Agricultural Bank Startup Costs For A $55M Year 1 Loan Plan

You’re not just opening an office you’re preparing a regulated bank that must support $55M in Year 1 agricultural loans This agricultural bank cost breakdown covers CAPEX, pre-opening expenses, working capital, and launch readiness, while separating those costs from regulatory capital, liquidity reserves, and loan funding These figures are planning assumptions from the model, not regulatory, legal, or vendor quotes

Calculate Fuding Needs

Startup cost summary

This table breaks out agricultural bank startup costs by capex and excluded cash needs across low, base, and high cases.

Minimum cash need, liquidity buffer, and launch runway

No

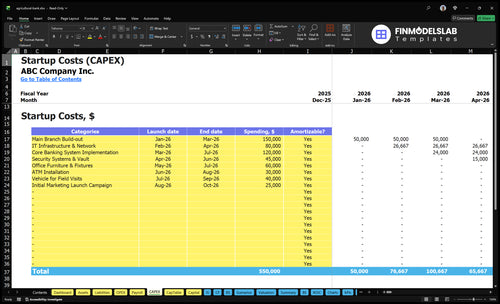

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only for opening the bank.

!

Scope note This block excludes regulatory capital, deposit liquidity, loan portfolio funding, payroll runway, working capital, debt service, and normal monthly overhead. It also leaves out recurring costs like the $12,000 monthly branch rent and the $8,000 monthly software license, plus non-CAPEX items such as inventory, marketing, and other operating expenses.

Startup cost moves with footprint, hiring, and tech. This model anchors on $33,800 fixed monthly costs, $55,417 payroll, $55M Year 1 loans, $17M other earning assets, and $58M liabilities.

Lean, Base, and Full launch options for an agricultural bank.

Scenario

Lean LaunchSponsor fit

Base LaunchRural depth

Full LaunchLaunch risk

Launch model

Administrative office with a small footprint, staged hiring, and a tighter vendor stack.

Single-market launch with one branch, core banking, compliance buildout, and the listed leadership team.

Broader branch coverage or higher-tech launch with larger implementation, more cybersecurity, more loan staff, and deeper marketing.

Typical setup

One office, limited branch services, and a lean back-office setup.

One branch with deposit, lending, and compliance functions in place.

Larger footprint, heavier systems work, and a bigger lending team.

Cost drivers

Branch shell

staged payroll

core banking

compliance fees

light marketing

One branch buildout

listed payroll

core banking

compliance

working capital

Bigger buildout

more loan staff

cybersecurity

marketing

implementation

Planning rangeCAPEX only

Lower funding bandTightest band

Mid funding bandCore build

Higher funding bandHeavy lift

Best fit

Fits sponsor-led teams testing one rural market before a wider rollout.

Fits operators with clear local demand and enough deposit depth to support steady lending.

Fits well-capitalized teams that want faster reach and can absorb a longer ramp.

!

Planning note: These ranges are researched planning assumptions, not exact vendor quotes, contractor bids, or loan offers.

How much money do you need to start an Agricultural Bank?

You don’t start an Agricultural Bank with only startup costs; you need startup cash plus bank capitalization, liquidity, deposits, and lending capacity, as explained in What Is The Primary Goal Of Agricultural Bank To Support Farmers And Agricultural Businesses?. In this model, first-year scale assumes a $55M loan portfolio, $17M other interest-earning assets, $58M liabilities, and $5M subordinated debt; Month 1 run-rate is $33,800 fixed expenses plus $55,417 listed payroll, or about $89,217 before benefits, taxes, and unlisted hires.

Startup Expenses

Cover chartering and legal setup

Build core banking systems

Prepare facility and security

Fund staffing readiness and working capital

Total Capital Need

Support $55M in planned loans

Hold $17M earning assets

Manage $58M liabilities

Include $5M subordinated debt

These figures are planning assumptions, not regulatory approval amounts.

What should an Agricultural Bank startup funding plan include?

An Agricultural Bank funding plan should tie startup cash to the launch clock, staffing, and the loan book ramp, not just the product pitch. Here’s the quick math: if Year 1 loans are $55M and grow to $215M by Year 5, while liabilities rise from $58M to $215M, sponsors need a model that shows CAPEX, pre-opening burn, interest income, interest expense, provision for loan losses, and monthly overhead working together. The deposit build and liquidity plan matter most early, because the bank has to fund growth before the loan book matures.

Startup cash needs

CAPEX for systems and setup

Pre-opening burn before revenue

Staffing for launch and credit

Monthly overhead from day one

Balance sheet drivers

$55M Year 1 loans

$215M loans by Year 5

65% to 80% Year 1 lending rates

$58M liabilities to $215M

What are the hidden costs of starting an Agricultural Bank?

The hidden cost is the pre-opening burn: $55,417 in payroll before benefits plus $33,800 in fixed monthly expenses can hit before loan income starts. Add legal revisions, regulatory response cycles, vendor due diligence, system testing, cybersecurity reviews, board setup, insurance binders, audit readiness, launch marketing, and working capital. If you want the owner-income side too, see How Much Does The Owner Of Agricultural Bank Usually Make?

Pre-launch burn

$55,417 payroll before benefits

$33,800 fixed monthly expenses

Regulatory delays extend payroll burn

Professional services run before revenue

Launch controls

Test systems before first loan

Review cybersecurity from day one

Set board governance early

Build contingency for $55M Year 1 loans

Key Takeaways

Charter work is pre-opening cost, not legal advice.

Year 1 loans target $55M across five products.

Payroll runs about $55,417 monthly before extras.

Core systems need cybersecurity and audit trails at launch.

Agricultural Bank Core Five Startup Costs

Agricultural Bank Charter Costs Startup Expense

Charter prep

For an agricultural bank, charter work is pre-opening spend, not a legal opinion. Budget for the application, counsel, regulatory consultants, board governance, policy manuals, compliance design, credit policy, BSA/AML controls, exam readiness, and organizer files so the model can support $55M in Year 1 loans.

Cost build

Here’s the quick math: the charter budget should cover the months and hours needed to get to approval and opening, plus revisions from regulator questions. Use $3,000 a month for regulatory compliance fees and $4,000 a month for professional services as anchors, then add payroll if the process runs long.

Count application and filing work

Include board and policy drafts

Add exam-readiness review time

Keep it tight

Keep counsel and consultant scope narrow, and ask for fixed fees where possible. The big mistake is treating charter work like a one-time filing; every regulator follow-up can add advisory hours and extend payroll. One clean control: tie spend to a launch checklist and freeze nonessential edits once policies are ready.

Fix scope before drafting starts

Use one owner for revisions

Track hours by deliverable

Readiness check

A charter-ready agricultural bank needs board minutes, approved policies, a credit policy for farm real estate, operating lines, equipment, livestock, and crop input loans, plus BSA/AML testing and document control. That setup supports a $55M Year 1 loan plan, but only if the compliance file is clean before opening.

Agricultural Bank Branch Setup Costs Startup Expense

Branch Space

Lease or buy the site, then split the cost right: rent and utilities are operating expense, while renovations, security, networking, furniture, fixtures, accessibility work, and records controls are startup CAPEX. Use the model anchors of $12,000 monthly rent, $2,500 utilities, and $800 for supplies and maintenance.

Buildout Scope

Estimate this cost by square feet, room count, and contractor quotes. A lean administrative office needs fewer teller stations; a base single-market branch needs customer space plus private loan offices; a full-service setup adds stronger access control and physical records controls. Farmer-facing branches usually need private advisory rooms more than high-volume teller lines.

Keep It Lean

Keep the branch sized to client flow. Start with advisory rooms and secure file storage before adding extra teller lanes. Use one-time fit-out budgets for buildout, and keep monthly anchors at $12,000 rent, $2,500 utilities, and $800 supplies and maintenance. Overbuilding space is the fastest way to burn cash.

Best Fit

If the branch serves farmers, design for private loan talks, document review, and secure file handling. High-volume teller space matters less than one-to-one lending support. That fit matters because the branch must support season-based borrowing, not a retail-heavy lobby.

Agricultural Bank Staffing Costs Startup Expense

Payroll Base

This startup cost covers executive leadership, credit leadership, agricultural loan officers, compliance, operations, finance, HR, recruiting, onboarding, training, and payroll while deposit and loan income are still ramping. The listed Year 1 roles total $665,000: CEO / President $220,000, Chief Credit Officer $160,000, Senior Ag Loan Officer $120,000, Junior Ag Loan Officer $75,000, and Operations Manager $90,000.

Runway Math

Estimate it from headcount times salary, then add payroll taxes, benefits, bonuses, and any unlisted roles. The base payroll is about $55,417 per month before those extras, so it belongs in pre-opening runway, not just ongoing operating expense. Use it to size cash needs until deposit and loan income starts covering staff costs.

Control It

The best control is phased hiring: start with the roles that support charter readiness, underwriting, and compliance, then add staff as loan volume grows. Don’t treat salary as the full cash need; taxes and benefits can move the real burn well above $665,000. Keep recruiting, onboarding, and training tight so the bank opens with the right core team.

Pre-Opening Cash

Separate this payroll from ongoing operating expense and fund it in working capital runway, because the bank may carry staff costs before deposits and loan income turn on. That cash gap is what breaks many launches, not the salary line itself.

Core Banking System Costs For Agricultural Bank Startup Expense

Core system scope

The core system should cover core processing, online and mobile banking, account opening, loan origination, credit administration, KYC (know your customer) and AML (anti-money laundering), reporting, integrations, and data conversion. For an agricultural bank, that means one platform that can handle farm real estate, operating, equipment, livestock, and crop input loans without bolting on later.

Cost split

Use the model’s $8,000 monthly software license as the recurring anchor. Then add processing, hosting, and support fees, plus capitalized implementation for setup, testing, data conversion, and vendor support. The quote should separate one-time startup cash from run-rate burn, with months of coverage and go-live work priced upfront.

Size it right

Capacity should match $55M in Year 1 loans, $58M in Year 1 liabilities, and multiple loan types. Ask how many accounts, users, and products are included before price jumps. If the system cannot support farm real estate, operating lines, equipment, livestock, and crop input loans at launch, the switch cost comes later.

Build for day one

Treat cybersecurity and audit trails as opening requirements, not later upgrades. That means role controls, log capture, alerts, exam-ready reporting, testing, and implementation support are part of launch work. If those items are missing at go-live, the bank pays twice: once to launch, and again to retrofit.

Professional Services Costs For Agricultural Bank Startup Expense

Approval support

$4,000 a month for professional services buys accounting setup, audit readiness, valuation support, vendor due diligence, financial reporting design, and board package support. Along with $1,500 insurance and $2,000 marketing, that is $7,500 per month, or $90,000 a year. These costs support launch credibility and operating controls, not charter legal work.

What it covers

Use this budget for the work that makes the bank usable on day one: clean books, board-ready reporting, insurance quotes, borrower pipeline prep, and outreach materials. Estimate it from months of coverage, vendor quotes, and the number of deliverables needed before opening. One clean rule: pay for control first, polish second.

Keep it lean

Limit spend by using one accounting firm, a fixed monthly retainer, and a short list of vendors. Separate recurring help from one-time launch work, and review insurance and marketing every month. Don’t duplicate charter legal fees inside this line. If the borrower list is thin, shift dollars to community outreach and pipeline building, not extra reports.

Pipeline math

These services should support a $55M Year 1 loan plan: $25M farm real estate, $10M operating lines, $8M equipment, $5M livestock, and $7M crop input loans. That means every report, board deck, and outreach dollar should help convert prospects into funded loans and keep approval, compliance, and lending decisions aligned.