The dashboard and launch assumptions tabs in the Precision Machining Financial Model Template test launch timing and break-even. Year 1 uses 1,500 aerospace brackets, 300 implants, 2,000 housings, 1,000 gears, and 2,500 connectors, for about $397M revenue. Open it now.

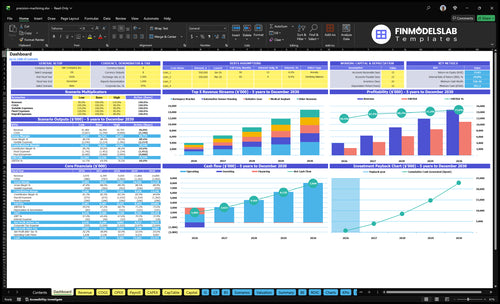

Financial model highlights

Monthly ramp chart

Part-family contribution

Labor load chart

Machine use and staffing

Cash runway to breakeven

What do you need to start a precision machining business?

For Precision Machining, you need a production cell that can quote, cut, inspect, document, and ship Year 1 work across 5 part families: aerospace brackets, medical implants, automotive sensor housings, robotics gears, and fluid connectors; What Is The Most Critical Measure Of Success For Precision Machining? helps tie that setup to measurable shop performance. The minimum practical setup is industrial space with adequate electrical service, CNC mills or lathes matched to target parts, tooling, workholding, fixtures, coolants, consumables, raw material vendors, CAD/CAM, inspection equipment, skilled operators, quote templates, revision control, and a delivery process; customer-required certifications vary by industry and contract.

Minimum Shop Setup

Secure suitable industrial workspace

Confirm adequate electrical service

Match CNC machines to parts

Stock tooling, fixtures, and coolants

Operating System

Build CAD/CAM workflow

Use inspection equipment

Control quotes and revisions

Plan delivery by contract

What mistakes create the biggest machine shop launch risks?

Precision Machining launch risk starts when owners buy machines before they validate the target work, then skip inspection planning and quote too loosely. That leads to poor fit, missed tolerance checks, hidden labor and rework, slow material flow, and cash strain before sales are steady.

Setup mistakes

Pick machines after work type

Skip documented inspection steps

Delay supplier setup

Take complex parts too early

Cash and quote risks

Hide tooling in quotes

Miss labor and material load

Open without customer pipeline

Skip pre-opening sales outreach

How long does it take to start a CNC machine shop?

For Precision Machining, the researched planning window is 3 to 9 months, and the real driver is whether the site clears lease approval, zoning, and power work on time. Start with the facility and electrical capacity, then machines, tooling, inspection setup, test parts, quotes, and first jobs; machine lead times, rigging, calibration, material suppliers, and hiring can all move the opening month. If you sign customers before you can prove tolerances, delay risk goes up fast.

What sets the timing

3 to 9 months is the range

Lease approval can slow launch

Zoning fit can block the site

Electrical capacity can force upgrades

What comes first

Facility and power come first

Then machines and tooling

Then inspection and test parts

Then quotes and first jobs

Build a day-one precision machining readiness checklist

Launch readiness checklist

Use this go-live approval checklist before opening the machining shop and taking customer orders.

1Compliance

Entity setup completeCritical

A clean legal setup is needed before permits, accounts, and contracts move.

Insurance boundCritical

Coverage should be active before staff work or customer parts are handled.

Permits and zoning clearedCritical

The shop cannot go live until the site is approved for machining use.

2Site

Power load supports CNCsCritical

Machines need stable power before install, testing, and first jobs.

Air and ventilation readyHigh

Compressed air and ventilation affect machine function and worker safety.

Coolant handling approvedHigh

Coolant storage and disposal must be set before production starts.

3Equipment

CNC centers installedCritical

The core machines must be in place before any customer order can run.

Test cuts meet toleranceCritical

Test parts prove the process can hit the required accuracy.

CAD/CAM workflow documentedHigh

Clear programming steps cut scrap, rework, and quoting mistakes.

4Supply

Tooling and fixtures stockedHigh

Without fixtures and tooling, setup time rises and jobs slip.

Raw material suppliers approvedCritical

Material supply has to be locked before the first production run.

Inspection gear calibratedCritical

Measurement tools must be ready so parts can be accepted or reworked.

5Team

Operators trained on setupHigh

Staff need to know setup, run, inspect, and rework steps.

Quote intake liveCritical

A working intake flow is needed before the first customer request lands.

Revision control activeHigh

Revision control keeps drawing changes from turning into bad parts.

6Finance

Cash covers Month 2 troughCritical

Minimum cash is about $951k in Month 2, so runway must cover the setup trough.

Year 1 revenue model checkedHigh

Year 1 output totals 7,300 units and about $3.97M in sales.

Go-live signoff completeCritical

Final signoff should confirm compliance, equipment, supply, staff, and cash.

Want the six launch drivers that control opening readiness?

1Facility Power

3-9 mo

Power, air, and floor checks keep machine delivery from slipping the open date.

2Machine Setup

Test cuts

Calibrated machines prove parts can hold spec before first customer quotes.

3Tooling Supply

Stocked

Tools, fixtures, and material rules cut idle time and speed first jobs.

4Inspection Ready

QC ready

Inspection steps and records help parts pass customer acceptance on the first run.

5Skilled Workflow

7.3K units

Cross-trained staff keep quoting, setup, machining, and shipping moving without one-person bottlenecks.

6Customer Pipeline

$3.97M

Named targets and quote follow-up turn proven capacity into paid orders faster.

Facility And Power Readiness

Facility and Power Readiness

If the shop space is not ready, the launch stops before the first part ships. A precision machining shop needs a zoned workspace, floor capacity, rigging access, ventilation, compressed air, coolant handling, and adequate electrical service so machines can be installed and used on day one.

The key dependency is finishing power and access checks before machine delivery. If those checks slip, you can end up paying for equipment that cannot be installed, which pushes out opening month and breaks day-one production flow.

Verify the space before delivery

Start with the lease review, then confirm utilities, machine layout, safety setup, and the waste handling process. Do not lock delivery dates until the space can take the machine, the service load, and the rigging path.

Confirm electrical service first

Map machine placement and clear paths

Test air, coolant, and ventilation

Document safety and waste handling

A clean handoff here cuts opening-month delays and gives the floor a smoother start instead of a crowded, stop-and-start first week.

1

Machine Acquisition And Commissioning

Machine Acquisition and Commissioning

This is the point where the shop becomes real. If the mill or lathe is matched to the work, safely rigged, calibrated, and proven with test parts, you can quote with confidence and open on time. If delivery slips or test cuts fail, day-one production stalls and the first jobs for brackets, housings, gears, and connectors move with it.

Here’s the quick read: equipment fit plus commissioning proof is the launch gate. The setup only works when facility power and rigging access are ready, because late machine delivery or bad install work can turn a funded buildout into dead time and extra cash burn.

Plan the install before the truck arrives

Lock the machine list to the target part mix first, then verify power, floor load, rigging path, and delivery dates. The founder should document install steps, leveling, programming, and test-cut signoff so each machine is accepted only after it makes parts that meet spec.

Use a simple readiness check: delivery booked, rigging approved, power verified, programs loaded, and test parts passed. If any one of those is missing, opening-day capacity is shaky, quote promises get soft, and the shop starts behind on its first revenue jobs.

2

Machine acquisition and commissioning includes selecting the right mills or lathes, arranging delivery, installing and leveling the equipment, loading the first programs, and proving the setup with test parts. For precision machining, that matters because customers buy accuracy and repeatability, not just machine hours. If the machine is not dialed in, the shop may be open on paper but not ready to ship usable parts.

The main inputs are machine specs, part tolerances, facility power, rigging access, delivery timing, and operator time for setup and test cuts. A failed commissioning run can delay the first paid jobs, force rework, and push out cash collection. One clean test part run is the launch signal: the equipment can hold spec, the programs work, and the shop can take on early orders without guessing.

Match machine capacity to target parts.

Confirm power before delivery is booked.

Check rigging access and floor space.

Level and calibrate before first cuts.

Run test parts and document results.

Hold launch if specs are missed.

Tooling, Fixtures, Materials, And Suppliers

Tooling And Supplier Readiness

For a machining shop, this driver decides whether the first jobs run on time or sit idle. Stocked cutting tools, workholding, fixtures, coolant, consumables, and approved raw material vendors have to match the target part mix and machine selection before opening, or you risk waiting on parts instead of cutting them.

Here’s the quick risk: idle machine time waiting for tools or material pushes out quotes, slows first revenue, and forces rush buys that hurt margin. Set minimum stock levels, vendor setup, material specs, fixture plans, and tool-life tracking before day one.

Build Reorder Rules Early

Do the setup before the first PO lands. Verify approved vendors, list each raw material by grade and form, and tie every tool and fixture to the parts you plan to quote. If a part needs a special cutter or vise, order it now, not after the customer accepts the job.

Also write simple reorder rules for fast movers and long lead items. One missing cutter can stop a machine, so track usage, set reorder points, and test the full flow from quote to setup to first cut. That keeps the opening realistic and protects day-one capacity.

3

Inspection And Quality Readiness

Inspection Readiness

Inspection and quality readiness is what lets a machining shop get parts accepted on day one. If you can’t verify dimensions, revision level, and tolerance limits before the first shipment, finished parts can sit in the shop instead of turning into revenue. For high-spec buyers, the first question is simple: can you prove the part matches the print?

The launch dependency is the customer’s tolerance requirements. That means the shop needs measuring tools, written inspection steps, revision control, and a clear rule for nonconforming parts. Certifications may matter by customer and industry, but they are not universal launch requirements, so the real bottleneck is whether finished parts can be checked and documented fast enough to ship.

Build the Check System First

Before opening, buy the gauges and metrology tools that match the tightest parts you plan to quote, then write the inspection steps for each part family. Train operators on what to measure, when to stop the job, and how to record results so the shop does not rely on memory.

Link inspection to quoting, too. If a job needs tighter checks, more records, or extra handling for nonconforming parts, that cost belongs in the quote. The goal is simple: no part should leave the shop unless the revision, dimensions, and accept/reject path are already defined.

Verify customer prints and revisions first.

Match gauges to required tolerances.

Store inspection records by job.

Define rework and scrap steps.

4

Skilled Labor And Production Workflow

Skilled Labor Coverage

For precision machining, launch risk is usable capacity, not just hiring names on a roster. You need coverage for manufacturability review, quoting, CAD/CAM programming, setup, machining, inspection, rework, and shipping. If one skilled person holds every step, the shop can open late or stall on day one. The target is a workflow that can support the Year 1 model volume of 7,300 units.

One clean handoff can keep the first jobs moving. Without it, quotes slow down, machines wait, and rework backs up the schedule.

Define the Job Flow Before Opening

Before launch, assign who writes travelers, who approves setups, and who clears inspection and shipping. Map each handoff and name a backup for every critical step. That is what turns headcount into day-one output. If shift coverage is thin, a sick day or a late program can stop the shop.

Document travelers for every part.

Assign CAD/CAM and setup owners.

Test inspection and rework handoffs.

Verify shipping closes the order loop.

Run a sample job through the full process before opening so the team can find bottlenecks early. If the workflow breaks in setup or inspection, first revenue slips even when the machines are ready.

5

Customer Pipeline And Quote-To-Production Readiness

Customer Pipeline Ready

This launch driver is the first revenue signal. A shop can have machines on the floor and still miss day-one sales if it does not start with a defined customer list, target industries, a quote template, sample capabilities, and a follow-up process. That turns machine proof and inspection proof into paid orders, not just test cuts.

The main risk is opening with capacity but no qualified work. If the quote package is weak or follow-up is slow, cash burns while the shop waits for RFQs. Early outreach to local manufacturers, overflow shops, and engineering firms should be in motion before opening so test production can move faster into paid orders.

Build the quote pipeline now

Start with a short list of target industries and named prospects, then match each one to a clear capability sheet and quote form. Keep follow-up timing, sample delivery, and quote ownership documented so leads do not stall. The goal is simple: make it easy to ask for work and easy to say yes.

Schedule local manufacturer outreach.

Book overflow shop conversations.

Activate engineering firm referrals.

Finish the quote package setup.

Show sample parts and tolerances.

Do this only after proven machine and inspection capability are in place, so the first quotes match what the shop can actually hold, inspect, and ship.