Commercial Bank Startup Costs For A $55M Year 1 Loan Plan

You’re planning a regulated commercial bank, so the opening budget has to separate startup expenses from the money needed to fund loans and meet capital rules This outline covers CAPEX, pre-opening costs, staffing readiness, technology, compliance setup, and working-capital planning over the first operating year, with model anchors of $55M in Year 1 loans, $60M in Year 1 liabilities, and $74K in monthly fixed expenses It does not treat regulatory capital, customer deposits, loan funding capacity, or liquidity reserves as basic startup CAPEX

Calculate Fuding Needs

Startup cost summary

This table summarizes startup CAPEX and excluded cash needs for a commercial bank, using researched ranges for buildout, systems, security, compliance, and reserve funding.

Highlighted CAPEX$590,000Base planning example

Excluded cash needs$2,883,000Outside CAPEX total

Funding need$3,473,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

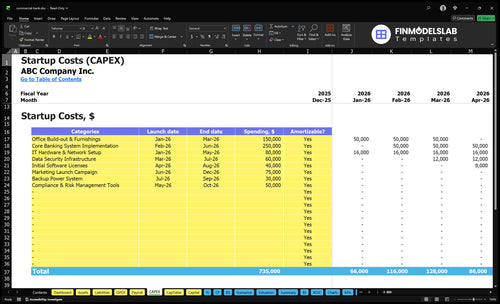

Office Build-out & Furnishings

$150,000

Branch buildout, fixtures, and workspace setup

Yes

Core Banking System Implementation

$250,000

Core processing software, configuration, and launch support

Yes

IT Hardware & Network Setup

$80,000

Servers, network gear, and user devices

Yes

Data Security Infrastructure

$60,000

Security controls, cloud setup, and backup protection

Yes

Compliance & Risk Management Tools

$50,000

Regulatory tools, monitoring, and risk reporting setup

Yes

Minimum Cash Reserve

$2,883,000

Month 60 minimum cash need and funding runway

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a commercial bank opening.

!

Exclusions This calculator covers only capitalized startup assets plus contingency. It excludes regulatory capital, working capital, payroll runway, deposits, loan portfolio funding, debt service, marketing launch spend, rent, salaries, subscriptions, and other non-capitalized pre-opening expenses.

What should the Commercial Bank startup cost model show?

Costs scale fast because fixed overhead is $74K monthly ($888K yearly) before growth, and the model already carries $55M of Year 1 loans and $60M of Year 1 liabilities.

Lean, Base, and Full launch bands for a commercial bank

Scenario

Lean LaunchOrganizer stage

Base LaunchFirst-office launch

Full LaunchFull-service buildout

Launch model

A lean organizer-stage setup supports application work and early planning before a full launch.

A base launch fits one commercial office with the core stack needed to start serving business clients.

A full launch adds deeper treasury management and more staff to support broader commercial banking activity.

Typical setup

It uses limited premises, basic IT, and only the core prep needed to get ready.

It includes core processing, cybersecurity, compliance software, and the initial executive team.

It adds more relationship managers, stronger compliance coverage, more systems integration, and extra office capacity.

Cost drivers

application work

limited premises

core planning

basic IT setup

office lease

core processing software

cybersecurity

compliance stack

initial executive team

treasury management

more relationship managers

added office capacity

stronger compliance bench

systems integration

Planning rangeCAPEX only

$1,800,000 - $2,300,000Lower cash need

$2,600,000 - $3,200,000Core launch band

$3,400,000 - $4,600,000Heavier funding

Best fit

Best for founders still in pre-launch work who want to delay a full office and full staff build.

Best for teams ready to launch a single-site commercial bank with real operating capacity.

Best for a bank aiming to scale faster with broader services and a thicker operating bench.

!

Planning note: These ranges are researched planning assumptions from the model, not exact vendor quotes or guaranteed launch costs.

How much money do you need to start a commercial bank?

You need well over $1.668M just for visible first-year overhead in a Commercial Bank, and total funding must be much larger because regulatory capital and balance-sheet capacity sit outside basic startup CAPEX; see How Is The Growth Of Client Accounts For Commercial Bank Trending Recently? for the account-growth angle. Here’s the quick math: $74K monthly fixed costs × 12 = $888K/year, plus at least $780K/year for four named leadership roles before full payroll, variable costs, compliance depth, and credit infrastructure.

Funding Floor

$888K fixed operating costs

$780K+ visible senior staffing

$1.668M+ before full buildout

Regulatory capital is separate

Balance Sheet

$55M Year 1 loans

$22M earning assets

$60M Year 1 liabilities

Needs compliance and credit capacity

What hidden costs of starting a commercial bank are often missed?

The hidden costs are people, compliance, and runway, not just branch buildout and equipment. For a Commercial Bank, the first bills can already sit at a $74K monthly fixed-cost anchor, with at least $780K a year in salaries before launch; if you want the owner-pay context, see How Much Does The Owner Of A Commercial Bank Typically Make?.

That stack also includes $10K a month for security and cloud services, $8K for compliance software, $4K for Federal Deposit Insurance Corporation premiums, and $3K for office maintenance. Missed runway hurts hiring and regulator readiness before deposits or loans scale.

Core costs

$10K security and cloud

$8K compliance software

$4K insurance premiums

$3K office maintenance

Pre-open spend

Pre-opening payroll

Executive recruiting

Compliance staffing

Audit readiness

How should founders build a commercial bank funding plan?

A Commercial Bank funding plan should start with startup costs, then tie in regulatory capital, launch timing, staffing ramp, loan growth, deposit growth, liquidity, and profit assumptions. For Year 1, anchor the model at $55M loans, $22M other earning assets, and $60M liabilities, with the listed figures pointing to about 5108M gross interest income and 1395M interest expense. Keep the model as the next step after startup-cost estimates, then run cases for slower deposits, higher funding costs, delayed lending, and added compliance hires.

Build the base case

Startup costs first

Regulatory capital next

Launch timing tied in

Staff ramp matched to volume

Stress the plan

Slower deposits cut liquidity

Higher funding costs squeeze margin

Delayed lending delays income

Compliance hires lift burn

Key Takeaways

Charter work is pre-opening expense, not capital spend.

Technology adds big recurring fees beyond launch.

Staffing readiness drives most Year 1 cash burn.

Compliance costs rise with lending and treasury.

Commercial Bank Core Five Startup Costs

Regulatory Formation And Chartering Startup Expense

Charter Prep

This is pre-opening expense, not CAPEX. It covers charter application prep, legal entity setup, board and governance papers, regulator communication, policy manuals, business plan support, and deposit insurance work where needed. Budget around $7K/month for legal and audit plus $8K/month for compliance software, with extra time if the regulator asks for revisions. No approval guarantee.

Budget Build

Build this cost from months × monthly retainer, then add drafting, filing, and response work. The model anchors are $7K monthly legal and audit plus $8K monthly regulatory compliance software, or $15K/month before spikes. One clean sentence: tighter scope means fewer billable hours.

Use charter type to size effort.

Count regulator asks as extra work.

Longer prep needs more months.

Control Spend

Keep the scope tight, answer regulator questions fast, and reuse board packs, policy drafts, and business plan tables where rules allow. The biggest waste is late management hires or a fuzzy deposit strategy, which trigger more follow-up. A clean first pass can keep the run rate near the $15K/month anchor.

Cost Drivers

Spend moves with charter type, regulator requests, management team readiness, planned loan mix, deposit strategy, and whether you open with one office or a wider footprint. More complexity means more legal review, more policy work, and more back-and-forth. This is setup cash for opening day, not an asset.

Commercial Bank Facility And Security Startup Expense

HQ Office Base

A one-office commercial bank launch usually starts near $20K per month in base occupancy costs: $15K lease, $3K utilities and maintenance, and $2K supplies plus minor IT. Add leasehold improvements, meeting rooms, secure storage, alarms, cameras, telecom, and backup connectivity if the site handles client meetings or cash.

What It Covers

This cost covers the flagship office buildout: client meeting rooms, relationship-manager offices, teller or service areas if used, secure cash handling, vault or secure storage, access control, signage, furniture, and telecom. Estimate it with square footage × finish level, security quotes, and months of pre-opening rent. The main drivers are local rent, cash-handling needs, and boardroom size.

Separate buildout from rent.

Quote security by spec.

Budget one office only.

Keep It Lean

Keep the cost down by opening with one commercial office and matching security to real cash flow risk. Don’t add retail-style features you won’t use. The best savings come from simpler finishes, fewer service counters, and shared meeting space, while still covering alarms, cameras, and backup connectivity.

Use appointment-based meetings.

Skip branch-network assumptions.

Buy backup internet on day one.

Runway Cue

A lean launch should treat facilities as pre-opening cash need, then carry $20K per month in base office overhead before any buildout, security upgrades, or staffing. That makes the office decision a runway issue: every extra month before opening adds the same fixed burn.

Risk, Compliance, Insurance, And Professional Fees Startup Expense

Core scope

After charter work, this bucket covers Bank Secrecy Act and anti-money laundering setup, risk controls, policy manuals, audit readiness, bonding, directors and officers coverage, accounting support, vendor risk reviews, penetration testing, and cybersecurity controls. Using the anchors, the run rate is about $29K per month before one-time legal setup or staff time.

Budget inputs

Start with $8K regulatory compliance software, $7K legal and audit retainer, $4K Federal Deposit Insurance Corporation premiums, and $10K data security and cloud services. Add quotes for bonding, directors and officers coverage, and penetration testing. Treat this as pre-opening expense, not capital spending.

Trim carefully

Keep cost down by phasing work to launch timing: policies, controls, and testing first, then deeper vendor reviews as activity grows. Do not trim legal review or cyber controls; exam fixes and incident response cost more than the saved monthly spend. One weak vendor can create a costly gap.

Pressure points

Cost pressure climbs fast in commercial lending, treasury management, and vendor-heavy banking because each adds controls, reviews, and testing. The $29K monthly anchor can move up if audit support, insurance, or cyber scope expands, so budget extra room when services start on day one.

Banking Technology Infrastructure Startup Expense

Core Stack

The bank tech stack starts with core processing, online banking, treasury tools, loan ops, payment links, cybersecurity, data hosting, reporting, and vendor onboarding. Budget the recurring base separately from implementation and hardware: at least $25K monthly core processing, $10K data security and cloud, and $8K compliance software, or $516K a year before support and rail fees.

What It Covers

Price it from vendor quotes, modules, and live volumes. The setup line should cover implementation support, user testing, and hardware; the monthly line should cover software, processing, data, and support. For Year 1, tie capacity to $55M of loans, treasury processing fees at 50%, and interchange fees paid at 30% so the stack fits actual activity.

Keep It Lean

Split one-time implementation from recurring spend. A common mistake is paying for treasury tools before launch. If treasury services are not live on day one, delay that module and keep the first build tight around core banking, loans, payments, and reporting. That keeps the recurring base closer to the $43K monthly anchor.

Day-One Treasury?

If treasury launches on day one, add integration, testing, and support load from the start. If not, stage it after the core stack is stable so you do not bury recurring SaaS in setup costs. That choice changes the first-year cash need, because the bank still carries the monthly processing, cloud, and compliance base.

Staffing Readiness And Pre-Opening Payroll Startup Expense

Payroll runway

For a commercial bank, staffing readiness is mostly pre-opening expense or working capital, not capital expense (CAPEX). The visible core team alone totals at least $780K a year: $250K CEO/president, $200K chief credit officer, $180K head of treasury management, and $150K senior relationship manager. That is about $65K a month before benefits and other hires.

What to load

Use headcount × salary, then add payroll taxes and benefits. Include finance, compliance, Bank Secrecy Act and anti-money laundering, operations, loan administration, client service, training, and recruiting. The key question is how many months of pre-opening coverage you need before deposits and loan income start paying the team.

Count launch roles.

Add taxes and benefits.

Set pre-open months.

How to pace it

Stage hiring around launch, not around hope. Keep credit, treasury, and compliance staffed first, then add client service and operations as onboarding starts. The usual mistake is hiring too early and funding dead payroll for months; every extra month adds about $65K before benefits.

Cash timing

Payroll cash should sit alongside facility, technology, and regulatory spend in the startup budget, because staff costs hit before revenue. If the bank opens slower than planned, the burn stays fixed while income lags. That makes payroll timing one of the fastest ways to change the launch cash need.