Car Leasing Startup Costs: Plan for a $23M Year 1 Fleet

It costs about $260M in first-year funded assets to start the car leasing business described in this plan, before state-specific licenses, deposits, and any founder-funded losses The core budget is $230M for lease assets across standard, premium, commercial, used, and specialty vehicles, plus $30M held in cash equivalents, short-term investments, Treasury bills, corporate deposits, and money market funds The plan uses $200M of debt funding in Year 1, so the remaining funding gap is about $60M before timing reserves and launch friction Monthly fixed overhead starts at $13,800, and Year 1 payroll shown in the model is $570,000

Estimate Startup Costs with Calculator

Startup Cost Snapshot

Estimates capitalized startup assets only for a car leasing launch.

!

CAPEX only Covers capitalized startup assets only. Excludes working capital, payroll runway, refundable deposits, inventory runway, marketing runway, debt service, insurance premiums, legal fees, and other operating costs. If vehicles are financed, debt service and cash reserve needs sit outside CAPEX.

Calculate Fuding Needs

Startup cost summary

This table splits car-leasing startup spend into build costs and excluded cash needs across low, base, and high planning cases.

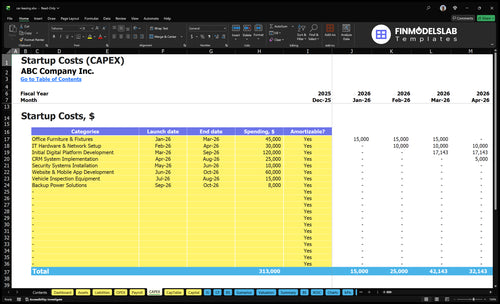

This Car Leasing Financial Model Template tab shows CAPEX, startup costs, timing, amounts, and depreciation or amortization—review assumptions now.

Key screenshot highlights

Vehicle and setup assets

Legal, insurance, software

Year 1 to 5 checks

Compare 3 Startup Cost Scenarios

Launch cost scenarios

Car leasing costs change fast with fleet size, funding mix, and reserves. Lean uses a small financed rollout, while Full assumes a larger asset-backed build with more staff and software depth.

Lean, Base, and Full launch paths for a car leasing business.

Scenario

Lean LaunchProof-of-demand

Base LaunchLocal operator

Full LaunchLarger asset-backed launch

Launch model

Start with a small, financed fleet and a narrow service area.

Run the researched case with a balanced mix of leased assets, liquid assets, and operating staff.

Scale the fleet mix, team, software, insurance, and reserves above the base case.

Typical setup

Use a small office, basic software, and tight working capital for one or two vehicle types.

Plan around $230M Year 1 lease assets, $30M liquid earning assets, $200M liabilities, and $13,800 monthly fixed overhead.

Add broader vehicle classes, deeper systems, more staff, and a larger cash cushion.

Cost drivers

Financed fleet

small office

basic software

minimal staff

tight reserves

Lease asset mix

liability funding

$13,800 overhead

$570,000 payroll

core software

Bigger fleet

more staff

deeper software

higher insurance

larger reserves

Planning rangeCAPEX only

$2M - $10MLower cash

$230M - $260MCore case

$300M - $450MScale build

Best fit

Fits proof-of-demand teams testing one market before they scale.

Fits local operators building a standard market launch with enough runway to absorb early losses.

Fits larger asset-backed launches and proof-backed operators ready for faster expansion.

!

Planning note: These scenario ranges are researched planning assumptions, not exact vendor quotes or loan offers.

How much does an initial car leasing fleet cost?

For Car Leasing, the clean planning anchor is about $230M in Year 1 fleet acquisition. A workable mix is $120M standard vehicles, $50M commercial fleet leases, $30M premium vehicles, $20M used vehicles, and $10M specialty vehicles. Buying outright pushes those assets into CAPEX and needs more equity, because down payments, titles, taxes, registration, interest, reserves, and lender covenants matter more than sticker price, and lease structures lower upfront cash but add monthly obligations and residual-value risk.

Fleet mix

$120M standard vehicles

$50M commercial fleet leases

$30M premium vehicles

$20M used vehicles

Cost drivers

$10M specialty vehicles

Model titles and taxes separately

Budget inspection and reconditioning

Count readiness costs beyond price

What hidden costs should car leasing founders budget for?

If you're launching Car Leasing, budget for cash costs that hit before they feel like capital spending (CAPEX). The core monthly model adds up fast: $1,200 insurance, $1,000 legal and compliance, $1,800 core software, $1,500 marketing tools, and $1,500 audit and accounting fees, or about $7,000/month before staff, lot costs, or repossession setup. Year 1 also carries 60% sales commissions and referral fees plus 30% digital platform transaction fees, so the funding need is bigger than the capex list alone; see How Much Does The Owner Of Car Leasing Business Typically Make Per Year? for the revenue side.

Day-one cash hits

Insurance deposits and coverage

$1,000 legal and compliance retainer

Licensing and lease document delays

Payment setup and underwriting tools

Launch costs that scale

$1,200 monthly general insurance

$1,800 core software subscriptions

$1,500 marketing platform subscriptions

$1,500 audit and accounting fees

Operating risks to reserve for

Reconditioning and maintenance reserves

Repossession and recovery costs

Bad debt allowance

Early payroll and idle office or lot costs

Year 1 variable fees

60% sales commissions and referrals

30% digital transaction fees

These are not all CAPEX

They raise total funding need fast

How much money do you need to start a car leasing business?

You need about $260M in first-year funding capacity to start this Car Leasing model at the researched scale, not just cash for vehicles; for demand context, see What Is The Current Growth Rate Of Car Leasing Customer Base?. Here’s the quick math: $230M lease portfolio plus $30M liquid earning assets, funded with $200M of liabilities, leaves an implied $60M equity or reserve need before operating timing.

Funding Need

$260M first-year funded assets

$230M lease portfolio

$30M liquid earning assets

$200M Year 1 liabilities

Cost Drivers

$60M implied equity or reserve need

$13,800 first-month fixed overhead

$47,500 monthly payroll from $570,000 salaries

Scale depends on fleet, financing, state rules, location, underwriting

Key Takeaways

Vehicle fleet is the largest startup cost driver.

Legal, bonds, and insurance need monthly budgets.

Office, software, and tracking add setup and run costs.

Separate capitalized assets from operating runway clearly.

Car Leasing Core Five Startup Costs

Initial Vehicle Fleet Startup Expense

Fleet Base

Owned vehicles are the biggest CAPEX item here. Use a $230M Year 1 lease asset base, split into $120M standard, $50M commercial, $30M premium, $20M used, and $10M specialty vehicles. The core math is vehicle count × average cost, then adjust for residual value and planned utilization.

Cost Stack

Build the estimate from purchase price or financing down payment, plus title, registration, taxes, inspection, reconditioning, delivery, keys, tracking hardware if capitalized, and lease-ready documents. Ask for vehicle count, new versus used mix, expected residual value, financing advance rate, and planned utilization. This sits inside the asset base, not in reserve cash.

Count units by segment

Price new and used separately

Model residual value first

Check advance rate and utilization

Trim Waste

Match purchases to signed demand, not wish lists. Used units and commercial fleets can lower cash needs, but only if residuals and upkeep still fit the lease plan. Don’t mix financing deposits with asset cost. A clean fleet schedule keeps the $230M base honest and makes lender talks much easier.

Buy to demand, not hype

Keep deposits off the asset line

Track residual risk by segment

Cash Split

Separate financing deposits and reserve accounts from the capitalized vehicle cost. That keeps the lease asset base clean and avoids double-counting cash you still control. If you store vehicles on-site, add secure parking and tracking controls; if you deliver direct, make sure title, registration, and inspection are ready before funding.

Fleet Insurance and Risk Protection Startup Expense

Core coverage

Fleet risk should cover physical damage, garage liability, general liability, workers’ compensation, and, where needed, cyber, payment risk, and errors and omissions. Use $1,200 per month as the general insurance anchor, but fleet pricing usually scales with vehicle count, vehicle value, and claims history.

Cost drivers

A $230M Year 1 lease portfolio means the carrier will look hard at the new vs. used mix, driver rules, state, deductibles, coverage limits, claims history, commercial fleet exposure, and storage location. Budget for required deposits or first-year premiums up front, then keep the monthly premium separate from operating cash.

Vehicle count drives pricing

Coverage limits change the bill

Storage location matters

Lower risk

Price the fleet by risk bucket, not one flat rate. Keep driver eligibility tight, split premium vehicles from used units, and quote commercial fleet exposure on its own. The cleanest savings come from higher deductibles and fewer claims, but don’t chase a cheap policy if it leaves gaps in garage, liability, or cyber cover.

Tighten driver approval rules

Separate vehicle classes

Review deductibles early

Prepaids vs. monthly

Put first-year premiums and carrier deposits in startup cash, not monthly overhead. Then track the ongoing $1,200 per month insurance line separately so runway stays clear. For a $230M lease base, that split matters because coverage terms, deductibles, and reserve needs can shift fast.

Software, Payments, and Operations Setup Startup Expense

Launch tech stack

Before launch, budget for lease management software, CRM, payment processing, e-signatures, accounting, underwriting workflows, website, telematics, fleet tracking, staff onboarding, and data security controls. The recurring anchor is $1,800 a month for core software plus $1,500 a month for marketing platforms. One-time setup, hardware, and integrations should be booked separately.

What drives cost

Use vendor quotes, user count, integration count, and months of coverage to size this line. The setup spend covers implementation, data migration, hardware, and connections between systems, while digital platform transaction fees run at 30% in Year 1. That fee load is variable, so keep it outside the monthly subscription bucket.

Quote each system separately

Split setup from subscriptions

Track Year 1 transaction fees

How to keep it lean

Start with standard configurations and only add integrations you need on day one. Delay custom builds until the leasing workflow is stable, and keep security controls in the first release. Also, don’t bury payroll here: Year 1 salaries of $570,000 are operating runway, not software CAPEX.

Use default workflows first

Limit custom integrations

Classify payroll correctly

Budget guardrails

Keep the recurring software base at $3,300 a month before variable fees, and treat anything tied to launch setup as a one-time startup cost. The fastest way to blow the budget is mixing subscriptions, implementation, and payroll into one bucket, which hides what you can actually cut or delay.

Licensing, Bonds, and Legal Setup Startup Expense

State setup

A US car leasing company usually needs state business registration first, then dealer or lessor registration where required. Add surety bonds, lease forms, disclosures, privacy policy, credit application language, and a repossession-process review. The cost split matters: one-time setup is separate from the $1,000 per month legal and compliance retainer.

Cost drivers

Price this from the facts that change by state and model: whether you own vehicles, broker leases, finance leases, or serve commercial fleets. Ask for filing fees, bond amount, contract review hours, data privacy review, and refresh timing. One-time legal work is quote-driven; the retainer covers ongoing questions.

State rules change the filing set

Bond needs are not uniform

Fleet model changes the review scope

Keep it lean

Use one outside lawyer for launch docs and a fixed compliance calendar for updates. That keeps the $1,000 monthly retainer on questions, while annual or state-change refreshes stay separate. Don’t reuse retail auto forms; leasing and repossession language needs a fresh review when your state, funding model, or fleet mix changes.

Watch the switch points

The biggest mistake is treating licensing as a one-and-done expense. If you start in multiple states, or move from broker to finance or owned-fleet leasing, extra registrations, bond changes, and disclosure updates can stack up fast. Keep one-time setup, monthly retainer, and refresh costs in separate lines.

Location, Lot, and Office Setup Startup Expense

Site and lot

Your launch site has two jobs: sell trust and control cars. Base monthly office cost starts at $6,000, plus $800 for utilities and office supplies. Add the lease deposit, signage, parking or storage lot, customer handoff area, furniture, computers, cameras, lighting, cleaning, and any leasehold improvements or equipment.

Cost build

Budget this as monthly rent + monthly ops + upfront fit-out. Use the lease quote for deposit, then add separate quotes for lot access, buildout, and hardware. The monthly base is $6,800 before cleaning and security. Ask one key question early: are vehicles stored on-site, at partner lots, or delivered directly?

Keep improvements off rent.

Capitalize equipment when needed.

Separate monthly and upfront costs.

Spend less

Commercial fleet leasing can need less retail frontage, but it usually needs more secure storage and tighter vehicle movement. That can cut showroom spend, but it can raise lot and logistics costs. The clean way to save is to trim front-office space only if the handoff flow still works and the storage lot stays secure.

Use partner lots when practical.

Keep camera coverage on access points.

Don’t underbuild the handoff area.

Frontage vs control

If vehicles sit on-site, the lot becomes part showroom, part control point. If they move through partner lots or direct delivery, you can shrink frontage and spend more on logistics, storage security, and customer handoff flow. Either way, make the lease terms, parking plan, and camera layout fit the vehicle path.