What do you need to start a textile manufacturing business?

To start a Textile Manufacturing business, validate demand for specific fabrics before you sign a lease, then line up the space, permits, machinery, suppliers, operators, quality checks, and sales pipeline. For launch sizing, model 5,100 Year 1 units and about $162 million in revenue; here’s the quick math: $162,000,000 / 5,100 = about $31,765 per unit, then test that against What Is The Current Growth Trajectory Of Your Textile Manufacturing Business?.

Launch basics

Validate demand before leasing space

Secure power, ventilation, loading, and storage

Plan water and wastewater handling

Match machinery to fabric type

Operating needs

Lock yarn, fiber, dye, and trim vendors

Verify zoning, fire review, OSHA, and environmental items

Hire trained operators and quality control staff

Build sample approval and sales pipeline

How do you get customers for textile manufacturing?

Get customers by selling approved samples to B2B buyers before full launch: apparel brands, cut-and-sew manufacturers, wholesalers, private-label companies, local designers, and fabric distributors. Use the first order to prove sample approval, minimum order quantities, fabric specs, lead times, quality tolerances, and reorder terms; if you need the setup context, see How Much Does It Cost To Open, Start, Launch Your Textile Manufacturing Business?.

Year 1 should read like a sales plan: 5,100 units total, split across 1,200 Cotton Twill, 1,500 Jersey Knit, 800 Organic Canvas, 700 Performance Blend, and 900 Recycled Fleece.

First buyers

Target apparel brands first

Sell to cut-and-sew manufacturers

Approach wholesalers and distributors

Pitch private-label and local designers

What closes orders

Approved samples beat vague capacity

Set MOQ and fabric specs

State lead times and tolerances

Show reliable delivery and capacity proof

How do you know if a textile factory is ready to open?

A Textile Manufacturing factory is ready to open when the plant, machines, people, materials, compliance, and customers can work together without daily firefighting. That means utilities have passed, machinery is commissioned, operators are trained, vendors are scheduled, samples are approved, the defect process is active, and maintenance is set. If supplier onboarding or equipment commissioning drags past plan by 14+ days, first revenue usually slips.

Operational gates

Utilities passed and stable

Machinery commissioned and tested

Operators trained on shifts

Maintenance plan in place

Risk checks

Fire and safety review done

Environmental checks cleared

Samples approved before orders

Purchase orders in pipeline

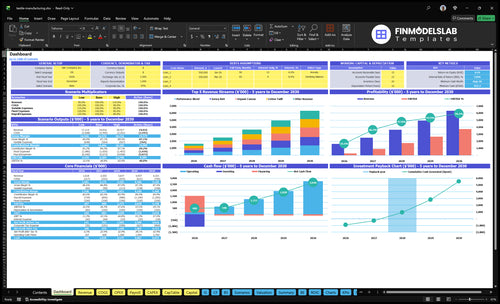

Textile Manufacturing Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Confirm the textile factory is ready before production begins

Launch readiness checklist

Use this go-live approval checklist to confirm the textile manufacturing business is ready before opening.

1Compliance

Business registration completeCritical

You need a legal entity before permits, bank accounts, and contracts move.

Fire review clearedCritical

Fire code clearance lowers shutdown risk before machines start.

OSHA plan documentedHigh

Machine guarding, PPE, and lockout rules need a written plan before launch.

Wastewater permit confirmedHigh

Needed if dyeing or finishing creates discharge.

2Facility

Industrial power confirmedCritical

Looms and dyeing lines need stable power before install and trial runs.

Layout supports flowHigh

A clean flow cuts handling time, scrap, and forklift conflicts.

Ventilation and lighting readyHigh

Good air and light support safety, inspection, and QC work.

Loading and storage readyMedium

Raw materials and finished rolls need safe receiving and hold space.

3Equipment

Looms installed and testedCritical

The core line must run before any customer order ships.

Dyeing line commissionedHigh

Needed for dyed goods and to prove stable output before launch.

Spare parts stockedMedium

Basic parts cut downtime when a loom or pump fails.

Trial run approvedCritical

Trial runs catch defects before first purchase orders ship.

4Suppliers

Fiber supply lockedCritical

Cotton, recycled fibers, and specialty inputs must be secured early.

Dyes and chemicals sourcedHigh

Safe material specs and supply timing matter before the first batch.

Packaging MOQ setMedium

Packaging must match order sizes so you don't overbuy or run out.

Delivery calendars signedHigh

On-time deliveries keep production from stopping between runs.

5Team

Operators hiredCritical

You need enough operators before the first production shift starts.

Maintenance support assignedHigh

Fast repair support protects uptime during early launch.

Quality workflow approvedCritical

Sample approval, batch tracking, and defect rules protect customer trust.

Supervisor trainedHigh

A clear shift lead keeps output, safety, and handoffs on track.

6Go-live

Year 1 model reconciledCritical

Check the model against Year 1 volume of 5,100 units before launch.

Cash trough fundedCritical

The plan needs enough cash to cover the $437k trough in Month 8.

Purchase orders in handHigh

Launch is not ready until the first customer orders are real.

Go-live signoff completeCritical

Final signoff should confirm permits, utilities, staff, vendors, and cash.

Want to see the six launch drivers that decide opening readiness?

1Facility And Utilities Readiness

6-12 mo

No power, ventilation, or loading flow means machine install slips and the opening month slows.

2Machinery Procurement And Commissioning

Machine lag

On-time commissioning keeps first batches stable and cuts rework from startup tests.

3Supplier And Material Availability

Vendor lag

Approved cotton, fiber, dyes, and packaging keep samples repeatable and first orders on schedule.

4Compliance And Safety Approvals

Approval gate

Zoning, fire, OSHA, and environmental checks can still stop production after machines arrive.

5Production Workflow And Quality

QC system

Repeatable routing, inspection, and defect handling turn first shipments into reorderable output.

6Customer Pipeline And Orders

5.1K / $1.62M

A real buyer pipeline supports 5.1K units and the $1.62M Year 1 plan.

Facility And Utilities Readiness

Facility and Utilities Ready

For a textile mill, production cannot start until the building can carry industrial power, ventilation, loading access, storage, water, fire safety, and any wastewater handling tied to finishing. The real readiness test is simple: the floor must support machine placement, safe movement, material storage, and the utility load before installation begins.

The biggest risk is signing a space that needs months of upgrades. That pushes commissioning, burns cash, and leaves the opening month weak. Site review, zoning, fire review, electrical assessment, ventilation plan, loading plan, and wastewater review, if needed, should all happen before the lease is locked.

Verify the site before the lease

Start with the lease terms, equipment specs, and local authority review. Match the utility plan to the machines you will actually install, then confirm that the floor layout allows safe traffic, raw material storage, and finished goods flow. If finishing is in scope, add a wastewater review early so you do not discover a discharge problem after signing.

Document the electrical, ventilation, loading, and fire requirements in one checklist, then assign each item to a person and due date. That keeps the buildout tied to day-one operating capacity, not just a building that looks ready. The goal is fewer commissioning delays and a cleaner opening month production run.

1

Machinery Procurement And Commissioning

Machinery Commissioning

Production starts only when the equipment is delivered, installed, calibrated, guarded, and tested, with operators trained and spare parts on hand. In textile work, that means looms, knitting, dyeing, finishing, cutting, or inspection gear must match the floor layout, power load, and ventilation plan before the first trial run.

If machines show up before utilities are ready, or after customer sampling deadlines, opening slips and first batches get pushed back. The risk is not just delay; weak setup also raises defect rates, which hurts day-one output, cash timing, and client trust.

Install in Sequence

Lock the order early: facility power, floor layout, ventilation, delivery, install, calibration, then trial runs. Have the supplier technician, maintenance routine, and spare parts confirmed before the first start-up. One missed dependency can stall the whole launch.

Here’s the quick math: the operating model already carries machine maintenance at 5% of revenue, quality control at 4%, utilities at 3%, production supervision at 2%, and waste management at 1%. If commissioning is sloppy, those costs show up fast as rework, downtime, and failed samples instead of stable output.

Confirm utility loads first.

Schedule delivery around install.

Train operators before trial runs.

Stock critical spare parts.

Document calibration and maintenance.

2

Supplier And Material Availability

Supplier Readiness

Supplier and material availability decides whether you can open on time and ship from day one. Textile production only starts when yarn, fiber, dyes, chemicals, trims, and packaging are all on hand in the right specs. A sample is not launch-ready if the same inputs can’t be reordered fast enough, because first orders depend on repeatable supply, not just a good lab sample.

Here’s the quick math: model lines show $33 for cotton-based inputs and $28 for recycled-fiber inputs. Readiness means approved vendors, minimum order quantities, lead times, payment terms, and backup options are locked before sample sign-off. If a material is slow to restock, the opening date slips, storage gets stressed, and cash runway tightens fast.

Lock Reorder Proof

Before you approve any sample, verify that every input can be bought again on the same terms and timeline. That means checking specs, minimums, lead times, and payment timing for each fiber, dye, chemical, trim, and packaging item. Also confirm machine energy assumptions where they affect ordering or production planning.

Get two vendors per critical input.

Match sample specs to reorder specs.

Check lead time against production dates.

Test packaging and storage fit.

If one core item has no backup, you can still pass a sample and miss the first shipment. That is the launch risk here: the line looks ready, but replenishment fails after the first run, which hurts customer trust and day-one operating capacity.

3

Compliance And Safety Approvals

Compliance and Safety Approvals

If zoning, business registration, or the fire inspection path is not cleared, the mill can’t open even when machines are installed. For a textile plant, this review also touches OSHA safety procedures, machine guarding, ventilation, chemical handling, wastewater review, and air-emissions review if applicable. One missed approval can stop day-one production and push cash receipts out.

The risk climbs when dyeing or finishing is added late, because that changes chemical storage, wastewater discharge, and local environmental checks. The readiness check is simple: confirm local, state, and federal requirements with the right authorities before you lock the opening date. This is verification work, not guesswork.

Verify Every Permit Path Early

Start with the facility use, machinery type, dyeing or finishing scope, chemical storage, and wastewater discharge. Those inputs decide which approvals matter and which inspections can block startup. If the scope changes after equipment is ordered, the opening plan can slip while the building waits on corrections.

Confirm zoning before buildout.

Map fire and safety inspections.

Document machine guarding checks.

Test ventilation before commissioning.

Review wastewater and emissions early.

Assign one owner to track each authority, keep approval dates in one file, and hold back opening until the last required sign-off is in hand. That keeps the launch safer and lowers the odds of a shutdown right after first orders ship.

4

Production Workflow And Quality Control

Production Workflow And Quality Control

Repeatable output is what gets a textile mill its second order, not just its first shipment. If production routing, batch tracking, inspection standards, and defect handling are not documented before launch, the team can open on paper but still miss delivery dates, ship inconsistent fabric, and lose reorder trust on day one.

The operating model needs clear SOPs, machine scheduling, maintenance routines, and sample approval steps before the first lot moves. The planned overhead here is 15% of revenue in total: machine maintenance 5%, quality control 4%, factory utilities 3%, production supervision 2%, and waste management 1%. The risk is scaling before defect data is known.

Lock the release gates before first production

Build the launch around one rule: no fabric leaves the floor without a documented finished-goods release. Start with standard operating procedures for routing, batch IDs, inspection points, and rework, then define fabric inspection rules and who approves samples. That gives the team a clear day-one path and cuts avoidable shipment holds.

Before opening, verify the handoff chain: sample approval, machine schedule, defect log, maintenance calendar, and release signoff. Train staff on what fails inspection, what gets reworked, and what gets scrapped. One clean one-liner: if the team can’t trace a batch, they can’t scale it safely.

Document routing before production starts.

Track every batch and defect.

Set inspection limits by fabric type.

Test rework and release steps.

Schedule preventive maintenance weekly.

5

Customer Pipeline And First Purchase Orders

Customer Pipeline And First Purchase Orders

Launch risk is high if you open with empty order books. For a textile mill, approved samples, spec sheets, minimum order quantities, lead times, and price quotes need to be in motion before machines are fully installed, or production turns into inventory risk. The Year 1 plan is about $162 million from 5,100 units, so the pipeline has to support real order volume, not just interest.

Start buyer outreach early with apparel brands, wholesalers, cut-and-sew partners, private-label companies, local designers, and B2B fabric distributors. One clean rule: no pipeline, no day-one revenue. If purchase order follow-up slips, cash receipts move later and production planning gets messy, which can leave the factory ready but idle.

Pre-open buyer pipeline setup

Build the buyer list before the facility is live, then send sample runs tied to clear tolerances and reorder terms. Capture each account’s MOQ, lead time, payment timing, and approval status in one tracker so sales and production can see what can ship first. That keeps sample work aligned with the actual opening date, not a hopeful one.

Use follow-up dates on every quote and sample approval. If a buyer has not signed off before equipment commissioning ends, flag that order as not ready for the first production slot. Here’s the quick test: if you cannot name the first few purchase orders, the opening plan still depends on wishful demand, not booked demand.

Start with a narrow fabric mix and prove buyer demand before adding machinery depth A lean launch can focus on samples, pilot batches, and a few B2B buyers The provided Year 1 plan totals 5,100 units, so a smaller start should still test capacity, operators, suppliers, and sample approvals

Plan for 6 to 12 months for a small to mid-sized operation The timing depends on facility condition, electrical capacity, ventilation, machinery lead time, permits, installation, trial production, and customer sample approvals A ready industrial space can shorten the path major utility upgrades can stretch it

Yes, you should verify permits and compliance before production begins Common checks include zoning, business registration, fire review, OSHA safety procedures, machine guarding, ventilation, chemical handling, and environmental items Dyeing or finishing may add wastewater or air-emissions reviews through local, state, or federal authorities

Machinery lead time and facility utility readiness are the usual blockers Power, ventilation, water, loading access, wastewater handling, machine installation, calibration, and operator training all affect the opening date If sample approvals wait until after commissioning, first purchase orders can slip even when the factory is technically ready

First revenue usually comes from approved fabric samples or reserved production capacity Target apparel brands, wholesalers, distributors, private-label companies, and cut-and-sew partners before full launch The Year 1 plan uses five product lines and about $162 million in modeled revenue, so buyer validation must start early

About the author

Arthur Grant

Startup Guide Author

Arthur Grant writes startup guide articles for Financial Models Lab, helping side-hustle builders think through realistic budget assumptions before launch. He studies common expenses, revenue drivers, and basic launch requirements, with a focus on rent, staff, equipment, and supplies. His small business startup guides also highlight the costs new founders often overlook.

Choosing a selection results in a full page refresh.