settles. Here’s the quick check: test ramp, staffing, fuel and power, maintenance downtime, and cash runway before you start.

Launch bottlenecks

Underestimate permitting and timing

Miss fuel access needs

Delay kiln commissioning

Leave emissions controls incomplete

Readiness checks

Stress test ramp assumptions

Confirm utility capacity early

Run lab tests before shipment

Plan for dispatch and cash gaps

Cement Manufacturing Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Confirm whether the cement production plant is ready to open

Launch readiness checklist

Use this go-live approval checklist before opening to confirm permits, plant readiness, buyers, staffing, and cash are in place.

1Permits

Zoning clearedCritical

The plant cannot open if the site use is not allowed.

Air permit approvedCritical

Kiln and grinding emissions need approval before first run.

Stormwater plan filedHigh

Runoff control helps avoid stop-work orders and fines.

Dust control signed offHigh

Dust control is a core safety and compliance gate.

2Plant

Kiln upgrade commissionedCritical

The kiln must run safely before any cement output starts.

Grinding mill testedCritical

Mill output drives product flow and must meet spec.

Silos and storage readyHigh

Storage must hold raw material and finished goods without loss.

Bagging line readyHigh

Bagging has to work before retail and dealer orders ship.

Bulk loading provenHigh

Bulk loading must move product fast enough for dispatch.

3Supply

Clinker supply signedCritical

Feedstock continuity is the first guard against plant shutdown.

Fuel contract lockedCritical

Kiln fuel must be secured before the first operating month.

Power service confirmedCritical

Stable power is needed for grinding, packing, and controls.

Spare parts stockedHigh

Critical spares reduce downtime when equipment fails.

4Team

Plant manager onboardCritical

One owner must run daily operations from day one.

Operators staffedCritical

The plant needs enough operators to cover production and shifts.

Lab team readyHigh

Quality testing must happen before shipment and release.

Safety drill completeHigh

Emergency response needs a live practice before launch.

5Sales

Buyer approvals signedCritical

Do not open without confirmed ready-mix, contractor, or distributor demand.

Credit terms setHigh

Terms need to protect cash in a capital-heavy business.

First orders bookedCritical

Launch should start with real demand, not just interest.

Dispatch routes testedHigh

Outbound flow must support bulk and bagged deliveries on day one.

6Finance

Cash runway checkedCritical

Month 1 needs enough cash for the plant and launch ramp.

Capex funding securedCritical

Major equipment spend must be funded before go-live.

Unit economics reviewedHigh

Pricing must cover raw materials, energy, labor, and logistics.

Go-live signoff doneCritical

Open only when permits, utilities, tests, and buyers are all clear.

Which launch drivers decide if the plant opens on time?

1Permits

18–36+ mo

Permits and emissions approvals can stretch opening by 18–36+ months if the design changes.

2Site Supply

136M units

Secure feedstock for Year 1's 136M units, or the plant can run but miss volume.

3Build Out

Long lead

Long-lead kiln and mill delivery can delay dry runs, so engineering freeze and procurement must stay tight.

4Utilities

Power/Fuel

Reliable power, fuel, and water keep hot commissioning on track and limit early uptime losses.

5Quality

ASTM pass

Dry runs, lab setup, and ASTM testing turn trial output into saleable cement buyers accept.

6Sales Ready

Signed demand

Signed buyers and dispatch planning keep Year 1's 136M units moving out, not stuck in storage.

Permitting And Compliance

Permitting Before Buildout

Environmental permits can set the opening date for a cement plant. Zoning, air permits, emissions controls, stormwater, dust management, safety systems, and public review all have to line up with the final engineering design before construction is truly launch-safe. If the permit package and site plan do not match, opening can slip, and startup work can get paused.

The key dependency is site control plus final equipment specs. One clear approval path matters because construction that starts before permit conditions are settled can trigger redesign, inspection delays, and shutdown risk during commissioning.

Lock the Permit Matrix

Build a permit matrix that maps each approval to the exact drawing, control, and operating limit it depends on. Then confirm the emissions plan, monitoring setup, reporting process, and inspection calendar all match the final design before any site work starts.

Assign each permit owner.

Freeze specs before ordering.

Track public review dates.

Set monitoring before startup.

Document every signoff.

The readiness signal is approved permits matched to the final engineering design. That is what lowers the odds of a commissioning stop, because the plant can move from trial runs to day-one output without permit surprises.

1

Site And Raw Material Supply

Site and Feedstock

A cement plant can be built on schedule and still miss opening if the site cannot support quarry access, haul routes, storage, utilities, and rail or truck movement. For integrated plants, the land must also fit limestone supply and quarry planning. For grinding plants, the first-day risk is different: no dependable contracts for clinker, gypsum, and additives means no product to ship.

The readiness signal is simple: secured feedstock for the Year 1 volume plan of 136M units. If land control, raw material testing, and logistics mapping are late, the plant may be mechanically ready but unable to feed, store, or ship reliably from day one.

Lock Supply Before Buildout

Start with the site, then prove the materials. Verify land control, quarry or supplier access, and storage design before civil work gets too far. One clean rule: no feedstock plan, no launch date.

Test limestone or input quality early

Map truck, rail, and storage flow

Sign supply contracts by volume

Match delivery timing to opening month

Document backup suppliers and routes

Weak execution here creates a hard stop: the plant can run, but it cannot feed or ship without delays, shortages, or rush freight. That hits opening timing, cash needs, and first-day customer service fast.

2

Equipment, Engineering, And Construction

Equipment Build Sequence

This driver decides whether a cement plant can move from dry runs to commercial output on time. The kiln, grinding mill, preheater, dust collectors, silos, conveyors, bagging, bulk loading, lab equipment, and controls all have to land in sequence, or startup stalls even if the building is done.

The launch signal is a vendor schedule tied to install and test dates. For a plant sized to Year 1 volume of 136M units, one late long-lead kiln or mill can push the whole opening date, since civil work, electrical fit-out, and commissioning all depend on that path. Here’s the quick math: the slowest item sets the launch, not the fastest crew.

Lock the Long-Lead Path

Freeze engineering before procurement, then tie every major vendor to a dated install and test plan. Sequence factory acceptance, civil works, mechanical install, electrical controls, and punch-list closeout in one master schedule so turnover is clean. If the kiln or mill slips, protect the launch date by delaying commercial opening rather than starting half-built.

Confirm vendor ship dates

Map crane and install windows

Track test-ready turnover dates

Assign one owner per system

Document punch-list closure

What this estimate hides: a plant can look nearly done while one missing control panel or conveyor section still blocks dry runs. So check that each line item is ready for handoff before you book startup crews, fuel, and trial production. If not, cash needs rise fast while revenue stays at zero.

3

Utilities, Fuel, And Infrastructure

Utilities, Fuel, And Infrastructure

A cement plant cannot start trial runs until power and kiln fuel supply are proven. That means reliable electricity, water, compressed air, material handling, backup systems, and truck or rail access where used. If any of those are late, hot commissioning slips even if the kiln, mill, and buildings are ready.

This driver has to match the equipment load and the planned production schedule, including the Year 1 136M units volume plan. Utility studies, interconnection, metering, fuel contracts, storage, and backup plans all need to be closed before startup. No utility signoff, no first-day output.

Prove the utility stack before trial dates

Lock the full utility map early: power, fuel, water, compressed air, access roads, and rail if used. Tie each item to the commissioning checklist, then assign an owner and due date. If the load study or interconnection is still open, do not treat the startup date as fixed.

Match utility capacity to equipment load.

Confirm fuel contracts and storage.

Test backup power and backup fuel plans.

Verify truck and rail access paths.

Close metering before hot commissioning.

Build in time for utility upgrades, because that is the main bottleneck risk here. If power, fuel, or access is weak, the plant may be built but still unable to run at full pace during early ramp-up. That hits uptime, delays first sales, and forces extra cash to sit in the project longer.

4

Quality Control And Commissioning

Quality Control And Commissioning

Commissioning is the point where the plant proves it can make saleable cement again and again, not just run equipment. If the first batches miss mix consistency checks or fail ASTM International testing, opening can slip even when the plant is mechanically finished.

The launch risk is simple: the plant may be able to run, but buyers may not approve the product. Stable utilities and trained operators are the key dependency, because dry runs, hot commissioning, and mill trial runs only work if the lab, calibration, batch records, and hold-release process are already in place.

Use a strict release gate

Before opening, lock the quality manual, test plan, and calibration schedule. Set the lab up early, then run trial batches through the same steps you will use on day one: sample pull, test, record, review, and release. No shortcuts.

Assign one owner for customer sample approval and one for the hold-release process. If the first lots fail approval, they stay on hold, so plan extra working capital and time for rework, retesting, and operator coaching before commercial sales start.

Finish lab setup before hot commissioning.

Verify operator training on every shift.

Track batch records from first run.

Release only approved lots.

5

Sales, Logistics, And Customer Onboarding

Sales Commitments Before Start

Sales has to be locked before the plant opens, because first revenue depends on ready-mix buyers, contractors, distributors, infrastructure accounts, bulk delivery, bagged options, and credit terms. The plan points to 136M units in Year 1 and $18,265M in modeled revenue, which implies about $134.30 per unit. If those customers are not signed or near-final, the plant can be production-ready but still miss day-one revenue.

What this hides is simple: a cement plant can make product and still fail the launch if buyers have not approved samples, routes, pricing, or delivery rules. That means the opening date depends as much on customer readiness as on equipment readiness. No qualified demand = no clean start.

Pre-Open Customer Readiness

Set the sales stack before commissioning. Confirm sample approvals, credit setup, delivery scheduling, route planning, and service rules for each buyer type. Keep a signed or near-final demand list tied to the Year 1 136M-unit plan, not just interest emails. If a contractor or distributor needs a 10-day credit review, build that into the opening calendar now.

Approve samples before first shipment

Map truck routes and dispatch slots

Set credit limits and payment terms

Define bulk and bagged service rules

Test order flow with real buyers

Watch the bottleneck: the plant may be ready, but if customers are not qualified, cash starts late and dispatch gets messy. Day-one service depends on day-one accounts.

Start by securing an industrial site, raw material supply, environmental approvals, equipment vendors, utility capacity, operators, a quality lab, and first buyers The provided model assumes Year 1 sales of 136M units and $18265M revenue across five cement products Use those numbers to test staffing, commissioning, dispatch, and cash runway before opening

Plan on 18–36+ months for an integrated cement plant because permitting, kiln equipment, construction, utilities, and commissioning control the schedule A grinding-only plant can move faster because it buys clinker instead of making it Still, it needs storage, milling, quality testing, bulk loading, logistics, and buyer approvals before first revenue

You need a quarry or secure limestone access for an integrated plant that makes clinker You do not always need a quarry for a grinding-only plant, but you do need dependable clinker, gypsum, and additive supply Match the supply plan to the Year 1 volume target of 136M units before finalizing equipment

The common delays are air permits, emissions controls, kiln fabrication, utility upgrades, fuel supply, lab testing, and customer qualification Even if construction finishes, the plant cannot ship dependable product until commissioning and quality approvals are complete If buyer onboarding lags, first revenue can slip despite the plant being mechanically ready

Control the site and prove the launch case before ordering major equipment That means checking zoning, environmental path, raw material access, utilities, haul routes, and buyer demand In the model, Year 1 revenue is $18265M at $120–$180 per unit, so the site must support real production and dispatch volume

About the author

Timothy Dawson

Small Business Educator

Timothy Dawson is a small business educator at Financial Models Lab who helps readers understand the numbers behind everyday business ideas, with a focus on pricing, margin basics, and the common business costs that shape early decisions. He writes about the practical choices founders need to make before launch, especially when planning the first months after a business opens and evaluating whether an idea makes sense.

Choosing a selection results in a full page refresh.