How to Start a Jewelry Making Business in 4 to 10 Weeks

You can open a jewelry making business by proving a small collection, setting prices, lining up suppliers, preparing photos, and opening sales channels before launch month This guide covers the 4 to 10 week launch path, with financial checks tied to Year 1 assumptions like $107 average unit price, $30 CAC, and Month 34 breakeven

Time to Open4-10 weeksSetup windowLaunch Sequence6 stagesDesign firstKey BottleneckMaterials gateLead timeFirst Revenue StepFirst orderLaunch collection

Launch Timeline

Short web summary of the launch plan; the XLSX export contains the detailed Gantt Chart.

Yes, Jewelry Making usually needs setup paperwork before the first sale, but the exact license mix depends on your state, city, sales channel, and craft market rules; use What Is The Most Important Indicator Of Success For Your Jewelry Making Business? alongside this compliance check so revenue tracking starts clean. This is not legal advice: 45 states plus Washington, DC have statewide sales tax, while 5 states do not, so tax setup can delay launch if ignored.

Check Before Selling

Register the business where required

Get a sales tax permit

Use resale certificates for wholesale buys

Confirm local home-business rules

Launch-Ready Means

Verify FTC Jewelry Guides, 16 CFR Part 23

Set craft fair and marketplace paperwork

Carry product and general liability insurance

Keep claims, invoices, policies, and records

What mistakes should you avoid when starting a jewelry business?

When starting Jewelry Making, don’t launch with weak pricing, shaky quality, or vague policies. In Year 1, modeled direct and variable costs hit 195% of revenue before fixed costs and payroll, so bad pricing can burn cash fast. Price from materials, labor, packaging, platform fees, marketing, returns, and profit, and verify every claim on metals, stones, handmade work, and limited editions.

Skip these launch mistakes

Avoid unclear niche.

Avoid poor photos.

Avoid unreliable suppliers.

Avoid missing policies.

Fix readiness before orders

Set custom-order rules first.

Build pricing from real costs.

Limit made-to-order burnout risk.

Check launch claims before opening.

How long does it take to start a jewelry business?

Jewelry Making can launch in 4 to 10 weeks if you keep it lean, hand make the first pieces, and skip custom orders or a studio buildout. Add wholesale accounts, complex materials, or custom work, and the timeline stretches into Month 3 to Month 6. Here’s the quick math: design first, then source beads, metals, stones, findings, packaging, and care materials; tools and equipment are modeled in Month 1 to Month 3, photography in Month 2 to Month 3, and packaging plus website work can keep running through Month 6.

Lean launch

Start with design first.

Source core materials next.

Model tools in Month 1 to Month 3.

Expect 4 to 10 weeks for launch.

Main delays

Supplier delays slow stock.

Photo setup lands in Month 2 to Month 3.

Packaging can run Month 3 to Month 5.

Sales tax setup can stall launch.

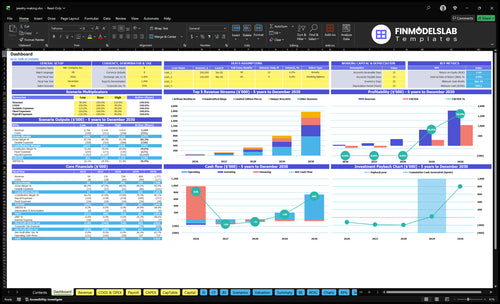

Jewelry Making Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Confirm whether the jewelry business is ready to sell

Launch readiness checklist

Use this go-live approval checklist to confirm the jewelry making business is ready before opening.

1Compliance

Business registration filedCritical

You need a legal entity before permits, taxes, and vendor accounts.

Sales tax permit confirmedCritical

Sales tax setup should be live before the first online or market sale.

Local rules reviewedHigh

Home-studio, studio, and market rules can block launch if missed.

Claim rules checkedHigh

Metal, gemstone, handmade, and limited-edition claims must match the law.

2Studio

Tools installedHigh

Tools must work before you build the first order.

Workspace clearedHigh

A safe bench and storage setup keeps output steady.

Security and utilities readyMedium

Power, access, and theft protection should be set before stock arrives.

3Supply

Backup vendors listedHigh

Backup supply keeps best sellers from going out of stock.

Initial stock orderedHigh

Opening stock should cover the first sales push.

Restock trigger setMedium

You need a clear rule for fast restocks on top sellers.

4Products

SKU list finalizedHigh

Each item needs a code so inventory and sales stay clean.

Care cards readyMedium

Care notes cut returns and help customers handle pieces right.

Photos and listings liveCritical

Ready means photos, pricing, shipping, tax, and policies are live.

Return policy postedHigh

Clear returns reduce dispute risk and speed first sales.

Order tracking worksHigh

Customers need tracking before the first shipment goes out.

5Pricing

Price sheet approvedHigh

Year 1 pricing should hold near the $107 average unit price.

Cost mix checkedCritical

Modeled direct and variable costs are about 19.5% of revenue.

Marketing budget setHigh

The Year 1 budget is $12,000, so spend needs a plan.

CAC target setHigh

Year 1 CAC is $30, so paid spend must stay disciplined.

6Cash

Owner capacity checkedCritical

The owner must cover the first orders with current time and skills.

Year 1 staffing mappedHigh

Year 1 assumes 1.0 lead artisan and 0.5 production assistant.

Cash runway reviewedCritical

Cash needs to survive the Month 34 break-even and Month 37 cash dip.

Launch signoff completeCritical

Final signoff confirms the launch is ready to open.

Which launch drivers matter most for handmade jewelry?

1Product Line Readiness

4-line set

A clean necklace, ring, bracelet, and limited-piece line speeds listings and cuts custom back-and-forth.

2Supplier and Material Reliability

$8K stock

Documented suppliers and backup components reduce stockouts and keep best sellers repeatable.

3Pricing and Margin Validation

AOV $118

Pricing that covers the 195% direct and variable cost load keeps each order from compounding losses.

4Sales Channel Setup

Live shop

Live listings, payments, tax, and shipping settings turn launch prep into first revenue.

5Photography and Brand Presentation

$3K setup

Clear photos, scale shots, and notes lift trust and cut pre-sale questions.

6Production Capacity and Fulfillment

1.5 FTE

A repeatable make, pack, and ship workflow limits late orders and launch burnout.

Product Line Readiness

Product Line Readiness

When shoppers can’t tell what’s for sale, launch slows fast. This jewelry line needs a cohesive SKU list across necklaces, rings, bracelets, and limited edition pieces so buyers can order without custom back-and-forth on day one. The Year 1 mix is 40% necklaces, 30% rings, 20% bracelets, and 10% limited edition pieces.

The launch depends on material availability and repeatable build steps. Too many one-off designs create the bottleneck: slower listings, messy photos, and more fulfillment errors. One clean line-up also makes it easier to write care notes, set size and variant choices, and define where custom orders stop.

Lock the SKU system before photos

Start with the niche, then name each SKU, choose sizes, and set only the variants you can build again. Write care notes for each piece and set clear custom-order boundaries so launch orders do not turn into manual design work.

Confirm the core product mix.

Approve every SKU name.

Standardize sizes and variants.

Prepare launch inventory.

Test repeatable build steps.

Here’s the quick test: if a customer can place an order, read the care notes, and know the delivery path without a message thread, the line is ready. If not, opening day will be slower and the first batch of orders will take longer to ship.

1

Supplier and Material Reliability

Supplier and Material Reliability

Open on time only works if the parts show up in the right spec. For jewelry, that means documented suppliers for beads, findings, metals, stones, packaging, and backup components. The launch risk is simple: if one piece is late or inconsistent, you can’t finish orders, restock best sellers, or keep quality steady from day one.

The readiness signal is real paperwork, not verbal promises. Keep test samples, record material specs, track lead times, approve substitutions, and store invoices for product claims. Planned stock is $8,000 of raw materials in Month 3 to Month 4 plus $3,500 of packaging in Month 3 to Month 5, so supplier slips can hit cash and launch timing at the same time.

Lock Material Specs Before Launch

Start with sample testing, then freeze the exact spec for each core input. If the finish, size, or stone grade changes, repeatability drops and customer complaints rise. Use one approval list for main suppliers and backups, so a missing bead or clasp does not stop production.

Confirm lead times in writing.

Save invoices for every material.

Approve substitute parts before launch.

Match packaging to order volume.

Here’s the quick math: if a best seller depends on one delayed component, you risk stockouts and missed restocks. A clean supplier file lowers that risk and helps first-day orders ship on time.

2

Pricing and Margin Validation

Pricing and Margin Validation

This driver decides whether each sale funds the next one or hides a loss. With Year 1 prices of $120 necklaces, $90 rings, $70 bracelets, and $180 limited edition pieces, the weighted unit price is about $107 and AOV is about $118 with 11 units per order.

But direct and variable costs are 195% of revenue, so the launch starts underwater unless pricing rules are set before opening. Here’s the quick math: at $118 AOV, variable cost is about $229.10 per order, before the $2,849 monthly fixed load and payroll.

Set price floors before you open

Build a SKU-level cost sheet for every necklace, ring, bracelet, and limited edition piece. Include materials, direct labor, shipping, packaging, platform fees, marketing, returns, and profit. Then set a floor price, a bundle rule, and a wholesale boundary so the founder and any sales help use the same numbers on day one.

Test 10% and 20% discount math.

Model bundle pricing before launch.

Set wholesale floor by SKU.

Check costs against every sample.

Approve price changes in writing.

Before opening, run one real cart test at the target mix: 11 units and about $118 AOV. If the cart loses cash at launch, fix the price sheet first; otherwise the first orders can drain stock and cash faster than new sales replace them.

3

Sales Channel Setup

Sales Channel Setup

This driver decides whether shoppers can buy on day one. If live listings, payment processing, tax settings, shipping profiles, return policy, and order notifications are not live, the launch slips from selling to “still setting up.”

Pick one primary channel and one proof channel. For this jewelry brand, that keeps early demand focused, avoids inventory spread, and gives cleaner feedback on which pieces, photos, and prices actually convert.

Launch with one path first

Use the easiest full checkout path first, then add a second channel only after packing, shipping, and reply times are stable. The channel mix can include Etsy for marketplace demand, Shopify for owned ecommerce, Instagram for discovery, craft fairs for local proof, boutiques for consignment, and custom commissions for higher-touch orders.

Verify product photos and pricing.

Test payment, tax, and shipping rules.

Load return policy and order alerts.

Keep inventory tight to avoid oversells.

Use one proof channel, not three.

Here’s the risk: opening too many channels before fulfillment is stable ties up cash in packaging and inventory, and it makes customer messages, returns, and order timing harder to manage. If the setup is clean, first revenue starts faster and the early feedback is easier to trust.

4

Photography and Brand Presentation

Trust-First Product Photos

Online buyers cannot touch size, weight, clasp, texture, or stone detail, so this launch depends on a full photo set before listings go live. The readiness signal is clear product photos, scale shots, hand or model images, sizing notes, care instructions, packaging images, and copy that stays consistent with the piece.

The photo and lighting setup is modeled for Month 2 to Month 3 at $3,000, and website development plus branding run from Month 1 to Month 6 at $4,000. If those assets slip, the opening can miss its date or go live with weak trust, which usually means more pre-sale questions and slower first orders.

Shoot the Full Listing Set

Build the content in the same order customers decide: each SKU, then size, then finish, then packaging. Write claims carefully so the photos and listing copy match what ships on day one. That keeps the launch from getting stuck in review, upload, or approval loops.

Verify every listing before opening: images, sizing notes, care card, packaging, and web copy. If one piece is missing, the buyer still has to ask. That adds service load on day one and weakens the trust signal the shop needs to convert traffic.

Shoot every SKU.

Show packaging clearly.

Add scale and hand shots.

Match copy to the product.

Approve claims before launch.

5

Production Capacity and Fulfillment

Production Capacity and Fulfillment

For a handcrafted jewelry launch, this driver decides whether orders ship on time from day one. The business needs a repeatable flow from order intake to making, quality control, packing, shipping, returns, and customer messages, or late orders and owner burnout start fast.

The setup also carries real cash and timing pressure. Tools and equipment are modeled for Month 1 to Month 3 at $15,000, and the launch plan assumes a staffed production base with a lead artisan plus 05 production assistant. If labor time is underestimated, capacity looks fine on paper but breaks at launch.

Lock the workflow before the first sale

Set batch days, custom-order cutoffs, and a quality checklist before opening. Also define shipping supplies, SKU storage, and a clear repair or return policy. That gives the team one path for every order, so fulfillment stays consistent when volume picks up.

Test the full loop with real timing: intake, making, check, pack, ship, and reply. If any step takes longer than planned, adjust order caps before launch, not after. That helps protect delivery reliability and keeps the first weeks from turning into a backlog problem.

Start with a small, repeatable collection, then set prices, source materials, photograph products, and open one sales channel A practical launch can take 4 to 10 weeks Use the model checks early: Year 1 average unit price is about $107, AOV is about $118, and CAC is modeled at $30

In the provided model, breakeven occurs in Month 34, with payback in 50 months That assumes Year 1 marketing of $12,000, Year 1 EBITDA of -$107,000, and a ramp toward $297,000 EBITDA in Year 4 Launch speed helps, but pricing, repeat purchases, and capacity drive the longer path

Insurance is a practical launch check, especially if you sell at markets, ship products, invite customers into a studio, or use higher-value materials The model includes business insurance at $100 per month Also verify venue rules, local requirements, and product claim documentation before you sell

The biggest delays are supplier lead times, unfinished photos, unclear pricing, and production workflows that cannot handle orders The model places tools in Month 1 to Month 3, photography in Month 2 to Month 3, raw material stock in Month 3 to Month 4, and packaging in Month 3 to Month 5

Build a launch-ready SKU list before opening the store Include product names, prices, variants, materials, care notes, photos, packaging, shipping rules, and return terms Then test the math: Year 1 direct and variable costs total 195% of revenue before fixed costs, payroll, and marketing

About the author

Simon Reed

Small Business Educator

Simon Reed is a small business educator at Financial Models Lab who helps service business founders understand the numbers behind everyday business ideas. He focuses on pricing and margin basics, common business costs, and the first months after launch, giving readers a clearer view of what it takes to build a healthy business. Simon brings a simple, confident approach that balances optimism with cost-aware planning.

Choosing a selection results in a full page refresh.