Cigarette Manufacturing Startup Costs for a 150,000-Unit Year 1 Launch

Cigarette Manufacturing Bundle

This US cigarette manufacturing startup cost outline covers cigarette factory CAPEX, pre-opening expenses, working capital, and total funding needs for the first operating year The researched model starts with 150,000 units, a $45000 unit sale price, $60,500 in monthly fixed expenses, and $1085 million in first-year payroll These are planning assumptions, not vendor quotes, tax advice, legal advice, or compliance guarantees

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only for a cigarette manufacturing launch, not operating cash needs.

!

Exclusions This excludes initial inventory, payroll runway, deposits, debt service, excise taxes, rent, and working capital. The model uses 3% of revenue for production equipment depreciation, about $202,500 in Year 1 on $675 million revenue, but it does not provide a vendor machinery quote.

What drives cigarette manufacturing equipment cost?

Cigarette manufacturing equipment cost is driven most by automation level, throughput, filter attachment, packing format, wrapping, conveyors, and the work needed to install and commission the line. For Cigarette Manufacturing, capacity planning should match the model’s 150,000 first-year units, 200,000 second-year units, and 350,000 fifth-year units, because extra product formats raise setup complexity even when volume grows later. Equipment is CAPEX, while maintenance readiness, spare parts, maintenance tools, and operator training can hit pre-opening expense or working capital.

Main cost drivers

Automation lifts upfront spend.

Throughput sets line size.

Filter and packing add complexity.

Wrapping and conveyors increase scope.

Budget timing

Installation and commissioning cost cash.

Spare parts protect uptime.

Training hits pre-opening spend.

More formats mean more setup.

How much money do you need to start a cigarette company?

You don’t need one universal startup number for Cigarette Manufacturing; you need a funding stack: CAPEX + pre-opening costs + working capital. In the researched first-year case, 150,000 units at $4,500 per unit equals $675 million revenue, with success tied to unit economics like What Is The Most Critical Measure Of Success For Cigarette Manufacturing?.

Funding stack

Fund facility and line capacity

Cover automation and equipment

Pay licensing and pre-opening

Carry inventory and tax timing

Operating case

Revenue: $675 million

Direct unit costs: $45 million

Manufacturing overhead: $115 million

Fixed expenses: $726,000; payroll: $10.85 million

Why build a cigarette manufacturing financial plan before funding?

Build the financial plan before funding Cigarette Manufacturing because lenders and investors need to see the cash gap before sales stabilize. Using the provided $675 million first-year revenue on 150,000 units, plus $3,000 direct cost per unit, 40% logistics and distribution, 20% sales commissions, $60,500 monthly fixed costs, and wages listed at $1,085 million, the model tests whether funding covers CAPEX, inventory, payroll, depreciation, and excise-tax timing. Here’s the quick math: direct cost is $450 million, logistics is $270 million, and commissions are $135 million, so the stated cost stack is already $855 million before fixed overhead and wages.

What lenders need

Show CAPEX and startup cash.

Map production ramp-up by month.

Model inventory and payroll timing.

Show the pre-stabilization funding gap.

What to quote

Quote the $3,000 unit cost.

Quote logistics at 40%.

Quote commissions at 20%.

Verify wages at $1,085 million.

Calculate Fuding Needs

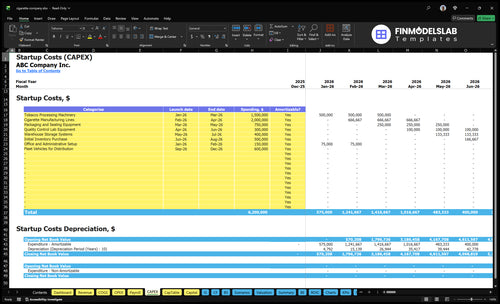

Startup cost summary

This table covers the biggest cigarette factory startup assets plus the separate opening cash reserve needed before operations stabilize.

Highlighted CAPEX$5,250,000Base planning example

Excluded cash needs$1,559,000Outside CAPEX total

Funding need$6,809,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Cigarette Manufacturing Lines

$2,000,000

Line capacity, automation, and installation scope

Yes

Tobacco Processing Machinery

$1,500,000

Processing output, spec level, and commissioning work

Yes

Packaging and Sealing Equipment

$750,000

Packaging speed, sealing specs, and setup complexity

Yes

Fleet Vehicles for Distribution

$600,000

Fleet size, vehicle type, and delivery range

Yes

Warehouse Storage Systems

$400,000

Storage capacity, racking, and handling equipment

Yes

Opening Cash Buffer

$1,559,000

Payroll, compliance, inventory, and launch timing

No

Cigarette Manufacturing Core Five Startup Costs

Cigarette Manufacturing Machinery Startup Expense

Machinery CAPEX

Cigarette manufacturing machinery is CAPEX, not monthly overhead. It covers cigarette making machines, filter attachment, production line equipment, packing, wrapping, conveyors, controls, installation, commissioning, spare parts, and maintenance setup. Size it to 150,000 first-year units and the 350,000 unit ramp by year five, with the budget shaped by capacity, automation, uptime, and line complexity.

Cost Inputs

Here’s the quick math: this line item is built from machine quotes, spare-parts depth, installation labor, and commissioning time. The research also uses a 3% revenue-based depreciation allocation, but there is no exact vendor quote yet. So the planning range should stay tied to vendor bids after throughput, packaging format, and uptime target are locked.

Set units per hour first

Price installation separately

Reserve spare parts upfront

Budget Fit

This cost sits inside the launch budget, but it should be tracked apart from facility rent, payroll, and raw materials. The machine package usually drives the biggest early cash outlay, so don’t mix it with operating expenses. One clean rule: if the line can’t support the year-one unit plan, the budget is too small.

Lean Setup

Keep the first build simple: match automation to the 150,000 unit target, avoid overbuying spare parts, and ask vendors to price installation and commissioning as separate lines. The big mistake is buying for the 350,000 unit year-five plan too early. That ties up cash before demand proves out.

Cigarette Factory Facility Startup Expense

Facility CAPEX

Factory buildout is separate from rent. Model leasehold improvements, ventilation, fire safety, humidity control, storage, loading areas, security, code compliance, and production flow as one-time CAPEX. Keep $25,000 monthly rent and $3,500 office supplies and utilities on the operating side, not inside the buildout line.

What To Budget

Use the $202,500 first-year facility CAPEX figure as a planning line, then add recurring rent, utilities, insurance, and maintenance separately. Build the estimate from lease or purchase terms, improvement quotes, and code-ready items like ventilation and fire safety. The clean rule: CAPEX changes the site; rent keeps the site open.

Quote the shell before signing.

Split buildout from monthly occupancy.

Keep compliance items fully funded.

How To Control It

Reduce spend by using an industrial space that already fits production flow, then pay only for the gap. Do not cut ventilation, fire safety, humidity control, or security. Track production utilities at 0.3% of revenue on a separate line, so the plant budget stays clean and easy to audit.

Reuse an industrial shell where possible.

Keep code items nonnegotiable.

Track utilities by cost type.

Operating Split

For year one, keep $25,000 monthly rent, $3,500 office supplies and utilities, and production utilities at 0.3% of revenue outside facility CAPEX. That split stops buildout costs from hiding in overhead and gives a clearer view of cash needed to keep the plant running.

Tobacco Manufacturer Compliance Startup Expense

Compliance Cost

Federal and state tobacco compliance can start at $12,000 per month in legal and compliance fees, plus one compliance officer at $140,000 a year. That covers license planning, U.S. Food and Drug Administration tobacco product requirements, Alcohol and Tobacco Tax and Trade Bureau permit planning, state cigarette manufacturer license work, labeling review, recordkeeping, and tax registration. Jurisdiction and distribution footprint change the budget.

Budget Inputs

Model this as fixed pre-opening spend. Use months of coverage × $12,000, then add the $140,000 salary, filing fees, and outside counsel quotes. The inputs that move the number are states, product type, and distribution channels. More states and more routes to market mean more filings, more review, and more staff time.

Count launch states first

Get written counsel quotes

Track renewal timing

Cost Control

The cleanest control is scope discipline. Start with the exact states you need, keep product files and labels ready, and avoid late changes that trigger rework. One line: fewer jurisdictions usually means lower compliance cash burn. Don’t trim recordkeeping or review; that creates delay and can raise total cost when shipments stall.

Centralize one filing set

Avoid late label changes

Keep recordkeeping current

Scope Gate

Set the first budget gate at $12,000 monthly plus the $140,000 annual compliance role, then add state license work, federal permits, and product documentation by launch scope. If you expand into more states or add new cigarette lines, re-run the estimate before you order inventory or schedule distribution. This is a budgeting model, not legal advice.

Raw Materials and Packaging Inventory Startup Expense

Inventory Cost

Treat this as inventory, not CAPEX. For first-year cigarette output, direct unit inputs are $1,500 leaf tobacco, $500 filters, $200 cigarette paper, $300 packaging, and $500 direct labor, or $3,000 per unit. At 150,000 units, direct production cost is $45 million, before adhesives, cartons, labels, cases, storage, and tax-stamp handling where applicable.

Buy Plan

Price this from supplier quotes, minimum order quantities, and months of coverage. Raw inputs move with volume, so a bigger launch batch or slower ramp can raise cash needs fast. Keep raw materials separate from machinery and facility CAPEX, because tobacco, filters, paper, packaging, and labor turn into working capital, not fixed assets.

Use supplier MOQ quotes

Stage buys with launches

Match stock to collections

Cash Need

Working capital depends on production ramp, payment terms, and distributor collections. If suppliers want cash up front and distributors pay late, you fund more inventory yourself. The fastest miss is budgeting one month of stock only; build the plan from lead times, batch sizes, and the cash gap between buying inputs and getting paid.

Track lead times by input

Watch distributor payment lag

Fund the gap, not hope

Stock Control

Separate raw material stock from finished goods and keep a tight count on leaf tobacco, filters, and paper. Storage, shrink, and tax-stamp handling can quietly push cash needs higher, so use clear reorder points and keep batch sizes aligned with the first-year 150,000-unit plan.

Staffing, Quality Control, and Insurance Startup Expense

Launch payroll

For launch, treat staffing as working capital, not plant equipment. The modeled team totals $1.085 million in year one: CEO $250,000, head of production $180,000, sales director $160,000, compliance officer $140,000, five production workers at $60,000 each, plus administrative staff at $55,000.

QC budget

Quality control runs at 0.2% of revenue, or about $135,000 in year one. Use it for QA testing, training, and release checks. Estimate it from expected revenue, then separate any lab asset or test equipment into CAPEX. That keeps the startup cash plan clean.

Base it on revenue.

Separate lab gear.

Track QA by batch.

Control spend

Keep staffing and QC lean by hiring in step with production. Put people, training, and testing in operating cash, but move any machine-linked or lab-linked spend to CAPEX. The main mistake is buying capacity before output is steady. That ties up cash fast.

Hire with volume.

Do not bundle equipment.

Review headcount monthly.

Insurance reserve

Insurance premiums are $8,000 per month, or $96,000 a year. This covers recurring protection like workers’ compensation, general liability, and product liability. Model it as operating cash, not buildout cost, because it is a live monthly expense tied to the plant’s start-up phase.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Scenario scale changes this factory's cash need fast because capex, inventory, and compliance rise with each added line. Lean keeps the footprint tight; Full adds automation, more products, and a longer runway.

Lean, Base, and Full launch cases show how factory cost rises with scale.

Scenario

Lean LaunchBest for validation

Base LaunchBest for controlled ramp

Full LaunchBest for scaled distribution

Launch model

Start with one core product line, basic equipment, and a small order book to test demand before adding more complexity.

Launch with the modeled Year 1 build: 150,000 units, a $450 unit price, $60,500 monthly fixed expense, and $1.085M payroll.

Scale into higher automation, deeper inventory, and a broader product rollout while building for wider distribution.

Typical setup

Use a smaller facility, thin inventory, fewer operators, and limited compliance support.

Run the core production line, standard packaging, and compliance coverage with a sales team sized for measured growth.

Use a larger facility, more line capacity, heavier compliance, and a longer cash runway.

Cost drivers

Basic equipment

smaller facility

lean inventory

fewer staff

lower setup overhead

Core production lines

compliance staff

$1.085M payroll

$60.5k monthly fixed costs

initial inventory

Automated lines

deeper inventory

larger facility

broader compliance

larger sales force

Planning rangeCAPEX only

$3M - $5MLower cash need

$6M - $9MMid-range funding

$10M - $15MHigher build cost

Best fit

Founders testing demand with the smallest practical launch footprint.

Founders who want the researched first-year setup and a controlled start.

Operators ready to fund a wider rollout and distribution reach from day one.

!

Planning note: These ranges are researched planning assumptions, not exact supplier quotes or lender terms.

The researched model does not give one all-in CAPEX quote, so plan total funding as machinery and facility CAPEX plus startup expenses and working capital The first-year operating case uses 150,000 units at $45000, or $675 million revenue Known monthly fixed costs are $60,500, and first-year payroll is $1085 million before inventory, licensing, and tax timing

Working capital should cover the early ramp-up period before collections are steady At a minimum, model payroll, rent, insurance, legal and compliance, inventory, and distribution costs together In this case, fixed costs are $60,500 per month, payroll averages about $90,400 per month, and direct production cost is $3000 per unit

You should validate licensing and compliance requirements before committing to major equipment purchases Federal, state, and local rules can affect facility design, recordkeeping, labeling, tax registration, and operating timing The model carries $12,000 per month for legal and compliance fees and a $140,000 compliance officer salary, but those are planning assumptions, not legal advice

The best scale is the smallest setup that can meet compliance needs, prove production quality, and serve committed buyers The researched base case starts with 150,000 units in the first year and grows the main product line to 350,000 units by the fifth year A leaner launch may reduce CAPEX, but it can raise unit cost and supply risk

CAPEX covers fixed assets like machinery, facility buildout, forklifts, storage systems, and quality-control equipment Total funding need also includes startup payroll, legal and compliance, insurance, rent, inventory, excise-tax timing, and distributor credit terms In this model, fixed expenses are $726,000 per year, payroll is $1085 million, and direct first-year production cost is $45 million

About the author

Anthony Ross

Independent Business Researcher

Anthony Ross is an independent business researcher at Financial Models Lab who writes practical guides for first-time entrepreneurs planning their first business. Focused on small business money management, he helps readers organize broad business ideas into clear planning assumptions, with straightforward revenue and profit examples that make financial thinking easier to apply.

Choosing a selection results in a full page refresh.