What do you need to start a sustainable laundry detergent business?

To start a Sustainable Laundry Detergent business, you need a tested formula, stable batch process, compliant labels, proven eco-friendly claims, reliable suppliers, packaging, insurance, sales channels, and fulfillment readiness; see How Is The Growth Of Sustainable Laundry Detergent Reflecting In Your Business Success? for the operating link between production and results. In the first-year planning case, 25,000 units across 3 initial SKUs generate $476,000, or about $19.04 per unit.

Launch Must-Haves

Prove cleaning performance before packaging spend

Lock repeatable batch records and quality checks

Prepare label files and Safety Data Sheet needs

Substantiate biodegradable and plastic-free claims

Launch Sequence

Test formula, then review claims

Set suppliers, packaging, and insurance

Run pilot production before full launch

Check ecommerce or wholesale order flow

How do you get first customers for sustainable laundry detergent?

First customers for Sustainable Laundry Detergent should come from channels that can absorb pilot inventory fast: ecommerce preorders, subscription bundles, local refill shops, zero-waste retailers, farmers markets, sustainability communities, and small wholesale accounts. For launch cost context, see How Much Does It Cost To Open And Launch Your Sustainable Laundry Detergent Business? and keep the first offer tight: $18 liquid, $22 pods, and $15 delicates, with Year 1 inventory matched to 25,000 units instead of a national rollout.

Fast first-sale channels

Ecommerce preorders test demand quickly

Subscription bundles drive repeat orders

Local refill shops move small batches

Farmers markets give direct feedback

Ready-to-sell checks

Wait until labels are done

Have packaging ready first

Keep batch records in place

Contact retailers after reorder capacity

How long does it take to start a sustainable laundry detergent business?

Sustainable Laundry Detergent usually takes 4 to 8 months to launch, and the clock moves by sequence, not a fixed date. The biggest delays come from formulation testing, packaging sourcing, label review, contract manufacturer scheduling, and first-batch quality assurance.

Launch blockers

Unsupported green claims can stall labels.

Late bottles or pouches delay filling.

Missing labels block release.

Failed pilot batches reset timing.

What speeds it up

Small-batch production can move faster.

Contract manufacturing cuts in-house work.

Tighter controls protect quality.

XLSX Gantt Chart maps owners and deadlines.

Confirm what must be ready before accepting detergent orders

Launch readiness checklist

Use this go-live approval checklist before opening to confirm the business is ready to launch.

1Compliance

Business registration completeCritical

You need a legal entity before contracts, accounts, and permits move forward.

Insurance policies boundCritical

Active coverage helps protect the launch team, inventory, and customer orders.

Label and claims reviewedCritical

Eco claims must be supported so packaging does not create legal or refund risk.

EPA claim reviewHigh

This is required if the product makes antimicrobial or disinfecting claims.

2Formula

Launch formulas lockedCritical

The launch needs final formulas before buying bulk inputs or printing labels.

Batch testing passedCritical

Batch tests help catch performance and consistency issues before first sales.

Stability testing loggedHigh

Stability data shows whether the detergent holds up in storage and shipping.

Quality control limits setHigh

Clear QC limits reduce bad batches and customer complaints after launch.

3Suppliers

Ingredient suppliers confirmedCritical

You need stable input supply before production starts and orders arrive.

Bottles and pouches securedCritical

Primary packaging must be in hand so finished goods can be packed and shipped.

Labels and cartons approvedCritical

Approved packaging avoids delays, waste, and relabeling costs at launch.

Backup vendors identifiedMedium

Backup sources lower the risk of shortages when a supplier slips or runs out.

4Production

Small-batch site readyCritical

A working production site is needed before the first launch batch is made.

Equipment installed and testedCritical

Installed equipment reduces startup delays and bad output during first runs.

Storage and fulfillment flow setHigh

Clear flow helps move goods from production to pick, pack, and ship.

Waste handling plan readyMedium

A waste plan keeps the site cleaner and lowers compliance risk.

5Channels

E-commerce checkout testedCritical

Customers need a working path to buy before marketing spend ramps up.

Subscription flow worksHigh

Recurring orders matter if the launch plan includes refill or repeat sales.

Refill retail outreach readyMedium

Refill stores can add volume, but only if the pitch and terms are ready.

Small wholesale offer setHigh

A simple wholesale offer helps turn interest into first purchase orders.

6Cash

Year 1 cash runway checkedCritical

The model shows a minimum cash need of $1.139M in Month 2, so runway is key.

Production and QC coverage setCritical

Production and quality control need named owners before the first batch ships.

Customer service coverage setHigh

Fast support keeps early orders, returns, and product questions from piling up.

Go-live signoff approvedCritical

Final signoff should confirm formula, labels, vendors, batch records, and first sales path.

Want the six launch drivers in one view?

1Formula Fit

Pilot pass

A stable formula that cleans well cuts refunds, supports repeat use, and improves first-customer reviews.

2Claim Validation

Label ok

Written support for labels and claims avoids relabeling and keeps retailer talks cleaner.

3Supply Ready

4-8 mo

Confirmed ingredients, packaging, and backup vendors keep the first batch from slipping.

4Production QC

QC set

A set batch process and quality checks prevent inconsistent runs and shipment holds.

5Channel Launch

25K units

Live checkout or preorder flow turns 25K units into demand signals before more inventory is built.

6Launch Economics

$476K

A cash and reorder model keeps launch spend aligned with the 25K-unit first-year plan.

Formula Readiness And Product Performance

Formula Readiness

If the detergent does not clean well, stay stable, and work in common washers, the launch slips fast. This is the first proof that the product can sell and be used again without refunds or complaints. A weak formula also breaks the sustainability promise, because buyers will not stay with a “green” product that underperforms on laundry day.

The launch gate is a tested pilot batch with performance checks, stability checks, scent or unscented decisions, and packaging compatibility. One bad bottle fit, separation issue, or residue problem can turn into returns, relabeling, and delayed first shipments.

Test Before You Print

Run small batches first and document results by wash type, temperature, and storage time. Tie each formula version to the ingredient supplier and production method so a late change does not reset the whole launch plan. If rework piles up, it also delays the batch process behind the modeled quality control load of 9% for liquid and delicates and 11% for pods.

Hold packaging until the formula passes. That keeps you from paying for cartons, labels, and bottles before the product is ready. Formula failure is the costly one here, because it can drive refund risk, weak reviews, and repeat-use complaints on day one.

Check common washers first.

Verify stability before printing.

Confirm packaging compatibility early.

1

Compliance And Claim Validation

Compliance Before Print

For a sustainable laundry detergent, label claims can make or break launch timing. Before packaging is printed, every eco claim, ingredient disclosure, and Safety Data Sheet must match the product page and the carton. If the claims are not supported in writing, relabeling can delay opening and block first shipments.

Green claims need care under Federal Trade Commission Green Guides principles, and any disinfecting or antimicrobial claim can trigger United States Environmental Protection Agency pesticide registration issues. The readiness test is simple: each claim on the package and site has written backup. No backup, no launch.

Document Every Claim

Build the launch file before labels go to print. Keep a claim matrix with the exact words used on the carton, product page, and retailer sheet, then tie each one to supplier specs, test results, or regulatory support. That is what keeps the opening date real.

Assign one owner to review ingredient disclosures, Safety Data Sheet needs, and any environmental language. If the product may ever be marketed as disinfecting or antimicrobial, pause and check whether EPA rules apply. One weak claim can force a full reprint and push first revenue back.

Match label and web copy exactly

Save written proof for each claim

Review EPA risk before launch

Clear claims with retailers early

Print only after final sign-off

2

Supplier And Packaging Readiness

Supplier and Packaging Readiness

Opening date depends on materials being real, in hand, and on time. For a sustainable laundry detergent launch, that means confirmed supply for plant-derived ingredients, fragrance or unscented inputs, enzymes if used, plus bottles or pouches, labels, cartons, and backup vendors. If packaging slips behind production, the plant can be ready but the business still can’t ship.

Here’s the quick math: unit packaging and carton cost is $0.33 for liquid detergent, $0.38 for pods film and carton, and $0.28 for delicates packaging and carton. The launch signal is simple: minimum order sizes, lead times, reorder triggers, and first-batch delivery dates are all documented and approved. That cuts stockout risk and makes first shipments cleaner.

Lock Materials Before Production

Do the supplier check before you print or schedule the run. Verify each input against the first batch plan: ingredient specs, packaging format, carton counts, and backup sources. Then map the longest lead time, not the shortest one, because one late pouch or label can push the whole opening date.

Use a simple launch sheet with vendor name, minimum order, lead time, reorder point, and first delivery date. If the packaging arrives after the production slot, cash gets tied up and day-one inventory goes out late. One clean rule: no materials, no launch.

Confirm all core inputs in writing.

Check lead times against launch date.

Set reorder triggers before first run.

Keep one backup vendor ready.

Match packaging delivery to production.

3

Production Capacity And Quality Control

Batch Process and QC

Before selling, you have to choose between in-house small-batch production and a contract manufacturer. That choice sets the launch date, because you need a confirmed batch process, quality control steps, batch records, storage space, packaging flow, and fulfillment timing before day one.

Quality control and batch testing are real launch costs, not afterthoughts: 9% of revenue for liquid detergent and delicates, and 11% for pods. If batches vary or co-packer slots slip, you get shipment holds, slower first sales, and weak customer trust. One clean rule: no batch proof, no launch.

Lock Release Rules Early

Write the batch spec, test steps, and release sign-off before you print labels or buy freight. Tie the process to the packaging flow and storage plan so finished goods can move from production to shelves or outbound shipping without sitting idle.

Confirm batch size and target fill weight.

Assign lot coding and record keeping.

Book co-packer time early.

Test packaging compatibility first.

Set hold-and-release checks in writing.

What this hides: if the first batch fails QC, you lose time on rework and can miss the first revenue window. A tight process protects reliable inventory and cuts the odds of shipment holds at launch.

4

Sales Channel Activation And First Orders

Sales Channel Activation

A launch only counts if you have a working path to sell on day one. For this detergent line, that can be a live ecommerce checkout, preorder flow, subscription offer, refill-store pitch, marketplace listing, or a small wholesale agreement. Without one of those, pilot inventory has nowhere to go, and opening slips from “ready to produce” to “waiting for demand.”

Channel choice also drives inventory timing. Year 1 assumes 25,000 total units, with early prices at $18 for liquid detergent, $22 for pods, and $15 for delicates. If you build stock before demand is visible, cash gets tied up and reorder planning gets messy. First revenue should come from pilot inventory through ecommerce, local refill stores, zero-waste retailers, or subscription preorders.

Test the first order path

Before buying the full batch, confirm one path from product page to paid order, then test how each SKU moves. The readiness check is simple: a customer can see the offer, pay, and receive clear shipping or pickup terms. If retail is the route, get a signed small wholesale agreement or store acceptance before you print too much packaging.

Confirm one live checkout.

Match SKU mix to channel demand.

Set the first reorder trigger.

Keep one backup sales channel.

What this hides is timing risk. If marketplace approval, retailer onboarding, or preorder setup runs late, you can have product ready but no way to sell it. That delays first cash, slows customer feedback, and makes the next production run harder to size.

5

Launch Economics And Inventory Planning

Inventory and Cash Plan

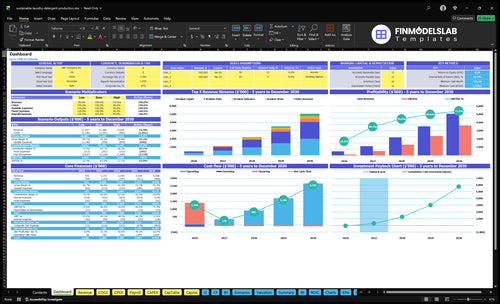

This driver decides whether you can open with enough stock and enough cash, not just a finished product. The Year 1 plan is 25,000 units and $476,000 in revenue: 15,000 liquid units at $18, 8,000 pods at $22, and 2,000 delicates units at $15.

Here’s the quick math: if one SKU moves slowly, cash gets trapped and reorder timing slips. Year 2 rises to 58,000 units and $1,118,500, so the launch model has to tie batch size, channel margin, launch spend, staffing, and cash runway together. That lowers stockouts and emergency production runs.

Lock Reorders Before First Sales

Before opening, set the first-batch mix and the reorder trigger for each SKU. Tie the launch plan to the 15,000 / 8,000 / 2,000 unit mix, then set a cash floor so slow movers do not crowd out the next run. If the model does not show when to reorder, day-one sales can still stall the next shipment.