How Much Does It Cost To Start A Bank With A $51M Year 1 Loan Plan

Bank Bundle

To start a bank in the United States, your direct startup budget can be large, but your total funding need is usually much higher because regulators expect adequate capital, liquidity, and operating runway In this plan, the first operating year includes $51M in loans, $22M in other interest-earning assets, and $63M in listed liabilities, leaving a modeled $10M funding gap before non-earning assets and startup costs Visible annual overhead includes $642K in fixed expenses and at least $132M in listed payroll, before unpriced charter work, buildout, core banking setup, recruiting, audit, and pre-opening costs Treat these figures as planning assumptions, not a universal minimum to open a bank

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a bank launch.

!

Excludes non-CAPEX funding Excludes regulatory capital, working capital, payroll runway, deposits, debt service, loan funding, inventory, and other non-capitalized pre-opening costs. Recurring $10K monthly software licensing, $5K cybersecurity, and $3K hosting stay in operating expenses.

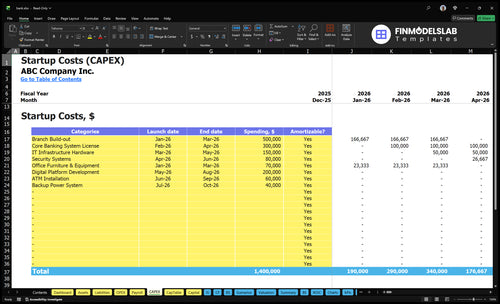

What does this Bank model screenshot show?

The screenshot shows the Bank Financial Model Template CAPEX tab: categories, launch timing, costs, and depreciation/amortization. Review assumptions.

Screenshot highlights

CAPEX and startup costs

Launch timing and amounts

Depreciation or amortization

Bank Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

How much capital do you need to start a bank?

For this Bank, don’t plan around startup costs alone; plan around total funding and regulator-acceptable capital. Based on the model, $51M in Year 1 loans plus $22M in other earning assets equals $73M, while listed liabilities total $63M, creating a $10M funding gap before non-earning assets, startup expenses, losses, liquidity, and buffers. For context, align the capital plan with What Is The Primary Goal Of Your Bank's Core Business Operations?, because the required amount changes by charter type, market, risk profile, and business plan.

Core Funding Math

$51M Year 1 loans

$22M other earning assets

$73M interest-earning assets

$10M gap before buffers

Capital Drivers

$55M Year 1 customer deposits

Checking, savings, and certificates

Liquidity and early losses

No universal minimum applies

How should bank startup financial projections be built?

Build Bank projections from the balance sheet up: start with uses of funds like CAPEX, pre-opening spend, and working capital, then model required capitalization, deposit growth, loan growth, interest income, interest expense, and profit. In Year 1, the stated portfolio is $51M in loans and $55M in deposits, with rates ranging from 65% on mortgages to 95% on consumer loans, plus $642K of fixed overhead and listed payroll of at least $132M per year. Keep regulatory assumptions visible and editable so the model can show how Bank stays funded, earns spread, and reaches profitability.

Core model blocks

Start with uses of funds

Show CAPEX and pre-opening costs

Model working capital needs

Set required capitalization

Revenue and risk drivers

Use $20M mortgages

Use $15M commercial loans

Use $5M consumer loans

Use $3M auto and $8M small business loans

What are the biggest costs to start a bank?

The biggest costs to start a Bank are the non-negotiables: regulatory formation, legal counsel, FDIC insurance application support, charter documents, compliance policies, and board materials, plus the tech stack for core banking, digital banking, payments, cybersecurity, hosting, and vendor integrations. Here’s the quick math: branch rent is $20K/month, fixed overhead totals $535K/month, and visible listed payroll is at least $132M in Year 1. Loan growth also drives capital needs, because the model starts at $51M in loans and reaches $610M by Year 5.

Startup cost drivers

Regulatory setup costs come first

Legal and charter work are core

FDIC support is not optional

Compliance policies need early spend

Operating costs

Technology is a major fixed cost

Payroll is already at least $132M

Branch rent runs $20K each month

Growth needs more capital as loans rise

Calculate Fuding Needs

Startup cost summary

This table shows bank startup CAPEX and the non-CAPEX cash need excluded from asset spend.

Highlighted CAPEX$1,230,000Base planning example

Excluded cash needs$149,372,000Outside CAPEX total

Excluded regulatory capital, deposit funding, and loan-funding cash need

No

Bank Core Five Startup Costs

Bank Charter And Regulatory Formation Startup Expense

Charter Filing Costs

This budget covers counsel, regulatory consultants, organizers, charter application work, Federal Deposit Insurance Corporation deposit insurance support, policies, board packs, and compliance planning for either a state banking department or the Office of the Comptroller of the Currency path. Approval is not guaranteed, so spend should be staged around filing milestones.

Cost Inputs

Size it from the number of filing rounds, board meetings, policy drafts, and consultant hours, plus the months of support needed through review. Tie the budget to the capital plan, deposit plan, and Year 1 model: $73M in interest-earning assets and $63M in listed liabilities mean the launch work has to fit the balance sheet.

Count every draft and resubmission

Price advisor hours by scope

Map work to filing stages

Keep It Tight

Pick the charter path early and keep one owner on the draft set, or rework will drive fees up fast. Use the same facts across counsel, consultants, and board materials, and do not let the deposit model drift away from the filing package.

Freeze assumptions before drafting

Reuse board and policy templates

Track changes in one log

Launch Readiness

Treat this as a launch gate, not a sunk cost. The formation budget should be high enough to support insured-deposit readiness, but still anchored to capital and funding plans for a bank with $73M in interest-earning assets and $63M in liabilities.

Core Banking Technology And Cybersecurity Startup Expense

Core Stack

Core banking tech has two buckets: one-time setup for core processing, online and mobile banking, payments links, vendor integration, and testing; plus recurring spend for licenses and hosting. The recurring floor is about $18K/month, made up of $10K software, $5K cybersecurity, and $3K data hosting.

Fee Load

Payment processing is the swing cost. Model fees at 20% in Year 1, then 18%, 15%, 12%, and 10%. Keep transaction fees separate from fixed tech spend so you can see the real cost of each channel and product.

Track volume by payment type

Stress-test fee compression

Separate fixed and variable costs

Build Smart

Cut setup cost by phasing features, testing in one market, and pushing noncritical tools to later releases. Don’t trim cybersecurity or testing. The common mistake is paying for custom work before transaction volume proves the model.

Launch core features first

Use standard integrations

Delay nice-to-haves

Delay Risk

Implementation delays are a cash trap. If go-live slips, you still pay vendors, hosting, and project teams before revenue starts. Build extra runway for overlap between installation and launch, because this cost often shows up after the budget is approved.

Branch Buildout, Office, And Security Startup Expense

What It Covers

This is the one-time buildout CAPEX: leasehold work, teller stations, secure cash handling, vault or safe gear, surveillance, access control, signage, furniture, ATMs if used, telecom, and customer service space. Keep it separate from $20K/month rent, payroll, deposits, and regulatory capital. One clean question drives the budget: one branch, office-led, digital-first, or branch-plus-digital?

How To Estimate It

Build the number from vendor quotes and room count: tenant improvements, security gear, furniture, telecom, and any ATM install. Then add recurring facility costs separately: $25K/month for utilities and $1K/month for office supplies. The estimate should show what is one-time and what repeats, so launch cash needs don’t get mixed with monthly run rate.

Keep It Lean

Don’t overbuild for a network you are not opening. Start with the smallest footprint that still handles cash safely and supports customers well. Ask for modular furniture, phased signage, and security equipment sized to real traffic. If the plan is digital-first, trim lobby space and teller count; if it is branch-plus-digital, spend where service and control matter most.

Fit To Launch Model

Make the scale explicit in the launch budget. A single branch needs different buildout than an office-led or digital-first setup, and the $20K/month rent figure alone does not justify a full branch network. Keep the fit-out line separate from rent, payroll, regulatory capital, and deposits so the cash plan stays honest.

Staffing Readiness And Pre-Opening Payroll Startup Expense

Payroll Burn

Before revenue ramps, the visible Year 1 team already totals $1.32M/year, or about $110K/month: CEO $250K, Head of Lending $180K, 3 Financial Advisors at $90K each, 4 Loan Officers at $80K each, and 3 IT staff at $100K each. That is base pay only, before benefits, taxes, recruiting, or branch hires.

Visible Roles

The visible roles still miss finance, compliance, operations, recruiting, background checks, training, and branch staff. Budget by headcount, start date, and months of coverage. At $110K/month, every pre-opening month adds real cash burn, so a delayed launch needs more runway even if the opening team looks small on paper.

Hiring Costs

One-time hiring and training belong in a separate launch budget, not inside ongoing payroll. That covers recruiter fees, screening, onboarding, and first-week training before the first account opens. Keeping them separate makes the runway math clean and avoids hiding startup cash needs inside normal salary expense.

Runway Gap

Payroll starts before revenue does. The cash test is simple: months of runway times $110K, then add the missing roles and employer costs. If the full team comes on early, the opening budget can jump fast, so finance should tie start dates to the hiring plan instead of assuming revenue will cover payroll right away.

Compliance, Insurance, Audit, And Launch Readiness Startup Expense

Launch Readiness

This spend covers policies, Bank Secrecy Act and anti-money laundering (BSA/AML) readiness, risk rules, and the first control tests. For launch, the recurring base is $8K/month in regulatory compliance fees plus $4K/month in insurance, or $12K/month before one-time setup work.

What It Covers

Budget for internal audit setup, accounting systems, vendor due diligence, marketing launch, and community outreach. The first check is simple: monthly run-rate × launch months, plus the cost of policy writing, staff testing, and vendor reviews. This is a launch buffer, not the full lifetime compliance load.

How To Keep It Tight

Keep vendors narrow, test controls early, and phase marketing so spend matches launch timing. Marketing and business development are modeled at 80% in Year 1, then fall to 20% by Year 5, so don’t lock in year-one burn too fast. The main mistake is overbuying tools before policies and reviews are working.

Cost Signal

Here’s the quick math: $12K/month recurring equals $144K/year before setup, staff time, and launch testing. That makes this a meaningful early cash item, but still smaller than core infrastructure and payroll. The decision is whether launch timing and client volume justify carrying that fixed base now.

Compare 3 Startup Cost Scenarios

Scenario table

Costs rise fast as the bank moves from charter work to a live branch and then to a bigger branch-plus-digital build. Deposits, lending, compliance, staffing, and liquidity all add up, so the launch model must match the funding plan.

Lean, Base, and Full bank launch cost comparison

Scenario

Lean LaunchOrganizing stage

Base LaunchCommunity bank setup

Full LaunchBranch plus digital

Launch model

Lean Launch focuses on charter work, policy drafting, and early model validation before a full branch opens.

Base Launch adds one operating branch or office, core banking setup, and a full launch team.

Full Launch adds deeper staffing, a stronger digital stack, and a larger branch buildout.

Typical setup

It uses a small office, limited staff, and basic compliance prep.

It includes cybersecurity, compliance readiness, and working capital for the first operating cycle.

It also assumes more vendor integrations, more liquidity, and a larger capital plan.

Cost drivers

charter work

organizer costs

policy drafting

minimal office setup

model validation

branch lease

core banking system

cybersecurity

leadership team

working capital

branch buildout

digital platform

added staff

vendor integrations

liquidity capital

Planning rangeCAPEX only

$2M - $5MLowest capital

$5M - $12MCore launch

$12M - $25MLargest plan

Best fit

Best for founders testing the bank thesis and funding path before scaling.

Best for a bank ready to serve customers with one main location and a full control stack.

Best for teams aiming to scale across branch and digital channels from day one.

!

Planning note: These ranges are researched planning assumptions from the model, not exact quotes or vendor bids.

Opening a bank requires more than direct startup expenses In this plan, visible first-year overhead includes $642K in fixed costs and at least $132M in listed payroll, before charter work, buildout, technology implementation, and pre-opening costs The balance sheet plan also includes $51M in Year 1 loans and $22M in other earning assets

Approval timing depends on the charter path, regulator review, organizer readiness, business plan quality, and capitalization This outline does not assume a fixed approval period The planning issue is cash burn during the startup period: fixed overhead is modeled at $535K per month, and visible payroll is at least $110K per month once listed roles are active

Deposits are funding for banking operations, not founder startup capital The Year 1 plan includes $25M in checking deposits, $20M in savings deposits, and $10M in certificates of deposit Those balances support lending and liquidity, but organizers still need startup funds, regulatory capital, working capital, and cash for pre-opening expenses

Separate implementation costs from monthly operating costs The model includes recurring software licensing at $10K per month, cybersecurity at $5K per month, and data center hosting at $3K per month A full budget should also price core processing setup, digital banking, payments connectivity, vendor integrations, testing, compliance systems, and capitalized software work

Not every new bank needs a full retail branch network, but the operating model must match the charter plan, customer strategy, and regulator expectations This plan includes branch rent at $20K per month, plus utilities of $25K and office supplies of $1K A digital-first plan still needs technology, cybersecurity, compliance, staffing, and working capital

About the author

Dennis Coleman

Small Business Consultant

Dennis Coleman is a small business consultant who writes for Financial Models Lab about everyday business finance and business plan basics. He helps readers compare business ideas by showing how small businesses really operate day to day, from realistic expenses to practical cash flow assumptions. Dennis focuses on building a basic plan before investing money, giving entrepreneurs clear, credible guidance they can use to make smarter decisions.

Choosing a selection results in a full page refresh.