How To Start An Insurance Agency In 60–120 Days With Carrier Access

Insurance Agency

You’re opening a licensed insurance agency, so the launch path starts with producer licensing, entity setup, errors and omissions coverage, carrier access, systems, and a first-client pipeline This guide uses a 60–120 day launch window and a 5-year planning model to pressure-test timing, revenue ramp, marketing, staffing, and readiness before the first policy is bound

Time to Open8-12 weeksSetup windowLaunch Sequence6 stagesLicense firstKey BottleneckCarrier gateApproval pathFirst Revenue StepPolicy boundCommission earned

Launch timeline

Short web summary of the launch plan; the XLSX export holds the detailed Gantt chart.

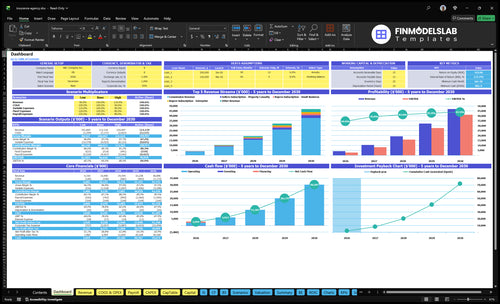

The screenshot shows revenue, costs, cash needs, assumptions, and breakeven logic. Open the Insurance Agency Financial Model Template to test launch timing, producer ramp, commission revenue, renewal assumptions, staffing, marketing spend, cash runway, and breakeven. Inputs cover 90% Year 1 variable commission, $0 fixed commission per order, 500% property and casualty, 400% life and health, 100% specialty lines, 700% individual, 250% small business, 50% enterprise, $1,200 individual AOV, $3,500 small business AOV, $10,000 enterprise AOV, $8,650 monthly overhead, and 75% variable operating load.

Model tabs to check

Revenue ramp charts

Lead cost and runway

Breakeven and staffing

How do you get clients for a new insurance agency?

For a new Insurance Agency, clients come from trust before scale, so start with referrals, local partnerships, niche targeting, online quote requests, cross-selling, community relationships, and tight follow-up. If you want the cost side, see How Much Does It Cost To Open An Insurance Agency?; the Year 1 model assumes $200,000 for buyer marketing at $20 CAC, or 10,000 buyer leads, plus $150,000 for seller acquisition at $500 CAC, or 300 seller relationships. The real bottleneck is follow-up discipline and carrier fit, because a $1,200 premium only throws about $108 in commission at a 90% rate.

Where clients start

Use referrals from first bound policies.

Build local partner relationships.

Pick one niche early.

Turn quotes into bound policies.

What the numbers say

$1,200 premium = $108 commission.

$3,500 premium = $315 commission.

$10,000 premium = $900 commission.

Follow-up and carrier fit decide wins.

Should you start an independent or captive insurance agency?

Choose the model that matches your readiness, not the one that sounds better on paper. An independent Insurance Agency gives you more carrier choice and branding control, but you usually need carrier appointments, aggregator access, cluster membership, or franchise support; a captive setup can speed training and market entry, but it narrows carrier choice and branding. The real test is simple: can you show a clear quote-to-bind path for the first policies?

Independent

More product choice

Needs carrier access

Needs lead sources

Needs service capacity

Captive

Faster launch support

More training help

Less branding freedom

Less carrier flexibility

Match your Year 1 mix to the model: 500% property and casualty, 400% life and health, and 100% specialty lines. Don’t pick the model before you confirm your license lines, carrier access, lead source, service capacity, and commission economics.

Best fit signals

License lines are set

Carrier access is real

Lead flow is proven

Commission math works

Common launch mistakes

Model chosen too early

Service capacity ignored

Lead source untested

Quote-to-bind path unclear

What licenses do you need to start an insurance agency?

Your Insurance Agency needs an active resident insurance producer license first; it lets the founder legally sell policies, and the chosen lines of authority set the product mix before launch. Use What Is The Main Goal You Want To Achieve With Your Insurance Agency? to tie licensing choices to revenue goals, because carrier appointments usually come after licensing.

Core licenses

Get a producer license before selling policies.

Pick lines: P&C, life, health, or specialty.

Follow state exams, fingerprints, and background checks.

Use nonresident licenses for multi-state sales.

Launch ready

50 states and D.C. regulate producers.

Some states require an agency entity license.

California requires 24 CE hours per 2-year term.

Add E&O coverage and a compliance workflow.

Insurance Agency Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Confirm what must be ready before accepting insurance clients

Launch readiness checklist

Use this go-live approval checklist before opening to confirm the insurance agency can sell, bind, and service policies.

1Licensing

Resident producer license activeCritical

You need the right license before you can sell or bind.

Lines of authority match productsCritical

Sell only the lines your license covers.

Agency entity license confirmedHigh

Some states require a separate agency filing.

Background checks completedMedium

Clean screening helps meet carrier and state standards.

Continuing education plan setMedium

Keep renewals from slipping after launch.

2Entity

Entity and tax registration doneCritical

This keeps contracts, taxes, and payouts in the right legal name.

Business bank account openCritical

You need one clean account for commissions and expenses.

Errors and omissions policy boundCritical

E&O protects you if advice or placement goes wrong.

3Carriers

Carrier appointments signedCritical

No appointment means no clean path to bind business.

Contract terms approvedHigh

Commission, authority, and payout rules must be clear.

Aggregator agreement reviewedMedium

Use this only if you plan to work through one.

4Systems

Agency management system liveCritical

This is the system of record for policies and tasks.

CRM, rater, email, and phone readyHigh

You need fast quoting and a clean client contact path.

Document storage and privacy setHigh

Store files and protect customer data from day one.

E-signature, payment, and records testedHigh

The handoff must work without manual fixes.

5Staffing

Founder producer coverage assignedCritical

Someone has to sell on day one.

Licensed backup producer scheduledHigh

Coverage keeps sales moving if the founder is out.

Customer service responsibilities assignedHigh

Clear ownership prevents missed calls and delays.

Training on quote and disclosure scriptsHigh

Staff need to say the right thing the same way.

6Go-live

Referral and online leads routedCritical

Lead sources should produce quotes from day one.

Quote-to-bind flow testedCritical

A prospect should move to issued policy without a gap.

Renewal diary and claims setHigh

Servicing can't wait until the first problem shows up.

Year 1 model tied outCritical

Tie the model to 90% commission, $8,650 fixed spend, $150k seller, and $200k buyer marketing.

Go-live signoff approvedCritical

Launch only when licensed, appointed, insured, and system-tested.

Want the six launch drivers at a glance?

1Licensing

60-120d

License and compliance clear the legal gate, so first policy sales can start on time.

2Carrier Access

Live quotes

Appointments unlock quoting and binding, which speeds first revenue and expands what you can sell.

3Product Mix

P&C-led

A clear mix of P&C, life, and specialty lines cuts wasted quotes and tightens carrier fit.

4Agency Systems

Quote-to-bind

A tested quote-to-bind system reduces manual rework and keeps compliance files clean from day one.

5Lead Pipeline

$200K / $20

The $200K buyer budget and $20 CAC need active referrals and campaigns to turn into bound policies.

6Service Capacity

1 FTE

Clear service roles protect renewals and free the founder to keep selling after launch.

Licensing And Compliance

Licensing and Compliance

For an insurance agency, active resident insurance producer licensing is the gate to legal selling. If the lines of authority don’t match the product mix, the agency may open with no bindable products on day one, which slows first policy activity and can force a launch reset.

The launch file also needs the agency entity license where required, background checks cleared, an E&O insurance policy, a continuing education plan, and clean recordkeeping. License before appointments and entity before contracts are the key dependencies here.

What to verify before opening

Start by selecting the exact products you will sell, then match the license to those lines. A property and casualty launch needs different authority than life and health, so the filing has to reflect the real launch mix. If the state approval is delayed, your opening date can slip even if the website and sales team are ready.

Before launch, complete prelicensing if required, pass the exam, file the state application, form the entity, register the agency, and document all disclosures. Keep a simple compliance file so appointments, contracts, and renewals do not stall later. One wrong line can block first revenue.

Select lines of authority first

Clear background checks early

File entity and agency registrations

Set E&O and CE tracking

1

Carrier Access And Appointments

Carrier Appointments

Carrier access decides what you can quote, bind, and service on day one. Without a signed appointment, aggregator access, cluster agreement, franchise approval, or captive contract with clear binding authority, the agency can look open but still miss first revenue. The launch path has to match the product mix, because the wrong access can block quotes and delay cash from the first policy sold.

The gate is simple: active license, agency entity, and insurance coverage in place. Before carrier review, prepare the agency profile, E&O certificate, license proof, business plan, niche focus, and production expectations. If due diligence slows down or appointments are limited, the agency may need to quote through an aggregator first and move to direct appointments later.

Prelaunch Checks

Start with access, not marketing. Confirm which carriers you can quote, which ones let you bind, and which service tasks you can handle at launch. Then match the niche to the access path so the agency does not sell coverage it cannot place or service.

Verify active license and entity status.

Collect E&O and license proof.

Set niche and production targets.

Map direct, aggregator, and captive paths.

Test quote-to-bind authority before opening.

Document service limits and escalation steps.

If approvals slip, first revenue slips too. That can leave staff underused, waste lead spend, and frustrate early buyers when quotes stop at intake. A narrower access path is fine for launch, but only if the team knows the exact binding rules and service limits before opening.

2

Product Mix And Niche Strategy

Niche and Product Fit

Your launch speed depends on whether the niche, line of authority, meaning the legal class of insurance you can sell, and carrier access all match. If you market a product you cannot bind, you waste quotes, delay first revenue, and frustrate buyers. The disclosed Year 1 mix is 500% property and casualty, 400% life and health, and 100% specialty lines, so day-one readiness has to match that product plan.

The buyer mix also shapes the sales cycle and staffing. The model leans 700% individual, 250% small business, and 50% enterprise, and that changes how much service load you carry at opening. A small business niche needs commercial carrier access and more follow-up than simple personal lines. Here’s the quick math: the tighter the niche, the fewer dead-end quotes and the faster the first policy can bind.

Verify Bindable Coverage First

Before opening, lock the niche, then map each product to the exact license, appointment, and underwriting appetite needed to sell it. Build scripts around only the products you can bind on day one, and stop any marketing that points buyers to lines still waiting on approval. That keeps the launch from filling the pipeline with quotes the agency cannot close.

Match niche to live carrier access.

Test scripts against bound products.

Document underwriting limits by line.

Assign one owner for product fit.

Review every ad before launch.

3

Agency Technology And Workflow

Agency Tech Stack

This launch driver is what makes quoting, binding, documents, renewals, and compliance work on day one. If the client intake, quote request, comparative rater, carrier portal access, document storage, CRM, renewal diary, and service workflow are not tested, the team falls back to manual rework and missed follow-up, which slows opening and hurts first revenue.

The key dependency is live carrier access. You can configure screens without it, but you cannot prove the quote-to-bind path, so launch risk stays high. Here’s the quick math: software overhead runs $1,500 a month in general licenses plus $1,000 in marketing platforms, or $2,500 before the workflow is clean and the compliance file set is ready.

Test the Full Quote Path

Set up the agency management system first, then load permissions, carrier credentials, intake forms, and retention reminders in that order. A lead should move from intake to quote request to bound policy to stored documents without anyone copying data twice. If any step breaks, fix it before opening.

Verify intake routes cleanly.

Test carrier quote access live.

Store policy docs in one file.

Auto-create CRM tasks and notes.

Check renewal diary alerts.

Treat missed follow-up as a launch blocker, not a cleanup task. Set service workflow tasks for quote follow-up, policy delivery, renewals, and compliance records before day one, because one gap can drop a lead and leave the file incomplete.

4

Lead Pipeline And Referral Readiness

Referral-Ready Lead Flow

If the lead pipeline is not live before opening, the agency may have licenses and carriers but still sit idle. Insurance closes on trust and fast follow-up, so day one needs ready referral partners, a working quote form, and a set response cadence. Slow replies or weak carrier fit can turn warm leads cold and delay bound policies.

Here’s the quick math: $200,000 in Year 1 buyer marketing at $20 CAC implies up to 10,000 buyer acquisitions if the funnel works cleanly. $150,000 in seller acquisition marketing at $500 CAC implies 300 seller targets. What this hides is simple: those leads only matter if tracking, scoring, and follow-up are live before launch.

Build It Before Open

Before opening, verify the pieces that turn interest into policies: named referral partners, a local outreach list, online quote form, niche landing pages, campaign tracking, and a renewal cross-sell plan. Build the quote request workflow now, not after launch. One clean rule: every inbound lead needs an owner, a response target, and a next step.

Match leads to carrier fit.

Set a same-day follow-up cadence.

Track source, quote, bind rates.

Test the renewal cross-sell path.

If leads come in without carrier fit, the team burns time on quotes it cannot bind. That slows the commission ramp, hurts the customer experience, and makes early cash flow less predictable. If response speed slips, referral partners lose confidence fast, and the launch starts with noise instead of revenue.

5

Service Capacity And Retention

Service Capacity and Retention

An insurance agency can open on time only if someone owns service from day one. If the founder is also selling, every quote intake, bind follow-up, and policy delivery task steals time from new business, so missed calls and slow responses show up fast in retention and referrals.

The readiness signal is clear: owner role, licensed producer coverage, a renewal diary, and a clean claims handoff. In the model, a CEO or founder starts in Month 1 at 10 full-time equivalent where data is provided, so the service load has to match that capacity before first policies bind.

Day-One Service Workflow

Set the service map before launch. Assign who handles endorsement requests, certificate requests, renewal reviews, and client communication, then document the escalation path for claims and urgent issues. If the founder is solo, keep the workflow tight because every extra handoff slows sales and hurts follow-up.

Use a simple launch check: one owner, one backup producer, one customer service path, one renewal diary, and one clear status on every open item. Small teams should lock role clarity before payroll expands, because weak service structure turns into churn, not growth.

Start with licensing, entity setup, E&O coverage, carrier access, systems, and a first-client pipeline A practical launch window is 60–120 days The model assumes 90% Year 1 commission, $0 fixed commission per order, and a starting product mix of 500% property and casualty, 400% life and health, and 100% specialty lines

Plan on 60–120 days for a typical US launch The main timing drivers are exam scheduling, license approval, agency entity setup, E&O underwriting, carrier appointments, and software setup If direct carrier access takes longer, an aggregator, cluster, franchise, or captive path may reduce the time to quote and bind policies

Prior experience is not always a formal requirement, but it lowers launch risk You still need the right producer license, lines of authority, and carrier access The model’s first-year economics assume real sales execution: 90% commission, $20 buyer CAC, and average premiums of $1,200 for individuals and $3,500 for small businesses

Carrier appointments and licensing delays are the biggest launch blockers Some steps cannot start until the license, agency entity, and E&O coverage are active The 60–120 day launch range assumes these dependencies are managed early, while software, referral outreach, and intake workflows can be built during the approval period

First revenue happens when the agency binds a policy and earns commission Under the Year 1 model, a 90% commission equals about $108 on a $1,200 individual policy, $315 on a $3,500 small business policy, and $900 on a $10,000 enterprise policy Awareness alone does not create revenue

About the author

Lucas Hart

Local Business Observer

Lucas Hart writes for Financial Models Lab as a local business observer focused on simple cash flow planning for people turning a service idea into a business. He explains business costs in plain language and shares startup budget examples to help readers make practical decisions before launch.

Choosing a selection results in a full page refresh.