How To Start A Geothermal Energy Company: 4–8+ Year Launch Path

You’re launching a power business before the first kilowatt can be sold, so the work starts with site control, resource proof, permits, drilling, interconnection, and offtake This guide keeps the scope on launch execution over a 4–8+ year planning path and uses the model period to test early ramp assumptions, including 200,000 MWh in Year 1 and 790,000 MWh by Year 5 Your next step is to turn the launch sequence into a gated plan before committing to drilling and construction

Time to Open48-96 monthsLaunch runwayLaunch Sequence8 stagesResource firstKey BottleneckInterconnection gateUtility reviewFirst Revenue StepPPA saleGrid live

Geothermal launch timeline

Short web summary of the launch plan; the XLSX export has the detailed Gantt Chart.

How long does it take to start a geothermal energy company?

For Geothermal Energy, plan on 4–8+ years to reach commercial operation; that’s a research-based planning assumption, not a guarantee. The critical path starts with land control, then resource confirmation and drilling, while permitting, environmental review, transmission interconnection, equipment lead times, and offtake negotiations all have to stay aligned with the commercial operation date (COD). If any of those slip, the whole schedule moves.

What has to happen first

Land control comes before drilling.

Reservoir data must support financing.

Plant design follows well results.

Interconnection studies must match COD.

Where delays show up

Weak wells can force redesign.

Environmental review can add more work.

Queue congestion slows grid tie-ins.

Year 1 assumes 200,000 MWh, and Year 5 assumes 790,000 MWh, so a late COD pushes every revenue line.

What are the biggest geothermal energy launch risks?

The biggest launch risks in Geothermal Energy are a weak reservoir, late grid interconnection, and shaky offtake; if heat, permeability, flow rate, depth, or injection performance do not support the plan, the project should not clear the next capital gate. That matters because the model has to hit 200,000 MWh in Year 1, then move from 50 to 100 units of capacity availability in Year 4, with a real revenue ramp in Year 5.

Reservoir and grid risk

Check heat and depth early

Test permeability and flow rate

Verify injection performance first

Start interconnection on time

Commercial and operating risk

Lock PPA timing before drilling

Secure REC and carbon proof

Prepare commissioning and safety

Model runway through all phases

How do you start a geothermal energy company?

Start a Geothermal Energy company by proving the resource first, then locking site control, geothermal rights, permits, grid interconnection, offtake, equipment, and operations before commercial operation; use What Is The Main Indicator That Shows Geothermal Energy's Growth Potential? to anchor the core growth test. Here’s the quick math: 200,000 MWh in Year 1 at $75/MWh equals $15.0 million of power revenue before REC, capacity, heat, or carbon offset revenue.

Prove the resource

Screen heat, depth, water, and access.

Secure site control and surface access.

Confirm geothermal and subsurface rights.

Drill, test, and prove reservoir output.

Build the launch path

Enter the interconnection queue early.

Start offtake talks before final design.

Line up EPC vendors and plant equipment.

Commission wells, controls, metering, and grid sync.

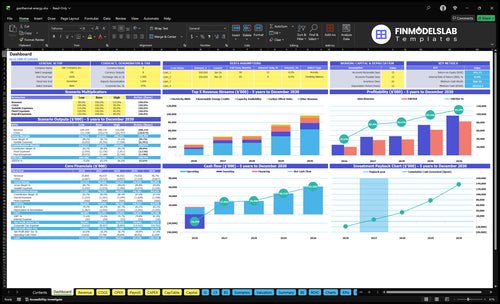

Geothermal Energy Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Check whether the geothermal project is ready for commercial operation

Launch readiness checklist

Use this go-live approval checklist to confirm geothermal energy is ready before opening.

1Rights

Land rights securedCritical

You need clear control of the site before drilling, plant work, or lender review starts.

Subsurface rights confirmedCritical

Geothermal heat use depends on rights below the surface, not just the land lease.

Water access documentedHigh

Injection and pumping plans need legal water access where the reservoir requires it.

Surface easements mappedHigh

Access roads, pipes, and power lines can stall launch if easements are missing.

2Permits

Permitting path mappedCritical

You need one approved path before filing, sequencing, and field work.

Environmental studies completeCritical

Environmental findings drive permit conditions and can block construction.

Drilling permits approvedCritical

No rig work should start without drilling approval from the right agencies.

Safety procedures writtenHigh

Crew safety rules need to be in place before field crews mobilize.

3Drilling

Rig contract lockedCritical

A firm rig plan keeps the well schedule from slipping in the opening window.

Well testing plan readyCritical

Test results prove the reservoir can support the launch forecast.

Injection strategy approvedHigh

Injection design affects pressure control and long-run field performance.

Plant vendors selectedHigh

Turbine, controls, and maintenance vendors must be set before installation starts.

4Grid

Interconnection queue checkedCritical

If queue status is unclear, power sales can be delayed or blocked.

Grid compliance confirmedCritical

The plant must meet grid rules before export and dispatch can start.

Capacity plan approvedHigh

Year 1 assumes 50 capacity availability units, so the contract path must fit.

Revenue channels confirmedCritical

Pick the first revenue path: PPA, utility offtake, aggregator, merchant, REC, or carbon.

5Team

Project roles staffedCritical

You need named owners for development, drilling, commercial, and finance.

Operations crew trainedHigh

Plant and field crews need clear handoffs before first operating month.

Compliance owner assignedHigh

Reporting, safety, and permit tasks need one accountable person.

Commissioning plan signedCritical

Missing commissioning steps raise start-up risk and delay first revenue.

6Financials

Year 1 model testedCritical

Test 200,000 MWh, 50 capacity units, and 100,000 offset units against cost checks.

Direct costs reviewedHigh

Maintenance, labor, grid, and REC costs must fit the model before launch.

Cash trough fundedCritical

The model shows minimum cash at Month 9, so funding must cover that dip.

Go-live signoff issuedCritical

Don't launch if reservoir data, interconnection status, offtake path, or commissioning plan is missing.

Want the six launch drivers that matter most?

1Resource Validation

200k MWh

Tested reservoir data supports the 200,000 MWh Year 1 plan and avoids a bad drill-out.

2Land Rights

Site control

Signed site and subsurface control lowers diligence risk and keeps drilling and buildout moving.

3Permitting

Permit matrix

A clear permit matrix prevents late surprises that can push drilling or construction back.

4Drilling

Rig slots

A drilled, tested well program proves commercial flow before plant build starts.

5Grid Offtake

COD revenue

A workable interconnection path and offtake terms make Year 1 revenue credible before COD.

6Commissioning Ops

First bill

Commissioning checks, training, and metering turn a built plant into first billing after COD.

Resource Validation

Resource Validation

Resource validation is the first launch gate for a geothermal plant. You have to prove the reservoir can deliver heat, permeability, flow rate, depth, injection performance, and enough generation to support permits, financing, and plant design. If the tested data does not support the 200,000 MWh Year 1 assumption, the project should not move into major buildout.

This is what keeps the opening plan real. A weak reservoir can turn a promising site into a redesign, delay, or stop decision after drilling spend is already sunk. Here’s the quick math: the forecast rises from 200,000 MWh to 790,000 MWh by Year 5, which is about a 3.95x ramp, so the early test program has to prove commercial headroom, not just a single good well.

Validate Before Major Spend

Run the work in order: desktop screening, geoscience studies, exploration drilling, well testing, reservoir modeling, and generation forecast review. Tie each step to a go or no-go decision, so the team knows when to advance, redesign, or stop. The readiness signal is tested reservoir data strong enough to back the plant size and the first revenue case.

Document the inputs that matter to lenders, engineers, and permit teams: temperature, depth, flow rate, injection response, drilling risk, and expected output by year. If testing shows poor flow or weak injection, fix the plan before buying major equipment. That protects cash, keeps the schedule honest, and reduces the chance of missing first-day operating capacity.

Heat profile and reservoir temperature

Permeability and fluid movement

Flow rate from test wells

Injection performance and pressure response

Generation forecast for Year 1 and Year 5

1

Land And Geothermal Rights

Secure Site Control Early

Geothermal projects can’t start drilling, build wells, or pour concrete until the legal footprint is locked. You need surface access, the geothermal lease, any needed mineral or subsurface rights, plus easements, road access, transmission corridor rights, and water access where relevant. One missing right can stop the whole site, even if the resource looks good.

This matters more when the plan targets 200,000 MWh in Year 1 and 790,000 MWh by Year 5, because that output depends on long-term control of the exact land needed for drilling, plant buildout, interconnection, and O&M access. Signed control also makes financing diligence cleaner and cuts late legal surprises.

Verify Every Right Against the Footprint

Start with title review, then match every parcel, easement, and access route to the actual project map. Confirm the lease covers the full wellfield, plant pad, roads, transmission path, and any water needs. If the project footprint and legal rights do not line up, fix that before drilling or construction commitments.

Check title and subsurface rights.

Align leases with the footprint.

Document road and corridor access.

Close gaps before capital spend.

Clean legal control keeps permitting, lender review, and contractor mobilization moving. If access is still conditional when rigs or crews are booked, launch timing slips fast, and day-one operating access can be weaker than the build plan assumes.

2

Permitting And Environmental Approval

Permitting Readiness

For a geothermal plant, permitting is the gate that decides whether drilling can start on time. If federal, state, local, tribal, or Bureau of Land Management approvals are still open, the project can’t move cleanly into capital-heavy work, and the Year 1 200,000 MWh case can slip.

This step includes NEPA review where needed, drilling permits, water use, air permits, wildlife review, construction approvals, and grid-related compliance. The real risk is not just a denied filing; it’s added environmental work that shifts drilling or construction timing after money has already been committed.

Build the permit matrix early

Before you book a rig or pour concrete, build a live permit matrix with owners, status, dependencies, and decision gates. That keeps agency meetings, baseline studies, application filings, public comment tracking, and compliance planning in one place so delays show up early, not after spend.

Assign one owner per permit.

Map federal, state, local, tribal layers.

Track water, air, wildlife, and grid items.

Link each filing to a decision gate.

If the matrix is missing, the project can look ready while key approvals are still moving. That is how drilling starts late, construction pauses, and the ramp to 790,000 MWh by Year 5 gets pushed right along with it.

3

Drilling And Technical Execution

Drilling Execution

Geothermal launch timing lives or dies on production wells, injection wells, and the rig schedule. If the drilling plan cannot prove reservoir flow and support plant design, you should not move from feasibility into construction. One weak well can reset both the budget and the opening date.

This driver includes contractor selection, rig slot booking, well design, safety planning, well testing, and the data handoff to engineering. The main risks are poor flow, deeper-than-expected drilling, rig delay, or well remediation. If testing data does not support commercial operation, the first-day operating plan is not real yet.

Lock the drilling plan before committing capital

Before opening, verify the drilling program approval, contractor availability, testing plan, injection strategy, spare parts, and contingency plans. Here’s the quick check: if the wells cannot feed the plant at the expected rate, the launch date slips and the construction budget is exposed.

Book rig time early.

Confirm well design.

Plan safety reviews.

Define testing handoffs.

Set remediation triggers.

Keep engineering, drilling, and operations on one timeline. If the test results change the reservoir picture, update plant design and cash needs before more spend goes out. That way, the project only advances when technical evidence supports commercial operation.

4

Grid Interconnection And Offtake

Grid Path And Offtake

Geothermal plants do not open on day one unless the grid path and revenue path are both real. That means queue position, transmission studies, metering, protection systems, and utility reliability rules must line up with a signed sale route, such as a PPA (power purchase agreement), utility offtake, corporate buyer, aggregator, capacity market, or REC and carbon sales.

The risk is simple: queue congestion can slow interconnection, and weak offtake terms can make Year 1 revenue shaky even if the plant is built. If the project cannot show a feasible grid path and a credible contract or market route, COD may happen before cash starts flowing.

Lock The Commercial Gate Early

Start interconnection application, study management, contract negotiation, REC certification planning, and settlement setup before late construction. The launch file should show who owns each step, what the utility or market requires, and what still blocks first billing. One clean test: can the project explain how power will move, get measured, and get paid?

Confirm queue status and study scope.

Map metering and protection requirements.

Set PPA, REC, and settlement owners.

Test merchant exposure assumptions.

Document carbon offset sales timing.

If offtake talks drag, use shorter contract terms, staged volume, or a market route to keep the Year 1 revenue case credible before COD.

5

Commissioning-Ready Operations

Commissioning-Ready Operations

When the plant is built, the launch risk shifts to a built-but-not-billable site. Commissioning-ready operations means the controls, safety steps, metering, and reporting all work before the commercial operation date and first bill. If startup tests fail or data is wrong, you can miss first revenue even with a finished plant. That matters when Year 1 output is planned at 200,000 MWh.

This driver covers turbine testing, grid synchronization, reservoir monitoring, compliance reporting, REC reporting, and carbon offset tracking. It also needs operator training, emergency procedures, spare-parts setup, and a clean handoff from construction to operations. If first-day metering or dispatch is weak, settlement errors and safety issues can hit cash flow right when the project should start earning.

Commission the plant before the bill

Build a commissioning checklist with named owners, test dates, and sign-off gates tied to COD and first billing. Verify controls, alarms, metering, vendor response, and reporting workflows before energizing so the team can move from test mode to live operation without rework. One clean handoff now saves a lot of pain later.

Start by proving the resource before you build the company around it Secure site control, geothermal rights, permits, drilling partners, interconnection progress, and an offtake path The planning model assumes Year 1 output of 200,000 MWh at $75/MWh, but that revenue only matters after commissioning and commercial operation

Plan for 4–8+ years from serious development work to commercial operation The range comes from resource testing, environmental review, drilling, grid studies, equipment procurement, financing, and offtake negotiation If drilling results are weak or the interconnection queue stalls, the opening month can move even when the plant design looks ready

You need utility-grade expertise on the team, even if the founder is not a former utility executive Bring in geothermal reservoir, drilling, power markets, permitting, interconnection, and plant operations talent early Year 1 assumptions include 200,000 RECs, 50 capacity availability units, and 100,000 carbon offset units, so reporting and compliance skills matter

The biggest delays come from reservoir uncertainty, permits, drilling setbacks, interconnection studies, and offtake terms A project can control land and still fail if heat, permeability, flow rate, or injection performance does not support power generation Enter the grid queue early and model revenue timing before you lock the full launch plan

The first step is a gated readiness review before final commissioning Confirm reservoir data, operating permits, interconnection requirements, metering, safety procedures, staff coverage, maintenance vendors, and offtake billing First revenue can come from electricity, RECs, capacity, heat sales, carbon offsets, or merchant sales, but only after the plant is commissioned

About the author

Victor Shaw

Practical Business Analyst

Victor Shaw is a practical business analyst at Financial Models Lab who writes about small business budgeting and estimating what a business can earn. He helps aspiring small business owners build realistic assumptions, understand break-even points, and compare business opportunities with greater clarity. His work focuses on simple, credible financial analysis that turns rough ideas into grounded expectations for real-world decision-making.

Choosing a selection results in a full page refresh.