The fastest first customers for a Pop-Up Yoga Studio come from presold class packs, corporate wellness sessions, apartment community classes, local event sessions, and partner-hosted classes. Use the Year 1 pricing plan of $20 for a single class, $18 per class-pack visit, $45 for a workshop, and $200 for a corporate wellness session, and tie every offer to a confirmed place and date; How Much Does It Cost To Open, Start, And Launch Your Pop-Up Yoga Studio? can help you match that offer to your launch spend. Underfilled classes are the warning sign, so focus first on attendance proof and cash collected before you add more locations.

Fast first sales

Presell class packs first.

Sell $200 corporate sessions.

Book apartment and event dates.

Use email, SMS, and referrals.

What to measure

Track cash before more locations.

Promote only confirmed venues.

Watch for underfilled classes.

Fix lead time and venue fit.

How long does it take to start a pop-up yoga studio?

A Pop-Up Yoga Studio usually takes 4 to 8 weeks to start. The fast path is one private venue, one instructor, limited class formats, and presold tickets; the slower path is public-space permits, multiple partners, or corporate approvals. Don’t promise an instant launch until the venue is confirmed, insurance is active, waivers are signed, payments work, and the day-of checklist is ready.

Fastest launch path

4 to 8 weeks is the realistic range.

Use one private venue first.

Keep one instructor and simple formats.

Sell presold tickets before day one.

What slows launch

Public-space permits take time.

Insurance certificates can delay approval.

Instructor scheduling adds friction.

Local marketing and booking setup also take lead time.

What do you need to open a pop-up yoga studio?

You need venue permission, insurance, signed waivers, qualified instructors, safe space controls, booking, payments, and local permit checks to open a Pop-Up Yoga Studio; there isn’t one national permit rule because city, park, event, and venue rules vary. Build the launch around 20 billable days and 40% occupancy in Year 1, then use What Is The Most Effective Way To Measure The Success Of Pop-Up Yoga Studio? to track if one venue is ready before expanding.

Launch checklist

Register the business first

Confirm venue permission in writing

Request insurance certificate

Prepare participant waiver

Operating rules

Set class capacity before sales

Publish schedule and booking page

Collect payment before arrival

Send reminders to reduce no-shows

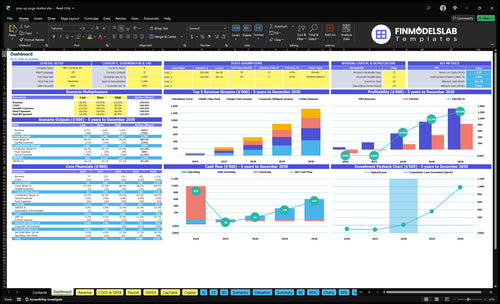

Pop-Up Yoga Studio Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Confirm every item needed before the first paid pop-up yoga class

Launch readiness checklist

Use this go-live approval checklist before opening the pop-up yoga studio.

1Compliance

Business registration filedCritical

You need a legal entity before venue contracts, insurance, and payment accounts go live.

General liability boundCritical

The model uses $250 monthly insurance, so coverage must start before any class.

Venue permit path clearedCritical

Check local rules for parks and public events before booking your first pop-up.

2Site

Site agreement signedCritical

A signed venue deal prevents last-minute venue loss and protects the class schedule.

Capacity limits confirmedHigh

Safe headcount keeps the class within space, layout, and insurer limits.

Power access testedMedium

Audio and lighting need reliable power if the pop-up site does not provide it.

3Equipment

Mats and props readyHigh

Portable mats, blocks, and straps must be on hand for each class.

Sanitation supplies stockedHigh

Cleaning supplies protect shared gear and keep the space ready between sessions.

Safety layout rehearsedCritical

Rehearsal helps staff set spacing, exits, and flow before guests arrive.

4Staff

Instructor credentials verifiedCritical

Verified credentials lower safety risk and support venue and client trust.

Substitute coverage assignedHigh

A backup instructor keeps classes running if the lead teacher misses a session.

Teaching flow trainedMedium

The team should know opening, pacing, and wrap-up so classes feel consistent.

5Booking

Booking system liveCritical

Guests need a working way to reserve spots before the first class.

Payments processed successfullyCritical

Payment flow must clear charges or the launch will lose revenue fast.

Waiver and reminders setHigh

Waivers and reminders reduce liability and no-shows before each session.

6Finance

Year one pricing checkedHigh

Match Year 1 prices to 20 billable days, 40% occupancy, and model costs.

Cash runway covers Month 25Critical

The model shows minimum cash of $745k at Month 25, so cash planning is key.

Launch signoff approvedCritical

Open only when venue, insurance, waiver, and payment flow are all ready.

What drives a clean pop-up yoga launch?

1Venue Readiness

4-8 wks

A written venue agreement and permit status control whether classes can open on time.

2Instructor Programming

5 formats

Confirmed coverage and class formats reduce cancellations and make the first sessions consistent.

3Portable Setup

$6K kit

A tested transport kit keeps setup fast and delivery consistent across rented spaces.

4Safety & Waivers

$250/mo

Active insurance and waivers let venues approve dates and cut last-minute cancellation risk.

5Booking Flow

Live page

A live class page turns interest into paid reservations instead of manual follow-up.

6Presales & Partners

40% occ

Presales and partners fill early classes faster and show which locations actually fit.

Venue And Permit Readiness

Venue and Permit Readiness

Venue choice controls launch timing for a pop-up yoga studio. It sets capacity, weather exposure, customer access, pricing, and whether you can repeat classes. Before you publish a booking page, you need a written venue agreement, a known headcount limit, confirmed class dates, and permit status checked. No venue means no launch date.

Shortlist private venues, parks, community spaces, apartment communities, and event partners. If a space needs host approval or a public permit, treat that as a launch gate, not a side task. With $250/month general liability insurance and a waiver flow ready, approvals move faster. If that work slips, presales can start too soon and the first class can get canceled.

Lock Permission Before Promotion

Verify the venue, permit rules, insurance certificate, waiver process, weather plan, and parking or entry instructions before you open sales. If access is unclear, day-one check-in gets messy and the class starts late. One missing approval can block the booking page, because you cannot promise dates you do not control.

Get the signed venue agreement first.

Write max capacity on paper.

Confirm permit status with the host.

Test backup plans for rain.

1

Instructor Readiness And Class Programming

Instructor Readiness

When the instructor calendar is not locked, the business cannot promise class dates, substitutions, or capacity from day one. For a pop-up yoga studio, that creates launch delays, last-minute cancellations, and a weak first customer experience because the calendar, credential file, class formats, and backup coverage are not in place.

The Year 1 staffing plan depends on 1 owner-operator, 1 lead yoga instructor, 0.5 marketing and community manager, and 0.5 admin and operations coordinator. If even one class type has no backup, the team cannot cover beginner, outdoor, workshop, corporate, and private sessions without trimming the schedule or turning away booked guests.

Lock the class map first

Before launch marketing starts, confirm the instructor’s calendar, credentials, and substitution plan. Then assign each format to a clear audience: apartment residents, office teams, or weekend event guests. That keeps the booking plan realistic and helps the team open with fewer cancellations and a cleaner customer experience.

Confirm backup teacher coverage.

Publish beginner and outdoor formats.

Match corporate and private sessions.

Test one full weekly schedule.

2

Portable Setup And Equipment

Portable Setup Readiness

If the kit is not packed, tested, and easy to move, launch day slips. For a pop-up yoga studio, the equipment is the studio, so readiness means a packed, transportable kit checked before the first paid class. Missing mats, blocks, straps, sanitation supplies, check-in materials, signage, audio, or weather backup can slow setup and make a rented space feel improvised.

The source-listed setup cost is $6,000: $3,000 for yoga equipment, $1,500 for portable sound and lighting, $1,000 for signage, and $500 for a transport cart. That spend supports safer classes, faster load-in, and a more consistent experience across parks, rooftops, and other temporary spaces.

Build the move-ready checklist

Before selling dates, verify the full load-in path: storage, transport, venue rules, and any power or weather limits. Test one complete setup end to end, then fix anything that slows the move from vehicle to class floor. The bottleneck risk here is slow setup or poor participant experience.

Mats, blocks, and straps

Sanitation and check-in items

Signage and portable audio

Lighting if needed

Weather backup supplies

Transport cart and storage bins

3

Insurance, Waivers, And Safety

Insurance, Waivers, And Safety

For a pop-up yoga studio, this is a launch blocker because venues may ask for proof of coverage before they confirm dates. No certificate means no space, and no space means no booking page, no presales, and no first-day revenue. The model includes $250 per month for general liability insurance, but that cost only helps if the policy is active and the venue accepts the certificate.

Readiness means more than buying insurance. You need active insurance, a venue-approved certificate, a signed waiver flow, an emergency procedure, instructor credentials on file, and a local permit check. If any one of those is missing, a venue can delay the class, cancel the date, or pause the booking page. One missing document can stop the whole launch.

Verify proof before you open sales

Confirm requirements with the venue, insurer, and local authority before you publish dates. That keeps the launch plan real. For pop-up yoga, the order matters: insurance first, then venue approval, then waiver flow, then permits and safety steps. If the venue wants a certificate naming it as additional insured, get that in writing so you do not lose the date later.

Get the certificate approved early

Test waiver signing on mobile

Save instructor credentials in one file

Write a simple emergency plan

Check permit rules by location

Weak execution here shows up fast as a canceled event, an unpaid booking page pause, or a last-minute customer refund. Strong execution lowers launch risk and builds venue trust, which helps you lock dates faster and start serving day one without avoidable compliance gaps.

4

Booking, Payment, And Customer Communication

Booking, Payment, and Customer Flow

This has to work before marketing starts. For a pop-up yoga studio, the booking flow is the proof that a class can actually run: a live class page, capacity limits, payment collection, confirmations, reminders, cancellation policy, waitlist, and day-of check-in. If any of that is manual, you risk lost sales, confused guests, and a launch that looks ready in ads but isn’t ready in real life.

The key input is a clean setup that turns interest into paid reservations. Set prices, publish the schedule, connect payment processing, and test mobile checkout before you spend on ads or partnerships. The Year 1 model assumes 15% payment processing fees plus $150/month for website and software, so the system has to support paid seats from day one.

Build the checkout path first

Verify the full customer flow on a phone, not just desktop. Test price display, class capacity, payment, confirmation message, waitlist, cancellation policy, and arrival instructions. One clean checkout. If checkout breaks, marketing only creates unpaid demand and the opening date slips while you fix preventable errors.

Set capacity before publishing.

Test one paid booking end-to-end.

Prepare reminders and check-in.

Document cancellation and waitlist rules.

Assign someone to check each class page before launch and again the day before each event. A broken link, missing reminder, or unclear check-in note can turn a full class into no-shows and refunds. Keep the payment and messaging setup simple enough that one person can run it without same-day manual work.

5

Presales And Local Partnerships

Presales And Local Partners

For a pop-up yoga studio, paid presales are the cleanest proof that a class will fill before you add more dates or locations. If people only like a post or say “interested,” you still don’t know if a room, park, or rooftop will pay on day one. The real readiness signal is confirmed class dates with paid attendance, plus a route to repeat that demand.

This driver shapes launch timing because weak presales usually show up as underfilled classes, slow cash, and too many empty slots to cover the venue plan. Use the first offers to test fit: $20 single classes, $18 class-pack visits, $45 workshops, $200 corporate sessions, and $200 merchandise sales monthly. If local partners do not help move real bookings, venue expansion is too early.

Sell Before You Scale

Before opening more locations, verify that each partner can drive paid signups, not just awareness. Ask host venues, apartment managers, and event organizers to share booking links, then track which channel fills seats first. Use email or SMS lists for direct reminders, because those contacts can convert faster than social likes and are easier to measure.

Start with one target audience, one viable venue, and one paid class format Then confirm permission, insurance, waivers, instructor availability, booking, payments, and customer reminders The researched launch window is 4 to 8 weeks, with Year 1 planning based on 20 billable days, 40% occupancy, and $20 single classes

Plan on 4 to 8 weeks if you move in sequence A private venue with clear approval can be faster than a public park or event site that needs permit checks The slow points are usually venue approval, insurance certificates, instructor schedules, booking setup, and enough local marketing time to fill the first class

No, a pop-up yoga studio is built around temporary or rented spaces You can use private venues, community rooms, apartment spaces, event sites, or approved outdoor areas Still, each location needs permission, capacity rules, safety planning, and sometimes permits The model assumes $800 monthly admin office rent, not a permanent class studio lease

Venue approvals delay launches more than equipment does Permit checks, proof of insurance, waiver setup, instructor substitutions, weather planning, and unclear cancellation terms can also slow the first paid class If you’re targeting 20 billable days per month in Year 1, repeatable venue access matters more than chasing too many one-off sites

Prove one location can sell, run smoothly, and repeat Use presold class packs, workshops, or a $200 corporate wellness session to test demand before expanding Watch occupancy against the Year 1 40% assumption, check payment and waiver completion, and confirm that setup, check-in, cleanup, and customer communication work without founder heroics

About the author

Ryan Spencer

First-Time Founder Guide Writer

Ryan Spencer writes for Financial Models Lab, where he focuses on launch budget planning and simple launch planning for first-time founders. He helps readers estimate startup needs before opening a physical location, breaking down business costs in clear, practical language. His work is built for people who want a realistic view of what it really takes to open a business, so they can plan with more confidence and fewer surprises.

Choosing a selection results in a full page refresh.